Get fully solved MBA assignments by subject code

•Download as DOCX, PDF•

0 likes•141 views

This document provides information about getting fully solved assignments for various MBA programs and semesters from an assignment help service. It lists the contact email and phone number and provides an example of an assignment question paper covering topics like taxation, capital gains, capital structure, service tax, and customs duty. Students are advised to contact the provided details to get their semester assignments solved and submit them.

Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (9)

Similar to Get fully solved MBA assignments by subject code

Similar to Get fully solved MBA assignments by subject code (20)

Get fully solved MBA assignments by subject code

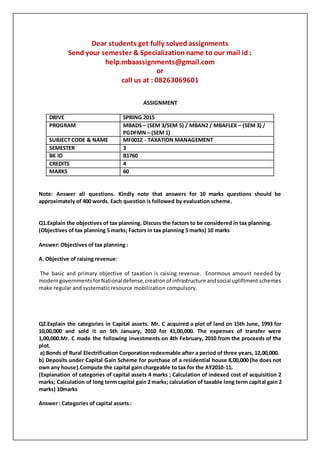

- 1. Dear students get fully solved assignments Send your semester & Specialization name to our mail id : help.mbaassignments@gmail.com or call us at : 08263069601 ASSIGNMENT DRIVE SPRING 2015 PROGRAM MBADS – (SEM 3/SEM 5) / MBAN2 / MBAFLEX – (SEM 3) / PGDFMN – (SEM 1) SUBJECT CODE & NAME MF0012 - TAXATION MANAGEMENT SEMESTER 3 BK ID B1760 CREDITS 4 MARKS 60 Note: Answer all questions. Kindly note that answers for 10 marks questions should be approximately of 400 words. Each question is followed by evaluation scheme. Q1.Explain the objectives of tax planning. Discuss the factors to be considered in tax planning. (Objectives of tax planning 5 marks; Factors in tax planning 5 marks) 10 marks Answer: Objectives of tax planning : A. Objective of raising revenue: The basic and primary objective of taxation is raising revenue. Enormous amount needed by moderngovernmentsforNationaldefense,creationof infrastructure andsocial upliftment schemes make regular and systematic resource mobilization compulsory. Q2.Explain the categories in Capital assets. Mr. C acquired a plot of land on 15th June, 1993 for 10,00,000 and sold it on 5th January, 2010 for 41,00,000. The expenses of transfer were 1,00,000.Mr. C made the following investments on 4th February, 2010 from the proceeds of the plot. a) Bonds of Rural Electrification Corporation redeemable after a period of three years, 12,00,000. b) Deposits under Capital Gain Scheme for purchase of a residential house 8,00,000 (he does not own any house).Compute the capital gain chargeable to tax for the AY2010-11. (Explanation of categories of capital assets 4 marks ; Calculation of indexed cost of acquisition 2 marks; Calculation of long term capital gain 2 marks; calculation of taxable long term capital gain 2 marks) 10marks Answer : Categories of capital assets :

- 2. 1. Collectibles : Long-terminvestmentsincollectiblesare taxedata flat28%. Short-terminvestments in collectibles are taxed as short-term capital gains at your ordinary income tax rates. Collectibles include the following items: stamps, Q3.Explain major considerationsin capital structure planning.Write about the dividend policy and factors affecting dividend decisions. (Explanation of factors of capital structure planning 6 marks; Explanation of dividend policy 2 marks; factors affecting dividend decisions 2 marks) 10marks Answer : Factors of capital structure planning : 1. Trading on Equity: The word “equity” denotes the ownership of the company. Trading on equity means taking advantage of equity share capital to borrowed funds on reasonable basis. It refers to additional profits that equity shareholders earn because of issuance of debentures and preference shares. 2. Degree of control: Q4.X Ltd. has UnitC which is not functioningsatisfactorily.The followingare the detailsof its fixed assets: Asset Date of acquisition Book value (Rs. lakh ) Land Goodwill (raised in books on 31st March, 2005) Machinery Plant 10th February, 2003 5th April, 1999 12th April, 2004 30 10 40 20 The written down value (WDV) is Rs. 25 lakh for the machinery, and Rs.15 lakh for the plant. The liabilities on this Unit on 31st March, 2011 are Rs.35 lakh. The following are two options as on 31st March, 2011: Option 1: Slump sale to Y Ltd for a consideration of 85 lakh. Option 2: Individual sale of assets as follows: Land Rs.48 lakh, goodwill Rs.20 lakh, machinery Rs.32 lakh, Plant Rs.17 lakh. The other units derive taxable income and there is no carry forward of loss or depreciation for the company as a whole. Unit C was started on 1st January, 2005. Which option would you choose, and why? (Computation of capital gain for both the options 4 marks; Computation of tax liability for both the options 4 marks ; Conclusion 2 marks) 10marks

- 3. Answer : Total price of the unit is : Option 1 : The net wealthof the undertaking(aggregatevalue of the total assets of the undertaking minus the value of the liabilities as appearing in books of accounts) shall be deemed to be the cost of acquisition and the cost of improvement for the Q5.Explain the Service Tax Law in India and concept of negative list. Write about the exemptions and rebates in Service Tax Law. (Explanation of Service Tax Law in India 5 marks; explanation of concept of negative list 2marks; Explanation of exemptions and rebates in Service Tax Law 3 marks) 10marks Answer : Service tax laws in India : Generally, the liability to pay service tax has been placed on the ‘service provider’. However, in respectof the taxable servicesnotifiedunderSec.68(2) of the Finance Act,1994, the service tax shall be paid by such person and in such manner as may be prescribed at the rate specified in Sec.66 of the Act and all the provisionsof Chapter-V shallapplytosuch person as if he is the person liable for paying the service tax. The following services have been notified under Sec.68(2) of Finance Act,1994: the services,- (i) in relation to telecommunication service Q6.What do you understand by customs duty? Explain the taxable events for imported, warehoused and exported goods. List down the types of duties in customs. An importer imports goods for subsequent sale in India at $10,000 on assessable value basis. Relevant exchange rate and rate of duty are as follows: Particulars Date Exchange Rate Declared by CBE&C Rate of Basic Customs Duty Date of submission of bill of entry 25th February, 2010 Rs.45/$ 8% Date of entry inwards granted to the vessel 5th March, 2010 Rs.49/$ 10% Calculate assessable value and customs duty. (Meaning and explanation of customs duty 2 marks; Explanation of taxable events for imported, warehoused and exported goods 3 marks; Listing of duties in customs 2 marks; Calculation of assessable value and customs duty 3marks) 10marks

- 4. Answer : Custom duty : A customsdutyis a tariff or tax on the importation (usually) or exportation (unusually) of goods. In the Kingdom of England, customs duties were typically part of the customary revenue of the king, and therefore didnotneedparliamentaryconsenttobe levied,unlike exciseduty, land tax, or other formsof taxes.Commercial goodsnotyetclearedthroughcustomsare heldinacustoms area, often called a bonded store, until processed. All Dear students get fully solved assignments Send your semester & Specialization name to our mail id : help.mbaassignments@gmail.com or call us at : 08263069601