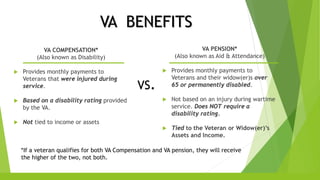

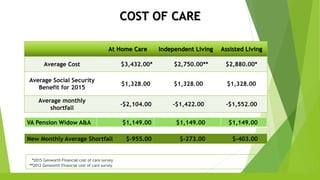

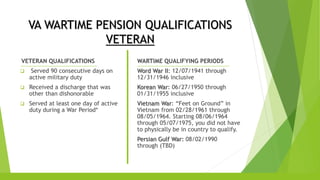

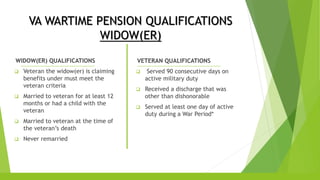

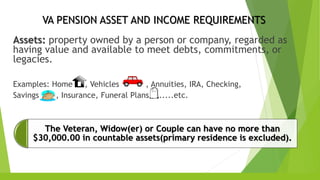

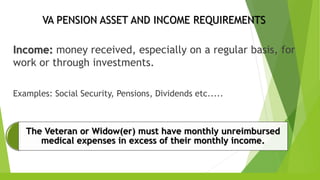

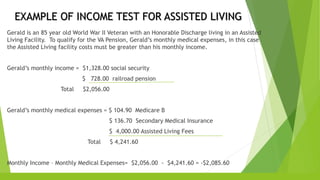

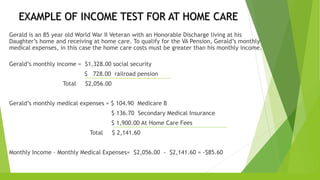

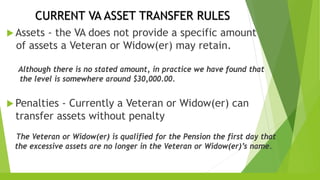

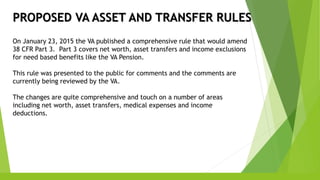

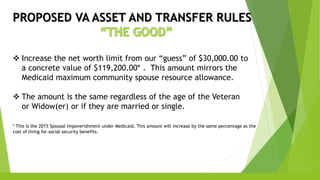

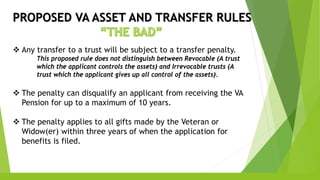

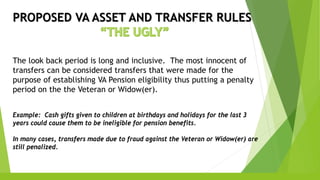

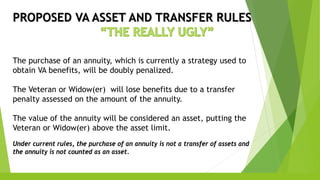

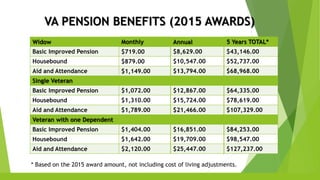

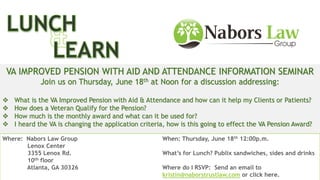

This presentation provides information about the VA Improved Pension with Aid and Attendance benefit. It discusses the qualifications for veterans and widows/widowers to receive the pension, how assets and income are assessed, and the monthly award amounts in 2015 which ranged from $719 to $2,120 depending on status. It also notes that proposed new VA rules may increase asset limits but also implement penalties for asset transfers, potentially disqualifying applicants for up to 10 years. The purpose is to make attendees aware of this underutilized benefit and help spread information to patients and clients who may be eligible.