VAT: Manage your risk and maximise your cashflow

•

1 like•271 views

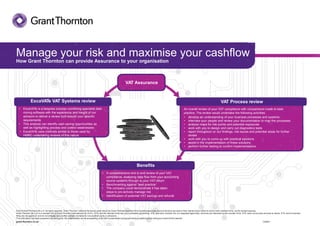

ExcaVATe is a bespoke process combining specialist data mining software with the experience and insight of our advisors to deliver a review built around your specific requirements. This analysis can identify cash saving opportunities as well as highlighting process and control weaknesses ExcaVATe uses methods similar to those used by HMRC undertaking reviews of this nature

Recommended

Recommended

More Related Content

Viewers also liked

Viewers also liked (13)

Similar to VAT: Manage your risk and maximise your cashflow

Similar to VAT: Manage your risk and maximise your cashflow (20)

More from Alex Baulf

More from Alex Baulf (20)

VAT: Manage your risk and maximise your cashflow

- 1. VAT AssuranceVAT Assurance Manage your risk and maximise your cashflow How Grant Thornton can provide Assurance to your organisation VAT Process review An overall review of your VAT compliance with comparisons made to best practice. The review would undertake the following activities: Benefits • A comprehensive end to end review of your VAT compliance, analysing data flow from your accounting source systems through to your VAT return • Benchmarking against ‘best practice’ • The company could demonstrate it has taken steps to pro-actively manage risk • Identification of potential VAT savings and refunds ExcaVATe VAT Systems review • ExcaVATe is a bespoke process combining specialist data mining software with the experience and insight of our advisors to deliver a review built around your specific requirements • This analysis can identify cash saving opportunities as well as highlighting process and control weaknesses • ExcaVATe uses methods similar to those used by HMRC undertaking reviews of this nature • develop an understanding of your business processes and systems • interview your people and review your documentation to map the processes • analyse maps for risk points and potential exposures • work with you to design and carry out diagnostics tests • report throughout on our findings, risk issues and potential areas for further review • work with you to come up with practical solutions • assist in the implementation of these solutions • perform further testing to confirm implementations. © 2014GrantThorntonUK LLP.All rights reserved. 'Grant Thornton’ refers to the brand under which the Grant Thornton member firms provide assurance, tax and advisory services to their clients and/or refers to one or more member firms, as the context requires. Grant Thornton UK LLP is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. GTIL and each member firm is a separate legal entity. Services are delivered by the member firms. GTIL does not provide services to clients. GTIL and its member firms are not agents of, and do not obligate, one another and are not liable for one another’s acts or omissions. This information has been prepared only as a guide. No responsibility can be acceptedby us for loss occasionedto any personactingor refrainingfrom actingas a result of this material. grant-thornton.co.uk V22847