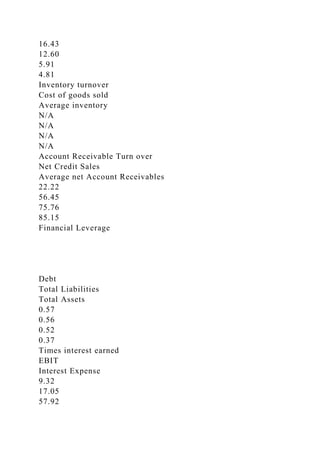

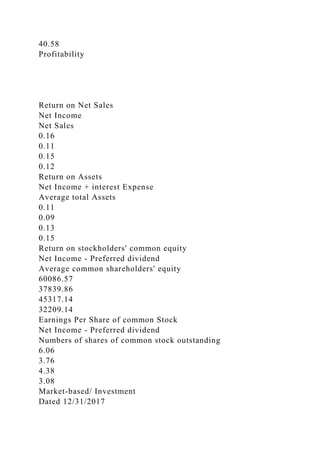

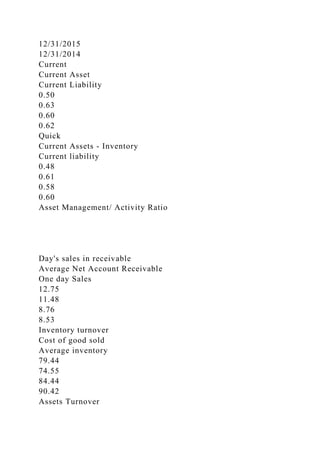

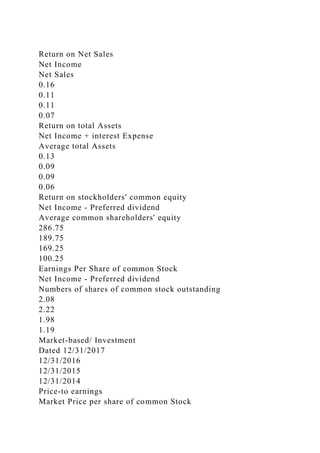

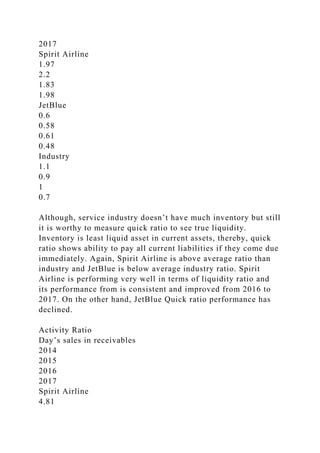

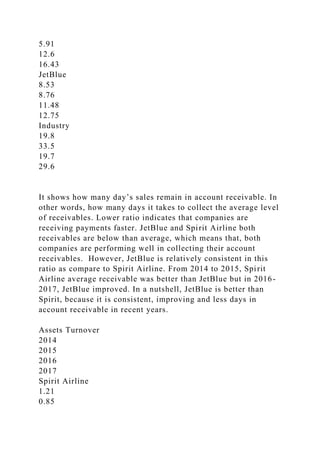

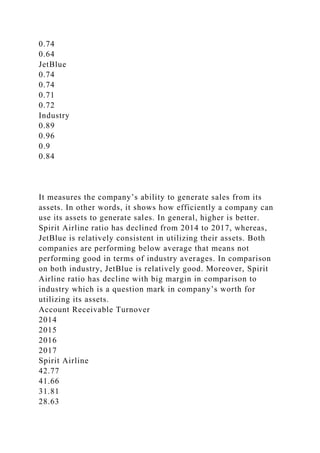

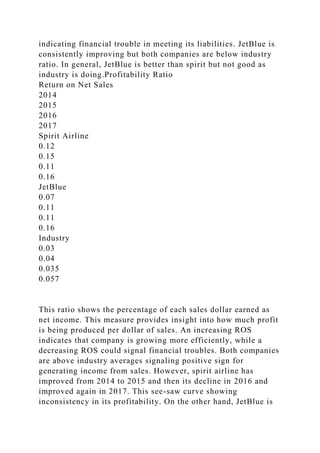

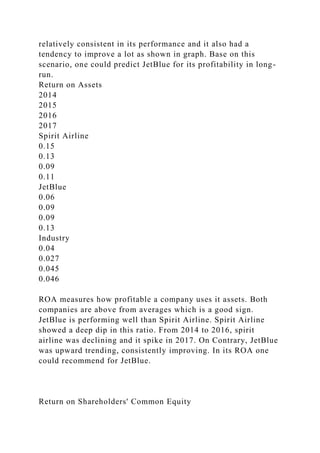

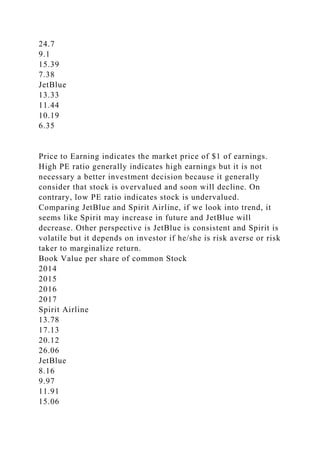

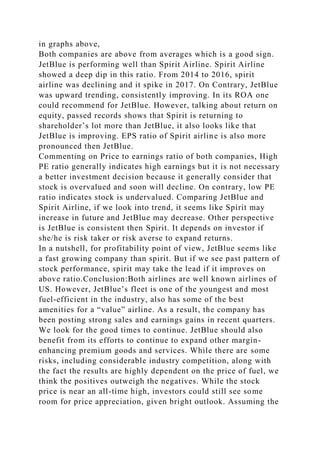

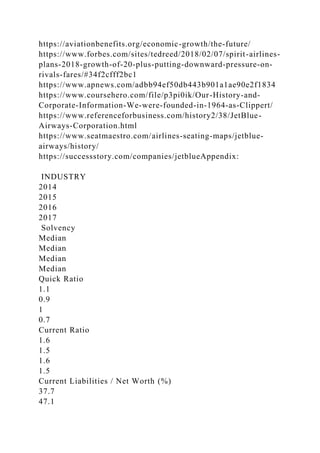

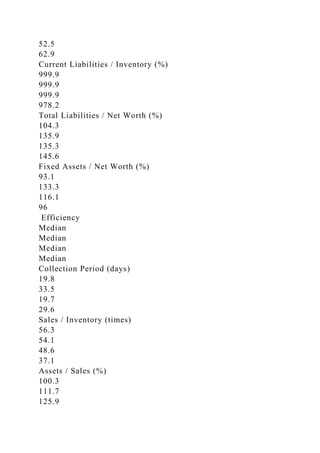

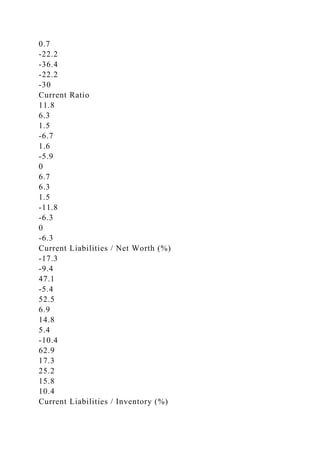

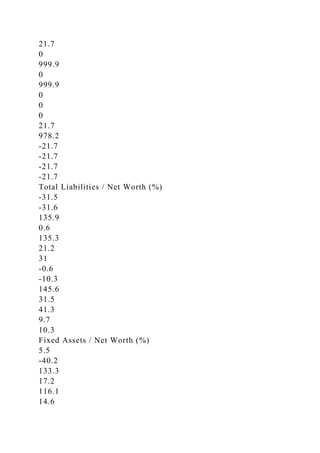

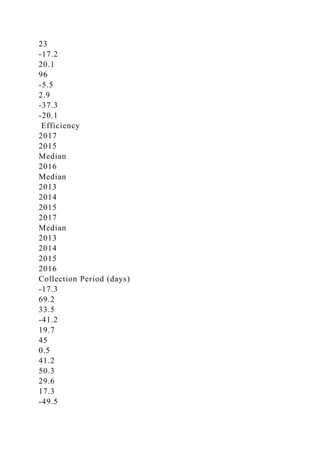

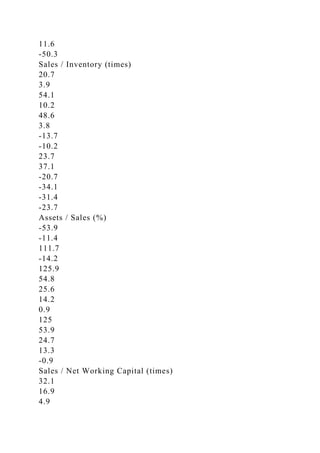

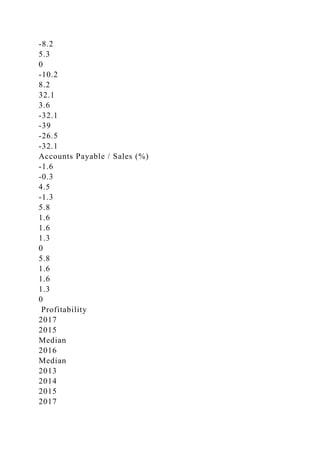

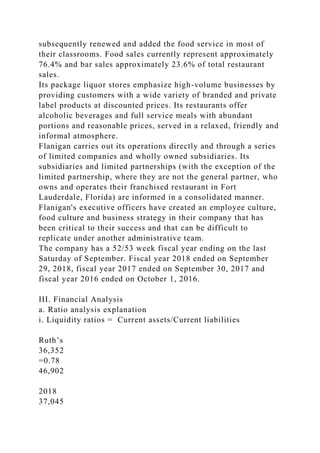

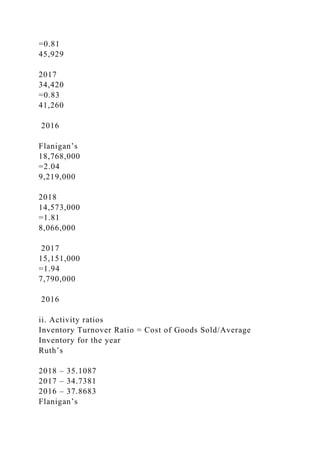

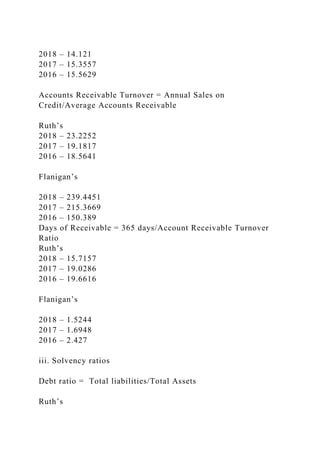

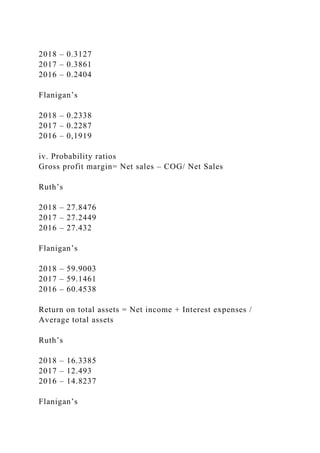

The document presents a comparative financial analysis of Spirit Airlines and JetBlue Airways between 2015 and 2017, focusing on business history, financial ratios, and investment attractiveness. It discusses the evolution of both airlines, highlighting their operational strategies and market positions within the airline industry. The analysis aims to draw insights and recommendations based on financial statements and industry trends to inform future business decisions.