Download free for 30 days

Sign in

Upload

Language (EN)

Support

Business

Mobile

Social Media

Marketing

Technology

Art & Photos

Career

Design

Education

Presentations & Public Speaking

Government & Nonprofit

Healthcare

Internet

Law

Leadership & Management

Automotive

Engineering

Software

Recruiting & HR

Retail

Sales

Services

Science

Small Business & Entrepreneurship

Food

Environment

Economy & Finance

Data & Analytics

Investor Relations

Sports

Spiritual

News & Politics

Travel

Self Improvement

Real Estate

Entertainment & Humor

Health & Medicine

Devices & Hardware

Lifestyle

Change Language

Language

English

Español

Português

Français

Deutsche

Cancel

Save

EN

Uploaded by

tusharnayak39

PPTX, PDF

10 views

Yield_Premiums_Unsecured_Bonds_India.pptx

Understanding yield premium on unsecured bonds in India

Economy & Finance

◦

Read more

0

Save

Share

Embed

Embed presentation

Download

Download to read offline

1

/ 8

2

/ 8

3

/ 8

4

/ 8

5

/ 8

6

/ 8

7

/ 8

8

/ 8

More Related Content

PDF

Artificial Intelligence, Data and Competition – SCHREPEL – June 2024 OECD dis...

by

OECD Directorate for Financial and Enterprise Affairs

PDF

How to Leverage AI to Boost Employee Wellness - Lydia Di Francesco - SocialHR...

by

SocialHRCamp

PDF

Storytelling For The Web: Integrate Storytelling in your Design Process

by

Chiara Aliotta

PDF

2024 State of Marketing Report – by Hubspot

by

Marius Sescu

PDF

2024 Trend Updates: What Really Works In SEO & Content Marketing

by

Search Engine Journal

PDF

Everything You Need To Know About ChatGPT

by

Expeed Software

PDF

Product Design Trends in 2024 | Teenage Engineerings

by

Pixeldarts

PPTX

PMS_AIF_AUM_Acquisition_Strategy_in_India.pptx

by

tusharnayak39

Artificial Intelligence, Data and Competition – SCHREPEL – June 2024 OECD dis...

by

OECD Directorate for Financial and Enterprise Affairs

How to Leverage AI to Boost Employee Wellness - Lydia Di Francesco - SocialHR...

by

SocialHRCamp

Storytelling For The Web: Integrate Storytelling in your Design Process

by

Chiara Aliotta

2024 State of Marketing Report – by Hubspot

by

Marius Sescu

2024 Trend Updates: What Really Works In SEO & Content Marketing

by

Search Engine Journal

Everything You Need To Know About ChatGPT

by

Expeed Software

Product Design Trends in 2024 | Teenage Engineerings

by

Pixeldarts

PMS_AIF_AUM_Acquisition_Strategy_in_India.pptx

by

tusharnayak39

Recently uploaded

PDF

Developing Soft Skills through Social Hackathons

by

GeorgeDiamandis11

PDF

India_Structural_Re-Rating_Beyond_Gold.pdf

by

ApoorvaRaval1

PDF

"Comprehensive Infographics on India's Budget 2026-2027: Key Reforms, Economi...

by

CA Suvidha Chaplot

PDF

The Blue Economy Paradox: Power, Survival, and Sustainability in the Indo-Pac...

by

Martin Koehring

PDF

"Comprehensive Overview of India's 2026-27 Budget: Fiscal Strategy, Tax Refor...

by

CA Suvidha Chaplot

DOCX

Buy Verified Binance Accounts with Guaranteed Security and Trust not risk .docx

by

marketing

PDF

Trade Facilitation Monitoring in Ukraine № 98

by

Інститут економічних досліджень та політичних консультацій

PDF

NVIDIA Corporation Leading the AI Revolution

by

DynamicDomain1

DOCX

11 Best Trusted Places to Buy Verified Remitly Accounts in 2026.docx

by

marketing

PPT

Mata Kuliah Pengauditan 1 pertemuan 1 ch01.ppt

by

farhandwinanda47

PDF

Financial Analysis Report ROCHE - Finance Club UoM.pdf

by

Finance Club UoM

PDF

10 Best Sites to Buy (X) Twitter Accounts for Sellers Top 11....pdf

by

marketing

PDF

apidays Paris 2025 | Building the API-Driven Future of European Payments

by

apidays

DOCX

Buy A Verified Remitly Account for Freelancers & Businesses.docx

by

marketing

PDF

SUB-SAHARAN AFRICA'S OIL SECTOR: SITUATION, DEVELOPMENTS AND PROSPECTS.pdf

by

Aurélie Dupassieux

PPTX

Dr. D. Sundari PRICING STRATEGIES ppt.pptx

by

DrSundariD

PDF

Bladex Earnings Call Presentation 4Q2025

by

Bladex

PPTX

Precious Metals Performance in 2025 and Outlook Outlook 2026

by

James Whitfield

PDF

Andhra Pradesh_Socio_Economic_Survey_2024_25.pdf

by

ssuser9d8e4e

PDF

Veritas Financial Statement presentation 2025

by

Veritas Eläkevakuutus - Veritas Pensionsförsäkring

Developing Soft Skills through Social Hackathons

by

GeorgeDiamandis11

India_Structural_Re-Rating_Beyond_Gold.pdf

by

ApoorvaRaval1

"Comprehensive Infographics on India's Budget 2026-2027: Key Reforms, Economi...

by

CA Suvidha Chaplot

The Blue Economy Paradox: Power, Survival, and Sustainability in the Indo-Pac...

by

Martin Koehring

"Comprehensive Overview of India's 2026-27 Budget: Fiscal Strategy, Tax Refor...

by

CA Suvidha Chaplot

Buy Verified Binance Accounts with Guaranteed Security and Trust not risk .docx

by

marketing

Trade Facilitation Monitoring in Ukraine № 98

by

Інститут економічних досліджень та політичних консультацій

NVIDIA Corporation Leading the AI Revolution

by

DynamicDomain1

11 Best Trusted Places to Buy Verified Remitly Accounts in 2026.docx

by

marketing

Mata Kuliah Pengauditan 1 pertemuan 1 ch01.ppt

by

farhandwinanda47

Financial Analysis Report ROCHE - Finance Club UoM.pdf

by

Finance Club UoM

10 Best Sites to Buy (X) Twitter Accounts for Sellers Top 11....pdf

by

marketing

apidays Paris 2025 | Building the API-Driven Future of European Payments

by

apidays

Buy A Verified Remitly Account for Freelancers & Businesses.docx

by

marketing

SUB-SAHARAN AFRICA'S OIL SECTOR: SITUATION, DEVELOPMENTS AND PROSPECTS.pdf

by

Aurélie Dupassieux

Dr. D. Sundari PRICING STRATEGIES ppt.pptx

by

DrSundariD

Bladex Earnings Call Presentation 4Q2025

by

Bladex

Precious Metals Performance in 2025 and Outlook Outlook 2026

by

James Whitfield

Andhra Pradesh_Socio_Economic_Survey_2024_25.pdf

by

ssuser9d8e4e

Veritas Financial Statement presentation 2025

by

Veritas Eläkevakuutus - Veritas Pensionsförsäkring

Featured

PDF

How Race, Age and Gender Shape Attitudes Towards Mental Health

by

ThinkNow

PDF

AI Trends in Creative Operations 2024 by Artwork Flow.pdf

by

marketingartwork

PDF

Skeleton Culture Code

by

Skeleton Technologies

PDF

PEPSICO Presentation to CAGNY Conference Feb 2024

by

Neil Kimberley

PDF

Content Methodology: A Best Practices Report (Webinar)

by

contently

PPTX

How to Prepare For a Successful Job Search for 2024

by

Albert Qian

PDF

Social Media Marketing Trends 2024 // The Global Indie Insights

by

Kurio // The Social Media Age(ncy)

PDF

Trends In Paid Search: Navigating The Digital Landscape In 2024

by

Search Engine Journal

PDF

5 Public speaking tips from TED - Visualized summary

by

SpeakerHub

PDF

ChatGPT and the Future of Work - Clark Boyd

by

Clark Boyd

PDF

Getting into the tech field. what next

by

Tessa Mero

PDF

Google's Just Not That Into You: Understanding Core Updates & Search Intent

by

Lily Ray

PDF

How to have difficult conversations

by

Rajiv Jayarajah, MAppComm, ACC

PDF

Introduction to Data Science

by

Christy Abraham Joy

PDF

Time Management & Productivity - Best Practices

by

Vit Horky

PDF

The six step guide to practical project management

by

MindGenius

PDF

Beginners Guide to TikTok for Search - Rachel Pearson - We are Tilt __ Bright...

by

RachelPearson36

PDF

Unlocking the Power of ChatGPT and AI in Testing - A Real-World Look, present...

by

Applitools

PDF

12 Ways to Increase Your Influence at Work

by

GetSmarter

PDF

ChatGPT webinar slides

by

Alireza Esmikhani

How Race, Age and Gender Shape Attitudes Towards Mental Health

by

ThinkNow

AI Trends in Creative Operations 2024 by Artwork Flow.pdf

by

marketingartwork

Skeleton Culture Code

by

Skeleton Technologies

PEPSICO Presentation to CAGNY Conference Feb 2024

by

Neil Kimberley

Content Methodology: A Best Practices Report (Webinar)

by

contently

How to Prepare For a Successful Job Search for 2024

by

Albert Qian

Social Media Marketing Trends 2024 // The Global Indie Insights

by

Kurio // The Social Media Age(ncy)

Trends In Paid Search: Navigating The Digital Landscape In 2024

by

Search Engine Journal

5 Public speaking tips from TED - Visualized summary

by

SpeakerHub

ChatGPT and the Future of Work - Clark Boyd

by

Clark Boyd

Getting into the tech field. what next

by

Tessa Mero

Google's Just Not That Into You: Understanding Core Updates & Search Intent

by

Lily Ray

How to have difficult conversations

by

Rajiv Jayarajah, MAppComm, ACC

Introduction to Data Science

by

Christy Abraham Joy

Time Management & Productivity - Best Practices

by

Vit Horky

The six step guide to practical project management

by

MindGenius

Beginners Guide to TikTok for Search - Rachel Pearson - We are Tilt __ Bright...

by

RachelPearson36

Unlocking the Power of ChatGPT and AI in Testing - A Real-World Look, present...

by

Applitools

12 Ways to Increase Your Influence at Work

by

GetSmarter

ChatGPT webinar slides

by

Alireza Esmikhani

Yield_Premiums_Unsecured_Bonds_India.pptx

1.

Understanding Yield Premiums

on Unsecured Bonds in India • Context: Private Placements & Public Issues

2.

What is a

Yield Premium? • - Extra return for holding unsecured vs secured bonds • - Compensates for higher credit risk & lower recovery • - Typically measured as a spread over secured bond yield

3.

Key Drivers of

Yield Premium • Recovery Rate: Lower recovery = Higher spread • Default Probability: Higher PD = Higher spread • Rating Notch Difference: Lower rating = Higher spread • Subordination Level: Lower seniority = Higher spread

4.

Market Dynamics &

Structural Risks • - Liquidity: Less tradability in unsecured bonds increases yield demand • - Investor Base: PFs, insurers prefer secured instruments • - Covenants & Trustee Rights: Stronger protections lower spreads

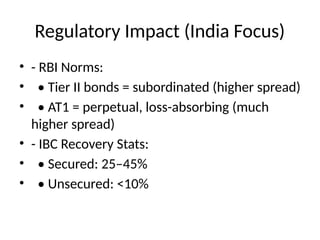

5.

Regulatory Impact (India

Focus) • - RBI Norms: • • Tier II bonds = subordinated (higher spread) • • AT1 = perpetual, loss-absorbing (much higher spread) • - IBC Recovery Stats: • • Secured: 25–45% • • Unsecured: <10%

6.

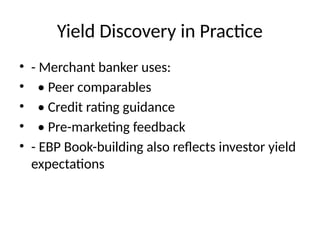

Yield Discovery in

Practice • - Merchant banker uses: • • Peer comparables • • Credit rating guidance • • Pre-marketing feedback • - EBP Book-building also reflects investor yield expectations

7.

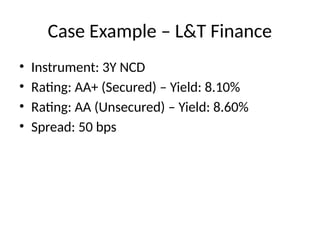

Case Example –

L&T Finance • Instrument: 3Y NCD • Rating: AA+ (Secured) – Yield: 8.10% • Rating: AA (Unsecured) – Yield: 8.60% • Spread: 50 bps

8.

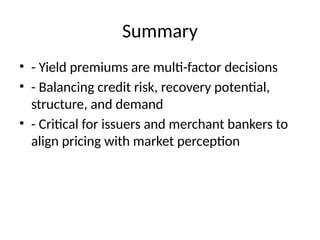

Summary • - Yield

premiums are multi-factor decisions • - Balancing credit risk, recovery potential, structure, and demand • - Critical for issuers and merchant bankers to align pricing with market perception

Download