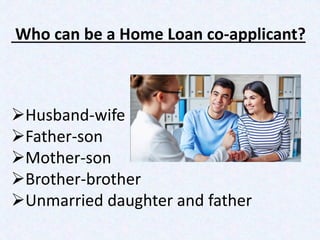

Who Can be Home Loan Co-applicant?

•

0 likes•19 views

A Home Loan is a huge responsibility. But, with a co-applicant you can share this responsibility and ease the financial burden.

Report

Share

Report

Share

Download to read offline

Recommended

Types of Life Insurance Policies Available in India

Life Insurance policy- Different types of life insurance Plans explained like Risk, Benefits of Term Plan, Whole life Plan, Endowment Plan, ULIP Plans, Money Back Policy, Child Policy & Annuity Plan available in India.

Understanding the Concept of Foir

What is Fixed Obligations to Income Ratio or FOIR? How can it impact your loan eligibility? Read on to know these answers.

Your personal loan rejection reasons may be one, few or all of the following

Banks may reject personal loan applications for several reasons including insufficient or unstable income, having too much existing debt from other loans, a poor credit history including many past loan rejections, or a history of frequently applying for loans.

Avoid making these mistakes when you apply for a personal loan

Borrow only what you can afford to repay, take time to compare loan options instead of rushing a decision, provide all requested information to the bank as they need it to evaluate your application, and make sure you understand the bank's application process and requirements before applying for a personal loan.

10 reasons to apply for a personal loan

This document lists 10 reasons to apply for a personal loan, including using the funds to pay off credit card or other debts, finance education or medical expenses, cover overdue bills, fund home renovations or vacations, or pay for weddings or new equipment.

5 myth

The document discusses 5 common myths about credit scores in India and provides facts to debunk each one. Specifically, it notes that building credit regularly through on-time payments can improve one's score, that annual credit reports don't hurt scores, that closing old accounts can reduce available credit and lower scores, that a mix of secured and unsecured loans is best, and that being a guarantor on a loan does impact one's liability and score.

Single women home loan borower

This 6-step strategy provides guidance for single women seeking a home loan. It advises determining an affordable loan amount, saving for a down payment, improving your credit score, utilizing government benefits, researching women-focused loan programs, and planning for unexpected costs.

Opt for a joint home loan

Opting for a joint home loan allows two individuals to purchase a home together, providing benefits such as higher loan eligibility due to combined incomes, the ability to make a larger down payment, sharing the responsibility of loan repayment, special interest rates when one applicant is a woman, and greater tax benefits from the joint ownership of the property.

Recommended

Types of Life Insurance Policies Available in India

Life Insurance policy- Different types of life insurance Plans explained like Risk, Benefits of Term Plan, Whole life Plan, Endowment Plan, ULIP Plans, Money Back Policy, Child Policy & Annuity Plan available in India.

Understanding the Concept of Foir

What is Fixed Obligations to Income Ratio or FOIR? How can it impact your loan eligibility? Read on to know these answers.

Your personal loan rejection reasons may be one, few or all of the following

Banks may reject personal loan applications for several reasons including insufficient or unstable income, having too much existing debt from other loans, a poor credit history including many past loan rejections, or a history of frequently applying for loans.

Avoid making these mistakes when you apply for a personal loan

Borrow only what you can afford to repay, take time to compare loan options instead of rushing a decision, provide all requested information to the bank as they need it to evaluate your application, and make sure you understand the bank's application process and requirements before applying for a personal loan.

10 reasons to apply for a personal loan

This document lists 10 reasons to apply for a personal loan, including using the funds to pay off credit card or other debts, finance education or medical expenses, cover overdue bills, fund home renovations or vacations, or pay for weddings or new equipment.

5 myth

The document discusses 5 common myths about credit scores in India and provides facts to debunk each one. Specifically, it notes that building credit regularly through on-time payments can improve one's score, that annual credit reports don't hurt scores, that closing old accounts can reduce available credit and lower scores, that a mix of secured and unsecured loans is best, and that being a guarantor on a loan does impact one's liability and score.

Single women home loan borower

This 6-step strategy provides guidance for single women seeking a home loan. It advises determining an affordable loan amount, saving for a down payment, improving your credit score, utilizing government benefits, researching women-focused loan programs, and planning for unexpected costs.

Opt for a joint home loan

Opting for a joint home loan allows two individuals to purchase a home together, providing benefits such as higher loan eligibility due to combined incomes, the ability to make a larger down payment, sharing the responsibility of loan repayment, special interest rates when one applicant is a woman, and greater tax benefits from the joint ownership of the property.

How do you calculate hl eligibility

To determine home loan eligibility, banks consider an applicant's current income, age, employment history, existing loan obligations, credit history and score, property value, location, and legal status to assess repayment ability and collateral risks.

Documents required for home loan

To apply for a home loan, applicants must provide documents to verify their identity such as a PAN card, Aadhaar card, voter ID, driving license or passport. Address proof documents include a registered rent agreement, Aadhaar card, driving license, lease agreement, passport or latest utility bill. Both salaried and self-employed applicants must also provide financial documents such as salary slips, bank statements, tax returns, profit/loss statements, and business registration certificates. Additional documents include a filled loan application, photographs, property documents, encumbrance certificates, and property tax receipts.

Travel Credit Cards For You

There are credit cards designed exclusively for a definite purpose. One such credit card is travel credit card which helps you enjoy travel benefits.

Documents required for home loan

To apply for a home loan, applicants must provide documents to verify their identity such as a PAN card, Aadhaar card, voter ID, driving license or passport. Address proof documents include a registered rent agreement, Aadhaar card, driving license, lease agreement, passport or latest utility bill. Both salaried and self-employed applicants must also provide financial documents such as salary slips, bank statements, tax returns, profit/loss statements, and business registration certificates. Additional documents include a filled loan application, photographs, property documents, encumbrance certificates, and property tax receipts.

Benefits of loans with longer tenures

Longer loan tenures offer borrowers higher loan eligibility which allows them to borrow more money, lower equal monthly installments (EMIs) since repayments are spread over a longer period, and more flexible repayment terms including the option to extend income tax benefits as interest payments are deductible over a longer period.

Benefits of availing a home loan

Taking out a home loan provides several benefits such as helping accomplish the dream of home ownership. It allows people to purchase a home now while interest rates are low and property values continue to appreciate over time. Home loans also offer tax benefits, allowing borrowers to deduct interest repayments and principal repayments from their taxable income each year.

9 must know things before you apply for a home loan

To apply for a home loan, you need to understand your eligibility, the types of loans available, get pre-approval for the amount needed and analyze total costs including insurance. You should also understand how EMIs work, choose the right loan tenure, gather required documents, and take out insurance.

5 ways to avoid home loan remeasures

Buy a home through a reputable realtor, choose a resale home over new construction, thoroughly inspect any home before purchasing, and avoid viewing other houses or overpaying once you have made an offer to reduce chances of post-purchase regret.

5 types for happy borrowing

Borrow only what you can comfortably repay, opt for short loan tenures, only borrow when necessary, look for better loan offers, and replace high-cost loans with lower-cost options to have a happy borrowing experience.

5 types to apply home loan

Before applying for a home loan, consider your borrowing needs, eligibility, loan offers from multiple lenders, carefully reading agreements, and choosing an appropriate loan tenure based on your repayment ability.

5 critical factors that impact your loan approval

The document outlines 5 critical factors that impact loan approval: 1) outstanding loan balance should be maintained between 20-30% of the total limit to demonstrate good credit management, 2) repayment history shows an applicant's ability and willingness to repay loans on time with delays over a month raising red flags, 3) lenders prefer to see a mix of secured and unsecured accounts that are all repaid, 4) a longer loan history is better but new borrowers must establish a 6 month track record, 5) avoid unnecessary credit applications and maintain responsible credit utilization.

4 home loan

The Reserve Bank of India plans to raise interest rates, so consumers are advised to apply now for home loans offering rates starting from 8.50% that provide up to Rs. 75 lakhs in funding with minimal processing fees and special rates for women and senior citizens.

5 best premim credit card

do you get short of cash at the end of every month because the salary is late! the credit card is the best alternative

Types of business loans

This document outlines 6 types of business loans: term loans, loans against property, loans against shares or financial securities, cash credit facilities, letter of credit facilities, and bank guarantees. These loans provide businesses with different financing options secured by property, shares, or backed by bank guarantees.

Top 5 types of business loans in india

these are many purpose one should take a business loan some of them are in the following presentation

How to improve your business loan approval chances

there are a lot of factors that can effect your business loan approve conciser the following things for same!

Dos n donts to follow if uh are appling for a home loan

Are you applying for home loan for the first time! so here are some dos and donts you should follow if you are applying for home loan

Business loan eligibility

To be eligible for a business loan, applicants must be between 21-65 years old, have a profitable sole proprietorship, partnership firm, private limited company, closely held public listed company, or society/trust that has been profitable for at least 3 consecutive years. Applicants must also provide complete and accurate financial documents including balance sheets, profit and loss statements from the last 2 years as well as tax audit reports, and have a good credit score of 650 or above.

7 reasons why lenders turn down business loan applications

Lenders often turn down business loan applications for several key reasons: having a low personal credit score, incomplete paperwork or not requesting enough funding, operating in a high-risk industry, lacking collateral, high existing debt levels, or applying for multiple loans simultaneously.

7 instances when a credit card make more sense than a small business loan hold

A business credit card may be preferable to a small business loan for new businesses, when avoiding interest payments or fees, if collateral is not available, to provide credit options for employees, or to take advantage of perks like rewards programs. A business credit card offers no-interest promotional financing, avoids the need for collateral unlike a loan, and can be used to give credit to employees or take advantage of rewards benefits.

1比1复刻(ksu毕业证书)美国堪萨斯州立大学毕业证本科文凭证书原版一模一样

原版定制【微信:bwp0011】《(ksu毕业证书)美国堪萨斯州立大学毕业证本科文凭证书》【微信:bwp0011】成绩单 、雅思、外壳、留信学历认证永久存档查询,采用学校原版纸张、特殊工艺完全按照原版一比一制作(包括:隐形水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠,文字图案浮雕,激光镭射,紫外荧光,温感,复印防伪)行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备,十五年致力于帮助留学生解决难题,业务范围有加拿大、英国、澳洲、韩国、美国、新加坡,新西兰等学历材料,包您满意。

【业务选择办理准则】

一、工作未确定,回国需先给父母、亲戚朋友看下文凭的情况,办理一份就读学校的毕业证【微信bwp0011】文凭即可

二、回国进私企、外企、自己做生意的情况,这些单位是不查询毕业证真伪的,而且国内没有渠道去查询国外文凭的真假,也不需要提供真实教育部认证。鉴于此,办理一份毕业证【微信bwp0011】即可

三、进国企,银行,事业单位,考公务员等等,这些单位是必需要提供真实教育部认证的,办理教育部认证所需资料众多且烦琐,所有材料您都必须提供原件,我们凭借丰富的经验,快捷的绿色通道帮您快速整合材料,让您少走弯路。

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

【关于价格问题(保证一手价格)】

我们所定的价格是非常合理的,而且我们现在做得单子大多数都是代理和回头客户介绍的所以一般现在有新的单子 我给客户的都是第一手的代理价格,因为我想坦诚对待大家 不想跟大家在价格方面浪费时间

对于老客户或者被老客户介绍过来的朋友,我们都会适当给一些优惠。

Economic Risk Factor Update: June 2024 [SlideShare]

May’s reports showed signs of continued economic growth, said Sam Millette, director, fixed income, in his latest Economic Risk Factor Update.

For more market updates, subscribe to The Independent Market Observer at https://blog.commonwealth.com/independent-market-observer.

More Related Content

More from MyMoneyMantra

How do you calculate hl eligibility

To determine home loan eligibility, banks consider an applicant's current income, age, employment history, existing loan obligations, credit history and score, property value, location, and legal status to assess repayment ability and collateral risks.

Documents required for home loan

To apply for a home loan, applicants must provide documents to verify their identity such as a PAN card, Aadhaar card, voter ID, driving license or passport. Address proof documents include a registered rent agreement, Aadhaar card, driving license, lease agreement, passport or latest utility bill. Both salaried and self-employed applicants must also provide financial documents such as salary slips, bank statements, tax returns, profit/loss statements, and business registration certificates. Additional documents include a filled loan application, photographs, property documents, encumbrance certificates, and property tax receipts.

Travel Credit Cards For You

There are credit cards designed exclusively for a definite purpose. One such credit card is travel credit card which helps you enjoy travel benefits.

Documents required for home loan

To apply for a home loan, applicants must provide documents to verify their identity such as a PAN card, Aadhaar card, voter ID, driving license or passport. Address proof documents include a registered rent agreement, Aadhaar card, driving license, lease agreement, passport or latest utility bill. Both salaried and self-employed applicants must also provide financial documents such as salary slips, bank statements, tax returns, profit/loss statements, and business registration certificates. Additional documents include a filled loan application, photographs, property documents, encumbrance certificates, and property tax receipts.

Benefits of loans with longer tenures

Longer loan tenures offer borrowers higher loan eligibility which allows them to borrow more money, lower equal monthly installments (EMIs) since repayments are spread over a longer period, and more flexible repayment terms including the option to extend income tax benefits as interest payments are deductible over a longer period.

Benefits of availing a home loan

Taking out a home loan provides several benefits such as helping accomplish the dream of home ownership. It allows people to purchase a home now while interest rates are low and property values continue to appreciate over time. Home loans also offer tax benefits, allowing borrowers to deduct interest repayments and principal repayments from their taxable income each year.

9 must know things before you apply for a home loan

To apply for a home loan, you need to understand your eligibility, the types of loans available, get pre-approval for the amount needed and analyze total costs including insurance. You should also understand how EMIs work, choose the right loan tenure, gather required documents, and take out insurance.

5 ways to avoid home loan remeasures

Buy a home through a reputable realtor, choose a resale home over new construction, thoroughly inspect any home before purchasing, and avoid viewing other houses or overpaying once you have made an offer to reduce chances of post-purchase regret.

5 types for happy borrowing

Borrow only what you can comfortably repay, opt for short loan tenures, only borrow when necessary, look for better loan offers, and replace high-cost loans with lower-cost options to have a happy borrowing experience.

5 types to apply home loan

Before applying for a home loan, consider your borrowing needs, eligibility, loan offers from multiple lenders, carefully reading agreements, and choosing an appropriate loan tenure based on your repayment ability.

5 critical factors that impact your loan approval

The document outlines 5 critical factors that impact loan approval: 1) outstanding loan balance should be maintained between 20-30% of the total limit to demonstrate good credit management, 2) repayment history shows an applicant's ability and willingness to repay loans on time with delays over a month raising red flags, 3) lenders prefer to see a mix of secured and unsecured accounts that are all repaid, 4) a longer loan history is better but new borrowers must establish a 6 month track record, 5) avoid unnecessary credit applications and maintain responsible credit utilization.

4 home loan

The Reserve Bank of India plans to raise interest rates, so consumers are advised to apply now for home loans offering rates starting from 8.50% that provide up to Rs. 75 lakhs in funding with minimal processing fees and special rates for women and senior citizens.

5 best premim credit card

do you get short of cash at the end of every month because the salary is late! the credit card is the best alternative

Types of business loans

This document outlines 6 types of business loans: term loans, loans against property, loans against shares or financial securities, cash credit facilities, letter of credit facilities, and bank guarantees. These loans provide businesses with different financing options secured by property, shares, or backed by bank guarantees.

Top 5 types of business loans in india

these are many purpose one should take a business loan some of them are in the following presentation

How to improve your business loan approval chances

there are a lot of factors that can effect your business loan approve conciser the following things for same!

Dos n donts to follow if uh are appling for a home loan

Are you applying for home loan for the first time! so here are some dos and donts you should follow if you are applying for home loan

Business loan eligibility

To be eligible for a business loan, applicants must be between 21-65 years old, have a profitable sole proprietorship, partnership firm, private limited company, closely held public listed company, or society/trust that has been profitable for at least 3 consecutive years. Applicants must also provide complete and accurate financial documents including balance sheets, profit and loss statements from the last 2 years as well as tax audit reports, and have a good credit score of 650 or above.

7 reasons why lenders turn down business loan applications

Lenders often turn down business loan applications for several key reasons: having a low personal credit score, incomplete paperwork or not requesting enough funding, operating in a high-risk industry, lacking collateral, high existing debt levels, or applying for multiple loans simultaneously.

7 instances when a credit card make more sense than a small business loan hold

A business credit card may be preferable to a small business loan for new businesses, when avoiding interest payments or fees, if collateral is not available, to provide credit options for employees, or to take advantage of perks like rewards programs. A business credit card offers no-interest promotional financing, avoids the need for collateral unlike a loan, and can be used to give credit to employees or take advantage of rewards benefits.

More from MyMoneyMantra (20)

9 must know things before you apply for a home loan

9 must know things before you apply for a home loan

How to improve your business loan approval chances

How to improve your business loan approval chances

Dos n donts to follow if uh are appling for a home loan

Dos n donts to follow if uh are appling for a home loan

7 reasons why lenders turn down business loan applications

7 reasons why lenders turn down business loan applications

7 instances when a credit card make more sense than a small business loan hold

7 instances when a credit card make more sense than a small business loan hold

Recently uploaded

1比1复刻(ksu毕业证书)美国堪萨斯州立大学毕业证本科文凭证书原版一模一样

原版定制【微信:bwp0011】《(ksu毕业证书)美国堪萨斯州立大学毕业证本科文凭证书》【微信:bwp0011】成绩单 、雅思、外壳、留信学历认证永久存档查询,采用学校原版纸张、特殊工艺完全按照原版一比一制作(包括:隐形水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠,文字图案浮雕,激光镭射,紫外荧光,温感,复印防伪)行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备,十五年致力于帮助留学生解决难题,业务范围有加拿大、英国、澳洲、韩国、美国、新加坡,新西兰等学历材料,包您满意。

【业务选择办理准则】

一、工作未确定,回国需先给父母、亲戚朋友看下文凭的情况,办理一份就读学校的毕业证【微信bwp0011】文凭即可

二、回国进私企、外企、自己做生意的情况,这些单位是不查询毕业证真伪的,而且国内没有渠道去查询国外文凭的真假,也不需要提供真实教育部认证。鉴于此,办理一份毕业证【微信bwp0011】即可

三、进国企,银行,事业单位,考公务员等等,这些单位是必需要提供真实教育部认证的,办理教育部认证所需资料众多且烦琐,所有材料您都必须提供原件,我们凭借丰富的经验,快捷的绿色通道帮您快速整合材料,让您少走弯路。

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

【关于价格问题(保证一手价格)】

我们所定的价格是非常合理的,而且我们现在做得单子大多数都是代理和回头客户介绍的所以一般现在有新的单子 我给客户的都是第一手的代理价格,因为我想坦诚对待大家 不想跟大家在价格方面浪费时间

对于老客户或者被老客户介绍过来的朋友,我们都会适当给一些优惠。

Economic Risk Factor Update: June 2024 [SlideShare]

May’s reports showed signs of continued economic growth, said Sam Millette, director, fixed income, in his latest Economic Risk Factor Update.

For more market updates, subscribe to The Independent Market Observer at https://blog.commonwealth.com/independent-market-observer.

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strate...

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strategies

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strate...

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strategies

一比一原版(RMIT毕业证)皇家墨尔本理工大学毕业证如何办理

RMIT硕士学位证成绩单【微信95270640】《皇家墨尔本理工大学毕业证书》《QQ微信95270640》学位证书电子版:在线制作皇家墨尔本理工大学毕业证成绩单GPA修改(制作RMIT毕业证成绩单RMIT文凭证书样本)、皇家墨尔本理工大学毕业证书与成绩单样本图片、《RMIT学历证书学位证书》、皇家墨尔本理工大学毕业证案例毕业证书制作軟體、在线制作加拿大硕士学历证书真实可查.

【本科硕士】皇家墨尔本理工大学皇家墨尔本理工大学本科学位证成绩单(GPA修改);学历认证(教育部认证);大学Offer录取通知书留信认证使馆认证;雅思语言证书等高仿类证书。

办理流程:

1客户提供办理皇家墨尔本理工大学皇家墨尔本理工大学本科学位证成绩单信息:姓名生日专业学位毕业时间等(如信息不确定可以咨询顾问:我们有专业老师帮你查询);

2开始安排制作毕业证成绩单电子图;

3毕业证成绩单电子版做好以后发送给您确认;

4毕业证成绩单电子版您确认信息无误之后安排制作成品;

5成品做好拍照或者视频给您确认;

6快递给客户(国内顺丰国外DHLUPS等快读邮寄)

真实网上可查的证明材料

1教育部学历学位认证留服官网真实存档可查永久存档。

2留学回国人员证明(使馆认证)使馆网站真实存档可查。

我们对海外大学及学院的毕业证成绩单所使用的材料尺寸大小防伪结构(包括:皇家墨尔本理工大学皇家墨尔本理工大学本科学位证成绩单隐形水印阴影底纹钢印LOGO烫金烫银LOGO烫金烫银复合重叠。文字图案浮雕激光镭射紫外荧光温感复印防伪)都有原版本文凭对照。质量得到了广大海外客户群体的认可同时和海外学校留学中介做到与时俱进及时掌握各大院校的(毕业证成绩单资格证结业证录取通知书在读证明等相关材料)的版本更新信息能够在第一时间掌握最新的海外学历文凭的样版尺寸大小纸张材质防伪技术等等并在第一时间收集到原版实物以求达到客户的需求。

本公司还可以按照客户原版印刷制作且能够达到客户理想的要求。有需要办理证件的客户请联系我们在线客服中心微信:95270640 或咨询在线父亲的家很狭小除了一张单人床和一张小方桌几乎没有多余的空间山娃一下子就联想起学校的男小便处山娃很想笑却怎么也笑不出来山娃很迷惑父亲的家除了一扇小铁门连窗户也没有墓穴一般阴森森有些骇人父亲的城也便成了山娃的城父亲的家也便成了山娃的家父亲让山娃呆在屋里做作业看电视最多只能在门口透透气不能跟陌生人搭腔更不能乱跑一怕迷路二怕拐子拐人山娃很惊惧去年村里的田鸡就因为跟父亲进城一不小心被人拐跑了至今不见踪影害不

快速办理(美国Fordham毕业证书)福德汉姆大学毕业证学历证书一模一样

学校原件一模一样【微信:741003700 】《(美国Fordham毕业证书)福德汉姆大学毕业证学历证书》【微信:741003700 】学位证,留信认证(真实可查,永久存档)原件一模一样纸张工艺/offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原。

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

【主营项目】

一.毕业证【q微741003700】成绩单、使馆认证、教育部认证、雅思托福成绩单、学生卡等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

如果您处于以下几种情况:

◇在校期间,因各种原因未能顺利毕业……拿不到官方毕业证【q/微741003700】

◇面对父母的压力,希望尽快拿到;

◇不清楚认证流程以及材料该如何准备;

◇回国时间很长,忘记办理;

◇回国马上就要找工作,办给用人单位看;

◇企事业单位必须要求办理的

◇需要报考公务员、购买免税车、落转户口

◇申请留学生创业基金

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

Does teamwork really matter? Looking beyond the job posting to understand lab...

Does teamwork really matter? Looking beyond the job posting to understand lab...Labour Market Information Council | Conseil de l’information sur le marché du travail

Vicinity Jobs’ data includes more than three million 2023 OJPs and thousands of skills. Most skills appear in less than 0.02% of job postings, so most postings rely on a small subset of commonly used terms, like teamwork.

Laura Adkins-Hackett, Economist, LMIC, and Sukriti Trehan, Data Scientist, LMIC, presented their research exploring trends in the skills listed in OJPs to develop a deeper understanding of in-demand skills. This research project uses pointwise mutual information and other methods to extract more information about common skills from the relationships between skills, occupations and regions.OAT_RI_Ep20 WeighingTheRisks_May24_Trade Wars.pptx

How will new technology fields affect economic trade?

1:1制作加拿大麦吉尔大学毕业证硕士学历证书原版一模一样

原版一模一样【微信:741003700 】【加拿大麦吉尔大学毕业证硕士学历证书】【微信:741003700 】学位证,留信认证(真实可查,永久存档)offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原海外各大学 Bachelor Diploma degree, Master Degree Diploma

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

Enhancing Asset Quality: Strategies for Financial Institutions

Ensuring robust asset quality is not just a mere aspect but a critical cornerstone for the stability and success of financial institutions worldwide. It serves as the bedrock upon which profitability is built and investor confidence is sustained. Therefore, in this presentation, we delve into a comprehensive exploration of strategies that can aid financial institutions in achieving and maintaining superior asset quality.

做澳洲澳大利亚国立大学毕业证荣誉学位证书原版一模一样

原版一模一样【微信:741003700 】【澳洲澳大利亚国立大学毕业证荣誉学位证书】【微信:741003700 】学位证,留信认证(真实可查,永久存档)offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原海外各大学 Bachelor Diploma degree, Master Degree Diploma

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

South Dakota State University degree offer diploma Transcript

办理美国SDSU毕业证书制作南达科他州立大学假文凭定制Q微168899991做SDSU留信网教留服认证海牙认证改SDSU成绩单GPA做SDSU假学位证假文凭高仿毕业证GRE代考如何申请南达科他州立大学South Dakota State University degree offer diploma Transcript

Accounting Information Systems (AIS).pptx

An accounting information system (AIS) refers to tools and systems designed for the collection and display of accounting information so accountants and executives can make informed decisions.

快速办理(RWTH毕业证书)德国亚琛工业大学毕业证录取通知书一模一样

原件一模一样【微信:bwp0011】《(RWTH毕业证书)德国亚琛工业大学毕业证》【微信:bwp0011】学位证,留信认证(真实可查,永久存档)原件一模一样纸张工艺/offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原。

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问微bwp0011

【主营项目】

一.毕业证【微bwp0011】成绩单、使馆认证、教育部认证、雅思托福成绩单、学生卡等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

如果您处于以下几种情况:

◇在校期间,因各种原因未能顺利毕业……拿不到官方毕业证【微bwp0011】

◇面对父母的压力,希望尽快拿到;

◇不清楚认证流程以及材料该如何准备;

◇回国时间很长,忘记办理;

◇回国马上就要找工作,办给用人单位看;

◇企事业单位必须要求办理的

◇需要报考公务员、购买免税车、落转户口

◇申请留学生创业基金

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

Machine Learning in Business - A power point presentation.pptx

Power point presentation on machine learning.

Dr. Alyce Su Cover Story - China's Investment Leader

In World Expo 2010 Shanghai – the most visited Expo in the World History

https://www.britannica.com/event/Expo-Shanghai-2010

China’s official organizer of the Expo, CCPIT (China Council for the Promotion of International Trade https://en.ccpit.org/) has chosen Dr. Alyce Su as the Cover Person with Cover Story, in the Expo’s official magazine distributed throughout the Expo, showcasing China’s New Generation of Leaders to the World.

RMIT University degree offer diploma Transcript

澳洲RMIT毕业证书制作RMIT假文凭定制Q微168899991做RMIT留信网教留服认证海牙认证改RMIT成绩单GPA做RMIT假学位证假文凭高仿毕业证申请墨尔本皇家理工大学RMIT University degree offer diploma Transcript

What's a worker’s market? Job quality and labour market tightness

What's a worker’s market? Job quality and labour market tightnessLabour Market Information Council | Conseil de l’information sur le marché du travail

In a tight labour market, job-seekers gain bargaining power and leverage it into greater job quality—at least, that’s the conventional wisdom.

Michael, LMIC Economist, presented findings that reveal a weakened relationship between labour market tightness and job quality indicators following the pandemic. Labour market tightness coincided with growth in real wages for only a portion of workers: those in low-wage jobs requiring little education. Several factors—including labour market composition, worker and employer behaviour, and labour market practices—have contributed to the absence of worker benefits. These will be investigated further in future work.International Sustainability Standards Board

Issb standards

New standard for reporting sustainability on lines of tcfd

Recently uploaded (20)

Economic Risk Factor Update: June 2024 [SlideShare]

Economic Risk Factor Update: June 2024 [SlideShare]

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strate...

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strate...

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strate...

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strate...

Does teamwork really matter? Looking beyond the job posting to understand lab...

Does teamwork really matter? Looking beyond the job posting to understand lab...

Upanishads summary with explanations of each upnishad

Upanishads summary with explanations of each upnishad

OAT_RI_Ep20 WeighingTheRisks_May24_Trade Wars.pptx

OAT_RI_Ep20 WeighingTheRisks_May24_Trade Wars.pptx

Enhancing Asset Quality: Strategies for Financial Institutions

Enhancing Asset Quality: Strategies for Financial Institutions

South Dakota State University degree offer diploma Transcript

South Dakota State University degree offer diploma Transcript

Machine Learning in Business - A power point presentation.pptx

Machine Learning in Business - A power point presentation.pptx

Dr. Alyce Su Cover Story - China's Investment Leader

Dr. Alyce Su Cover Story - China's Investment Leader

What's a worker’s market? Job quality and labour market tightness

What's a worker’s market? Job quality and labour market tightness

Who Can be Home Loan Co-applicant?

- 1. Who can be a Home Loan co-applicant? Husband-wife Father-son Mother-son Brother-brother Unmarried daughter and father