Download to read offline

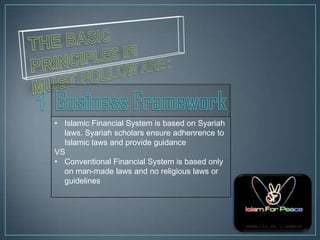

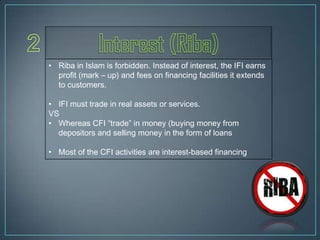

The document compares Islamic financial institutions (IFIs) and conventional financial institutions (CFIs). [1] IFIs must operate according to Islamic principles from the Quran and Sunnah, prohibiting interest and ensuring compliance with sharia. [2] IFIs use profit-sharing models like murabaha instead of interest for financing, and invest only in real assets, while CFIs use interest-based models. [3] IFIs aim to achieve socio-economic goals and serve all members of society, guided by sharia scholars, unlike the solely economic focus of CFIs.