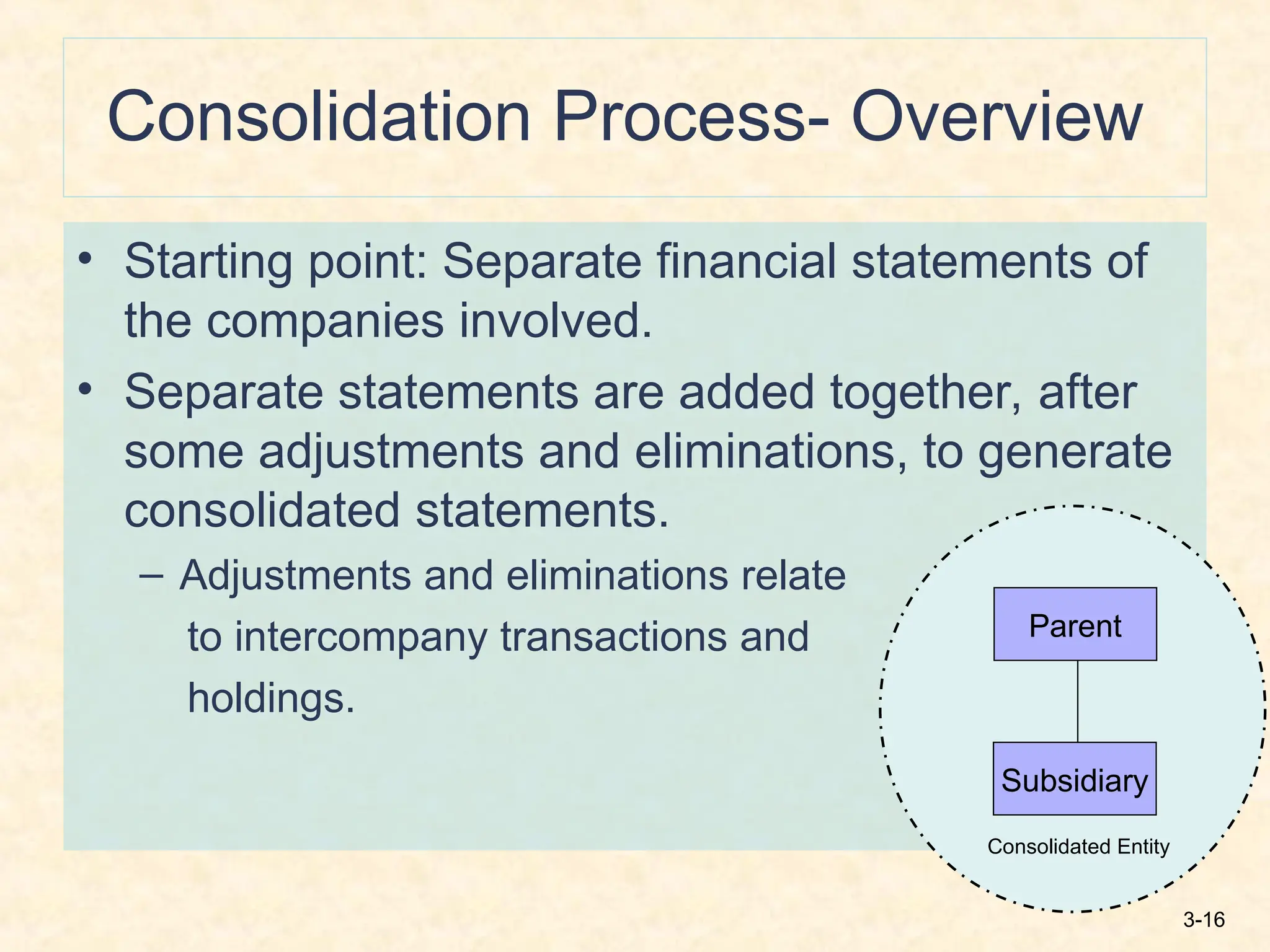

Consolidated financial statements present the financial position and results of operations for a parent (controlling entity) and one or more subsidiaries (controlled entities) as if the individual entities actually were a single company or entity.

Consolidation is required when a corporation owns a majority of another corporation’s outstanding common stock and occasionally under other circumstances.

Two companies are considered to be related when one controls the other or both are under the common control of another entity.

The same accounting principles should be applied in preparing consolidated financial statements as in preparing separate-company financial statements.

More useful than the separate financial statements of the individual companies when the companies are related

Presented primarily for those parties having a long-run interest in the parent company, including its management, shareholders, long-term creditors or other resource providers.

Often provide the only means of obtaining a clear picture of the total resources of the combined entity that are under the parent's control.

Results of individual companies included in the consolidation are not disclosed, thereby hiding poor performance.

Not all the consolidated retained earnings balance is necessarily available for dividends of the parent.

Financial ratios are not necessarily representative of any single company in the consolidation.

Similar accounts of different companies that are combined in the consolidation may not be entirely comparable.

Additional information about companies may be needed for a fair presentation, thus requiring voluminous footnotes.

Information is lost any time data sets are aggregated

Creditors, preferred stockholders, and noncontrolling common stockholders of subsidiaries are most interested in the separate financial statements of the subsidiaries in which they have an interest.

Because subsidiaries are legally separate from their parents, the creditors and stockholders of a subsidiary generally have no claim on the parent, and the stockholders of the subsidiary do not share in the profits of the parent

Traditional view of control includes:

Direct control that occurs when one company owns a majority of another company’s common stock.

Indirect control or pyramiding that occurs when a company’s common stock is owned by one or more other companies that are all under common control.

Differences in Fiscal Periods

Difference in the fiscal periods of a parent and subsidiary should not preclude consolidation.

Often the fiscal period of the subsidiary is changed to coincide with that of the parent.

Another alternative is to adjust the financial statement data of the subsidiary each period to place the data on a basis consistent with the fiscal period of the parent.

Changing Concept of the Reporting Entity

FASB 94, requiring consolidation of all majority-owned subsidiaries, was issued to eliminate the inconsistencies found in practice until a more comprehensi