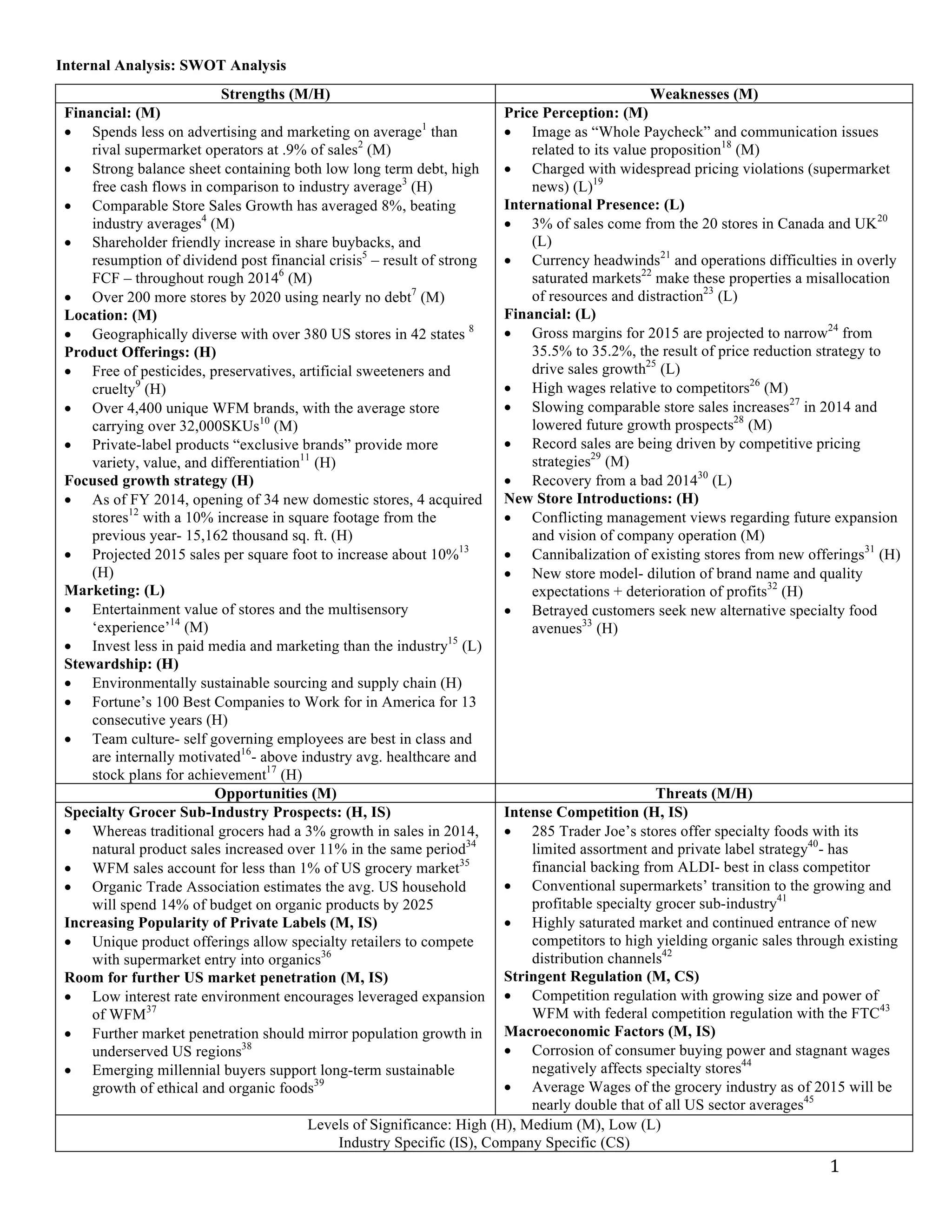

This strategic analysis focuses on Whole Foods Market (WFM) through internal and external frameworks, including SWOT, VRIO, and a six forces analysis. Key findings highlight WFM's strengths as a growing industry leader and its challenges such as pressured profit margins and increased competition. The report provides strategic recommendations to leverage WFM's financial strength and capitalize on market opportunities while addressing potential threats.

![17

"Publix Super Markets." Publix Super Markets. Accessed May 21, 2015.

http://supermarketnews.com/publix-super-markets. [growth comperable]

"Grocery Market Sales per Employee." Revenue per Employee (WFM), Sales per Employee, Current

and Historic Results, Rankings and More, Quarterly Fundamentals. Accessed May 21, 2015.

http://csimarket.com/stocks/singleEfficiencyet.php?code=WFM.

J5- "Whole Foods Market Reports First Quarter Results." Accessed May 21, 2015.

http://www.wholefoodsmarket.com/sites/default/files/media/Global/Company Info/PDFs/WFM-

2014-Q1-financial.pdf.

Whole Foods Market, 2014 Annual Report. http://www.mergentonline.com.lib.pepperdine.edu/

documents.php?compnumber=71872, accessed May 2015.

Walmart. 2014 Annual Report. http://www.mergentonline.com.lib.pepperdine.edu/documents

.php?compnumber=8865

Sprouts Farmers Market. 2014 Annual Report. http://www.mergentonline.com.lib.pepperdine.

edu/documents.php?compnumber=136871

The Fresh Market. 2014 Annual Report. http://www.mergentonline.com.lib.pepperdine.edu

/documents.php?compnumber=130261

Kroger Co. 2014 Annual Report. http://www.mergentonline.com.lib.pepperdine.edu

/documents.php?compnumber=4788

Hoover’s Company Records- In-depth Records of Whole Foods Market, Inc, via LexisNexis, accessed

May 2015.

Hoover’s Company Records- In-depth Records of Sprouts Farmers Market, Inc, via LexisNexis,

accessed May 2015.

Hoover’s Industry Snapshots, 2015, Speciality Food Stores, via LexisNexis, accessed May 2015.](https://image.slidesharecdn.com/finalversion-sherrer-businesspolicy-wfmindividualcase-170205012119/75/Whole-Foods-Market-WFM-Internal-and-External-Marketing-Analysis-Strategic-Recommendation-19-2048.jpg)

![[Entertainment Management]Polyphonic HMI](https://cdn.slidesharecdn.com/ss_thumbnails/13polyphonic-hmipresentation-1221293607726235-8-thumbnail.jpg?width=640&height=640&fit=bounds)