New base 29 august energy news issue 1066 by khaled al awadi-ilovepdf-com...

Oil And Gas Sector Industry

1. .'1 33

29 September 2010 | Industry Update

Oil and Gas Sector Maintain OVERWEIGHT

The making of a Premier Hub for Oil Services

Oil and gas initiatives. PEMANDU has identified 8 entry point projects (EPPs) under the oil and gas sector that may

potentially raise the nation’s gross national income (GNI) by RM26.8 billion by the year 2020. The specifics of the

EPPs will only be released on 26 October but the headlines plus our commentaries are as follows:

GROWTH IN UPSTREAM

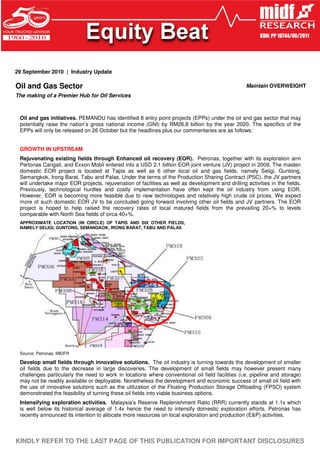

Rejuvenating existing fields through Enhanced oil recovery (EOR). Petronas, together with its exploration arm

Pertonas Carigali, and Exxon Mobil entered into a USD 2.1 billion EOR joint venture (JV) project in 2009. The maiden

domestic EOR project is located at Tapis as well as 6 other local oil and gas fields, namely Seligi, Guntong,

Semangkok, Irong Barat, Tabu and Palas. Under the terms of the Production Sharing Contract (PSC), the JV partners

will undertake major EOR projects, rejuvenation of facilities as well as development and drilling activities in the fields.

Previously, technological hurdles and costly implementation have often kept the oil industry from using EOR.

However, EOR is becoming more feasible due to new technologies and relatively high crude oil prices. We expect

more of such domestic EOR JV to be concluded going forward involving other oil fields and JV partners. The EOR

project is hoped to help raised the recovery rates of local matured fields from the prevailing 20+% to levels

comparable with North Sea fields of circa 40+%.

APPROXIMATE LOCATION (IN CIRCLE) OF TAPIS AND SIX OTHER FIELDS,

NAMELY SELIGI, GUNTONG, SEMANGKOK, IRONG BARAT, TABU AND PALAS

Source: Petronas, MIDFR

Develop small fields through innovative solutions. The oil industry is turning towards the development of smaller

oil fields due to the decrease in large discoveries. The development of small fields may however present many

challenges particularly the need to work in locations where conventional oil field facilities (i.e. pipeline and storage)

may not be readily available or deployable. Nonetheless the development and economic success of small oil field with

the use of innovative solutions such as the utilization of the Floating Production Storage Offloading (FPSO) system

demonstrated the feasibility of turning these oil fields into viable business options.

Intensifying exploration activities. Malaysia’s Reserve Replenishment Ratio (RRR) currently stands at 1.1x which

is well below its historical average of 1.4x hence the need to intensify domestic exploration efforts. Petronas has

recently announced its intention to allocate more resources on local exploration and production (E&P) activities.

KINDLY REFER TO THE LAST PAGE OF THIS PUBLICATION FOR IMPORTANT DISCLOSURES

2. 0,') (48,7< %($7

:HGQHVGD 6HSWHPEHU

Reserve Replenishment Ratios (RRR)

Year (FYE March) RRR

2006 1.80x

2007 1.40x

2008 0.90x

2009 1.80x

2010 1.10x

Source: Petronas

GROWTH IN DOWNSTREAM

Unlocking gas demand in Peninsular Malaysia. The domestic gas demand-supply equation will be driven mainly

by the depleting supply especially from Peninsular Malaysia fields. Sources indicate that the present offshore

Terengganu gas supply is estimated to suffice demand only until 2021, with first indication of reductions expected by

2017. Nevertheless, replenishment of new gas supply will be delivered from Petronas’ East Malaysia fields as well as

its Australian LNG development (Gladstone, Western Australia) comprising of bed-methene and coal seam gas. First

investment decision on the Australian LNG project is expected to be announced by 2011-12. The proposed re-

gasification plant located in Melaka will also act as an entry point to the external gas sources, hence addressing the

impending Peninsular Malaysia gas supply shortage. This will also unlock values from Petronas’ (via Petronas Gas)

present gas pipelines, emphasizing on the gas transmission business apart from its traditional processing business.

We view this beneficiary towards Petronas Gas, given it being the owner of Peninsula’s only gas pipeline system.

Building a regional oil storage and trading hub. A huge oil storage facility will be built next to neighboring

Singapore to form a regional oil products trading hub. While the exact location of the facility was undisclosed however

we believe it to be in Tanjung Bin, southwest of Johor (other location is in Tanjung Pengerang, southeast of Johor).

Vitol Tank Terminal International (VTTI), which is 50%-owned by MISC Berhad, is building a major new oil terminal in

Tanjung Bin with initial capacity of 750,000 cubic meters. Tanjung Bin is geographically strategic due to its close

proximity to Singapore tank terminals which are located mainly in Jurong, west of Singapore. This proximity may help

to facilitate convenient logistics and trade activities between the two oil storage centers. We believe this initiative

would be a boost for the domestic oil terminal business. Malaysian players will able to tap into Singapore’s proven oil

terminal market and shall present opportunities to widen our clientele networks.

MAKING MALAYSIA AS ASIA’S PREMIER HUB FOR OIL FIELD SERVICES

Consolidating the domestic fabricators. There are currently six Petronas-licensed major fabricators (see Table

below) in addition to other smaller companies. We reckon the proposed EPP would involve the merger or even

outright acquisition of smaller fabricators by the bigger players. Moreover we expect the three largest fabricators,

namely Malaysia Marine and Heavy Engineering (MMHE), Sime Darby Engineering (SDE) and Kencana Petroleum

(Kencana) to become the ‘anchors’ upon the consolidation of local oil field service industry. The consolidation exercise

is seen to help elevate the capacities of local oil field service companies thus increasing their likelihood of winning

major contracts locally and overseas.

Company Location Capacity (tpa)

MMHE Pasir Gudang, Johor 69,200

SDE Pasir Gudang / Teluk Ramunia, Johor 107,700

Kencana Lumut, Perak 48,000

OilFab Pulau Indah, Port Klang 16,000

Boustead Penang Shipyard Pulau Jerejak, Penang 9,000

Brooke Dockyard Sejingkat, Sarawak 5,000

Source: Petronas, MIDFR

2

3. 0,') (48,7< %($7

:HGQHVGD 6HSWHPEHU

Attracting MNCs to bring their global oil field service and equipment operations to Malaysia. The world’s

largest oil field service companies such as Schlumberger, Halliburton and Baker Hughes do currently have some

degrees of presence in Malaysia. However it is hoped that they will increase their scope of activities by bringing their

global oil field service and equipment to Malaysia. We opine that a well mapped out, orderly and robust development

of the local oil and gas industry is in itself a pull factor for these major players to choose Malaysia as their regional hub

and to increase their activities in the country. We view the EPPs as the catalysts for a more robust development of the

domestic oil and gas industry.

Developing engineering, procurement and installation capabilities and capacity through strategic

partnerships and joint ventures. Upon consolidation of the domestic oil field service players, the local ‘anchors’ will

be in more favourable positions of strength to enter into joint ventures as well as strategic partnerships with the world’s

largest oil field service companies. These arrangements may help to expedite the development of domestic

engineering, procurement and installation capabilities and capacity.

CONCLUSION

Most of the companies under our oil and gas sector coverage are oil field service contractors that will most likely

benefit from the increased activities particularly in the upstream oil and gas sector. The oil and gas initiatives which

pertain to the upstream and downstream growth of the domestic oil and gas sector are mostly ongoing but

nonetheless are now given more prominence with their inclusions in the EPP.

However the proposed strategic partnership and consolidation of the domestic fabricators as well as the efforts to

attract global oil field service companies to Malaysia are novel EPP ideas that are seen to help elevate the level of

competencies and competitiveness of the local oil field service and equipment sector and turning Malaysia into the

regional hub for oil field services.

Despite lacking in details, we view the EPPs positively as they are meant to provide the impetus for a more robust

development of the domestic oil and gas industry. Maintain OVERWEIGHT on the sector as we await further details

on the EPP initiatives.

3

4. 0,') (48,7< %($7

:HGQHVGD 6HSWHPEHU

MIDF RESEARCH is part of MIDF Amanah Investment Bank Berhad (23878 - X).

(Bank Pelaburan)

(A Participating Organisation of Bursa Malaysia Securities Berhad)

DISCLOSURES AND DISCLAIMER

This report has been prepared by MIDF AMANAH INVESTMENT BANK BERHAD (23878-X). It is for

distribution only under such circumstances as may be permitted by applicable law.

Readers should be fully aware that this report is for information purposes only. The opinions contained

in this report are based on information obtained or derived from sources that we believe are reliable.

MIDF AMANAH INVESTMENT BANK BERHAD makes no representation or warranty, expressed or

implied, as to the accuracy, completeness or reliability of the information contained therein and it should

not be relied upon as such.

This report is not, and should not be construed as, an offer to buy or sell any securities or other financial

instruments. The analysis contained herein is based on numerous assumptions. Different assumptions

could result in materially different results. All opinions and estimates are subject to change without

notice. The research analysts will initiate, update and cease coverage solely at the discretion of MIDF

AMANAH INVESTMENT BANK BERHAD.

The directors, employees and representatives of MIDF AMANAH INVESTMENT BANK BERHAD may

have interest in any of the securities mentioned and may benefit from the information herein. Members

of the MIDF Group and their affiliates may provide services to any company and affiliates of such

companies whose securities are mentioned herein This document may not be reproduced, distributed or

published in any form or for any purpose.

MIDF AMANAH INVESTMENT BANK : GUIDE TO RECOMMENDATIONS

STOCK RECOMMENDATIONS

BUY Total return is expected to be >15% over the next 12 months.

Stock price is expected to rise by >15% within 3-months after a Trading Buy rating has been

TRADING BUY

assigned due to positive newsflow.

NEUTRAL Total return is expected to be between -15% and +15% over the next 12 months.

SELL Total return is expected to be <-15% over the next 12 months.

Stock price is expected to fall by >15% within 3-months after a Trading Sell rating has been

TRADING SELL

assigned due to negative newsflow.

SECTOR RECOMMENDATIONS

POSITIVE The sector is expected to outperform the overall market over the next 12 months.

NEUTRAL The sector is to perform in line with the overall market over the next 12 months.

NEGATIVE The sector is expected to underperform the overall market over the next 12 months.

4