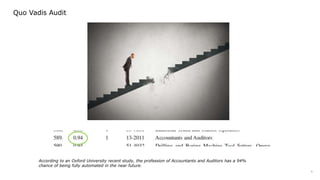

In an Oxford study in recent years, Audit was evaluated as one of the most likely professions to be fully automated in the near future / with a probability of 94%.

While the pressure for more effective and efficient audits has always been there, in recent years one can also see a clear trend of greater expectations towards auditors.

Regulators, clients and the public want to see beyond the pages of the Audit Opinion. They don’t want to get just assurance, they want to get insights.

While routine procedures can be performed in a more automated way, insight requires knowledge that goes beyond data analysis.

Auditors accumulate a vast experience throughout their career in subjects that go beyond just the financial figures: understanding of the industry, value creating mechanisms, governance and control, systems and processes etc.

All this can generate valuable insight that can be channeled through various services both in the Assurance and Advisory area.

Through this presentation in the conference organized for the 20 years anniversary of IEKA, I outline some of the ways in which auditors can expand their role in the future in a meaningful way for businesses in Albania and the region.