"القرض الروسي" لتمويل البرنامج النووي المصري من منظور مبدأ "الديون الكريهة"Dr. Islam Abou Elmagd

الديون السيادية , أي تلك الديون التي تقوم الإئتلافات المهيمنة على نظم الحكم , والتي تسيطر على القرار السياسي والاقتصادي في دولة بإستدانتها , ويتحملها الجيل الحالي من المواطنين والأجيال القادمة , تعد من أهم سبل تمويل دخول للأعضاء والمجموعات المكونة لهذا الإئتلاف المهيمن على نظم الحكم , عن طريق إستخدام تلك الديون بشكل مباشر أو غير مباشر في منح إمتيازات تدر دخل في إطار الفساد لتلك الفئات.

The document provides an overview of Estonia's tax system and structure. Some key points include:

- Estonia has a flat tax rate system with a 21% personal income tax rate and 21% corporate tax rate on distributed profits.

- Taxes include direct taxes like personal income tax, corporate income tax, and social tax as well as indirect taxes like VAT.

- The tax system aims to be simple with a broad tax base and low rates to encourage business and economic growth. Estonia was a pioneer in introducing a flat tax system in 1994.

"القرض الروسي" لتمويل البرنامج النووي المصري من منظور مبدأ "الديون الكريهة"Dr. Islam Abou Elmagd

الديون السيادية , أي تلك الديون التي تقوم الإئتلافات المهيمنة على نظم الحكم , والتي تسيطر على القرار السياسي والاقتصادي في دولة بإستدانتها , ويتحملها الجيل الحالي من المواطنين والأجيال القادمة , تعد من أهم سبل تمويل دخول للأعضاء والمجموعات المكونة لهذا الإئتلاف المهيمن على نظم الحكم , عن طريق إستخدام تلك الديون بشكل مباشر أو غير مباشر في منح إمتيازات تدر دخل في إطار الفساد لتلك الفئات.

The document provides an overview of Estonia's tax system and structure. Some key points include:

- Estonia has a flat tax rate system with a 21% personal income tax rate and 21% corporate tax rate on distributed profits.

- Taxes include direct taxes like personal income tax, corporate income tax, and social tax as well as indirect taxes like VAT.

- The tax system aims to be simple with a broad tax base and low rates to encourage business and economic growth. Estonia was a pioneer in introducing a flat tax system in 1994.

The document summarizes Estonia's tax system and structure. It outlines that Estonia's tax system aims to be simple, stable, broad-based and transparent with low tax rates. The main taxes include personal income tax, corporate income tax, VAT, excise duties and social tax. Personal income tax rates are 20% with deductions available. Corporate income tax is 20% on distributed profits and 14% on regularly distributed profits. VAT and excise duties are also important indirect taxes. Overall, the tax burden in Estonia averages around 33% of GDP.

The document summarizes Estonia's tax system and structure. It outlines the main principles of the Estonian tax system including a simple, stable system with broad tax bases and low rates. The tax system consists of direct taxes such as personal income tax, corporate income tax, and social tax, as well as indirect taxes like VAT and excise duties. Personal income tax rates are a flat 20% while corporate income tax is charged at 20% on distributed profits and 14% on regularly distributed profits.

The Estonian tax system aims for simplicity, stability, broad tax bases and low rates. It consists of direct taxes like personal income tax at 20%, corporate income tax at 20% on distributed profits, and indirect taxes like VAT at 20%. The tax authority is the Tax and Customs Board which collects various taxes that make up around a third of Estonia's GDP and funds the government. Personal income tax revenue has grown steadily while corporate income tax fluctuates based on profit distributions.

Estonian taxes and tax structure as of September 2020. A presentation by the Tax Policy Department of the Ministry of Finance of the Republic of Estonia

The document is a disclaimer for an investor presentation by the Republic of Estonia. It states that the information provided does not constitute an offer to purchase securities and any investment decisions should not be based on this information alone. The information is for informational purposes only and should not be redistributed or used for any other purpose. Projections and forecasts included are based on government budget numbers and actual results may differ.

The document provides an overview of Estonia's tax system and structure as of January 1, 2019. It discusses the main principles of Estonia's tax policy including a simple and stable tax system with a broad tax base and low rates. It outlines the direct taxes of personal income tax, corporate income tax, and others. It also discusses indirect taxes such as VAT and excise duties. Key points covered include tax rates, tax revenue sources, and the tax authority.

The document provides an overview of Estonian taxes and tax structure as of June 1, 2017. It discusses the main principles of Estonia's tax system including a simple tax system and broad tax base with low rates. It then outlines the major taxes in Estonia including direct taxes like personal income tax, corporate income tax, social tax, and land tax as well as indirect taxes like VAT, excise duties, and customs duty. It provides details on the rates and calculations for personal income tax, corporate income tax, social tax, and land tax.

The document summarizes Estonia's tax system and structure. It outlines that Estonia's tax system aims to be simple, stable, broad-based and transparent with low tax rates. The main taxes include personal income tax, corporate income tax, VAT, excise duties and social tax. Personal income tax rates are 20% with deductions available. Corporate income tax is 20% on distributed profits and 14% on regularly distributed profits. VAT and excise duties are also important indirect taxes. Overall, the tax burden in Estonia averages around 33% of GDP.

The document summarizes Estonia's tax system and structure. It outlines the main principles of the Estonian tax system including a simple, stable system with broad tax bases and low rates. The tax system consists of direct taxes such as personal income tax, corporate income tax, and social tax, as well as indirect taxes like VAT and excise duties. Personal income tax rates are a flat 20% while corporate income tax is charged at 20% on distributed profits and 14% on regularly distributed profits.

The Estonian tax system aims for simplicity, stability, broad tax bases and low rates. It consists of direct taxes like personal income tax at 20%, corporate income tax at 20% on distributed profits, and indirect taxes like VAT at 20%. The tax authority is the Tax and Customs Board which collects various taxes that make up around a third of Estonia's GDP and funds the government. Personal income tax revenue has grown steadily while corporate income tax fluctuates based on profit distributions.

Estonian taxes and tax structure as of September 2020. A presentation by the Tax Policy Department of the Ministry of Finance of the Republic of Estonia

The document is a disclaimer for an investor presentation by the Republic of Estonia. It states that the information provided does not constitute an offer to purchase securities and any investment decisions should not be based on this information alone. The information is for informational purposes only and should not be redistributed or used for any other purpose. Projections and forecasts included are based on government budget numbers and actual results may differ.

The document provides an overview of Estonia's tax system and structure as of January 1, 2019. It discusses the main principles of Estonia's tax policy including a simple and stable tax system with a broad tax base and low rates. It outlines the direct taxes of personal income tax, corporate income tax, and others. It also discusses indirect taxes such as VAT and excise duties. Key points covered include tax rates, tax revenue sources, and the tax authority.

The document provides an overview of Estonian taxes and tax structure as of June 1, 2017. It discusses the main principles of Estonia's tax system including a simple tax system and broad tax base with low rates. It then outlines the major taxes in Estonia including direct taxes like personal income tax, corporate income tax, social tax, and land tax as well as indirect taxes like VAT, excise duties, and customs duty. It provides details on the rates and calculations for personal income tax, corporate income tax, social tax, and land tax.

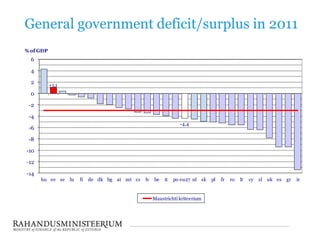

1. General government deficit/surplus in 2011

% of GDP

6

4

2 +1,1

0

-2

-4

-4,4

-6

-8

-10

-12

-14

hu ee se lu fi de dk bg at mt cz lv be it po eu27 nl sk pl fr ro lt cy sl uk es gr ir

Maastrichti kriteerium

2. General government debt in 2011

% of GDP

180

Maastrichti kriteerium

160

140

120

100

82,5

80

60

40

20

6,1

0

ee bg lu ro se lt cz lv sk dk sl fi pl nl es mt cy at de hu eu27 uk fr be ir po it gr

3. General government revenue in 2011

% of GDP

70

60

50

44,7

39,4

40

30

20

10

0

lt ro sk bg ir lv es pl ee mt cz cy uk lu gr sl de eu27 po nl it at be fr se hu fi dk

4. General government expenditure in 2011

% of GDP

70

60

49,1

50

38,3

40

30

20

10

0

bg lt ro sk ee lv lu mt cz pl es de cy ir uk eu27 po hu nl it at sl se gr be fi fr dk