7. The Corporate Value Model is a useful way of valuing companies that are privately owned because it

relies on the discounting of future cash flows at an appropriate discount rate to measure the overall

value of a firm. Most of the other methods require comparative data on price, beta, dividends per share, and

of similar publicly traded firms for estimates of inputs to be used in applying the respective models.

Calculation of Citrus Glow's stock price based on the Corporate Value Model

1) Find the market value (MV) of the firm.

2) Find PV of firm’s future FCFs

3) Subtract MV of firm’s debt and preferred stock to get MV of common stock.

MV of stock = MV of Firm - MV of debt and preferred stock (if any)

Divide MV of common stock by the number of shares outstanding to get intrinsic stock price (value).

P0 = MV of common stock / # of shares

Also called the free cash flow method. Suggests the value of the entire firm equals the present value of the fir

Remember, free cash flow is the firm’s after-tax operating income less the net capital investment

where net capital investment is equal to the change in net fixed assets

FCF = NOPAT – Net capital investment

EBIT

Tax Rate

NOPAT

Change in Fixed assets

Free Cash Flow (2009)

Expected growth rate of free cash flows =

year 1

year 2

Required rate of return on equity (based on CAPM Model)

2. Comment on Lisa’s preference of the Corporate Value Model.

Based on her approach, what would Citrus Glow’s selling price per share be

if they were to issue 5 million shares?

8. Risk-fee rate (T-Bill rate)

Market Risk Premium

Beta (Average of 3 competitors' betas)

Required rate of return on equity

Cost of Debt

After-tax cost of debt

Weights

Debt

Equity

WACC

FCF in 2010

FCF in 2011

FCF in 2012

Firm Value in 2009

Debt

Equity Value

Number of shares

Price per share

9. t are privately owned because it

unt rate to measure the overall

a on price, beta, dividends per share, and earnings per share

applying the respective models.

get intrinsic stock price (value).

ire firm equals the present value of the firm’s free cash flows.

ss the net capital investment

hange in net fixed assets

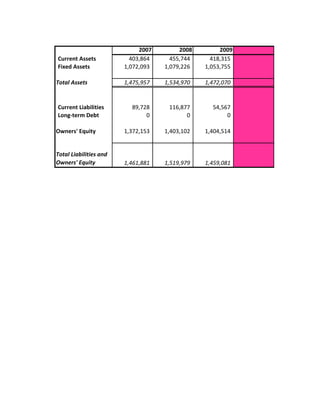

87,317

0%

87,317

(25,471)

112,788

20%

10%

APM Model)

http://english.alrroya.com/content/uae

Value Model.

e per share be

13. 2007 2008 2009

Price/Earnings 9.2 10.3 20

Price/Book 1.2 1.1 0.76

Price/Sales 3.00 1.63 1.81

Price/Cash Flow 0.11 0.13 0.06

Beta 0.42

Risk-free rate 4%

Market Risk Premium 8%

Required Rate (CAPM)= 7.78%

Number of shares to be issued 358,800

Estimated Price Per share 2.57

Total Value of Equity 922,219.17

Dan's estimate under the Price-ratio approach turns out to be between $31 and $63 with an average of $47 as compared w

Under Dan's approach the firm's value is determined in relationship with the relative valuation ratios of the firm's top

3 competitors. So it would give a more realistic value. Also, only 1-year ahead growth estimates have to be made reducing

forcasting error. However, beta and required return estimates are still required.

3. How does Lisa’s price estimate compare with Dan’s price

price-ratio models? What are the pros and cons of Dan’s preferred

14. Average Current Level

2 year

Compound

Growth

1-year ahead

Projected

Level

End of year

Estimated Value

13.2 86,592 Net Income -13.05% 75,289 991,311

1.0 1,404,514 Book Value 1.17% 1,420,980 1,449,399

2.1 699,833 Sales 1.79% 712,375 1,527,805

0.1 86,592 Cash Flow -13.05% 75,289 7,356

average of $47 as compared with Lisa's estimate of $57.91

n ratios of the firm's top

tes have to be made reducing

e compare with Dan’s price estimate based on the

and cons of Dan’s preferred approach?

16. Period

Growth

rate

Dividend

during non-

constant

growth

phase

Price at end

of non-

constant

growth

phase

2007 30% 1.95

2008 30% 2.54

2009 30% 3.30

3.30

3.30

42.36$

Dividend in Year 0 1.50$

Required Rate 7.78%

Intrinsic Value $40.46

Joe's estimate of $207.12 is the lowest of the 3. However it is much closer to Lisa's estimate of $5.298

than Dan's estimate of $2.57

4. How far off would Joe’s price estimate if he were to use a 3-stage approach with growth

assumptions of 30% for the first 3 years, followed by 20% for the next two years, and a long-term

growth assumption of 6% thereafter. Assume that the firm pays a dividend of $1.50 per share at th

end of the first year.

17. e approach with growth

o years, and a long-term

of $1.50 per share at the

18. Lisa's estimate 5.298409 based on Corporate Value Model

Dan's Estimate 2.57 based on Price ratio models

Joe's estimate $40.46 based on Dividend Discount Model

Average 16.10809

Since the estimated values are based on fairly conservative expectations a simple

average would be fine. So a offer price of around $50 per share would be reasonable. This price is

similar to the competitors' current prices.

5. Based on all three estimates and on the valuation figures for the three competitors how much pe

Glow is really worth? Explain your rationale.

19. sonable. This price is

hree competitors how much per share do you think that Citrus