1. Page of

Economic Commentary

QNB Economics

economics@qnb.com

January

The Great Deflation of 2015

The global economy has started 2015 on the

wrong foot. The sharp decline in oil prices

pushed the Eurozone into deflation in

December and resulted in a significant

slowdown in inflation in Japan, the UK and the

US. More worrisome, there is growing

evidence that these disinflationary pressures

are affecting wages and, to a lesser extent,

asset prices. This is leading global investors to

further hedge against deflation by buying

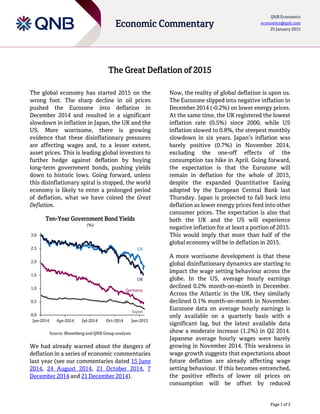

long-term government bonds, pushing yields

down to historic lows. Going forward, unless

this disinflationary spiral is stopped, the world

economy is likely to enter a prolonged period

of deflation, what we have coined the Great

Deflation.

Ten-Year Government Bond Yields

(%)

Source: Bloomberg and QNB Group analysis

We had already warned about the dangers of

deflation in a series of economic commentaries

last year (see our commentaries dated 15 June

, 24 August 2014, 21 October 2014, 7

December 2014 and 21 December 2014).

Now, the reality of global deflation is upon us.

The Eurozone slipped into negative inflation in

December 2014 (- on lower energy prices.

At the same time, the UK registered the lowest

inflation rate (0.5%) since 2000, while US

inflation slowed to 0.8%, the steepest monthly

slowdown in six years. Japan’s inflation was

barely positive (0.7%) in November 2014,

excluding the one-off effects of the

consumption tax hike in April. Going forward,

the expectation is that the Eurozone will

remain in deflation for the whole of 2015,

despite the expanded Quantitative Easing

adopted by the European Central Bank last

Thursday. Japan is projected to fall back into

deflation as lower energy prices feed into other

consumer prices. The expectation is also that

both the UK and the US will experience

negative inflation for at least a portion of 2015.

This would imply that more than half of the

global economy will be in deflation in 2015.

A more worrisome development is that these

global disinflationary dynamics are starting to

impact the wage setting behaviour across the

globe. In the US, average hourly earnings

declined 0.2% month-on-month in December.

Across the Atlantic in the UK, they similarly

declined 0.1% month-on-month in November.

Eurozone data on average hourly earnings is

only available on a quarterly basis with a

significant lag, but the latest available data

show a moderate increase (1.2%) in Q2 2014.

Japanese average hourly wages were barely

growing in November 2014. This weakness in

wage growth suggests that expectations about

future deflation are already affecting wage

setting behaviour. If this becomes entrenched,

the positive effects of lower oil prices on

consumption will be offset by reduced

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-2014 Apr-2014 Jul-2014 Oct-2014 Jan-2015

UK

Germany

US

Japan

2. Page of

Economic Commentary

QNB Economics

economics@qnb.com

January

expectations of future income, thus putting

further negative pressure on an already weak

aggregate demand. The impact on growth from

lower oil prices would therefore ultimately be

negative.

There is also growing evidence that

disinflationary pressures are hitting asset

prices. The latest available data show that

house prices are falling in China, the Eurozone,

Japan and Singapore and they are significantly

slowing down in the UK and the US. Going

forward, house prices are likely to decline

further as deflation and lower wage growth set

in. In London, for example, estate agents

expect house prices to drop by up to 5%,

according to the UK Royal Institute of

Chartered Surveyors. In addition, global equity

prices have fallen by about 5% since their peak

in early July 2014, according to the MSCI

World Advanced and Emerging Markets Index.

While this is still within the normal volatility

range, it suggests that equity markets are also

pricing in the impact of deflation on global

growth.

In summary, deflation is starting to spread into

lower global consumer prices, depressed wages

and, to a lesser extent, softer asset prices.

Unless governments around the world prop up

aggregate demand through an appropriate

fiscal response, this disinflationary dynamics

is likely to continue in 2015 and possibly

beyond.

Contacts

Joannes Mongardini

Head of Economics

- -

Rory Fyfe

Senior Economist

- -

Ehsan Khoman

Economist

- -

Hamda Al-Thani

Economist

- -

Ziad Daoud

Economist

- -

Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report.

Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend

on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a

complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group.