Understanding Section 1061:

CarriedInterest Rules

Section 1061 of the Internal Revenue Code reshapes how investment profits

are taxed, particularly for fund managers receiving carried interest.

2.

The Three-Year Rule

Pre-2017

Fundmanagers paid lower capital gains rates (20-23%) after

holding assets for just one year.

Tax Cuts and Jobs Act

Introduced Section 1061, changing the holding period

requirement.

Current Rule

Fund managers must now hold assets for more than three years

to access lower tax rates.

3.

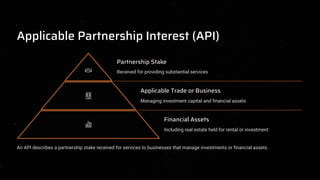

Applicable Partnership Interest(API)

Partnership Stake

Received for providing substantial services

Applicable Trade or Business

Managing investment capital and financial assets

Financial Assets

Including real estate held for rental or investment

An API describes a partnership stake received for services to businesses that manage investments or financial assets.

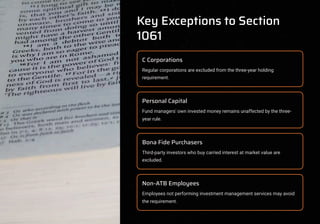

4.

Key Exceptions toSection

1061

C Corporations

Regular corporations are excluded from the three-year holding

requirement.

Personal Capital

Fund managers' own invested money remains unaffected by the three-

year rule.

Bona Fide Purchasers

Third-party investors who buy carried interest at market value are

excluded.

Non-ATB Employees

Employees not performing investment management services may avoid

the requirement.

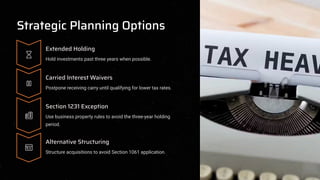

5.

Strategic Planning Options

ExtendedHolding

Hold investments past three years when possible.

Carried Interest Waivers

Postpone receiving carry until qualifying for lower tax rates.

Section 1231 Exception

Use business property rules to avoid the three-year holding

period.

Alternative Structuring

Structure acquisitions to avoid Section 1061 application.