Account reconciliationis the process of comparing

internal financial records against monthly statements

from external sources—such as a bank, credit card

company, or other financial institution—to make sure

they match up.

Knowing how to reconcile your accounts accurately is

essential for the financial health of your business, as it

helps to detect any errors, discrepancies, or fraud.

3.

The termReconciliation has taken from the word

“Reconcile” which means to tally, check, equate.

The Reconciliation is done to reconcile the

Profits/Loss as per the Financial Accounts with the

Cost Accounts.

4.

When Costand Financial Accounts are prepared separately

in different set of books, results or profits/losses in both the

accounts don’t match with each other.

In this Case, both the accounts results are necessary to

reconcile. It is prepared by showing the reasons for the

difference in the results of accounts. It is done to make the

arithmetical accuracy.

Reconciliation Statement is a Memorandum Reconciliation

Account to know the items required to make the profits of

Cost Accounts with the Financial Accounts.

5.

Earlier wehave studied how Cost Accounts (or Cost

Sheets) help to ascertain the cost of products.

Cost Accounts also reveal the profit or loss in respect of

the products.

Such profit or loss as per the Cost Accounts is, however,

likely to be different from the profit or loss shown by the

Financial Accounts of the concern for many reasons.

6.

Some itemsof income and expenses appearing only in the

Financial Accounts and not in the Cost Accounts.

For Example, Income from dividends, Goodwill written off etc.

Some items of income and expenses appearing only in Cost

Accounts,

For Example, Notional Interest on Owner’s Capital etc. and

Different treatment given to some items in the two sets of

Accounts,

For Example, Different methods of valuation of stock, Different

methods of charging depreciation, or the Overheads being taken

on estimated basis in Cost Accounts etc.

7.

Main reasons fordifference in the profits (or losses) disclosed

by the Cost Accounts and the Financial Accounts are…..

(A) Items Appearing in Financial Accounts Only

(1) Expenses/Losses/Appropriations Debited in Financial

Accounts only.

(2) Income Credited in Financial Accounts only.

8.

(B) Item AppearingIn Cost Accounts Only

(1) Expenses Debited in Cost Accounts only.

(2) Income Credited in Cost Accounts only.

(C) Different Treatment in Two Accounts

(1) Valuation of Opening and Closing Stocks.

(2) Methods of Charging Depreciation.

(3) Methods of Recovery/Absorption of Prime Cost/Overheads

in Cost Accounts.

9.

Financial Accountscover all the items of Income and

Expenses pertaining to the organization as a whole

Cost Accounts, on the other hand, are limited in scope.

Cost Accounts take into consideration only the items of

income and costs pertaining to the cost unit i.e.

product, process, contract etc.

10.

(1) Financial Expenses

Interest paid on Loans, Fixed Deposits, Debentures.

Expenses on Issue of Shares, Debentures etc.

Discount on Issue of Shares, Debentures etc.

Underwriting Commission on Issue of Shares.

11.

(2) Financial Losses

Capital Losses such as Loss on sale of fixed assets,

Loss on sate of Investment, Loss of assets by fire or

flood, Machinery Scrapped etc.

Penalties and Fines.

Damages paid as ordered by Court.

12.

(3) Appropriations Outof Profits:

Donations.

Writing Off Fictitious Assets e.g. Goodwill,

Preliminary Expenses, etc.

Income Tax.

Transfers to Sinking Funds.

Dividends - both Preference and Equity.

Transfer to Reserves.

13.

Interest Receivedon Loans / Fixed Deposits / Bank

Deposits / Debentures etc.

Dividend Received on Investments made in Shares.

Premium on Issue of Shares/ Debentures credited to the

Profit and Loss Account.

Rent Received.

14.

Transfer FeesReceived in respect of Share Transfers.

Capital Gains such as Profit on sale of fixed assets,

profit on sale of Investments.

Penalties and Fines or Discounts Received from

customers etc.

Damages Received as ordered by Court.

15.

Similarly, there arecertain items of Income and

Expenses which appear only in Cost Accounts and not

in Financial Accounts.

16.

1. Expenses Debitedin Cost Accounts Only

Notional interest on Owner’s Capital.

Notional Remuneration to Owner for his Labour and

Management.

Notional Rent to Owner for use of his premises for

business.

17.

Notional interest chargedto owner for drawings (debit

balance in Capital Account).

Notional Rent charged to owner for personal use of

business premises.

18.

There areseveral items of income and expenses which

are treated differently in the two sets of accounts viz, the

Cost Accounts and the Financial Accounts.

The amounts of such items in two sets of accounts are

different due to the different treatment.

The difference in the amounts has to be ascertained and

adjusted in order to reconcile the respective profits as per

the two accounts. These items are explained in detail

below.

19.

Raw Materials maybe valued on FIFO basis in Cost

Accounts and LIFO basis in Financial Accounts.

20.

Work inProgress maybe valued at actual prime cost

plus an estimated percentage of overheads in Cost

Accounts, while in Financial Accounts, work-in-

progress may be valued only at prime cost.

Work in progress in respect of a long term contract,

may be valued by different methods in the Cost

Accounts and the Financial Accounts.

21.

Finished Goods maybe valued at Cost of Good Sold

including Office Overheads in Cost Accounts, while in

Financial Accounts, they may be valued at production

cost excluding Office expenses.

Finished goods maybe valued in the Financial

Accounts at market price if it is lower than cost.

However, in Cost Accounts, Finished Goods may be

valued only at Cost, irrespective of the market price.

22.

The method adoptedfor charging depreciation in the two

accounts - Cost Accounts and Financial Accounts - may be

different.

While the Cost Accounts may follow the Straight Line

Method.

Financial Accounts may follow the Written Down Value

Method.

This obviously leads to either Overcharging or

Undercharging of depreciation in the Financial Accounts.

23.

Materials: Sometimes inCost Accounts, the cost of Materials,

Labour or Overheads is taken at an estimated or pre-determined

value instead of the actual expenditure.

Thus Raw Materials may be taken at a cost equal to

Actual Quantity Consumed x Fixed Rate.

The actual cost of raw materials debited in the Financial

Accounts will be different from such cost of materials debited in

the Cost Accounts. Some difference in the value of consumption

of materials may also arise due to different treatment of Wastage

and Loss of materials in the two sets of accounts.

24.

Wages: Like materials,Wages too may be debited in the

Cost Accounts at an estimated amount equal to

Actual labour Hours x Fixed Wage Rate

The actual amount of Wages debited in the Financial

Accounts will be different from the Wages debited in the

Cost Accounts.

The treatment of Idle Time and Overtime may be

different in the two sets of Accounts leading to

difference between the Financial Profits and the Costing

Profits.

25.

Overheads: Overheads arefrequently debited or charged

to products, processes etc. on estimated basis in Cost

Accounts.

The amount of overheads thus recovered or absorbed in

the Cost Accounts is bound to be different from the actual

amount of overheads appearing in the Financial Accounts.

The overheads are likely to be either over recovered or

under recovered in the Cost Accounts leading to difference

between the Financial Profit and the Cost Profit.

26.

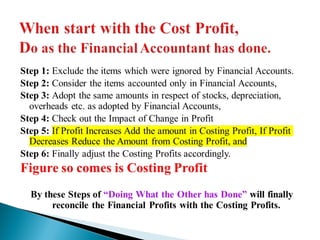

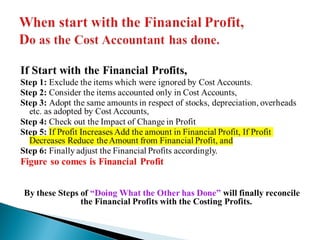

BASIC RULE

The basicrule for preparing the Reconciliation Statement is

“Do as what the other has done”

Plus as per the Impact of Profit Increases

and Decrease make additions and

subtraction respectively in the Books,

which is taken into account for

Reconciliation

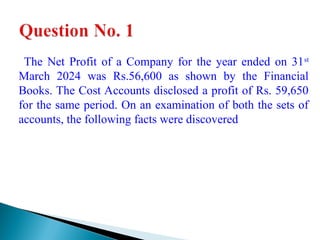

29.

The Net Profitof a Company for the year ended on 31st

March 2024 was Rs.56,600 as shown by the Financial

Books. The Cost Accounts disclosed a profit of Rs. 59,650

for the same period. On an examination of both the sets of

accounts, the following facts were discovered

30.

(a) Goodwill writtenoff in Financial Accounts – Rs.1,500.

(b) Transfer fees received during the year Rs.200

(c) Depreciation charged in financial accounts Rs.750

(d) Depreciation recovered in cost statements Rs.1,000.

(e) Opening stock as on 1st

April 2023 as per financial records Rs.13,000

(f) Opening stock as on 1st

April 2023 as per cost statement Rs.12,000

(g) Closing stock as on 31st

March 2024 as per financial records Rs.14,000

(h) Closing stock as on 31st

March 2024 as per cost statement Rs.15,000.

Prepare a Reconciliation statement reconciling the profit as shown by

financial

and cost books taking

(i) Financial profit as the starting point,

(ii) Costing profit as the starting point.

![MEFA_UNIT-IV_Part-1[1].pptx kkkkkkkkkkkkkkkkkkkkkkk](https://cdn.slidesharecdn.com/ss_thumbnails/mefaunit-ivpart-11-250504093650-39e41996-thumbnail.jpg?width=640&height=640&fit=bounds)