Downloaded 11 times

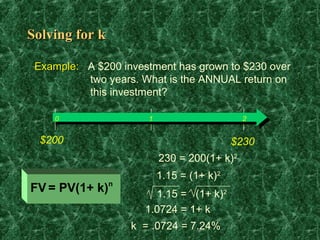

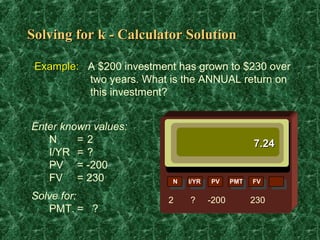

Let k = annual rate of return FV = PV(1+k)n 230 = 200(1+k)2 1.15 = (1+k)2 1.075 = 1+k .075 = k k = 7.5% annual return Therefore, the annual return on this investment is 7.5% Solving for k Example: You invest $1,000 today and want it to grow to $1,500 in 5 years. What rate of return is needed? 0 1 2 $1,000 $1,500