More Related Content

Similar to Anita Charlesworth: The Funding Outlook for Health Care (20)

More from Nuffield Trust (20)

Anita Charlesworth: The Funding Outlook for Health Care

- 1. The Funding Outlook for Health

Anita Charlesworth

Chief Economist

March 2013

Twitter: #NTSummit

© Nuffield Trust

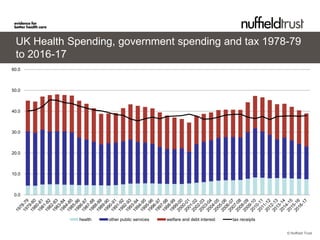

- 2. UK Health Spending, government spending and tax 1978-79

to 2016-17

60.0

50.0

40.0

30.0

20.0

10.0

0.0

health other public services welfare and debt interest tax receipts

© Nuffield Trust

- 3. The magic circle: health spending increases rapidly, overall

public spending and tax falls

Share of Total Public Health Other public Welfare and Receipts

GDP Spending spending services debt

interest

1978-79 45.1% 4.4% 25.9% 14.7% 40.1%

2007-08 40.7% 7.1% 20.3% 13.2% 38.6%

Difference - 4.4 +2.7 -5.6 -1.5 -1.5

Source: OBR, HMT PESA 2012

In 2016-17 spending as a share of GDP and receipts as a share of GDP will

be at the average for the 20 years pre-crisis (40% and 38%).

2 key differences: Health spending will be much larger (2 percentage

points of GDP) and spending on other public services will be at the share

last seen in at the end of 1990’s.

© Nuffield Trust

- 5. Closing £13 billion Funding Gap: 2010/11 to 2014/15

£105 Funding pressures on the NHS in England

Funding pressures after for pay restaint

Funding pressures after pay restraint and

managing hospital activity for chronic conditions

Funding (£billion in 2010/11 prices)

£100

Funding pressures after pay restraint, managing Pay

hospital activity for chronic conditions, and

productivity savings reduction:

Funding allocation based on 2010 spending review £5bn

£95 Disease

management:

£3bn

Acute QIPP

Actions: £4bn

£90

£85

2010/11 2011/12 2012/13 2013/14 2014/15

Year

© Nuffield Trust

- 6. Initial Progress in 2011-12?

Expected Actual Difference

Emergency Admissions trend 5,784,376 5,411,015 -7%

Emergency Admissions with QIPP actions 5,648,234 5,411,015 -4%

Emergency Bed Days trend 39,639,520 35,600,921 -11%

Emergency Bed Days with QIPP actions 37,352,528 35,600,921 -5%

Planned Admissions trend 8,766,957 8,735,584 0%

Modelled Planned Bed Days 16,747,173 16,555,415 -1%

Planned Bed Days with QIPP actions 16,159,549 16,555,415 2%

OP Appointments 67,079,975 72,799,662 8%

OP Appointments with QIPP actions 62,572,388 72,799,662 14%

A&E Attendances trend 15,503,662 17,602,055 12%

© Nuffield Trust

- 7. Variation in labour productivity at selected providers in

England: 2006/07 to 2011/12

© Nuffield Trust

- 9. Closing £11 billion Funding Gap: 2014/15 to 2017/18

£105

Funding pressures after pay restraint, managing hospital

activity for chronic conditions, and productivity savings

Funding pressure after releasing all semi-fixed costs

from QIPP

Funding (£billion in 2010/11 prices)

£100 Funding pressures after releasing all semi-fixed costs Releasing semi-fixed

from QIPP, and management of activity for chronic costs: £2bn

conditions

Funding pressures after releasing all semi-fixed costs Disease Management:

from QIPP, management of activity for chronic

conditions, and extension of pay restraint

£2bn

Flat Real

£95 Continued Pay

Restraint: £3bn

Remaining Gap:

£3bn

£90

£85

2014/15 2015/16 2016/17 2017/18

Year

© Nuffield Trust

- 10. Earnings will be key

2011 2012 2013 2014 2015 2016 2017

Nominal 2.2 2.7 2.2 2.8 3.7 4.0 4.0

average

earnings

growth

GDP 2.7 2.3 2.0 2.0 2.0 2.0 2.0

deflator

Nominal 1.7 1.7 2.5 2.5 ? ? ?

NHS pay bill

per head

growth

Source: OBR 2012, NHS employers 2012 © Nuffield Trust

- 11. Conclusions

• From 2010/11 to 2014/15 the NHS faces its tightest budget of last 50

years.

• This period of austerity is likely to extend at least until 2017-18.

• Only a even larger cut in other public services or welfare or relatively

large tax increases would allow NHS funding to grow at historic levels.

1p extra on income tax raises around £4 billion a year.

• Without unprecedented productivity gains, there is likely to be a rapid

growth in the gap between the demand for care and the ability to

provide high-quality services.

• Although the NHS is delivering headline savings its not clear that it is

making the necessary progress on service productivity and models of

care.

• The scale of workforce cost growth after 2015 will be crucial.

© Nuffield Trust