This document provides an overview of key financial ratios used to analyze the financial performance and health of banking institutions. It discusses ratios categorized as profitability, liquidity, asset quality, efficiency, and capital/solvency ratios. Specific ratios covered include net margin, cost-to-income, return on equity, return on assets, current ratio, non-performing loans ratio, debt-to-equity, and capital-to-risk weighted assets. The document emphasizes that analyzing multiple ratios together provides a fuller picture of a bank's financial standing than any single ratio alone.

1. THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

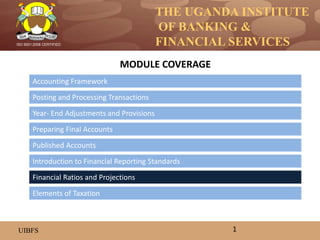

Accounting Framework

Posting and Processing Transactions

Year- End Adjustments and Provisions

Preparing Final Accounts

Introduction to Financial Reporting Standards

Published Accounts

MODULE COVERAGE

1

Financial Ratios and Projections

Elements of Taxation

2. THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

Ratio analysis for interpreting financial statements

• A ratio is a numerical value calculated by dividing one number (or a combination of

numbers) by another and it can be presented as numbers, currency value or

percentage.

• Ratios tell a more complete story of proportionate relationships between

performance variables than we can get from absolute figures in the financial

statements. It can be used to compare the risk and return relationships of firms of

different sizes. It is defined as the systematic use of ratio to interpret the financial

statements so that the strengths and weaknesses of a firm as well as its historical

performances and current final condition can be determined.

• A single ratio in itself has limited or no value. A set of ratios read in combination

will have substantial value in aiding the drawing of conclusions and eventual

decision making. Ratio analysis involves comparing one figure against another to

produce ratios, and assessing whether the ratio indicates a weakness or strength.

The comparison can be with other institutions, or for the same institution but over

different periods.

• Because Ratio Analysis is based upon accounting information, its effectiveness is

limited by the distortions which arise in financial statements due to such things as

Historical Cost Accounting and inflation. Therefore, Ratio Analysis should only be

used as a first step in financial analysis, to obtain a quick indication of a firm's

performance and to identify areas which need to be investigated further.

2

3. THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

Rationale of Ratio Analysis:

The rationale of ratio analysis lies in the fact that it makes related information

comparable. A single figure by itself has no meaning but when expressed in terms

of a related figure, it yields significant inferences, e.g if a firm’s net profit is say

100M; does it show how adequate this firm is?

The figure of net profit has to be considered in relation to other variables. How does it

stand in relation to sales? What does it represent by way of net capital employed

or return on total assets used?

In banking, the most useful financial ratios can be broadly grouped into the following

categories;

• Profitability ratios

• Liquidity ratios

• Portfolio quality ratios

• Efficiency ratios

• Capital ratios

3

4. THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

1. Profitability ratios

Apart from creditors, owners and managers of a firm are interested in the financial

soundness of the company.

The operating efficiency of a firm is ultimately determined by its profits.

Profitability ratios can be determined on the basis of either sales or investments.

Profitability ratios indicate how well an institution’s resources have been utilized to

generate income or returns.

These ratios indicate the extent of an institution’s profitability in relation to its

business size, turnover, capital and other aspects.

Profitability ratios usually include sets of items from the Income Statement and or

from Balance Sheet.

There are many profitability ratios. Here, we look at some examples;

a. Net Margin (NM)

b. Cost-to-Income Ratio (CIR)

c. Return on Equity (ROE)

d. Return on Assets (ROA)

4

5. THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

a. Net Margin (NM)

Net margin compares the net operating profit to the gross revenue or turnover. It

measures the bank’s ability to convert turnover into profit through controlling costs

and expenses.

Formula: Net profit before tax

Total turnover or gross revenue

b. Cost-to-Income Ratio (CIR)

The cost-to-income ratio is both an efficiency and profitability measure. It shows the

efficiency of a firm in minimizing costs while increasing profits. The more efficient a

bank is, the more profit it generates. The lower the cost-to-income ratio; the more

efficient and profitable the institution is running. The reverse also holds.

Formula: CIR = Total Operating Expenses

Total Operating Income

c. Return on Equity (ROE)

This is a key measure for financial performance, indicating a bank's ability to generate

earnings using shareholder capital. Over time, ROE is one of the major indicators of

the rate at which a bank creates shareholder wealth.

5

6. THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

d. Return on Assets (ROA)

This ratio presents measurement of the income the bank generates from the

utilization of all of its assets, whatever the underlying capital structure is.

A low ratio indicates an inefficient use of business assets whereas a high one means

efficient use of assets.

Formula:

Return on Assets = Net Income after taxes

Average total assets

2. Liquidity ratios

Liquidity refers to the ability of an organization to meet its obligations as and when

they fall due. It depends on the availability of cash and near cash assets in relation

to the liabilities of the organization.

When an institution fails to meet its debt obligations, its creditors can potentially place

it under liquidation.

It is therefore imperative that the management of a bank maintains appropriate

liquidity levels to enable the institution meet its obligations as they fall due.

Liquidity indicators include the following ratios

6

7. THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

a. Liquidity ratio

The liquidity ratio measures an institution’s proportion of liquid assets to the total

assets. Liquid assets are cash and assets that can easily be converted into cash. The

ratio therefore measures how easily an organization can meet its obligations such

as savings withdrawals and debt service.

Overall, the institution has to balance between holding cash or liquid assets and

putting cash into good yielding investments like the loan portfolio. The higher the

liquidity ratio, the lower the income earned by an entity and while the lower the

ratio the more likely it is for the entity to suffer liquidity problems.

Two ways of calculating the current/liquidity ratio are;

Formulae:

Liquid assets to total assets

Under this method, Liquidity ratio = Cash and near assets

Total assets

Liquid assets to total liabilities

Under this method, Liquidity ratio = Cash and near assets

Total current liabilities

7

8. THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

b. Current ratio

The current ratio compares the institution’s total current assets with its total

current liabilities. It measures the extent to which short term assets are

financed by liabilities of corresponding maturity.

If the short term or current assets are far less than the current liabilities, it

could trigger an unpleasant situation of difficulties in meeting current

liabilities as they mature.

Formula:

Current ratio = Total current assets

Total current liabilities

Quick (acid test) ratio = Total Current assets- Inventory (stock)

Total current liabilities

It is the ratio of quick assets to total liabilities. Quick assets are those current

assets that can be converted into cash immediately without diminution of

value. The current assets excluded are pre-paid expenses and inventory.

8

9. THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

3. Asset (or portfolio) quality ratios

a. Loan loss (write-off) ratio

This ratio indicates amount of loans written off (Removed from the balance sheet) as a

percentage of average portfolio during the period.

The loan loss ratio provides an indication of the past quality of the loan portfolio. Its

usefulness is strongly dependent on the institution’s write off policy.

Formula:

Loan loss ratio = Amount written off year

Average gross portfolio

b. Non Performing Loans (NPL) ratio

Non-performing loans are loans that are no longer producing sure income for the bank

because the have been classified as substandard, doubtful or loss.

Loans become non-performing when borrowers default on loan servicing for a

specified period. A smaller NPL ratio indicates a good or healthy asset quality while

a larger (or increasing) NPL ratio indicates poor assets quality.

Formula:

NPL ratio = Non-performing loans

Gross loan portfolio

9

10. THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

c. Portfolio Yield

This ratio measures how much the institution received in interest and fees during the

period relative to its average outstanding loan portfolio. Yield is the initial indicator

of a loan portfolio’s ability to generate revenue with which to cover financial and

operating expenses.

Formula;

Portfolio Yield = Income from loan portfolio (including interest and fees)

Average gross portfolio

4. Efficiency ratios

a. Cost-to Income ratio (CIR)

This was explained as a measure of both efficiency and profitability. It shows the

bank’s efficiency in minimizing costs while optimizing profits.

b. Loans to Assets ratio (LTA)

This compares the loan portfolio to the bank’s total assets. On the positive side, it

measures the efficiency of the bank in deploying its assets for optimum income

generation.

On the flip side, beyond a certain level a higher ratio indicates that a bank is highly

loaned up, negatively affecting its liquidity. The higher the ratio, the more sensitive

a bank may be to loan defaults.

10

11. THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

Formula:

LTA = Loans and advances

Total assets

Loans to Deposits ratio (LTD)

This compares the loans/ advances with the volume of customer deposits. It therefore

shows the bank’s level of efficiency in placing its deposit liabilities into high

earning assets

Formula:

Loans-to-Deposits (LTD) = Value of loans and advances

Customer deposits

5. Solvency/ capital adequacy ratios

Solvency ratios are financial indicators that show an institution’s ability and capacity to

meet its liabilities from its assets (leverage of the bank).

Solvency indicators are therefore concerned with how much an BANK owes in relation

to its asset values.

When an institution is heavily in debt and yet it continues earning a modest net

income, it incurs high interest charges which will eventually lead to illiquidity and

perhaps liquidation.

11

12. THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

a. Debt to Equity Ratio (DER)

The debt equity ratio is the simplest and best known measure of capital adequacy,

measuring the overall leveraging or gearing of the institution.

The Debt/ Equity ratio is of particular interest to lenders, regulators and depositors

because it indicates how much of a safety cushion (in the form of equity) the

institution has available to absorb losses before the depositor or lender is put at

risk.

Formula;

DER = Total liabilities

Total equity

b. Capital to Risk-weighted Assets Ratio (CRAR)

CRAR indicates the stability of a bank. A bank's capital is the net claim on the assets by

shareholders.

It is the amount that would remain if the bank’s assets were sold at their book value

and all the creditors were paid off.

A good measure of a bank's health is its CRAR, which is usually required to be above a

prescribed minimum.

12

13. THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

Formula;

CRAR = Capital

Total value of Risk weighted assets

Debt to total Capital ratio = Total debt

Total assets

It indicates the proportion of total assets financed by owners.

Interest coverage ratio = EBIT

Interest

It measures the debt servicing capacity of the firm in so far as fixed interest

on long term loans is concerned. For banks, this can either be equity(core

capital) or a combination of equity and quasi-equity (total capital)

13

Editor's Notes

ByIf all adjusting entries have been made, and a trial balance done, preparing financial statements is really just a matter of putting the trial balance amounts onto properly formatted statements.

As already discussed, financial statements prepared by most banks are;

The Balance Sheet

Income Statement (Statement of comprehensive Income)

Cash Flow Statement

Portfolio Report (optional but important)

the end of this unit, the students should be able:

Explain the end of period adjustments that are made to the various accounts.

Pass the end of period adjustments

Close off the ledger accounts

To extract the account balances after closing of the accounts

Prepare the trial balance

A moratorium on new commercial bank licenses was declared in 2004, with the passage of the Financial Institutions Act 2004 by Parliament, which established new banking institution classification guidelines, shifting the focus and modality of supervision from forensic to risk-based, and introduced robust, tight rules for management and governance of banks in Uganda.

The moratorium on new banks was lifted in July 2007. During the eighteen (18) months that followed the lifting of the moratorium, several new commercial banks were licensed. These included Kenya Commercial Bank, Equity Bank and Fina Bank, all from Kenya. Global Trust Bank and United Bank for Africa which trace their roots from Nigeria were also licensed during this period. The others were Ecobank; headquartered in Togo and Housing Finance Bank an indigenous bank.

Between 2008 and 2009, several of the existing banks went on an accelerated branch expansion either through mergers and acquisitions or through new branch openings. As of October 2010[update], there were twenty-two (22) licensed commercial banks in Uganda, with nearly four hundred (400) bank branches and a total of almost six hundred (600) ATMs.

In November 2010, Bank of Uganda directed that all commercial banks in Uganda, must raise their minimum capital to UGX 10 billion (approximately US$4.34 million) by March 2011 and to UGX 25 billion (approximately US$11 million) by March 2013. Any new commercial bank entering the Ugandan market effective November 2010 had to have a minimum capitalization of UGX 25 billion. Today (June 2012), most of the banking activity is concentrated around Kampala and other urban centers, leaving most Ugandans out of the formal financial sector.

A moratorium on new commercial bank licenses was declared in 2004, with the passage of the Financial Institutions Act 2004 by Parliament, which established new banking institution classification guidelines, shifting the focus and modality of supervision from forensic to risk-based, and introduced robust, tight rules for management and governance of banks in Uganda.

The moratorium on new banks was lifted in July 2007. During the eighteen (18) months that followed the lifting of the moratorium, several new commercial banks were licensed. These included Kenya Commercial Bank, Equity Bank and Fina Bank, all from Kenya. Global Trust Bank and United Bank for Africa which trace their roots from Nigeria were also licensed during this period. The others were Ecobank; headquartered in Togo and Housing Finance Bank an indigenous bank.

Between 2008 and 2009, several of the existing banks went on an accelerated branch expansion either through mergers and acquisitions or through new branch openings. As of October 2010[update], there were twenty-two (22) licensed commercial banks in Uganda, with nearly four hundred (400) bank branches and a total of almost six hundred (600) ATMs.

In November 2010, Bank of Uganda directed that all commercial banks in Uganda, must raise their minimum capital to UGX 10 billion (approximately US$4.34 million) by March 2011 and to UGX 25 billion (approximately US$11 million) by March 2013. Any new commercial bank entering the Ugandan market effective November 2010 had to have a minimum capitalization of UGX 25 billion. Today (June 2012), most of the banking activity is concentrated around Kampala and other urban centers, leaving most Ugandans out of the formal financial sector.

A moratorium on new commercial bank licenses was declared in 2004, with the passage of the Financial Institutions Act 2004 by Parliament, which established new banking institution classification guidelines, shifting the focus and modality of supervision from forensic to risk-based, and introduced robust, tight rules for management and governance of banks in Uganda.

The moratorium on new banks was lifted in July 2007. During the eighteen (18) months that followed the lifting of the moratorium, several new commercial banks were licensed. These included Kenya Commercial Bank, Equity Bank and Fina Bank, all from Kenya. Global Trust Bank and United Bank for Africa which trace their roots from Nigeria were also licensed during this period. The others were Ecobank; headquartered in Togo and Housing Finance Bank an indigenous bank.

Between 2008 and 2009, several of the existing banks went on an accelerated branch expansion either through mergers and acquisitions or through new branch openings. As of October 2010[update], there were twenty-two (22) licensed commercial banks in Uganda, with nearly four hundred (400) bank branches and a total of almost six hundred (600) ATMs.

In November 2010, Bank of Uganda directed that all commercial banks in Uganda, must raise their minimum capital to UGX 10 billion (approximately US$4.34 million) by March 2011 and to UGX 25 billion (approximately US$11 million) by March 2013. Any new commercial bank entering the Ugandan market effective November 2010 had to have a minimum capitalization of UGX 25 billion. Today (June 2012), most of the banking activity is concentrated around Kampala and other urban centers, leaving most Ugandans out of the formal financial sector.

A moratorium on new commercial bank licenses was declared in 2004, with the passage of the Financial Institutions Act 2004 by Parliament, which established new banking institution classification guidelines, shifting the focus and modality of supervision from forensic to risk-based, and introduced robust, tight rules for management and governance of banks in Uganda.

The moratorium on new banks was lifted in July 2007. During the eighteen (18) months that followed the lifting of the moratorium, several new commercial banks were licensed. These included Kenya Commercial Bank, Equity Bank and Fina Bank, all from Kenya. Global Trust Bank and United Bank for Africa which trace their roots from Nigeria were also licensed during this period. The others were Ecobank; headquartered in Togo and Housing Finance Bank an indigenous bank.

Between 2008 and 2009, several of the existing banks went on an accelerated branch expansion either through mergers and acquisitions or through new branch openings. As of October 2010[update], there were twenty-two (22) licensed commercial banks in Uganda, with nearly four hundred (400) bank branches and a total of almost six hundred (600) ATMs.

In November 2010, Bank of Uganda directed that all commercial banks in Uganda, must raise their minimum capital to UGX 10 billion (approximately US$4.34 million) by March 2011 and to UGX 25 billion (approximately US$11 million) by March 2013. Any new commercial bank entering the Ugandan market effective November 2010 had to have a minimum capitalization of UGX 25 billion. Today (June 2012), most of the banking activity is concentrated around Kampala and other urban centers, leaving most Ugandans out of the formal financial sector.

A moratorium on new commercial bank licenses was declared in 2004, with the passage of the Financial Institutions Act 2004 by Parliament, which established new banking institution classification guidelines, shifting the focus and modality of supervision from forensic to risk-based, and introduced robust, tight rules for management and governance of banks in Uganda.

The moratorium on new banks was lifted in July 2007. During the eighteen (18) months that followed the lifting of the moratorium, several new commercial banks were licensed. These included Kenya Commercial Bank, Equity Bank and Fina Bank, all from Kenya. Global Trust Bank and United Bank for Africa which trace their roots from Nigeria were also licensed during this period. The others were Ecobank; headquartered in Togo and Housing Finance Bank an indigenous bank.

Between 2008 and 2009, several of the existing banks went on an accelerated branch expansion either through mergers and acquisitions or through new branch openings. As of October 2010[update], there were twenty-two (22) licensed commercial banks in Uganda, with nearly four hundred (400) bank branches and a total of almost six hundred (600) ATMs.

In November 2010, Bank of Uganda directed that all commercial banks in Uganda, must raise their minimum capital to UGX 10 billion (approximately US$4.34 million) by March 2011 and to UGX 25 billion (approximately US$11 million) by March 2013. Any new commercial bank entering the Ugandan market effective November 2010 had to have a minimum capitalization of UGX 25 billion. Today (June 2012), most of the banking activity is concentrated around Kampala and other urban centers, leaving most Ugandans out of the formal financial sector.

A moratorium on new commercial bank licenses was declared in 2004, with the passage of the Financial Institutions Act 2004 by Parliament, which established new banking institution classification guidelines, shifting the focus and modality of supervision from forensic to risk-based, and introduced robust, tight rules for management and governance of banks in Uganda.

The moratorium on new banks was lifted in July 2007. During the eighteen (18) months that followed the lifting of the moratorium, several new commercial banks were licensed. These included Kenya Commercial Bank, Equity Bank and Fina Bank, all from Kenya. Global Trust Bank and United Bank for Africa which trace their roots from Nigeria were also licensed during this period. The others were Ecobank; headquartered in Togo and Housing Finance Bank an indigenous bank.

Between 2008 and 2009, several of the existing banks went on an accelerated branch expansion either through mergers and acquisitions or through new branch openings. As of October 2010[update], there were twenty-two (22) licensed commercial banks in Uganda, with nearly four hundred (400) bank branches and a total of almost six hundred (600) ATMs.

In November 2010, Bank of Uganda directed that all commercial banks in Uganda, must raise their minimum capital to UGX 10 billion (approximately US$4.34 million) by March 2011 and to UGX 25 billion (approximately US$11 million) by March 2013. Any new commercial bank entering the Ugandan market effective November 2010 had to have a minimum capitalization of UGX 25 billion. Today (June 2012), most of the banking activity is concentrated around Kampala and other urban centers, leaving most Ugandans out of the formal financial sector.

A moratorium on new commercial bank licenses was declared in 2004, with the passage of the Financial Institutions Act 2004 by Parliament, which established new banking institution classification guidelines, shifting the focus and modality of supervision from forensic to risk-based, and introduced robust, tight rules for management and governance of banks in Uganda.

The moratorium on new banks was lifted in July 2007. During the eighteen (18) months that followed the lifting of the moratorium, several new commercial banks were licensed. These included Kenya Commercial Bank, Equity Bank and Fina Bank, all from Kenya. Global Trust Bank and United Bank for Africa which trace their roots from Nigeria were also licensed during this period. The others were Ecobank; headquartered in Togo and Housing Finance Bank an indigenous bank.

Between 2008 and 2009, several of the existing banks went on an accelerated branch expansion either through mergers and acquisitions or through new branch openings. As of October 2010[update], there were twenty-two (22) licensed commercial banks in Uganda, with nearly four hundred (400) bank branches and a total of almost six hundred (600) ATMs.

In November 2010, Bank of Uganda directed that all commercial banks in Uganda, must raise their minimum capital to UGX 10 billion (approximately US$4.34 million) by March 2011 and to UGX 25 billion (approximately US$11 million) by March 2013. Any new commercial bank entering the Ugandan market effective November 2010 had to have a minimum capitalization of UGX 25 billion. Today (June 2012), most of the banking activity is concentrated around Kampala and other urban centers, leaving most Ugandans out of the formal financial sector.

A moratorium on new commercial bank licenses was declared in 2004, with the passage of the Financial Institutions Act 2004 by Parliament, which established new banking institution classification guidelines, shifting the focus and modality of supervision from forensic to risk-based, and introduced robust, tight rules for management and governance of banks in Uganda.

The moratorium on new banks was lifted in July 2007. During the eighteen (18) months that followed the lifting of the moratorium, several new commercial banks were licensed. These included Kenya Commercial Bank, Equity Bank and Fina Bank, all from Kenya. Global Trust Bank and United Bank for Africa which trace their roots from Nigeria were also licensed during this period. The others were Ecobank; headquartered in Togo and Housing Finance Bank an indigenous bank.

Between 2008 and 2009, several of the existing banks went on an accelerated branch expansion either through mergers and acquisitions or through new branch openings. As of October 2010[update], there were twenty-two (22) licensed commercial banks in Uganda, with nearly four hundred (400) bank branches and a total of almost six hundred (600) ATMs.

In November 2010, Bank of Uganda directed that all commercial banks in Uganda, must raise their minimum capital to UGX 10 billion (approximately US$4.34 million) by March 2011 and to UGX 25 billion (approximately US$11 million) by March 2013. Any new commercial bank entering the Ugandan market effective November 2010 had to have a minimum capitalization of UGX 25 billion. Today (June 2012), most of the banking activity is concentrated around Kampala and other urban centers, leaving most Ugandans out of the formal financial sector.

A moratorium on new commercial bank licenses was declared in 2004, with the passage of the Financial Institutions Act 2004 by Parliament, which established new banking institution classification guidelines, shifting the focus and modality of supervision from forensic to risk-based, and introduced robust, tight rules for management and governance of banks in Uganda.

The moratorium on new banks was lifted in July 2007. During the eighteen (18) months that followed the lifting of the moratorium, several new commercial banks were licensed. These included Kenya Commercial Bank, Equity Bank and Fina Bank, all from Kenya. Global Trust Bank and United Bank for Africa which trace their roots from Nigeria were also licensed during this period. The others were Ecobank; headquartered in Togo and Housing Finance Bank an indigenous bank.

Between 2008 and 2009, several of the existing banks went on an accelerated branch expansion either through mergers and acquisitions or through new branch openings. As of October 2010[update], there were twenty-two (22) licensed commercial banks in Uganda, with nearly four hundred (400) bank branches and a total of almost six hundred (600) ATMs.

In November 2010, Bank of Uganda directed that all commercial banks in Uganda, must raise their minimum capital to UGX 10 billion (approximately US$4.34 million) by March 2011 and to UGX 25 billion (approximately US$11 million) by March 2013. Any new commercial bank entering the Ugandan market effective November 2010 had to have a minimum capitalization of UGX 25 billion. Today (June 2012), most of the banking activity is concentrated around Kampala and other urban centers, leaving most Ugandans out of the formal financial sector.

A moratorium on new commercial bank licenses was declared in 2004, with the passage of the Financial Institutions Act 2004 by Parliament, which established new banking institution classification guidelines, shifting the focus and modality of supervision from forensic to risk-based, and introduced robust, tight rules for management and governance of banks in Uganda.

The moratorium on new banks was lifted in July 2007. During the eighteen (18) months that followed the lifting of the moratorium, several new commercial banks were licensed. These included Kenya Commercial Bank, Equity Bank and Fina Bank, all from Kenya. Global Trust Bank and United Bank for Africa which trace their roots from Nigeria were also licensed during this period. The others were Ecobank; headquartered in Togo and Housing Finance Bank an indigenous bank.

Between 2008 and 2009, several of the existing banks went on an accelerated branch expansion either through mergers and acquisitions or through new branch openings. As of October 2010[update], there were twenty-two (22) licensed commercial banks in Uganda, with nearly four hundred (400) bank branches and a total of almost six hundred (600) ATMs.

In November 2010, Bank of Uganda directed that all commercial banks in Uganda, must raise their minimum capital to UGX 10 billion (approximately US$4.34 million) by March 2011 and to UGX 25 billion (approximately US$11 million) by March 2013. Any new commercial bank entering the Ugandan market effective November 2010 had to have a minimum capitalization of UGX 25 billion. Today (June 2012), most of the banking activity is concentrated around Kampala and other urban centers, leaving most Ugandans out of the formal financial sector.

A moratorium on new commercial bank licenses was declared in 2004, with the passage of the Financial Institutions Act 2004 by Parliament, which established new banking institution classification guidelines, shifting the focus and modality of supervision from forensic to risk-based, and introduced robust, tight rules for management and governance of banks in Uganda.

The moratorium on new banks was lifted in July 2007. During the eighteen (18) months that followed the lifting of the moratorium, several new commercial banks were licensed. These included Kenya Commercial Bank, Equity Bank and Fina Bank, all from Kenya. Global Trust Bank and United Bank for Africa which trace their roots from Nigeria were also licensed during this period. The others were Ecobank; headquartered in Togo and Housing Finance Bank an indigenous bank.

Between 2008 and 2009, several of the existing banks went on an accelerated branch expansion either through mergers and acquisitions or through new branch openings. As of October 2010[update], there were twenty-two (22) licensed commercial banks in Uganda, with nearly four hundred (400) bank branches and a total of almost six hundred (600) ATMs.

In November 2010, Bank of Uganda directed that all commercial banks in Uganda, must raise their minimum capital to UGX 10 billion (approximately US$4.34 million) by March 2011 and to UGX 25 billion (approximately US$11 million) by March 2013. Any new commercial bank entering the Ugandan market effective November 2010 had to have a minimum capitalization of UGX 25 billion. Today (June 2012), most of the banking activity is concentrated around Kampala and other urban centers, leaving most Ugandans out of the formal financial sector.

A moratorium on new commercial bank licenses was declared in 2004, with the passage of the Financial Institutions Act 2004 by Parliament, which established new banking institution classification guidelines, shifting the focus and modality of supervision from forensic to risk-based, and introduced robust, tight rules for management and governance of banks in Uganda.

The moratorium on new banks was lifted in July 2007. During the eighteen (18) months that followed the lifting of the moratorium, several new commercial banks were licensed. These included Kenya Commercial Bank, Equity Bank and Fina Bank, all from Kenya. Global Trust Bank and United Bank for Africa which trace their roots from Nigeria were also licensed during this period. The others were Ecobank; headquartered in Togo and Housing Finance Bank an indigenous bank.

Between 2008 and 2009, several of the existing banks went on an accelerated branch expansion either through mergers and acquisitions or through new branch openings. As of October 2010[update], there were twenty-two (22) licensed commercial banks in Uganda, with nearly four hundred (400) bank branches and a total of almost six hundred (600) ATMs.

In November 2010, Bank of Uganda directed that all commercial banks in Uganda, must raise their minimum capital to UGX 10 billion (approximately US$4.34 million) by March 2011 and to UGX 25 billion (approximately US$11 million) by March 2013. Any new commercial bank entering the Ugandan market effective November 2010 had to have a minimum capitalization of UGX 25 billion. Today (June 2012), most of the banking activity is concentrated around Kampala and other urban centers, leaving most Ugandans out of the formal financial sector.