7.1. Introduction

Inflationcan be defined as an overall increase in price

level.

The percentage change in the overall level of price is

called rate of inflation.

Inflation that exceeds 50% per month, which is just over

1% per day is called Hyperinflation.

Every where in the world today, inflation is officially

regarded as a major economic problem and is one of the

major concerns of macroeconomic policies.

High inflation results in high costs due to

a) Time and energy devoted to cash management when cash

loss value quickly..

3.

Contd….

b) Menu costsbecome larger due to printing and distributing

catalogs because fixed prices become impossible

c) Relative prices do not do a good job of reflecting true

scarcity of resources.

d) Tax systems are distorted-due to delay between the time tax

is leveled and time tax is paid to government - reduce tax

revenue.

e) Weight of currency become heavy. Add more zeros and

becomes intolerable.

4.

7.2 Excess-Demand orDemand Pull

Inflation

Excess-Demand or Demand Pull Inflation is one of the

earlier theories of inflation.

Inflation is a persistent and appreciable rise in general

level of price.

Inflation is a process of a rising price, not just high

price rise.

That means it is dynamic in nature.

5.

a) Classical Analysis

Accordingto the classical analysis, the price level

depends directly and proportionately on the quantity of

money (quantity theory of money).

Inflation occurred when the quantity of money increased

and stopped when the quantity of money is stabilized.

The rate of inflation thus presumably depended on the

rate of new money creation

If price rises by 3%.

%

3

M

M

6.

If the Economyis at full employment?

New money flowing into the economy in the form of bank

loans to businesses to finance investment in excess of the

current rate of saving leads to net increase in the aggregate

demand for an unchanged total supply of goods (since the

economy was already at full employment).

As a result price of goods increase and also price of inputs

increases, and extract “forced savings” from consumers,

whose money incomes were based on earlier price level.

This leads to monetary inflation which is an excess demand

phenomenon.

7.

Ctd

An economy couldexperience inflation even with a constant

money supply if consumption or investment propensity

increased under condition of full employment.

Full employment:- level of employment beyond which unit

labor cost, and thus price levels, where sure to rise.

If money supplies were constant, higher price would raise

the transaction demand for money and thus push up interest

rates tending to choke off some investment (or consumer)

demand and thus to moderate the inflationary pressure

But it would not completely avoid a rise in price level.

8.

Contd….

The reason isthat the rise in interest rate would also release

money from idle balance to supply the added transaction

needs at higher price.

Thus same inflation would still occur until interest rate rose

enough to eliminate excess demand.

On the other hand, if government spending increases with

no rise in taxes, the difference (deficit) must be financed

either by:

(a) borrowing from the general public (non-bank) or

borrowing from banks with excess reserve.

9.

Ctd…

(b) Printing morepaper money,

Condition “b” directly raise price level or

even “a” some times.

Excess of aggregate demand over potential out

put causes prices to bid up until market were

cleared at a price level high enough to

eliminate excess demand.

10.

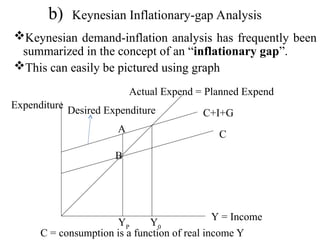

b) Keynesian Inflationary-gapAnalysis

Keynesian demand-inflation analysis has frequently been

summarized in the concept of an “inflationary gap”.

This can easily be pictured using graph

C

C+I+G

Actual Expend = Planned Expend

Y = Income

Expenditure

A

B

C = consumption is a function of real income Y

YP

Y0

Desired Expenditure

11.

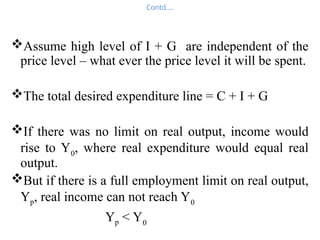

Contd….

Assume high levelof I + G are independent of the

price level – what ever the price level it will be spent.

The total desired expenditure line = C + I + G

If there was no limit on real output, income would

rise to Y0

, where real expenditure would equal real

output.

But if there is a full employment limit on real output,

Yp, real income can not reach Y0

Yp < Y0

12.

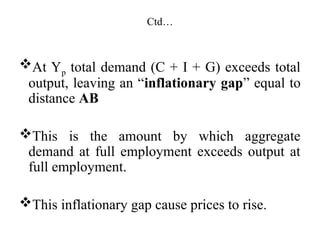

Ctd…

At Yp totaldemand (C + I + G) exceeds total

output, leaving an “inflationary gap” equal to

distance AB

This is the amount by which aggregate

demand at full employment exceeds output at

full employment.

This inflationary gap cause prices to rise.

13.

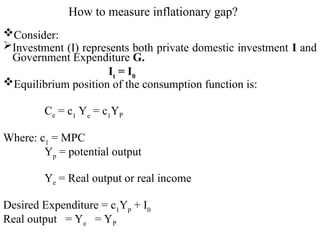

How to measureinflationary gap?

Consider:

Investment (I) represents both private domestic investment I and

Government Expenditure G.

It

= I0

Equilibrium position of the consumption function is:

Ce = c1

Ye

= c1

YP

Where: c1

= MPC

Yp = potential output

Ye = Real output or real income

Desired Expenditure = c1

Yp + I0

Real output = Ye = YP

14.

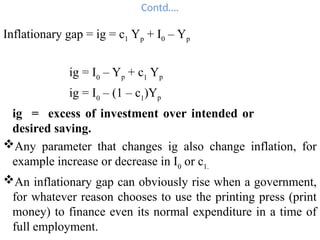

Contd….

Inflationary gap =ig = c1 Yp + I0 – Yp

ig = I0

– Yp + c1

Yp

ig = I0

– (1 – c1

)Yp

ig = excess of investment over intended or

desired saving.

Any parameter that changes ig also change inflation, for

example increase or decrease in I0

or c1.

An inflationary gap can obviously rise when a government,

for whatever reason chooses to use the printing press (print

money) to finance even its normal expenditure in a time of

full employment.

15.

Contd…..

Inflation from excessdemand could also occur during a

strong private investment boom, especially if monetary

policy were willing to “accommodate” increased demands

for money.

Other important causes of excess demand inflation are

usually those associated with war or preparation for war.

When government expenditure typically increases far more

than private expenditures are reduced by higher tax

16.

c) The Dynamicsof Demand Pull Inflation

As mentioned earlier, inflation is a dynamic process.

Inflationary gap analysis do not tell about how fast price

will rise – it is static analysis

We need to introduce dynamic analysis.

Hypothesis for Dynamic Theory ?

In most general sense, the rate of price increase is

functionally related to the size of inflationary gap.

The larger the gap, the faster price rise and the smaller the

gap, the more slowly they rise.

17.

Contd….

Market demand forgoods at any one time is limited

by the money income accruing from previous

production.

Consumers come to market with money incomes

derived from the earlier sale of output at the price

level then prevailing.

Their demand competes with that of businessmen

supplied with new bank money.

18.

Ctd…

Given the totalof this available purchasing power,

price at any given time are bid up to the point at

which all markets are cleared

i.e the point at which there are no unsatisfied

demands, given the available purchasing power

“excess demand” is zero.

However, with some lag, money incomes rise as a

result of the sale of output at the new higher price

recreating excess demand and requiring

progressively higher price levels for markets to

remain cleaned.

19.

Contd…..

Let use consumptionfunction to analyze rigorously the

process.

Yt

= Ct

+ It

= YP (1)

Yt

= current real demand for output made up of real

consumer demand Ct and real investment It (which include G

and I)

Note: Tax are included with lag in tax function but for

present ignore taxes.

YP = Fixed potential output

Assume Yt

= YP

Assuming no unsatisfied demand, all markets are cleared

20.

Contd….

Our consumption functionmakes current real consumption

proportional to real consumer income.

t

t

t

t

P

P

Y

c

C 1

1

1

(2)

C1 = Marginal propensity to consume.

Yt-1

Pt-1

= money income from sale of output at an earlier

date

Convert to real income by dividing by Pt

It = I0 (3)

21.

Contd…..

It

= I0

implies thatall real investment demands are carried

out regardless of current price.

The banks currently provide whatever new funds are

necessary for borrowers to be able to buy the investment

goods demanded at whatever price it takes.

By substitution of equation (2) and (3) in to (1) we obtain a

simple result.

Assume, output in previous period was also at full

employment level YP.

From (1), Ct + It = YP

22.

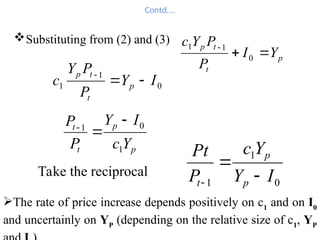

Contd….

Substituting from (2)and (3)

p

t

t

p

Y

I

P

P

Y

c

0

1

1

0

1

1 I

Y

P

P

Y

c p

t

t

p

p

p

t

t

Y

c

I

Y

P

P

1

0

1

Take the reciprocal

0

1

1 I

Y

Y

c

P

Pt

p

p

t

The rate of price increase depends positively on c1

and on I0

and uncertainly on YP

(depending on the relative size of c1

, YP

23.

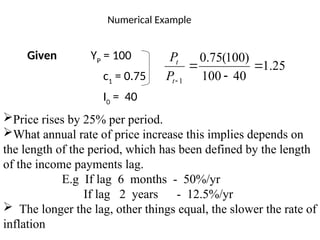

Numerical Example

Given YP

=100

c1

= 0.75

I0

= 40

25

.

1

40

100

)

100

(

75

.

0

1

t

t

P

P

Price rises by 25% per period.

What annual rate of price increase this implies depends on

the length of the period, which has been defined by the length

of the income payments lag.

E.g If lag 6 months - 50%/yr

If lag 2 years - 12.5%/yr

The longer the lag, other things equal, the slower the rate of

inflation

24.

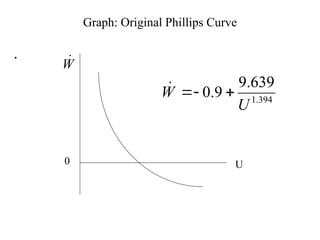

7.3. Inflation andPhillips Curves

New view of inflation came as a result of the discovery

of empirical regulatory in 1958, by a British Professor

A.W. Phillips.

He studied annual changes in British wage rate over a

period of almost 100 yrs.

Over the first 52 ending 1913 he found fairly stable

relationship between the annual % change in wage rate in

any year and the average level of unemployment.

25.

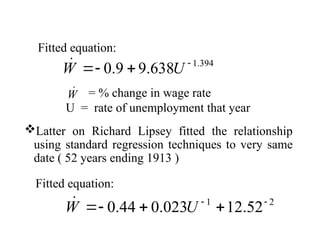

Fitted equation:

Latter onRichard Lipsey fitted the relationship

using standard regression techniques to very same

date ( 52 years ending 1913 )

Fitted equation:

2

1

52

.

12

023

.

0

44

.

0

U

W

394

.

1

638

.

9

9

.

0

U

W

= % change in wage rate

U = rate of unemployment that year

W

26.

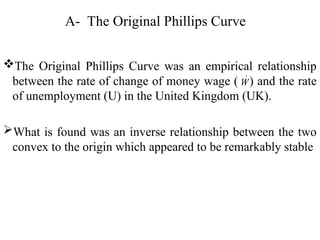

A- The OriginalPhillips Curve

The Original Phillips Curve was an empirical relationship

between the rate of change of money wage ( ) and the rate

of unemployment (U) in the United Kingdom (UK).

What is found was an inverse relationship between the two

convex to the origin which appeared to be remarkably stable

W

27.

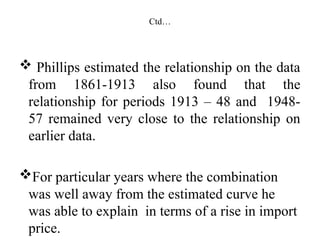

Ctd…

Phillips estimatedthe relationship on the data

from 1861-1913 also found that the

relationship for periods 1913 – 48 and 1948-

57 remained very close to the relationship on

earlier data.

For particular years where the combination

was well away from the estimated curve he

was able to explain in terms of a rise in import

price.

Contd….

Two years laterLipsey (1960) provided a theoretical

rational to Phillips estimated empirical relationship.

Lipsey – started from individual labor market,

disaggregated from the overall national labor market

by region or by skill, and worked up to the overall

macroeconomic relationship.

First, he made a simple dynamic assumption that rate

of change of wages varies positively with the

proportionate amount of excess demand for labor in

individual labor market

30.

Ctd..

L

ED

W

For>0

W

W

W

= Proportionate rate of change of wage

EDL = DL - SL = Excess demand for labor

= Factor of Proportionality

31.

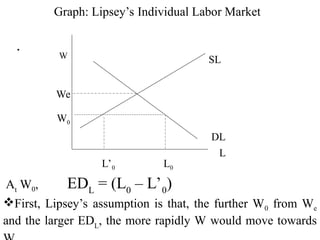

Graph: Lipsey’s IndividualLabor Market

.

L

W SL

DL

We

W0

L0

L’0

At

W0, EDL

= (L0

– L’0

)

First, Lipsey’s assumption is that, the further W0 from We

and the larger EDL

, the more rapidly W would move towards

32.

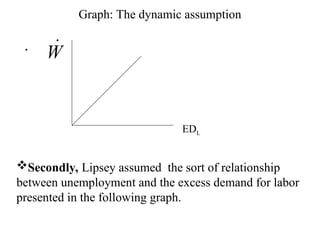

Graph: The dynamicassumption

.

EDL

W

Secondly, Lipsey assumed the sort of relationship

between unemployment and the excess demand for labor

presented in the following graph.

33.

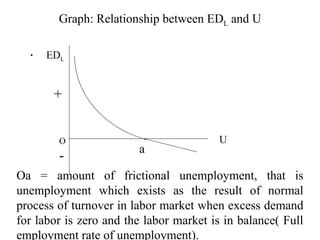

Graph: Relationship betweenEDL and U

.

U

EDL

O

+

- a

Oa = amount of frictional unemployment, that is

unemployment which exists as the result of normal

process of turnover in labor market when excess demand

for labor is zero and the labor market is in balance( Full

employment rate of unemployment).

34.

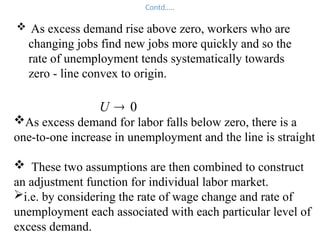

Contd…..

As excessdemand rise above zero, workers who are

changing jobs find new jobs more quickly and so the

rate of unemployment tends systematically towards

zero - line convex to origin.

0

U

As excess demand for labor falls below zero, there is a

one-to-one increase in unemployment and the line is straight

These two assumptions are then combined to construct

an adjustment function for individual labor market.

i.e. by considering the rate of wage change and rate of

unemployment each associated with each particular level of

excess demand.

35.

Contd….

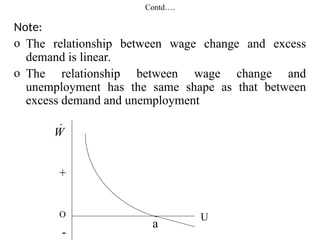

Note:

o The relationshipbetween wage change and excess

demand is linear.

o The relationship between wage change and

unemployment has the same shape as that between

excess demand and unemployment

W

O

U

a

+

-

36.

Ctd….

In final stageof his analysis in order to construct a

“macro adjustment function” Lipsey aggregated the

individual labor market adjustment function, which

he assumed to be identical.

He showed that this macro adjustment function

(Phillips curve for the economy as a whole) is non-

linear below the horizontal axis if the unemployment

rate in individual labor market differ.

37.

Ctd…

The furtheraway from the origin the greater is

the difference between unemployment rate in

various individual markets.

The government in principle could shift the

curve towards the origin if it could reduce

dispersion of unemployment rates between

individual labor markets.

38.

Contd….

The Phillips –Lipsey analysis predate the Keynesian –

Monetarist debate of the 1960’s and do not belong to

any particular school.

As a result, it was taken up rapidly by wide range of

economist in different countries and became a basic

element of macroeconomic thought.

The basic result is that change in wage rate is a function

of excess demand.

)

( 0

U

U

W

where U0 = natural rate of unemployment

U = Actual rate of unemployment

39.

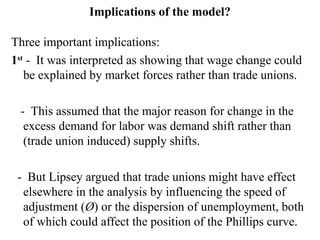

Implications of themodel?

Three important implications:

1st

- It was interpreted as showing that wage change could

be explained by market forces rather than trade unions.

- This assumed that the major reason for change in the

excess demand for labor was demand shift rather than

(trade union induced) supply shifts.

- But Lipsey argued that trade unions might have effect

elsewhere in the analysis by influencing the speed of

adjustment (Ø) or the dispersion of unemployment, both

of which could affect the position of the Phillips curve.

40.

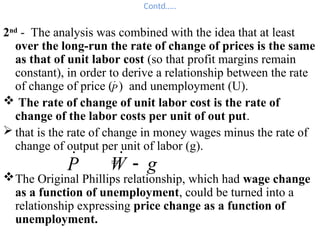

Contd…..

2nd

- The analysiswas combined with the idea that at least

over the long-run the rate of change of prices is the same

as that of unit labor cost (so that profit margins remain

constant), in order to derive a relationship between the rate

of change of price ( ) and unemployment (U).

The rate of change of unit labor cost is the rate of

change of the labor costs per unit of out put.

that is the rate of change in money wages minus the rate of

change of output per unit of labor (g).

=

The Original Phillips relationship, which had wage change

as a function of unemployment, could be turned into a

relationship expressing price change as a function of

unemployment.

P

P

g

W

41.

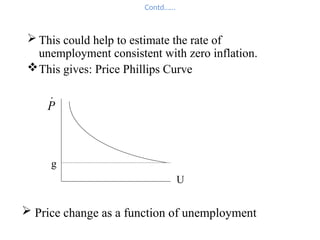

Contd……

This couldhelp to estimate the rate of

unemployment consistent with zero inflation.

This gives: Price Phillips Curve

P

U

Price change as a function of unemployment

g

42.

Cntd…..

3rd.

The Phillips curvewas interpreted as showing that there

was a trade-off between inflation and unemployment.

Less unemployment was possible only with higher inflation

rate and less inflation could be obtained only at the cost of

higher unemployment.

The problem for macroeconomic policy was then the

problem of choosing and attaining the preferred

combination of the two.

That is, preferred point on the curve.

43.

Ctd..

However, some economistsalso argue that the

“trade-off” could be favorably modified by

the use of an incomes policy (set kind of

norm or limit on to the rate of increase in

wages and salaries )

This could make wage rise more slowly at any

given level of U and would therefore shift to

Phillips curve inward to wards the origin

44.

7.4. Expectation-Augmented PhillipsCurve

By the Mid 1960 Phillips Curve had been estimated for

variety of countries and time periods with apparent success.

But in late 1960’s and early 1970’s many countries began to

experience combination of inflation and unemployment well

outside the estimated Phillips curve.

Original Phillips Curve “empirical break down”.

Even before this, however, the original Phillips Curve

analysis had been strongly criticized by Friedman (1968)

and Phelps (1967)

Critics refer to the figure on excess demand labor of Lipsey

(1960); which shows an upward sloping SL curve and

down ward sloping DL curve drawn against the money

wage on the vertical Axis.

45.

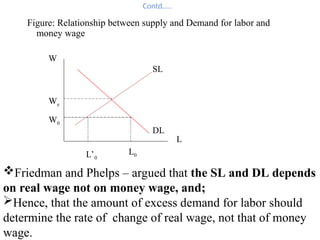

Contd…..

Figure: Relationship betweensupply and Demand for labor and

money wage

L

L0

L’0

W0

We

W

SL

DL

Friedman and Phelps – argued that the SL and DL depends

on real wage not on money wage, and;

Hence, that the amount of excess demand for labor should

determine the rate of change of real wage, not that of money

wage.

46.

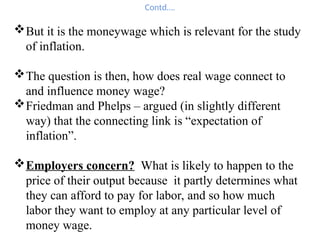

Contd….

But it isthe moneywage which is relevant for the study

of inflation.

The question is then, how does real wage connect to

and influence money wage?

Friedman and Phelps – argued (in slightly different

way) that the connecting link is “expectation of

inflation”.

Employers concern? What is likely to happen to the

price of their output because it partly determines what

they can afford to pay for labor, and so how much

labor they want to employ at any particular level of

money wage.

47.

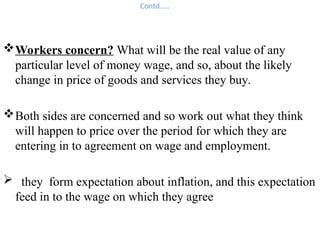

Contd…..

Workers concern? Whatwill be the real value of any

particular level of money wage, and so, about the likely

change in price of goods and services they buy.

Both sides are concerned and so work out what they think

will happen to price over the period for which they are

entering in to agreement on wage and employment.

they form expectation about inflation, and this expectation

feed in to the wage on which they agree

48.

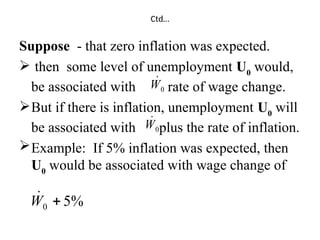

Ctd…

Suppose - thatzero inflation was expected.

then some level of unemployment U0

would,

be associated with rate of wage change.

But if there is inflation, unemployment U0

will

be associated with plus the rate of inflation.

Example: If 5% inflation was expected, then

U0

would be associated with wage change of

%

5

0

W

0

W

0

W

49.

Contd…..

For Phillips &Lipsey – excess demand determined the

growth of money wage.

For Friedman & Phelps – excess demand determine the

growth of real wage, and excess demand plus expected

inflation determine the growth of money wage.

When expected inflation is zero, employers and workers

expect the rate of change of money wage to be the same as

that of real wage.

In this case the original Phillips Curve (which Lipsey’s

rational did not distinguish between the two) makes sense.

50.

Contd…..

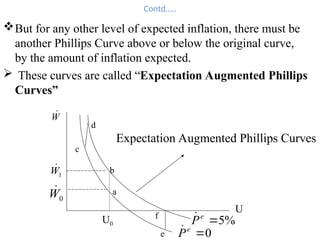

But for anyother level of expected inflation, there must be

another Phillips Curve above or below the original curve,

by the amount of inflation expected.

These curves are called “Expectation Augmented Phillips

Curves”

W

0

e

P

%

5

e

P

0

W

1

W

e

f

b

a

c

d

U

U0

Expectation Augmented Phillips Curves

51.

Contd…..

The vertical distancebetween the two curves is equal

to the expected inflation between the two curves.

ab = cd = ef = 5%

The rate of wage change on the vertical axis, can be

translated into price change (inflation) by using the

assumption :

g

W

P

52.

Ctd….

• g =productivity growth and is assumed to be constant

in the short run.

• Suppose g = associated with unemployment

level of U0, on curve,

• Then: Unemployment is U0 and expected inflation is

zero, actual inflation is:

Expectation of inflation is correct

0

W

0

e

P

0

0

g

W

P

53.

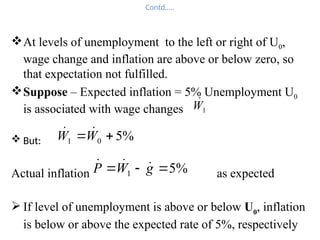

Contd…..

At levels ofunemployment to the left or right of U0,

wage change and inflation are above or below zero, so

that expectation not fulfilled.

Suppose – Expected inflation = 5% Unemployment U0

is associated with wage changes

But:

Actual inflation as expected

If level of unemployment is above or below U0

, inflation

is below or above the expected rate of 5%, respectively

1

W

%

5

0

1

W

W

%

5

1

g

W

P

54.

Contd…..

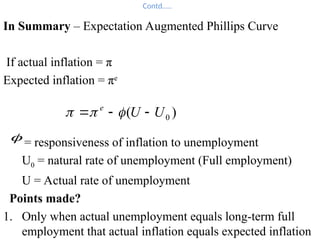

In Summary –Expectation Augmented Phillips Curve

If actual inflation = π

Expected inflation = πe

= responsiveness of inflation to unemployment

U0 = natural rate of unemployment (Full employment)

U = Actual rate of unemployment

Points made?

1. Only when actual unemployment equals long-term full

employment that actual inflation equals expected inflation

)

( 0

U

U

e

55.

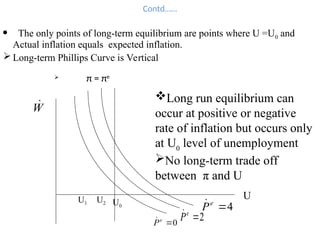

Contd……

The onlypoints of long-term equilibrium are points where U =U0 and

Actual inflation equals expected inflation.

Long-term Phillips Curve is Vertical

π = πe

0

e

P

2

e

P

Long run equilibrium can

occur at positive or negative

rate of inflation but occurs only

at U0

level of unemployment

No long-term trade off

between π and U

4

e

P

U0

U2

U1

W

U

56.

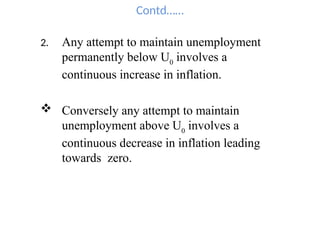

Contd……

2. Any attemptto maintain unemployment

permanently below U0

involves a

continuous increase in inflation.

Conversely any attempt to maintain

unemployment above U0

involves a

continuous decrease in inflation leading

towards zero.

57.

7.5 Adaptive andrational Expectation

Long-term Phillips Curve which is vertical at the natural

rate of unemployment depends on two things

1) Absence of money illusion, which ensures that expected

inflation is fully incorporated into the determination of

wage change and inflation.

The difference between different short-run curves must be

equal to the difference between them in expected

inflation.

2) The existence of some mechanism by which actual

inflation is, ultimately if not immediately, fully

incorporated in to expected inflation.

What is the mechanism?

58.

Contd…..

There are twohypothesis as to how expectations are

formed.

a) Adaptive expectation Hypothesis

b) Rational expectation Hypothesis

Each can be combined with the natural rate hypothesis to

analyze how the economy reacts to certain events and each

predicts that actual inflation is in the end fully incorporated

in to expectation.

59.

Ctd…

The choice willhave no effect on the

implication of the natural rate hypothesis

regarding the long-run equilibrium.

The two, however, have different implications

for – the movement of the economy away from

long-run equilibrium and between positions.

Hence they have different implication for

short-run policy.

60.

1. Adaptive Expectation

Theadaptive Expectation is the one used implicitly by both

Friedman and Phelps in their original exposition of the

natural rate hypothesis and used implicitly in large amount

of later work on the natural rate hypothesis.

Basic idea:- Economic agents adapt or adjust their

expectation in the light of the errors they find they have

made in the past.

Agents are assumed to change their expectation between

one period and the next by same fraction of the

difference between their expectation and the actual rate

of inflation in the first period.

61.

Contd……

)

( 1

1

1

t

e

t

t

e

t

e

P

P

P

P

Rearranging

1

0

1

1

1 )

(

t

e

t

e

t

t

e

P

P

P

P

)

)

1

( 1

1

t

e

t

t

e

P

P

P

1

1

1

t

e

t

e

t

t

e

P

P

P

P

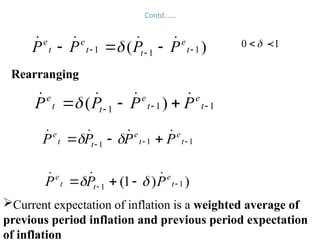

Current expectation of inflation is a weighted average of

previous period inflation and previous period expectation

of inflation

62.

Contd….-

2

2

1 )

1

(

)

1

(

t

e

t

t

t

e

P

P

P

P

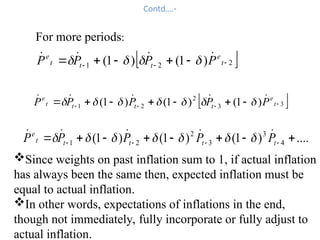

Since weights on past inflation sum to 1, if actual inflation

has always been the same then, expected inflation must be

equal to actual inflation.

In other words, expectations of inflations in the end,

though not immediately, fully incorporate or fully adjust to

actual inflation.

....

)

1

(

)

1

(

)

1

( 4

3

3

2

2

1

t

t

t

t

t

e

P

P

P

P

P

3

3

2

2

1 )

1

(

)

1

(

)

1

(

t

e

t

t

t

t

e

P

P

P

P

P

For more periods:

63.

Contd….

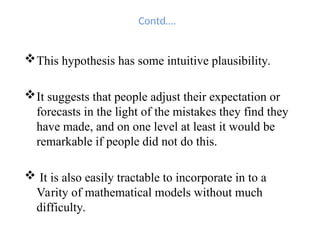

This hypothesis hassome intuitive plausibility.

It suggests that people adjust their expectation or

forecasts in the light of the mistakes they find they

have made, and on one level at least it would be

remarkable if people did not do this.

It is also easily tractable to incorporate in to a

Varity of mathematical models without much

difficulty.

64.

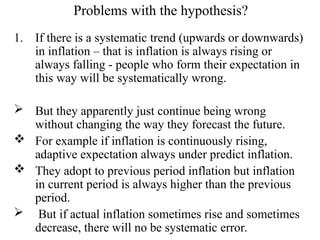

Problems with thehypothesis?

1. If there is a systematic trend (upwards or downwards)

in inflation – that is inflation is always rising or

always falling - people who form their expectation in

this way will be systematically wrong.

But they apparently just continue being wrong

without changing the way they forecast the future.

For example if inflation is continuously rising,

adaptive expectation always under predict inflation.

They adopt to previous period inflation but inflation

in current period is always higher than the previous

period.

But if actual inflation sometimes rise and sometimes

decrease, there will no be systematic error.

65.

Contd…..

2. The secondproblem with adaptive expectation hypothesis is

that it assumes that people take no notice of any information

about future inflation other than their past error.

But there is considerable amount of such information

available, in the form of reports in the media of the forecasts

professional forecasting agencies, including the

government.

Information are also available about factors supposed to

affect future inflation.

E.g In open economy devaluation or depreciation of currency

may lead to inflation

But adaptive expectation hypothesis could not know or take

into account until offer the effect.

66.

2. Rational Expectation

RationalExpectation hypothesis in its simplest form

suggests that economic agents use all the information

available to them in trying to forecast the future.

Assumptions:-

a - Economic agents make their forecast as if on the basis of a

current model of the economy, and,

b - This current model includes the systematic element in

government policy.

According to the first assumption, agents understand the

natural rate hypothesis, realize that nominal aggregate

demand is determined by the growth of the money supply,

know the value of U0

and so on

67.

Contd…..

The Weak versionof the hypothesis argue that, when the

govt. decide to increase the growth of the money supply

from g to g + 5%, people immediately perceive it and

realize that this brings about an inflation rate of 5% and

expect inflation of 5%.

Stronger version of the hypothesis argue that people

understand how the government typically manipulates its

monetary policy.

Understand that if unemployment rises by j% above U0

the

govt. reacts by increasing monetary growth by k%

68.

Ctd…

Therefore, whenever unemploymentrises

above U0

by j% people expect the govt. to

increase monetary growth by k%, and

immediately revise their expectation of

inflation accordingly.

Problem: - Cost of acquiring the information

-Finding (choosing) the correct

model of the economy

- Knowing the typical behavior of

the authorities manipulating the policy

69.

7.6. Cost –Push Inflation

Cost – Push Inflation theory was important in the

1960s and 1970s when it formed the key element of

the Keynesian side in the Keynesian – Monetarist

debate and has become less important and prominent

since then

However, it is worth discussing for more than

theoretical reason because some legacy of this idea

persist in mainstream economics in the form of the

possibility of certain kinds of supply side shock.

For easy understanding, think of the price of an

individual good produced by a particular firm.

70.

Contd…..

The price ofthe good can be decomposed into:

cost of material /unit of good

cost of labor used /unit of good

indirect taxes (a positive component)

or subsides (a negative component)

profit

Profit = Average revenue (net of any tax or subsidy) minus

average cost (excluding cost of capital).

The same procedure can also be undertaken at the

macroeconomic level.

the only difference is that when all firms are included in the

analysis the materials used by one firm which are also the

outputs of another firm, can be decomposed in their turn into

separate components, so that the material cost disappears except

for imports.

71.

Contd…..

Thus value ofthe total output of Goods and Services

available for domestic use

=

Value of import

+

Total Labor cost involved

+

Total profit

+

Total indirect taxes

-

Subsidies

72.

Contd….

It isconvenient to concentrate on output at factor cost

rather than at market prices because the factor cost excludes

indirect taxes and subsidies.

On this basis the value of output can be decomposed as

follows:

PQ = F + W + R

Where: PQ = value of output

P = Price of Output/Unit

Q = Quantity of Output

F = Import cost

W = Labor cost

R = Profit

73.

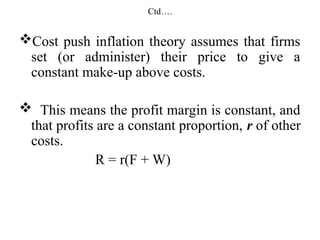

Ctd….

Cost push inflationtheory assumes that firms

set (or administer) their price to give a

constant make-up above costs.

This means the profit margin is constant, and

that profits are a constant proportion, r of other

costs.

R = r(F + W)

74.

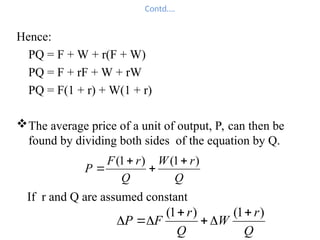

Contd….

Hence:

PQ = F+ W + r(F + W)

PQ = F + rF + W + rW

PQ = F(1 + r) + W(1 + r)

The average price of a unit of output, P, can then be

found by dividing both sides of the equation by Q.

Q

r

W

Q

r

F

P

)

1

(

)

1

(

If r and Q are assumed constant

Q

r

W

Q

r

F

P

)

1

(

)

1

(

75.

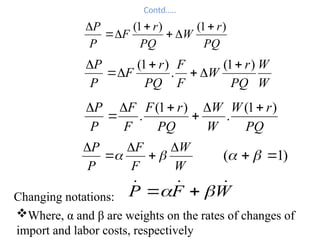

Contd…..

PQ

r

W

PQ

r

F

P

P )

1

(

)

1

(

W

W

PQ

r

W

F

F

PQ

r

F

P

P)

1

(

.

)

1

(

PQ

r

W

W

W

PQ

r

F

F

F

P

P )

1

(

.

)

1

(

.

W

W

F

F

P

P

)

1

(

Where, α and β are weights on the rates of changes of

import and labor costs, respectively

W

F

P

Changing notations:

76.

Contd…..

With constant profitmargin, the change in price is a

function of change in import cost and change in labor cost.

If output at market price was being considered, the change

in indirect taxes and subsidies would figure in the equation.

Cost push inflation theory regards the labor cost change and

import cost change as proximate determinants of inflation.

Particularly change in labor costs are singled out as the

main causes of inflation.

In the 1970s and 1980s, a number of studies tried to relate

the change in labor cost to some measures or indicator of

trade unions militancy.

77.

Contd…..

Thus inflation isseen as caused by increase in costs;

variation in demand have no direct effect on prices

and indeed no indirect effect either, since cost push

theories generally consider that the rate of change of

wages is also independent of demand conditions.

Thus the appropriate way to reduce or prevent

inflation is the use of an income policy that reduce

the rate at which wages increase.

Spiral = Wage increases lead to Price increases and this

in turn leads to inflation

78.

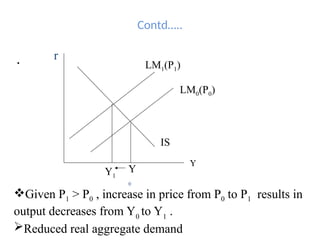

Cost – Pushand Real Demand

If variation in demand does not cause inflation, what is

the effect of cost-push inflation on real demand?

In IS-LM framework, for example, an increase in

prices shifts the Lm curve to the left, reducing real

aggregate demand and therefore output.

P

M

P shifts the Lm curve to the left

If LM curve was horizontal because of the liquidity trap or

if IS curve was vertical because investment was interest-

inelastic, demand and output would not be affected.

But if these extreme cases are excluded, cost-push inflation

must lead directly to lower output and higher unemployment

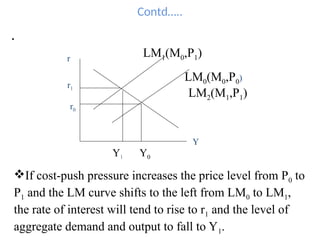

Contd…..

However, the inflationwhich has been experienced in

most industrialized countries has not typically taken this

form, and Cost-push inflations theories usually regarded

inflation to be independent of level of economic

activity.

The apparent inconsistency is reconciled by positing

some more processes by which the money supply

grows in response to inflation in such a way as to

maintain the level of real demand unchanged.

Suppose the government is committed to stabilize the

rate of interest at r0

or to maintain employment at a level

corresponding to output Y0.

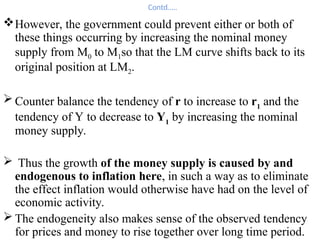

Contd…..

However, the governmentcould prevent either or both of

these things occurring by increasing the nominal money

supply from M0 to M1so that the LM curve shifts back to its

original position at LM2.

Counter balance the tendency of r to increase to r1

and the

tendency of Y to decrease to Y1

by increasing the nominal

money supply.

Thus the growth of the money supply is caused by and

endogenous to inflation here, in such a way as to eliminate

the effect inflation would otherwise have had on the level of

economic activity.

The endogeneity also makes sense of the observed tendency

for prices and money to rise together over long time period.

83.

Contd…..

An alternativepossibility is that the response of money supply to

inflation may not be only due to any commitment or specific

decisions by the government, but also due to some monetary

control system.

E.g Cost-push inflation might increase budget deficit if it

tends to increase nominal government expenditure by more than it

increases tax revenue.

If not reacted by increasing government borrowing from private

sector money supply will increase.

A second example is where bank lending to the private sector is

determined essentially by demand for credit, cost-push inflation

leads companies to borrow more to maintain the real value of

their working capital.

84.

Contd…..

That means, banklending and the money

supply will increase in line with prices.

The precise mechanism involved has not

been well developed, there is little empirical

analysis.

But some mechanism that makes money

supply endogenous to inflation is essential to

cost-push inflation theory.