Download to read offline

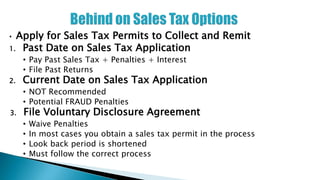

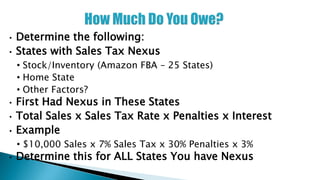

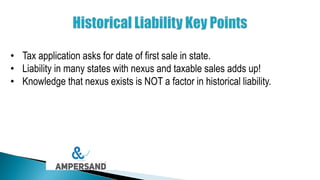

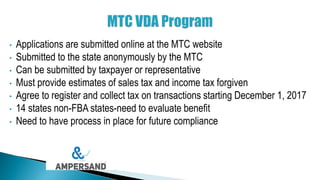

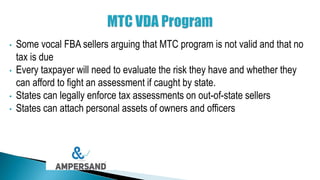

This document summarizes a presentation by Ned A. Lenhart, CPA on voluntary disclosure agreements (VDAs). It discusses: 1. Options for businesses that owe back sales tax, including applying for permits and filing past due returns with penalties and interest, or filing a VDA to waive penalties. 2. How to determine sales tax liability in multiple states, including calculating taxes, penalties, and interest owed based on sales and tax rates. 3. Key details of a VDA, including limited lookback periods, reduced or eliminated penalties, and agreeing to register and collect future taxes. 4. Important considerations for the VDA process like eligibility, timeframes, and common mistakes to avoid

![[ON-DEMAND WEBINAR] Manufacturing Education Day 2020 Addresses PPP Loans, R&D...](https://cdn.slidesharecdn.com/ss_thumbnails/manufacturingdayslides-201005180957-thumbnail.jpg?width=640&height=640&fit=bounds)