Download to read offline

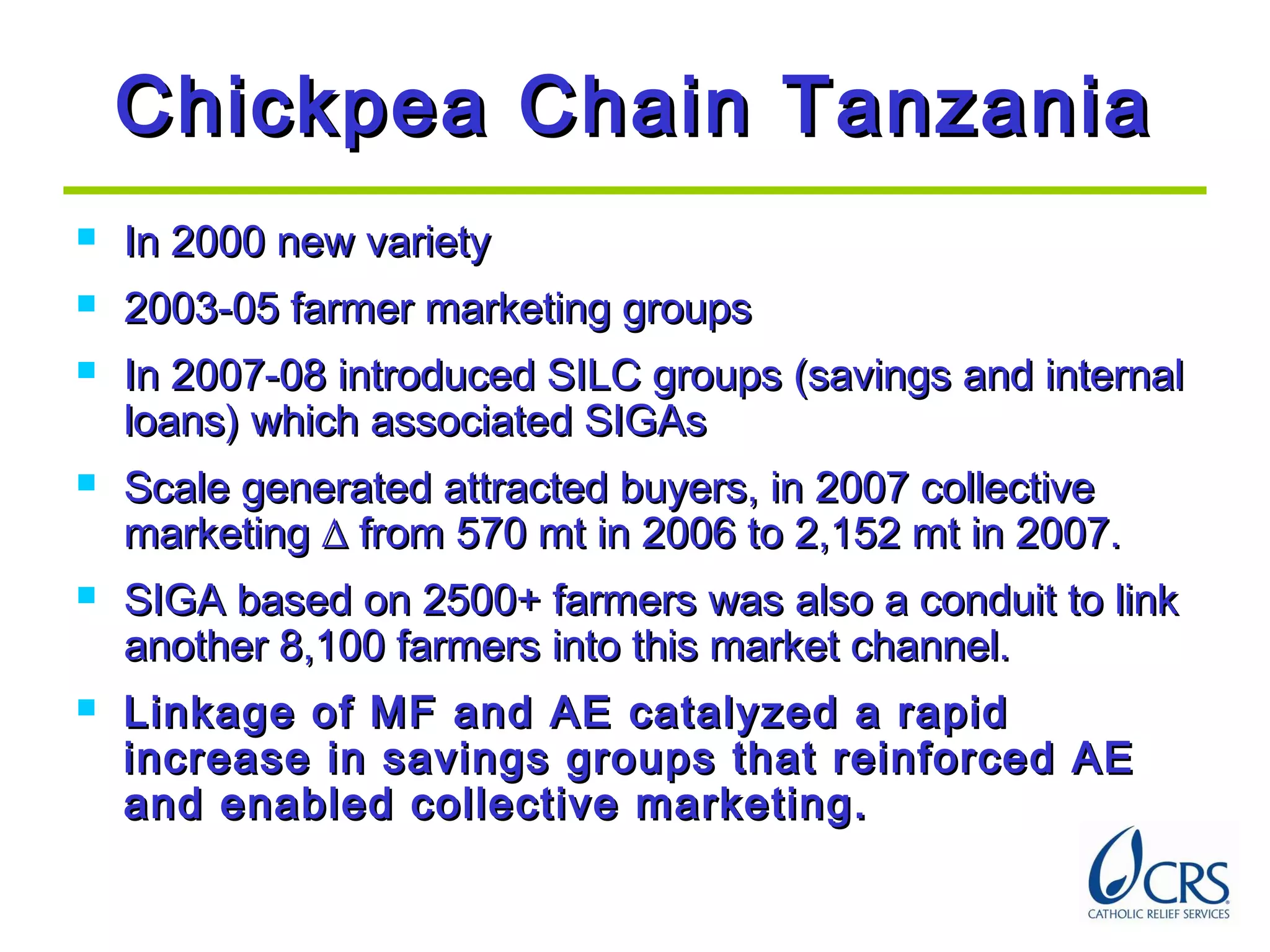

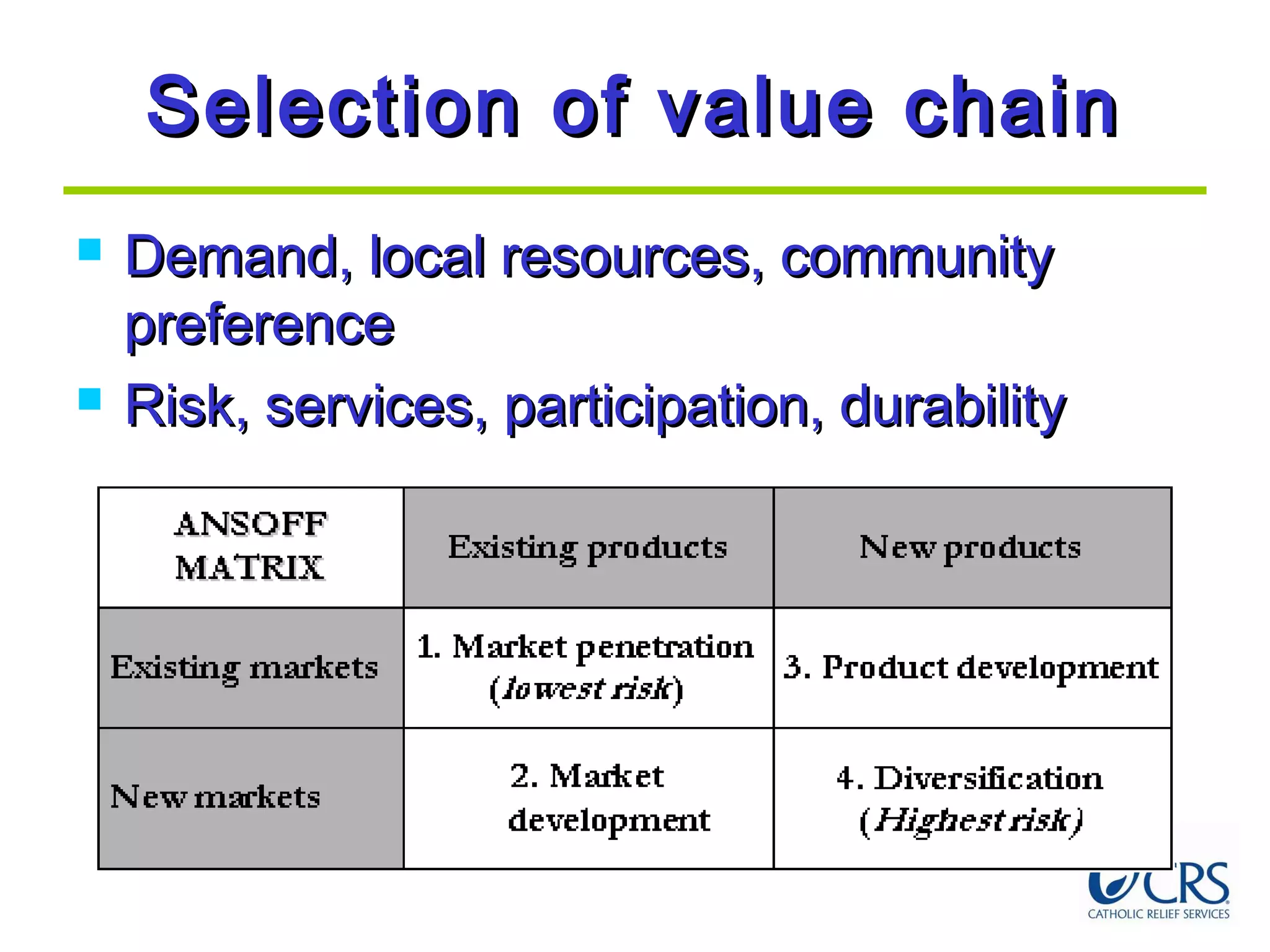

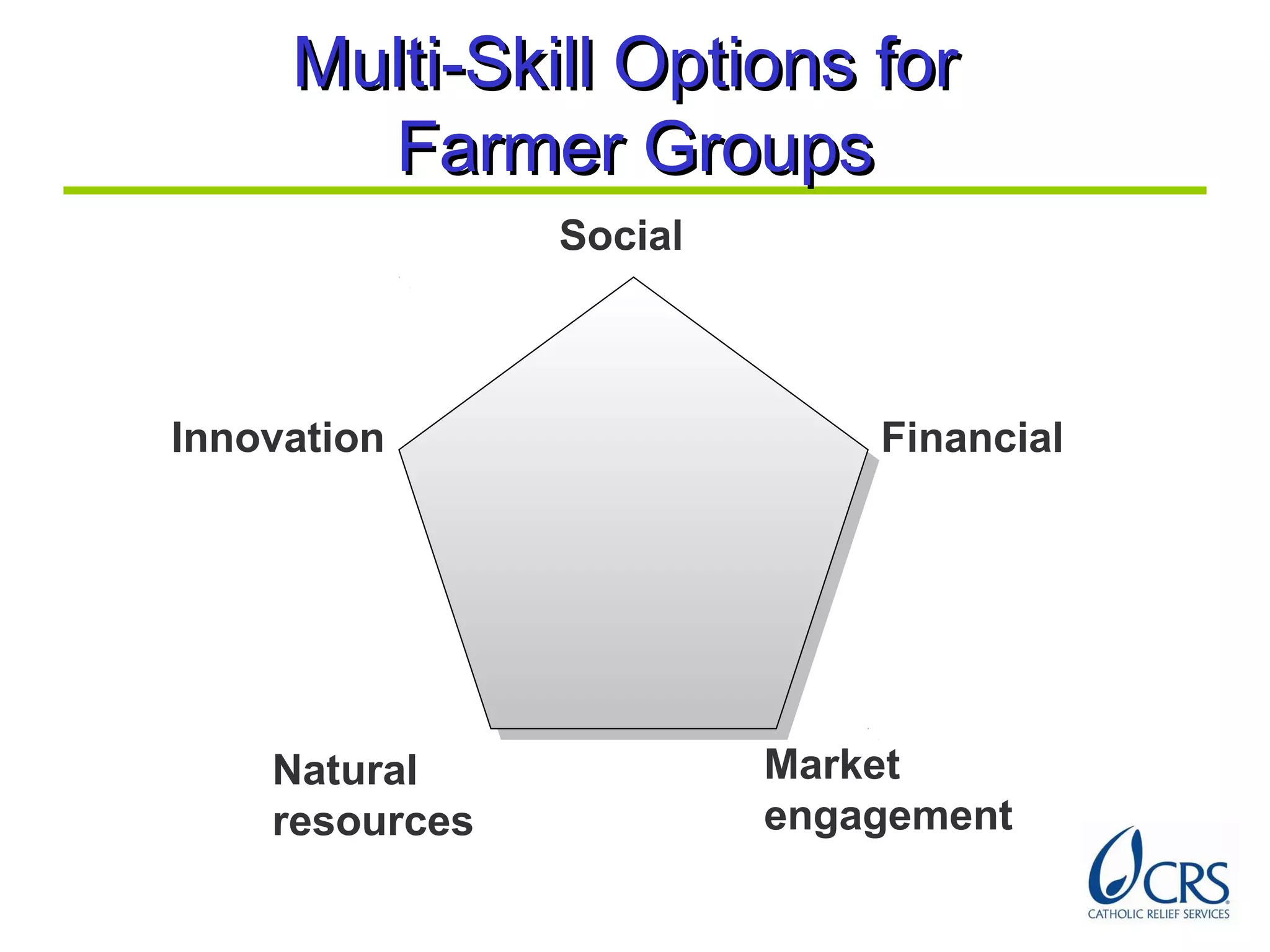

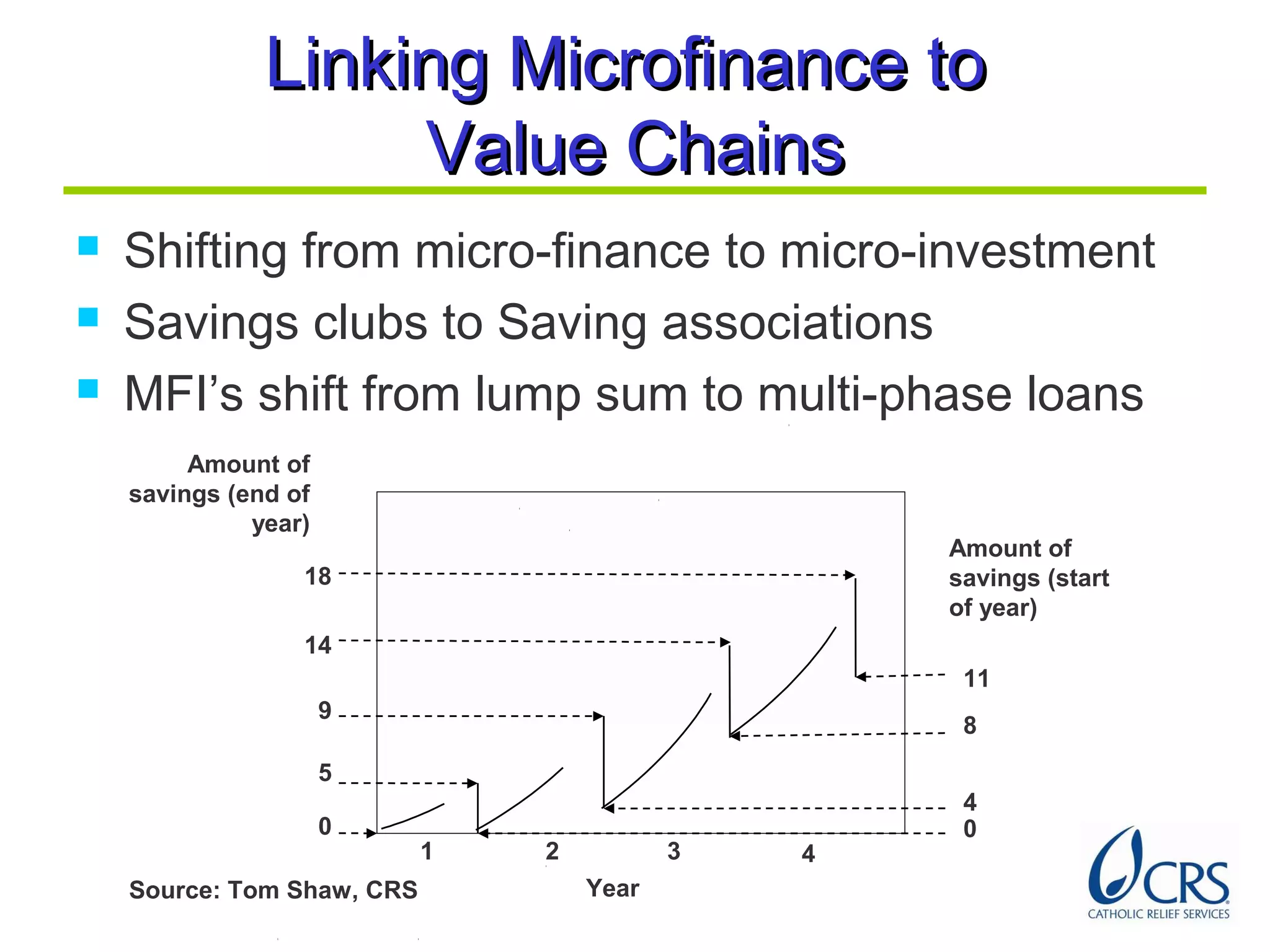

CRS implemented Agroenterprise Learning Alliances over 5 years to help shift smallholder farmers from subsistence agriculture to competitive agroenterprise. The goal was to provide a bridge from relief to development by linking farmers to markets, diversifying crops, strengthening access to finance and services, and improving food security. Key aspects included participatory value chain development, multi-skill training for farmer groups, savings mobilization, strengthening local service providers, and integrating infrastructure, training and marketing linkages. Case studies in navy beans in Ethiopia and chickpeas in Tanzania showed increases in farmers, crops, and collective marketing. Challenges remained around skills transfer, farmer organization, value chain analysis, access to finance and information for rural