Accounting Rate of Return ARR example

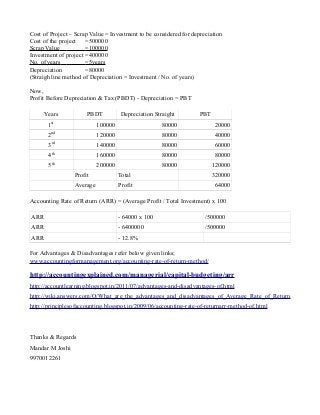

- 1. Cost of Project – Scrap Value = Investment to be considered for depreciation

Cost of the project =500000

Scrap Value =100000

Investment of project =400000

No. of years =5years

Depreciation =80000

(Straigh line method of Depreciation = Investment / No. of years)

Now,

Profit Before Depreciation & Tax (PBDT) - Depreciation = PBT

Years PBDT Depreciation Straight PBT

1st

100000 80000 20000

2nd

120000 80000 40000

3rd

140000 80000 60000

4th

160000 80000 80000

5th

200000 80000 120000

Profit Total 320000

Average Profit 64000

Accounting Rate of Return (ARR) = (Average Profit / Total Investment) x 100

ARR - 64000 x 100 /500000

ARR - 6400000 /500000

ARR - 12.8%

For Advantages & Disadvantages refer below given links;

www.accountingformanagement.org/accounting-rate-of-return-method/

http://accountingexplained.com/managerial/capital-budgeting/arr

http://accountlearning.blogspot.in/2011/07/advantages-and-disadvantages-of.html

http://wiki.answers.com/Q/What_are_the_advantages_and_disadvantages_of_Average_Rate_of_Return

http://principlesofaccounting.blogspot.in/2009/06/accounting-rate-of-returnarr-method-of.html

Thanks & Regards

Mandar M Joshi

9970012261