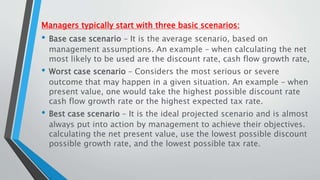

This document provides information on various valuation models and cash flow concepts used in discounted cash flow analysis. It defines key terms like FCFF, FCFE, scenario analysis and provides examples of how to calculate free cash flows. It also outlines the differences between FCFF and FCFE and discusses the benefits of scenario analysis for evaluating potential outcomes and making informed decisions.

![FCFF(FREE CASH FLOW FOR FIRM)

• After operational and investing expenses are paid, free cash flow is the amount of money

available to investors. Free cash flow to the firm (i.e., FCFF) and Free cash flow to equity

(i.e., FCFE) are two different forms of free cash flow measurements used in valuation.

We usually refer to FCFF when we speak of free cash flow (FCF). Operating EBIT is

normally adjusted for non-cash expenses as well as fixed and working capital

investments to arrive at FCFF.

• FCFF = Operating EBIT – Tax + Depreciation or Amortization (non-cash expenses) –

Fixed capital expenditures – Increase in net working capital

• Alternatively, FCFF = Cash flow from operations (taken from cash flow statement) +

Interest expense adjusted for tax – Fixed capital expenditures

• FCFF = Net Income + Interest expense adjusted for tax + non-cash expenses – Fixed

capital expenditures – Increase in net working capital

• Thus, FCFF stands for free cash flow for the firm and it is a financial performance metric

that looks at the amount of cash created by a company after all expenses, taxes,

changes in net working capital, and changes in investments have been taken into

account.

• After all other outflows have been controlled and paid, the FCFF is the amount that is

dispersed to the firm’s stockholders and bondholders. Calculating the FCFF is necessary

for any business because it serves as a tool for measuring its profitability and financial

stability. If the FCFF has a positive value, it means the company has a surplus after

expenses are stripped away; if the FCFF has a negative value, the company is in danger

of not having enough revenue to cover expenses or investments[1].](https://image.slidesharecdn.com/unit2valuation-230623131116-27346a86/85/UNIT-2-VALUATION-pptx-10-320.jpg)