CSC World 2012

•

3 likes•2,406 views

CSC World is our corporate publication that seeks to explain the business meaning behind advances in IT. http://www.csc.com/cscworld

Recommended

Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (12)

Similar to CSC World 2012

Similar to CSC World 2012 (20)

Recently uploaded

Recently uploaded (20)

CSC World 2012

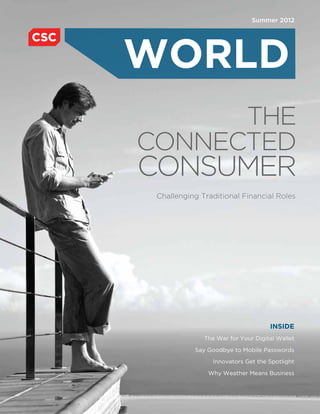

- 1. Summer 2012 WORLD the Connected Consumer Challenging Traditional Financial Roles INSIDE The War for Your Digital Wallet Say Goodbye to Mobile Passwords Innovators Get the Spotlight Why Weather Means Business

- 2. Let’s face IT The coevolution of online services and mobile devices is driving BUSINESS SOLUTIONS demand for fast, easy and affordable authentication solutions. CSC TECHNOLOGY specializes in delivering comprehensive identity-based services. We blend the latest technologies, systems, policies and processes to OUTSOURCING deliver integrated identity management and privacy assurance solutions that are secure, efficient and increase business value. Learn more at www.csc.com/ConfidentIDMobile.

- 3. WORLD Inside CSC World DIRECTOR, GLOBAL BRAND & DIGITAL MARKETING In one of America’s most cash-strapped and crime-ridden cities, creative financing is funding Nick Panayi the return of one famous policeman. An idea to build a monument to RoboCop, the part-man, EDITORIAL DIRECTOR part-machine sci-fi movie character, will soon become reality — and the effort behind the Patricia Brown statue is indicative of changes sweeping across the financial services industry. Senior managing editor Jeff Caruso Today, a global community of consumers armed with mobile devices is redefining the rela- editor tionship between customers and banks. The ensuing change is bringing about some very Chris Sapardanis creative uses of money. It is enabling projects that never would have been possible before. Contributing Writers Jim Battey The idea to bring a statue of the crime-fighting icon to stand watch over the Detroit neigh- Dale Coyner borhoods he patrolled in the movies began as a Tweeted suggestion to Detroit’s mayor, and Peter Krass Jenny Mangelsdorf then went viral in February 2011. Art director Deric Luong Some Detroiters decided to explore how far they could take the proposal by using a financing option called “crowd funding.” Crowd funding describes the process of people networking Design Kelly Dare online and pooling money or other resources to support projects started by others. The RoboCop team chose Kickstarter, the largest crowd-funding platform, which boasts $200 Design & production million pledged to projects since April 2009. Corporate Marketing Shared Services — P2 But it isn’t just pop-culture sculpture that can benefit from this alternative financial service. CSC www.csc.com Crowd funding helps technology innovators who otherwise lack enough capital to bring their ideas to market. THE AMERICAS 3170 Fairview Park Drive Falls Church, VA 22042 In May, the Pebble e-paper watch for iPhone and Android became the most-funded project United States in Kickstarter history, gaining more than $10 million in pledges, after asking for $100,000. It Tel: +1.703.876.1000 took the RoboCop crew in Detroit a few weeks to generate $67,436 to build the statue, after EMEA asking for $50,000, and building is under way. Royal Pavilion Wellesley Road Aldershot, Hampshire GU11 1PZ Consumers everywhere are supplementing traditional financial services or bypassing them United Kingdom altogether. In our cover story, “The Connected Consumer,” CSC World speaks with Patrick Tel: +44(0)1252.534000 Molineux, the researcher behind the Leading Edge Forum’s new report about the evolving AUSTRALIA financial services industry. The report examines changes driven by mobility, microfinance, 26 Talavera Road Macquarie Park NSW 2113 media and mining. Australia Tel: +61(0)2.9034.3000 Also in this issue, we hear how “The Constantly Connected Customer” is adding mobile ASIA devices to the retail shopping experience in stores without the shopkeepers’ blessing. These 20 Anson Road #11-01 customers are using their own devices and apps to gather information about products, Twenty Anson Singapore 079912 brands, pricing and availability. Republic of Singapore Tel: +65.6221.9095 In “The War for Your Digital Wallet,” we explore how companies are vying to meet the needs of these consumers. The battle extends beyond traditional financial services companies, CSC WORLD (ISSN 1534-5831) since a wide range of companies are looking for a piece of this rapidly expanding pie. is a publication of Computer Sciences Corporation. The Connected Consumer is a global phenomenon. In “Mobile Money Can Deposit Great Copyright ©2012 Computer Sciences Corporation Change in Emerging Markets,” we see further implications. In developed countries, mobile All rights reserved. phones are just another way to access traditional banking, but in emerging markets, the Reproduction without permission is prohibited. effect of “mobile money” is monumental. Comment on what you’ve We hope you enjoy the issue. CSC World is also available at read in CSC WORLD at www.csc.com/cscworld. www.csc.com/cscworld, where you can subscribe, comment on stories or download mobile versions. Or write: CSC WORLD Chris Sapardanis 3170 Fairview Park Drive Falls Church, VA 22042 USA Editor, CSC World www.csc.com/cscworld SUMMER 2012 | CSC WORLD 1

- 4. CSC WORLD | summer 2012 | VOLUME 11 | NUMBER 2 20 34 24 42 10 NEWS 4 CSC’s footprint grows in Canada, managed security services gain flexibility, major client contracts and accolades are won, and our long-standing support of the U.S. Navy continues. cover story 10 The Connected Consumer As mobile devices become more popular and sophisticated, they are rapidly transforming the relationship between consumers and financial services firms. CSC World speaks with Patrick Molineux, the lead researcher behind “Connected Consumer and the Future of Financial Services,” a report that examines these changes. 14 The War for Your Digital Wallet Consumers are already using their mobile phones to make in-store purchases, and as the technology evolves, the payment-processing industry will never be the same. 16 Mobile Money Can Deposit Great Change in Emerging Markets In developed countries, mobile phones are just another way to access traditional banking services, but in emerging markets, the effect of “mobile money” on financial services is monumental. 18 The Constantly Connected Customer Customers are adding smartphones and mobile devices to their shopping experience in your stores without your blessing. What are you going to do about it? 2 CSC WORLD | SUMMER 2012

- 5. Social media 20 Should Healthcare Organizations Use Social Media? New ON CSC.COM Social media is drastically changing the way healthcare Big Data Getting Bigger: The world of data is changing organizations communicate with customers and accomplish dramatically — from the amount of data being produced to their business objectives. the way in which it’s structured and used. This trend presents enormous challenges, but it also presents opportunities. 22 Social Business: the Next Big Step Learn more at www.csc.com/Big_Data. Add social customer relationship management to Enter- prise 2.0, and you get something truly transformational: CSC Town Hall: CSC introduces its Town Hall events, our social business. continuing series of online conferences on IT topics that matter to you, featuring CSC experts and special guest CLIMATE DATA speakers ready to answer your questions. Registration is 24 Climate Economy: Why Weather Means Business free at townhall.csc.com. Climate and weather patterns are in flux and the impact Success Story Briefing Center: View video success stories featur- is being felt across many industries. A new climate data ing CSC subject-matter experts, clients and global partners, or reporting tool provides insights into how these changes search hundreds of stories that cover a wide range of industries, affect bottom lines. locations and clients at www.csc.com/success_stories. 26 Finding Big Fish in Big Data Off Florida’s coast, scientists are diving into a sea of data. They’re tracking tiny Atlantic bluefin tuna larvae using climate and weather data mined from one of the world’s largest data libraries. BIOMETRICS By the numberS 28 Say Goodbye to Mobile Passwords 38 Big Data, Bigger Potential Passwords remain a popular security device simply because Once you get your mind around just how big our data they are easy and inexpensive to use. But thanks to new has become, the next trick is to open your mind to the technologies, the last days of forgettable letters and possibilities created by having all that data. numbers may be in sight. IN PRACTICE: Utilities CLOUD COMPUTING 40 National Grid Energizes IT via Virtualization 30 From Pilot to Production: Key Questions Emerge When National Grid was looking for a world-class IT as Companies Adopt Cloud Architectures team to deliver highly reliable and efficient IT support Cloud computing is transforming the IT infrastructure of services, CSC was chosen to provide enterprise services today’s enterprise, helping companies reduce costs, expand for the ecosystem. relationships, support a mobile workforce and respond to changing business conditions. 42 wissgrid Powers Up Cybersecurity S As a strategic player in Europe’s power grid, Swissgrid 32 5 Questions CIOs Should Ask Before Moving needs to meet the most robust cybersecurity standards Email to the Cloud or the lights could go out in several countries. The modern office requires instant and rich communica- tions among a dispersed workforce. The cloud provides a SUSTAINABILITY way to give companies that flexibility with collaboration 44 Do Your Suppliers Measure Up to Your and email services. Ethical Standards? Supply chains don’t often make headlines. But when they do, FEATURE it’s usually not good news. CSC advocates environmentally, 34 Innovators Get the Spotlight socially and fiscally responsible supply chain practices. Forward-thinking CIOs are on the lookout for emerging technologies that will help position their organization for growth and performance. The CSC Award for Excellence recognizes individuals who have created innovative solu- tions that advance our clients’ business or our own. SUMMER 2012 | CSC WORLD 3

- 6. news ANNOUNCEMENTS CSC BRINGS PRIVATE CLOUD TO CANADA Although cloud computing is widely known to save businesses addition to CSC’s unified communications and collaboration money and make them more productive, many Canadian firms (UCC) solutions suite. have been slow to adopt the technology due to concerns about data privacy and security. CSC’s UCaaS solution enhances the clients’ productivity and accelerates business processes and decision making while CSC’s latest offering in Canada addresses those issues with the lowering costs. The service was developed in close collaboration availability of CSC BizCloud™, the first on-premises private cloud with Cisco and complemented by CSC’s multiplatform integra- billed as a service and ready for workloads in 10 weeks. BizCloud tion. UCaaS builds on CSC’s capability of providing custom, combines the privacy, security and control of a private cloud with outsourced UCC solutions, serving as the underlying platform the agility, convenience and commercial model of a public cloud. for the full range of collaboration capabilities and services that offer clients communication and collaboration flexibility as their “Cloud computing has tremendous promise in Canada,” says businesses grow and change. Mark Schrutt, director of services and enterprise applications for IDC Canada. “Up to this point, many Canadian businesses have “We welcome CSC’s UCaaS offering to Canada and the opportu- been sitting on the sidelines waiting for in-Canada solutions. nities it presents to organizations looking to realize the benefits of IDC’s research finds that 60% of buyers prefer in-Canada Infra- a hosted collaboration solution,” says Mike Ansley, vice president, structure as a Service offerings. In addition, Canadian businesses partner organization, Cisco Canada. “The combination of CSC want flexibility at cost-effective prices. CSC’s BizCloud hits on all and Cisco provides clients with world-class collaboration services these points. We see BizCloud as a key addition to the Canadian to meet the changing needs in the workplace.” cloud market.” The hosted unified communications service allows businesses BizCloud accelerates the adoption of a private cloud by busi- around the world to bring converged voice, mobile and data nesses and government agencies, eliminating lengthy capital services to every desktop in their organization. Companies that acquisition cycles. Compared to do-it-yourself private clouds, are tightly managing their capital expenditures will be able to where multiple components are acquired and then integrated, take a first step into converged communications by basing BizCloud is based on fully integrated VCE Vblocks and comes their telephony, voicemail, conferencing and unified messaging with a service catalog, chargeback methodology, and automa- technologies on a utility-based, per-user pricing model. tion to simplify management and orchestration. Learn more at www.csc.com/cloud or www.csc.com/ucc. In April, CSC also introduced Unified Communications as a Service (UCaaS), based on Cisco’s Hosted Collaboration Solution for Canada. This offering is the latest standard managed service 4 CSC WORLD | SUMMER 2012

- 7. FLEXIBILITY ADDED TO SECURITY SERVICES TO DETER THREATS CSC will offer its Managed Security Services, including its most advanced capabilities, on a stand-alone basis to help clients better address the continually escalating threat environment. Delivered through the company’s around-the-globe Security Operations Centers, CSC Managed Security Services now offer convenient access to enhanced core security, along with risk- appropriate options for advanced malware protection; global threat intelligence; situational awareness; and governance, risk and compliance support. Now available for a much wider range of client organizations, the offering reflects CSC’s enterprise-level managed services experience, expertise across both public and private sector se- curity environments and record of strengthening cybersecurity for some of the world’s largest intelligence organizations. SAFEAUTO LICENSES CSC LEGAL SOLUTIONS SUITE Recognized as a “Leader” in “The Forrester Wave™: Managed SafeAuto Insurance Co., a direct-to-consumer property and Security Services, North America, Q1 2012,” CSC designed its casualty insurance carrier, has licensed CSC’s legal matter Managed Security Services portfolio around a flexible, tiered management software, Legal Solutions Suite. SafeAuto sells, approach that helps organizations access security with low risk, markets and underwrites state-required, minimum-limit stages their evolution over time toward the most effective pos- personal automobile insurance coverage in 16 states, as well ture addressing the complexity of today’s threat-and-compliance as higher-limit options in multiple states, and has chosen CSC environment and better aligns spending to their specific needs. Legal Solutions Suite to manage legal expenses and improve communication with outside counsel as the company expands “Organizations do not have a single risk profile; some aspects of operations into new geographic regions. their business are lower risk while others are of extremely high value and require the most advanced protection available,” says Legal Solutions Suite helps reduce legal expenditures by Carlos Solari, CSC vice president of cybersecurity technology streamlining and managing collaboration with outside counsel. and services. “Our services tiers enable our clients to buy risk- The software provides detailed data regarding charges, appropriate coverage, from enhanced core services to the most performance and outcomes that will enable SafeAuto to quickly advanced and elevated state-of-the-art cyber-protection.” evaluate patterns and trends among law firms and individual attorneys. Legal Solutions Suite also assists with improving Learn more at www.csc.com/cybersecurity. transparency and consistency in legal matter planning and bill review. “As we expand our business across the nation, it is critical to enforce outside counsel guidelines and ensure budget compli- ance,” says Mark LeMaster, senior vice president and general counsel at SafeAuto. “Legal Solutions Suite will help us efficiently manage outside counsel and improve our bottom line through an automated, structured expense-management process.” CSC’s Legal Solutions Suite software automates core processes and enables legal or claims organizations to lower expenses, simplify the legal billing process, analyze legal invoices, docu- ment outside law firm performance and create a collaborative electronic workspace for budgeting, planning and strategy. Legal Solutions Suite keeps companies better informed throughout the case-management process and helps identify firms that consistently drive superior results. Learn more at www.csc.com/legalsolutionssuite. SUMMER 2012 | CSC WORLD 5

- 8. news AWARDS RANKINGS CSC RECOGNIZED FOR CORPORATE RESPONSIBILITY CSC has achieved a Gold ranking in Business in the CSC also maintains its inclusion for the third consecutive year Community’s (BITC) 2012 Corporate Responsibility Index in the FTSE4Good Index Series, which recognizes companies (CRI), the United Kingdom’s leading voluntary benchmark for their corporate responsibility standards. CSC once again of corporate responsibility. received a high ranking in environmental management. Achieving a Gold-level designation means that CSC is able “We are honored to be part of the FTSE4Good Index Series for to demonstrate openness and transparency through effec- the third consecutive year,” says Susan Pullin, vice president of tive public reporting of its material environmental and social corporate responsibility at CSC. “This achievement is confirma- issues, programs and performance. Gold companies also tion of CSC’s firm commitment to being a responsible corporate tend to expand and adapt their risk management processes citizen, and that we are creating a sustainable business which by incorporating relevant aspects of corporate responsibility takes environmental, social and governance reporting seriously.” risk and opportunity. Their corporate responsibility strategy is articulated in an effective manner and includes clear and Learn more at www.csc.com/cr. measurable targets. CSC’s Michael During Cirafesi’s more than 10 years with CSC, the Philadelphia- Cirafesi Wins Top based executive has worked in both commercial and federal Consulting Award consulting. Most recently, in July 2011, he assumed the CTO Michael Cirafesi, a partner and CTO position and rejoined the commercial consulting side. “These for CSC’s Global Business Solu- dramatic changes are why I’ve stayed in consulting,” he says. tions (GBS) Eastern Region, has “I’ve worked with so many different clients and industry segments won this year’s Consulting maga- and accounts and divisions across CSC that I always feel as if I’m zine Top 25 Consultants award for doing something different. Each day is a new challenge.” excellence in technology. Cirafesi is proud of CSC’s culture of putting the client first. The annual Consulting magazine awards honor 25 consultants That means getting close to clients, learning what makes them from leading firms for their extraordinary efforts in seven critical tick, and hanging tough — even when projects get complex service areas: client services, energy, financial services, health- and challenging. “It has a lot to do with being able to deliver care, leadership, public sector and technology. Cirafesi was and being in the trenches,” Cirafesi says. “I consider myself a cited by Consulting magazine for helping GBS achieve record- success when, after a year, I know the business better than the breaking growth; leveraging past relationships to develop new client does.” business; modernizing techniques across the sales, business development and alliance management processes; reinstituting Learn more at www.csc.com/management_consulting. the GBS CIO Council; and leading multiple proposals for some $60 million worth of potential consulting and business process outsourcing engagements. 6 CSC WORLD | SUMMER 2012

- 9. INSURANCE BILLING SYSTEM NAMED AN INDUSTRY LEADER CSC received the XCelent Functionality 2012 and XCelent Service 2012 awards from Celent, an industry research and consulting firm, for its Exceed Billing insurance software. Exceed Billing enables consolidated billing across multiple market segments, lines of business, distribution channels and/or policy systems. The awards are based on Celent’s assessment of CSC’s con- figurable, scalable application, as compared to other offerings profiled in a report titled “Stand-Alone Billing System Vendors: North American Property and Casualty Market 2012.” The report uses Celent’s proprietary framework called the ABCD Vendor View to profile and benchmark stand-alone systems in use by property and casualty carriers. Vendors with the highest score in each category are recognized as XCelent award winners. CSC’s Exceed Billing led the “Functionality” and “Depth of Service” categories following an analysis of the functions and features provided in the base offering; the power and ease of use of rules, workflow and product configuration capabilities; supported lines of business and number of deployments; size and experience of CSC’s services and support team; and users’ REPORT NAMES CSC AS A ‘LEADER’ IN implementation experiences. MANAGED SECURITY SERVICES Forrester Research Inc. has placed CSC in its strongest cat- Learn more at www.csc.com/banking. egory — “Leader” — in the March 26 report “The Forrester WaveTM: Managed Security Services: North America, Q1 2012.” The report evaluated significant providers of managed security services (MSS) against 60 criteria that included current offer- ings, strategies and market presence. “CSC’s current and potential clients now have further indepen- dent validation that they have the best-in-class security protection with CSC,” says Samuel Visner, vice president and lead cyberexecutive at CSC. According to the report, CSC “leverages its large consulting practice to identify suitable candidates for a managed model. CSC uses cost-benefit models to demonstrate the return on investment in its services, and it has one of the better portals in terms of flexibility and features that we tested.” The report also noted that “customers identified its well-run Security Operations Centers and responsiveness as positive attributes for CSC.” CSC’s investment in offering discrete Managed Security Services to the market has been well received by organizations and analysts. Previously available only to its IT outsourcing clients, CSC’s Managed Security Services are now available as a stand- alone offering to a much wider range of client organizations as the company moves aggressively to play a larger and more influential role in this rapidly expanding market. Learn more at www.csc.com/cybersecurity. SUMMER 2012 | CSC WORLD 7

- 10. news contract wins Amerisafe Chooses BPO for Legal Services CSC signed a three-year business process services contract with Amerisafe Inc., a specialty insurer in DeRidder, La. Under the agreement, CSC will provide business process outsourcing (BPO) services to manage and automate legal expenditures for Amerisafe by using Legal Bill Analyzer, a component of CSC’s Legal Solutions Suite, strengthening transparency in legal mat- ter planning and communication with outside counsel. CSC’s customized BPO offering for Amerisafe includes a range of services, such as bill review, resolution, reporting, invoice management and Web hosting support. The agreement provides a low-risk approach to transforming operations and controlling costs, and encourages constructive collaboration Merged AMP and AXA Extend between Amerisafe and law firms. Relationship Wealth management company AMP Ltd. has extended its relation- “Growing organizations like Amerisafe are blending compo- ship with CSC to 2016. The comprehensive services contract is nents of Legal Solutions Suite with our BPO capabilities to worth more than AUD$220 million and is designed to support gain measurable efficiencies in legal matter management,” says the merged operations of AMP and AXA Asia Pacific Holdings Jeffery Schwalk, president of CSC’s Property and Casualty Australia and New Zealand. The merger, which took place last year, Insurance Division. “CSC’s customizable software and services brought together two of the region’s most established businesses. ensure transparency for litigated and nonlitigated matters by reducing compliance risks and proactively managing legal The deal expands a six-year, AUD$150 million contract signed in spend, with immediate savings of up to 8%.” 2009, and continues the original engagement between the two companies that was formed in 1993. Currently, CSC provides Learn more at www.csc.com/legal_solutions. AMP with fully outsourced managed infrastructure services for mainframe, midrange, network, desktop, service desk and cloud email service, as well as information and system security. CSC’s services will enable AMP to maximize efficiencies from the integration of all infrastructure services across the new AMP/AXA entity. CSC will continue to deliver advanced and consistent services across all AMP business units, and work has already begun on the technology integration of AMP and AXA. Transport for London Renews Outsourcing Agreement CSC has signed a new IT outsourcing agreement valued at $33 million with Transport for London (TFL), extending the current contract by 27 months. The contract extension was signed dur- ing CSC’s fiscal 2012 third quarter. Under the extended agreement, CSC will continue to manage a range of IT services for TFL, including service desk, desktop support and the delivery of real-time customer information at a number of London underground stations. “We are delighted to be extending our relationship with TFL and working hand in hand with them as they implement a new IT agenda to support their critical business systems and servic- es,” says Liz Benison, CSC UK president. “Levering our skills and expertise, we will be providing technology-enabled solutions to support them through the transformation.” 8 CSC WORLD | SUMMER 2012

- 11. U.S. NAVY Support for Sealift Program Office The U.S. Navy has awarded CSC a task order to provide pro- gram management support to the Strategic and Theater Sealift Program Office. The order was awarded in the fourth quarter of CSC’s fiscal year 2012 under the Naval Sea Systems Command SEAPORT-Enhanced contract vehicle won by CSC in 2004. The task order has a one-year base period and four one-year options, bringing the estimated total value to $113 million. Under the terms of the agreement, CSC will provide a full range of program management support, including acquisition document preparation, financial management, test and evaluation, integrated logistics, systems integration and technical/engineering. The Strategic and Theater Sealift Program Office is responsible for executing the Joint High Speed Vessel and Mobile Landing Platform acquisition programs as well as the Sealift Research and Development initiative, which includes operational logistics. Training Systems Solutions The U.S. Naval Air Warfare Center Training Systems Division (NAWCTSD) has awarded CSC a Multiple Award Contract (MAC). With a base ordering period of five years and two one- year ordering period options, the Training Systems Contract Video as a Service to Yield III (TSC III) has a potential ceiling value of $2 billion. It was Battlefield Intelligence awarded in the third quarter of CSC’s 2012 fiscal year. The U.S. Navy’s Naval Air Systems Command (NAVAIR) has awarded CSC an Unmanned Aerial Systems (UAS) contract to “Every day, we’re helping the Navy achieve mission-critical deliver streaming video as a service. This is an indefinite deliv- requirements, enhance warfighter readiness, improve citizen ery/indefinite quantity multiple-award contract with three prime services and, most importantly, save lives,” says Alan B. awardees. The contract has a 60-month period of performance, Weakley, president of CSC’s North American Public Sector with a total maximum value of $874 million. Defense Group. “We’ve been developing and enhancing complex training systems for the Navy and other agencies for decades, Under the terms of the agreement, CSC is eligible to receive and this new vehicle will further expedite our customers’ ability task orders to fly land-based UAS aircraft to deliver stream- to access additional critical offerings.” ing video from electro-optic and infrared cameras directly to military users in a remote theater of operations. CSC will deploy Under the terms of the contract, CSC will compete for delivery people, equipment and supplies. The combination of these orders to design, develop, produce, test and evaluate, deliver, capabilities as a service translates into significant savings to modify and support training systems. customers, who will receive intelligence, surveillance and recon- naissance (ISR) coverage without having to invest in additional Learn more at www.csc.com/government. labor and equipment. The customer pays only for video hours delivered as a service. “CSC has extensive experience delivering technology as a service,” says Hal Smith, vice president of CSC’s North American Public Sector ISR Group. “Delivery of video as a service is a natural extension of the CSC business model. We’ll now apply this service delivery model to reliably and efficiently deliver intelligence on the battlefield.” Learn more at www.csc.com/xaas. SUMMER 2012 | CSC WORLD 9

- 12. CONNECTED CONSUMER QA CONNECTED CONSUMER CSC’s Patrick Molineux Talks About the Quickly Evolving Financial Services Industry by Patricia Brown The dialogue between consumers and financial services firms has taken a number of dramatic turns in recent years. Banking relationships once built on local ties became conversations controlled by voice prompts and customer management systems as mergers and acquisitions turned neighborhood banks into international financial powerhouses. Today, a global community of customers, armed with mobile devices and instant answers, is once again redefining the relationship between customers and banks. Institutions find themselves in unfamiliar territory as they struggle to reconnect with customers on customers’ own turf and attempt to fend off challenges from new companies infiltrating value chains that once belonged exclusively to the financial services industry. 10 CSC WORLD | SUMMER 2012

- 13. The Leading Edge Forum’s most recent report, “Connected A lot of people say mobile technology isn’t secure enough Consumer and the Future of Financial Services,” examines the to use in financial services and I fundamentally disagree. changes in that relationship through the development of four They’re not comparing it with the right thing. Compare a key areas: mobile technology, microfinance, media and data mobile transaction with cash. Cash is insecure. Cash is almost mining. The report was developed by Patrick Molineux, chief untraceable. It is very easy to steal. It’s the most insecure strategy officer for CSC’s financial services business. As an LEF thing possible. associate, Molineux drove the research for this report, shaping the core themes and drawing on a team of CSC experts and Security on mobile devices is changing, and fast. It’s becoming select financial services and technology firms. Patrick spoke with harder to break the security. We’re starting to see the availability CSC World about the quickly evolving financial services industry. of multiple security mechanisms like CSC’s ConfidentIDTM Mobile, which establishes security through multiple layers of This report highlights the emergence of the connected identification and authentication. consumer and the ensuing implications for financial services firms. What aspects of this transformation did In advanced mobile devices, you’ll see security that goes beyond you find surprising? pass codes using a range of biometric authentication modalities. We don’t know which will be the most practical yet, but mobile One of the most stunning aspects is the pace of change. We technology is already far more secure than what we’ve had examined the impact of four major trends in the report: mobile before and will become even more secure in the near future. technology, microfinance, media and data mining. The speed of consumer-driven technological change cuts across all four. The report discusses the advent of the super card. Do you see a role for this type of device? This speed is something financial services firms must grasp. A firm might spend months looking at an innovative idea, and then Compared to other transaction mechanisms, the super card is perform months of feasibility studies, months of implementation, a comparatively new arrival. These are cards with capabilities pilots and final roll outs. Today at that pace an idea may well be almost rivaling that of a basic phone with digital displays and obsolete or leap-frogged before it hits the street. keypads. These could potentially act as a payment management tool, providing a bank balance, warnings if you reach a preset Consumer control is another important implication. Firms have limit, and multiple accounts from different financial institutions, said for years that the consumer is in control, but it wasn’t really eliminating the need to carry a pocketful of cards. true. Technologies now are making it possible for consumers to gain real control over the financial services process, forcing The report discusses the tug of war between competing firms to engage on the consumer’s turf for the first time. payment technologies, between super cards and mobile phone technologies. I think there’s a role for both types That leads to a third striking development, the need for firms to because payment preferences vary widely by country, culture speak to consumers in an authentic voice. An authentic voice and purpose. is not one that has been scrubbed by the legal department, whitewashed by the marketing department, and signed off Will firms need to implement something different on a country upon by the chief executive. The way firms balance that need by country basis? Will there be a point where we reach a for an authentic voice with the need for maintaining compliance single payment system? will be one of the great customer engagement challenges of the next few years. Maybe in 20 years we’ll be such a unified global village that our payment systems will have merged into a single form, but that’s What makes these issues important right now? What are the well beyond the time horizon anyone is looking at right now. colliding forces that have created this nexus point? So there will be differences to contend with. Japan is far and away the largest user of NFC [near-field communication] phone We care about these issues now because incredibly powerful payments. Kenya is leading the world in SMS-based payments mobile devices are so embedded within the consumer lifestyle. with M-Pesa. Sweden may be the most advanced country This is driving change in consumer behavior with astonishing moving to a cashless society, with stores in certain towns speed. The factors are feeding each other — the capability of starting to refuse to accept cash. devices, the acceptance of new forms of conducting financial transactions, and the sheer number of mobile devices that are To say one payment system will win out over the others would in use. It’s almost a vortex of change. require more certainty than I or anyone else should have. Each country has a different kind of infrastructure to cope with Your report examined the impact of mobility in great depth. payments, so the successful transaction technology will be the One issue we hear about repeatedly is the risk associated with one that’s most convenient: and that’s going to vary by country mobile devices used for financial transactions. How realistic based on the available alternatives and the transaction at hand. are those concerns and how will they affect the growth of mobile use in financial services? SUMMER 2012 | CSC WORLD 11

- 14. CONNECTED CONSUMER The report examines the role of microfinance on the world’s financial future. How important is this trend and what’s the impact on financial services? You can look at microfinance from an altruistic perspective and a hard-nosed capitalist perspective. It makes sense from both. From the capitalist’s perspective, microfinance is about a long- term investment that grows new markets for financial services. In the short to mid-term, the benefit of microfinance can be more altruistic, helping people gain a foothold out of poverty, directly affecting lives. Microfinance isn’t a magic wand and we don’t want to misrepresent it. Citizens of developing countries face many challenges, and microfinance is just one tool to help them. But there is clearly huge value in both the near term and long term. If people have more money, they can break themselves out of poverty; providing accessible financial services is one of the tools to equip people with that ability. What are the barriers that firms face in developing microfinance solutions, and how are they overcoming them? Many barriers to microfinance have nothing to do with finance itself. Just one example is education. Many financial products are complex to understand. There’s no need for financial products to be complex. We can make them simple. Low-cost tablets can have an impact. As soon as people have access to tablet technology, they have sufficient screen real estate to engage in financial education along with other learning opportunities. Mobile devices are overcoming another barrier: distance. If you live a day’s walk from a bank, how do you establish a savings account? Even if you got to the bank, the cost of doing business would be so high, saving would be impractical. Today, phone-based savings accounts allow people to manage financial accounts from anywhere. Technology will never be the whole answer but it’s a big part. You highlighted some facets of the connected consumer at the outset, but in the section of your report that discusses the impact of media, specifically, the Internet, what were the other aspects of this phenomenon that stood out to you? We’ve known since the creation of the Internet that it provides consumers with knowledge. The connected consumer is one who uses the Internet to talk with others on a global scale and convert knowledge into power. And by that I mean taking advice from other consumers, challenging the brands and banks if they don’t like the service they’re getting. That conversion of knowledge into power is an extraordinary shift that is unstoppable. Financial services firms used to act as interpreters, magicians almost, explaining things 12 CSC WORLD | SUMMER 2012

- 15. like pensions that few really understood. Now firms are acting as aggregators or executors because customers can go online and find out anything financial. This isn’t exclusive to financial services. It’s happened in many other industries. Learn more at Download the LEF Report at www.csc.com/connectedconsumer. www.csc.com/financialservices. Investments in social media are imperative. It’s easy to say “you need to get on Facebook.” The hard part is determining what conversation you’re going to have with consumers when you’re there and who will handle it. That goes back to the question of having an authentic voice. The particular imperative for financial services firms is to address the new consumers coming to a bank for the first time The report discusses the impact of mining as the fourth “M.” expecting that level of engagement with the firm. No firm has What is mining and how is it relevant to financial services firms? worked out exactly how that is going to play out. That’s not a failure of anyone. It’s simply that this is moving so fast. We’re familiar with data mining, using large sets of structured data to answer specific questions. This is a capability many Will these factors make financial services easier to understand firms are still wrestling with as they try to respond to complex and to buy? Are we seeing more transparency as a result of regulation. Now there are other types as well. mobile technologies and the influence of media? Web mining refers to posing questions to unstructured data We’re seeing financial systems turn toward greater sets. Google made data miners of us all. Consumers using transparency and simplicity, almost like a financial version of search engines are constantly and almost unthinkingly creating iTunes. But that begs the question: How simple can we make sophisticated algorithms such as “Which bank account should I it? There is a certain sophistication of the products that defies use,” or “Which insurance company has the best claims payout simplification. Making a decision to invest in a Latin American record?” Consumers can get good answers because they’re fund versus an Asian fund is not an inherently simple decision. asking specific questions at one point in time. Web mining is a harder task for the firm that needs to have a continually updated That’s a great comparison. If financial services are as easy view of those questions. to buy as a song on iTunes, do you think it will diminish the discipline of investing? Then there’s a third development. Social mining reveals who is saying things about you, what’s being said about your firm on There is a danger that too much simplicity can mask the Twitter feeds, what discussions are taking place in online forums. sophistication of the decision. The consequences are low if I This is huge. Firms can even start to adapt their product and buy a Salt-n-Pepa tune instead of the Pink Floyd track I meant service offerings based on what individual consumers are saying to buy. Financial mistakes are expensive. Accidentally putting about them online. money into the wrong fund can fundamentally affect my retirement. Perhaps in 10 years time we’ll be having the debate The real revolution may come in what we term “society mining.” around making financial services that bit harder for consumers This is the concept of aggregating a whole range of data to purchase to force them to think through the consequences! sources, public and private, that will help us understand the customer at an incredibly sophisticated level. What impact are digital peer-to-peer (P2P) payments having on consumers and the financial services industry? There’s a struggle to balance the interests of companies and consumers with respect to this type of data and privacy, but it’s It’s absolutely huge. A genuine revolution. Everyone’s heard clear that mining data and gaining new insights could be the of PayPal. In China, everyone has heard of Alipay, which now most important theme of them all. Ultimately, perhaps the only has more transactions than PayPal because of the size of the barrier to a firm knowing anything they could ever wish to know Chinese market. Mobile P2P payments are becoming huge as about every customer they have and may wish to have in the well. Banks face a stark choice: engage in P2P payments or face future is a combination of data privacy regulation and access disintermediation. Many firms are entering the payments value to the right technology. We’re not there yet. Will we get there? chain: Safaricom in Kenya, O2 in the UK, technology firms as Leading this report has made me think we might. illustrated by Google Wallet, for example. This is a value chain being broken apart by different players; you can join but you can’t stop it. Patricia Brown is director of content strategy for CSC’s digital marketing team. SUMMER 2012 | CSC WORLD 13

- 16. CONNECTED CONSUMER THE WAR FO YOUR DIGI R TAL WALLET by Randy Ba rker Consumers are already using their mobile phones to make in-store purchases, and as the technology evolves, the payment-processing industry will never be the same. The shift from plastic to digital wallets and mobile payments is in full swing. Consumers can walk into Best Buy and not only use their phone to make a purchase, but they can also get information on the hottest deals or compare prices with other stores. Mobile devices are sitting at the intersection of payments, advertising and marketing. Credit card companies, banks, mobile service providers, Internet companies and retailers are all scrambling for a piece of the growing market for payment processing, and the winners will be those who demonstrate technology leadership, provide the best user experience, and give the most business value to merchants. Consumers will choose the winners with their digital wallets — but what’s in it for them? What does the typical consumer really want, and how can companies deliver that? 14 CSC WORLD | SUMMER 2012

- 17. Get to the point (of purchase) Many of the top companies in the United States are attempting to answer these questions. Financial institutions derive a significant percentage of their annual revenue from processing Payment-processing power payments, but that piece of the pie is quickly shrinking. Banks are being crowded out by emerging competition from With decades of financial services industry experi- nontraditional financial services companies, such as PayPal and ence, CSC has the expertise to help all the players Square Inc., both of which offer a small hardware device that in the payment landscape to better compete and can be attached to a cell phone to read credit cards. provide the services that customers want. We offer a broad range of payment-related solutions, including: The number of nonfinancial companies jumping on the payment- processing bandwagon is growing and includes some of the top retailers. Wal-Mart and Target are among the large retailers • Electronic Payment Processing Software: CSC’s developing technology that will let customers make purchases financial services offerings include the ePayments via mobile phones. In addition, several U.S. mobile carriers have payment processing gateway; the CAMS II Card created their own mobile wallet technology, Isis, a joint venture Merchant System, the industry’s leading in-house of Verizon Wireless, ATT Mobility and T-Mobile USA. cards management system; and Celeriti, our end-to- end suite of enterprise software for global banking, To see who wins the early battles in the payment-processing cards, payments and lending. Learn more at war, also keep a close eye on the big four companies that have www.csc.com/financial_services. emerged as “consumer darlings”: Apple, Google, Facebook and Amazon. Consumers keep flocking to these brands because • Mobility Solutions: CSC’s mobility portfolio is a they are familiar, and in many cases, their products and services complete and modular system, tailoring solutions have become interwoven with everyday life. to meet the unique needs of different industries. Apple’s massive popularity with consumers may indicate how Learn more at www.csc.com/mobility. they will choose payment-processor winners. Consumers simply prefer the sleek design and ease of use of Apple products. In • Cloud Services: We offer a wide array of public the case of mobile phones and tablets, user experience trumps and private cloud solutions, such as CloudCompute price, and Apple has won. Not surprisingly, Apple has publicly and BizCloud. Our Trusted Cloud Services provide stated that it will eventually transform its iTunes ecosystem into customers with secure tools and infrastructure. a platform for payment processing. Learn more at www.csc.com/cloud. Whom do you trust? • FuturEdge: CSC’s application portfolio management With all the jockeying for market share, it will be the consumers service helps companies modernize their systems for who decide the winners — with their wallets. Or their digital improved efficiency. Learn more at wallets, that is. www.csc.com/applications. When a consumer goes about making a purchase, three questions come to mind: Whom do you trust the most? Whom are you most comfortable sharing information with? And finally, Learn more about CSC’s services at who is going to blend the advertising world and the payments www.csc.com/solutions. world most successfully? The companies that win will be the companies that address these consumer questions and provide the easiest and most secure experience for people who walk into a store to make a purchase by using a mobile phone. The best news for many is that the ultimate winners could be the consumers themselves. Increased competition will drive Security is of paramount importance. Consumers demand the down processing fees, and the wider playing field will give most stringent security possible for their credit card purchases, consumers a better selection of financial services and banking and companies that can deliver relatively secure solutions offerings to choose from. Still, when it comes to credit card and can also address concerns about potential fraud will set payments, trust and security will be the key factors. May the themselves apart from those that cannot. best (and most trusted) solution win. RANDY BARKER is director of channel solutions for banking and credit services at CSC. SUMMER 2012 | CSC WORLD 15

- 18. CONNECTED CONSUMER MOBILE MONEY Can Deposit Great Change in Emerging Markets by Erica Salinas In developed countries, mobile phones are just another way to access traditional banking services, but in developing nations, the effect of “mobile money” on financial services is already monumental. When the Internet came along, banks in developed countries rushed to provide online banking services. This changed the customer interface and moved services out of the bank branch. Today, mobile phone users pull up an app on their phone rather than on their computer screen. But under it all, the services and the customers have remained essentially the same. Contrast that with developing countries, where mobile phones are bringing financial services to billions of consumers who had previously been completely excluded from the formal financial sector. Many refer to this group of people as the unbanked. The more astute identify them as potential clients: They are the billions of potential clients who need and want financial services and are ready and able to pay for them. 16 CSC WORLD | SUMMER 2012

- 19. The push for mobile money leveraging the mobile channel as well. Financial institutions Mobile money services in developing countries are primarily tar- began offering formal financial services, such as credit, savings geted at the unbanked. It is estimated that 2 billion people have and insurance, to newly accessible geographic areas and a mobile phone but do not have a bank account. This means consumer groups. that over half of the world’s unbanked can be accessed through a basic cell phone. With this unprecedented level of access, the While microfinance institutions already serving the unbanked push for mobile money continues to increase for both social are familiar with the unique needs of the poor, larger financial and profit motives. institutions still struggle to design products for this new client base. Microfinance products are not simply standard financial products Financial inclusion is a priority in emerging markets. It has been sold in smaller amounts. Success in this market requires new shown to alleviate poverty, increase social justice and improve qual- products lines designed specifically for those with small incomes. ity of life. Increased financial inclusion also contributes to the eco- nomic growth and stability of an emerging market. Consequently, A future mobile money ecosystem the potential for mobile phones to overcome so many barriers in The mobile money market is spreading quickly across the serving the unbanked has created great excitement. developing world, particularly in Africa. In 15 African countries, more than 10% of adults used mobile money in 2011. Globally, Many developing countries lack the physical infrastructure there are 137 live mobile money deployments, with 95 mobile required to offer financial services, such as roads, bridges and money services in the planning stages. electricity. These issues make it cost-prohibitive for banks to set up branches in rural areas. Mobile phones enable banks to But the current mobile money ecosystem is siloed. Each mobile overcome these physical barriers. money service stands alone, with minimal interconnection to other services or to an international payment service. Even for banks willing to serve the unbanked, the fees necessary to cover the associated costs of serving them — particularly Despite its shortcomings, the current mobile money ecosystem people in rural areas — tend to be prohibitively high for the is maturing at a rapid rate. While others started the movement, target consumer. Variable costs for financial services tend to be it is now time for companies with years of IT, financial and based on number of transactions and not number of customers. mobile expertise to start playing a more significant role. The This is particular troublesome for those living on a low income, initial obvious players, MNOs and financial institutions, are who tend to perform frequent, low-value transactions. being joined by others, such as cell phone manufacturers, platform providers, service integrators and international Mobile money systems allow financial services to be provided payment providers. Each of these players is key to developing with low overhead and therefore at reasonable rates. Such and expanding the mobile money value chain, and leaders are systems also charge customers a fee per transaction, which emerging with the expertise, reputation and market power allows consumers to weigh the costs against the benefits of necessary to shape the market. frequent transactions and to determine their own personal optimal number of transactions. Whether a mobile money system is led solely by an MNO or through open partnerships, mobile money will always require a Mobile money and microfinance strong multiplayer ecosystem. However, for the mobile money For mobile money to be sustainable in the long term, it must market to maintain and expand its value proposition, these be profitable. It is estimated that up to 364 million low-income players will need to develop an open, interoperable ecosystem individuals will be utilizing mobile money by the end of 2012, based on a scalable, agile and cost-effective platform. which would generate $7.8 billion in revenue. In Kenya, the M-PESA mobile money service is the success case most often The future structure of the mobile money ecosystem is yet to referenced when discussing profitability. Offered by Safaricom, be determined. However, the potential for a unified ecosystem the country’s largest mobile network operator, M-PESA’s gross is already coming to fruition. Western Union has numerous revenues amounted to $157 million in 2010, up 56% from the partnerships established with international mobile network previous year. operators. Visa and MasterCard are already developing and supporting multiple mobile money services. As linkages with M-PESA accounts for 13.3% of Safaricom’s total revenue and international payment networks transform national mobile is a significant part of its operations. However, this level of money systems into a unified international mobile money profitability is thus far unique. The mobile money market ecosystem, the life-changing benefits of mobile money will is still very young, so while the potential exists, the level of truly be realized. profitability predicted is still to be achieved. When mobile money services were first offered by mobile network operators (MNO), they consisted of money transfer ERICA SALINAS is a strategy consultant in CSC’s Federal and payment systems. Then financial institutions soon began Consulting Practice, North American Public Sector. SUMMER 2012 | CSC WORLD 17

- 20. CONNECTED CONSUMER The Constantly A dramatic change is sweeping across the retail landscape. Connected Customers are adding smartphones and mobile devices to their shopping experience in your stores without your blessing. Your customers are using their own tools and apps to gather Customer information about products, brands, pricing and availability — and this could be sending sales to your competition. This change is more seismic than e-commerce. It introduces real-time digital interaction to the shopping experience. by John Gentry Customers like it. They feel in control. Yet, they have a set of expectations that go with it — expectations you need to meet. They are the Constantly Connected Customers, and right now they are unilaterally changing your relationship with them. Customer power Today’s Constantly Connected Customers are equipped with smartphones, tablets and other mobile devices. They engage with Twitter, Facebook and other social networks. And they can quickly and easily comment online — and read the comments of others — about their favorite (and not-so- favorite) retail brands. At stake is nothing less than control of the retailer-customer relationship. In the past, retailers held most of the cards, primarily controlling their relationship with the customer. Now, control of the relationship is quickly moving to the Constantly Connected Customer empowered by all of this technology. For most of our history, customers engaged with retailers through one or two channels: the brick-and-mortar retail store and the catalog. Over the past 15 years, retailers have expanded to four channels by adding online and mobile channels. Retailers have typically operated each of these channels separately, and this approach met customers’ needs for a while. 18 CSC WORLD | SUMMER 2012

- 21. But times are changing. Today, when Constantly Connected Retail Enterprise Intelligence Customers enter a brick-and-mortar store, the retailer does not necessarily recognize them or the extent of their relationship In the evolution of Web 1.0 to 2.0, those who began early with the retailer across all of its channels. Now a new challenge and learned about what works for their businesses and faces retailers: Offer a cross-channel view to customers, their stores gained market advantage. Companies that one that integrates mobile, online and the brick-and-mortar embraced e-commerce are already ahead, and many have channels into a complete, consistent and seamless shopping transformed processes and policies to enable profitable experience that increases sales. growth. No one can specify what the final digital shopping experience will be, but it is sure that those who are not In social media and on your own e-commerce site, Constantly experimenting and developing it now will miss a significant Connected Customers can now gather information to make business opportunity. purchase decisions regarding a brand without the brand’s involvement — a new and unprecedented situation. CSC is ready to help those retailers that see the opportunity. We can help you “get mobile” with industrial- For example, a customer could shop for a brand from his or grade, secure mobile apps to interact with your customers. her smartphone using nothing more sophisticated than a basic CSC can integrate that new “digital” location with the Web browser and common search engine. What’s more, the enterprise systems that feed it data, and operational search results will likely be displayed without any of the brand’s systems that fulfill, ship and bill the order. carefully crafted messaging. Our Enterprise Intelligence for Retail solution provides Cashing in the business intelligence tools you need to make sure that Retailers that cater successfully to the Constantly Connected your plans are working: if products are moving, if sales are Customer will reap significant competitive advantage. For one, up, and if service levels are honored. In short, if you are Constantly Connected Customers purchase more than their ready to embrace the value of the Constantly Connected less-wired counterparts. It’s all about basket size and lift — and Customer, CSC stands ready to help with proven capability. these customers will respond to better information and relevant promotions, spending more. Additionally, these customers Learn more at www.csc.com/retail. engage more strongly with their favored brands, translating into greater revenue over time. In a new IDC Retail Insights case study1, UK department store retailer John Lewis is reportedly reaping the benefits of catering to multi-channel shoppers. Among the findings: Over 60% of Connected Customers expect personalized treatment, their customers research online before going to the store, and advantageous promotional pricing, more product and service 40% use their phones to interact with the brand when in the information, and the ability to purchase online yet pick up store. Plus, the study says these multi-channel shoppers spend and return at the store. Simply put, they want the ability to 3.5 times more. buy anywhere, anytime and have it fulfilled anywhere — at competitive prices. Moreover, these customers create streams of digital information about how they browse the Web — and because of location- Constantly Connected Customers also share their unfiltered, aware smartphones — how they browse the store and the very sometimes negative, opinions of retail brands and stores. And shopping mall that contains that store. Combined with point-of- thanks to social media, they can share these views quickly and sale (POS) data, smart retailers can use this information to gain to a potentially large worldwide audience. Complaints, whether insights, improve operations, forecast demand and even create fair or not, can quickly go viral, dissuading thousands of other new products. consumers from purchasing a brand. You can’t control this, but you can mitigate it with active awareness of comments about Finally, Constantly Connected Customers provide more your brand. feedback than do other customers, essentially acting as a virtual focus group that provides an ongoing stream of quick On the upside, this same awareness can spot good comments reactions and suggestions. about your products or brand that create new opportunity for your business. Good or bad, it’s there, and there is a gold mine Higher expectations of value in the information. The emergence of the Constantly Connected Customer also 1 IDC-Insights-Community.com, analyst Christine Bardwell, John Lewis: Multichannel presents retailers with several challenges. Connected Customers shoppers spend 3.5 times more, May 17, 2012. expect more from retailers. There is more to it than offering a mobile version of your e-commerce site. Certainly this is a good place to get started, but as soon as you do it, your customers JOHN GENTRY is managing director of CSC’s Global Consumer move up the expectation curve. Products and Retail Group. SUMMER 2012 | CSC WORLD 19

- 22. Social Media Should Healthcare Organizations Use Social Media? by Jared Rhoads Social media has revolutionized the way people interact, and it is drastically changing the way healthcare organizations communicate with customers and accomplish their business objectives. On average, global consumers spend nearly a quarter of their online time using social media sites. One out of every seven minutes spent online is on Facebook, according to the research firm comScore. Leveraging the popularity of these and other sites can be advantageous for healthcare organizations. In our recent report, “Should Healthcare Organizations Use Social Media — a Global Update,” CSC’s Global Institute for Emerging Healthcare Practices describes best practices shared by early adopters around the world. The report shows that healthcare organizations are already taking advantage of social media to accomplish a number of strategic goals related to marketing, information sharing, engaging patients and encouraging innovation. 20 CSC WORLD | SUMMER 2012

- 23. External communications Belgium-based biopharmaceutical company UCB is one organiza- Social media can supplement an organization’s overall commu- tion that uses aggregated, de-identified patient data from these nication and marketing strategy. For instance, by maintaining sites (with patients’ permission) to look for new product ideas. a presence on Facebook, Twitter and YouTube, German drug maker Boehringer Ingelheim shares news, promotes events and The experiences of early adopters demonstrate that social public awareness campaigns, and presents the company to a media can be a valuable tool. Healthcare organizations that global audience. have not yet started to use social media should take the leap; if they wait, they may find themselves playing catch-up to Many hospitals have also launched Facebook pages to promote their competitors. their facilities. Some also use social media to facilitate patient engagement and care management, and to gain early feedback Our recommendations with regard to products in development. Organizations should develop an overall strategy that uses social media to help influence customers and accomplish strategic Facebook and Twitter have fostered the development of several healthcare goals. As healthcare organizations consider what to online health communities. In addition, a number of health-specif- do with and about social media, we offer the following advice: ic sites have been created to encourage information sharing and, especially, to provide a context for giving and getting support. 1. Don’t take a “wait-and-see approach.” Although some believe social media is a passing fad, we believe it is here Patient interactions to stay, and the sooner your organization develops an Physician-patient interaction on social media sites is a less com- active presence, the less distance you will have to make mon but growing phenomenon, as more patients are initiating up later. contact with their physicians through social media than ever 2. Establish a social media policy. At a minimum, this will before. Through patient networking sites such as PatientsLikeMe help protect against security, privacy or ethics breaches in the United States and HealthUnlocked in the United Kingdom, by your employees or customers. You should also offer patients and caregivers are forming communities of people with staff education. Training and outreach are necessary to like conditions, creating profiles to document details of their ensure that your staff fully understands and is able to health condition, sharing advice on treatments and providing carry out the policy. motivational support. 3. Follow your customers. Listen to what others are say- ing about your organization, your product(s) and your Early reports indicate that participation in online communities brand(s). Monitor the social media activities of others in can help educate and engage patients as well as encourage your market, and use social media to listen to what others healthy behaviors. For this reason, a number of groups are saying about your competition. encourage patients to participate in such interactions. Some 4. Consider starting where many organizations start. Use providers, such as Raboud University Nijmegen Medical Centre social media to enhance marketing, branding, recruitment, in the Netherlands and the Mayo Clinic in the United States, reputation management, customer relations and customer have launched their own online communities to promote service. However, educate yourself first on what is allow- patient interaction. able under existing laws in your country. 5. Start small and monitor outcomes. You don’t have to Some groups leverage online communities to connect patients develop a full-blown social media strategy now, but and providers, and to aid in care-management activities. How Are eventually you will need one. Ask yourself what your You, a website launched by the National Health Service (NHS) organization should be doing now to anticipate a wider Midlands East and Cambridge Healthcare, connects patients with use of social media to help accomplish key healthcare goals. their network of formal and informal (family) caregivers. 6. Recruit social media managers internally. Distribute responsibilities among staff that know your organization, The site prompts patients to enter periodic status updates are Internet-savvy and are excited about using social about how they are feeling, which are communicated to media to benefit your organization. Keep social media their followers. Tracking patient updates on the site helps content accurate and current. providers and loved ones monitor a patient’s well-being and recognize when an individual may need medical assistance or earn more at www.csc.com/health_services. L additional encouragement. Product development Patient communities can also help companies develop the next generation of prescription drugs and medical devices. Conver- sations on patient networking sites provide insight into disease progression, how medications and devices are used, their JARED RHOADS is a senior research analyst in CSC’s Global effectiveness, their side effects and unmet patient needs. Institute for Emerging Healthcare Practices. SUMMER 2012 | CSC WORLD 21

- 24. Social Media Social Business The Next Big Step by Mark Walton-Hayfield 22 CSC WORLD | SUMMER 2012