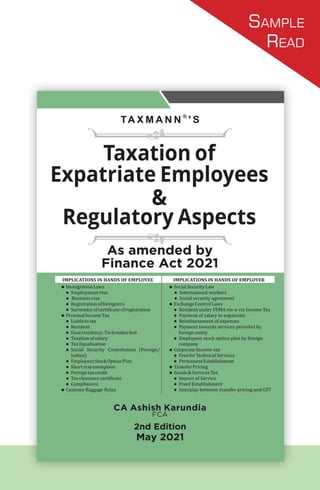

Taxmann's Taxation of Expatriate Employees & Regulatory Aspects

This book provides a comprehensive commentary to understand & comply with the taxation and regulatory aspect of the cross-border movement of employees, that results in secondment. As with any cross-border arrangement, multiple complex laws are involved, this book serves as a primer to understand these complexities and related compliances. The discussion in this book starts with determining who is the employer of the expatriate, which is important to identify the correct laws to be complied with. This book aims at providing the reader, an insight into implications that typically arise in secondment arrangement(s), under various Indian laws in the hands of the expatriate & company, such as: • Expatriate ◦ Immigration Laws ◦ Personal Income Tax ◦ Custom Baggage Rules • Company ◦ Social Security Laws ◦ Exchange Control Laws ◦ Corporate Income Tax ◦ Transfer Pricing ◦ Goods & Services Tax ◦ Corporate Law The Present Publication is the 2nd Edition, authored by Ashish Karundia, with the following noteworthy features: • [Explains Situs of Accrual of Salary], i.e. place of enforcement of employment contract or place of the rendering of services • [Social Security Deduction] Discusses taxability as well as deductibility of contribution to overseas social security contribution in the hands of the employee • [Disputed Salary Ingredients] Captures detailed analysis of disputed salary ingredients such as: ◦ Per-Diem/Per-Day Allowance ◦ Tax Equalization ◦ Hypothetical Tax ◦ Employee Stock Option Plan(s) • [Short Stay Exemption] Explains the conditions for short stay exemption and related issues • [Employment Visa vs. Business Visa] Points out the difference between employment visa and business visa • Explains various clauses such as detachment, exportability and totalization of social security agreements • [Meaning of Resident] Lucidly explains the difference between ‘resident’ as per income-tax and ‘resident’ as per FEMA • [Deemed International Transactions] Explains whether secondment agreement will qualify as deemed international transaction or not • [Case Laws] for deciding the employer employee relationship. • Explains situations when fixed establishment (GST) of the foreign entity is triggered

Recommended

More Related Content

More from Taxmann

More from Taxmann (20)

Taxmann's Taxation of Expatriate Employees & Regulatory Aspects

- 1. Sample Read

- 3. I-5 About the Author Ashish Karundia i s a p r a c t i s i n g C h a r t e r e d A c c o u n t a n t h a v i n g a p o s t q u a l i f i c a t i o n e x p e r i e n c e o f m o r e t h a n 1 0 y e a r s . H i s e x p e r t i s e l i e s i n i n t e r p r e t i n g v a r i o u s l a w s a n d i n t e r - c o n n e c t i n g l e a r n i n g ’ s a c r o s s t h e v a r i e d s u b j e c t s t o g i v e a 3 6 0 - d e g r e e v i e w o n t h e i s s u e s e x a m i n e d b y h i m . H e h a s e x p e r i e n c e i n i n d i r e c t t a x e s , viz., s a l e s t a x / V A T a n d G S T , d i r e c t t a x e s , i n t e r n a t i o n a l t a x a n d t a x t r e a t i e s . H e r e g u l a r l y a d v i s e s c l i e n t s o n c o m p l e x i s s u e s o f t r e a t y i n t e r p r e t a t i o n s u c h a s p e r m a n e n t e s t a b l i s h m e n t , s e c o n d m e n t , r o y a l t y a n d f e e s f o r t e c h n i c a l / i n c l u d e d s e r v i c e s . H e h a s a u t h o r e d a n u m b e r o f a r t i c l e s a t v a r i o u s p r o f e s s i o n a l f o r u m s . H i s w o r k r e c e i v e d h i g h e s t r e c o g n i t i o n w h e n h e w a s q u o t e d i n E q u a l i z a t i o n L e v y R e p o r t i s s u e d b y t h e E - C o m m e r c e C o m m i t t e e s e t u p b y t h e G o v e r n m e n t o f I n d i a . H i s b o o k o n P e r m a n e n t E s t a b l i s h m e n t i s v e r y w e l l r e c e i v e d b y t h e p r o f e s s i o n a l s a n d t a x a d m i n i s t r a t o r s e q u a l l y i n c l u d i n g A u t h o r i t y f o r A d v a n c e R u l i n g s – I n c o m e T a x . H e i s a l s o a n e m i n e n t m e m b e r o f T a x T r e a t y G r o u p h e a d e d b y M r . N e d S h e l t o n a d d r e s s i n g t r e a t y i s s u e s a r i s i n g w o r l d w i d e . H e w a s I n d i a ’ s C o u n t r y R e p o r t e r f o r 2 0 1 9 I F A L o n d o n C o n g r e s s . Education and Professional Affiliations u B . C o m . , G o r a k h p u r U n i v e r s i t y . u F C A , I n s t i t u t e o f C h a r t e r e d A c c o u n t a n t s o f I n d i a .

- 4. Preface Expansion of trade and commerce coupled with rapid economic growth has witnessed substantial cross-border movement of people. The cross-border movement of people can be due to various reasons such as movement of employees due to secondment/deputation, movement of independent service provider such as consultants, artists and entertainers. The cross-border movement of employees requires compliance with tax as well as non-tax laws of the host country. This book deals with aspects pertaining to cross-border movement of employees due to secondment arrangement. One of the key aspects in ensuring that all the laws/regulations are correctly complied with in the host country is to decide who is the employer of the expatriate. The book discusses various criteria laid down by the courts in deciding the employer employee relationship. It also serves as a guide for arriving at the optimum employment structure holistically. It further attempts to address implications under various laws in the hands of the stakeholders v i z . , expatriate (such as immigration, personal income tax and custom baggage rules), and the company (such as social security, exchange control, corporate income tax, transfer pricing, goods & services tax and corporate law). It is hoped that the tax administrators, professionals, authorities, researchers, scholars and other readers will find the book cogent and helpful. Any suggestions for the further improvement of the same are most welcome. D e l h i , I n d i a . ASHISH KARUNDIA I-7

- 6. P A G E About the author I-5 Preface I-7 Acknowledgement I-9 Contents I-13 List of cases I-21 Glossary of terms I-37 PART I INTRODUCTION CHAPTER 1 AN OVERVIEW 3 CHAPTER 2 EMPLOYER-EMPLOYEE RELATIONSHIP 8 PART II IMPLICATIONS IN THE HANDS OF EMPLOYEE CHAPTER 3 IMMIGRATION LAWS 19 CHAPTER 4 PERSONAL INCOME TAX 36 CHAPTER 5 CUSTOMS BAGGAGE RULES 94 PART III IMPLICATIONS IN THE HANDS OF COMPANY CHAPTER 6 SOCIAL SECURITY LAWS 99 CHAPTER 7 EXCHANGE CONTROL LAWS 120 CHAPTER 8 CORPORATE INCOME TAX 137 Chapter-heads I-11

- 7. P A G E CHAPTER 9 TRANSFER PRICING 177 CHAPTER 10 GOODS AND SERVICES TAX 190 CHAPTER 11 CORPORATE LAW 199 C H A P T E R - H E A D S I-12

- 8. Contents I-13 P A G E About the author I-5 Preface I-7 Acknowledgement I-9 Chapter-heads I-11 List of cases I-21 Glossary of terms I-37 PART I INTRODUCTION CHAPTER 1 AN OVERVIEW u A n O v e r v i e w 3 CHAPTER 2 EMPLOYER-EMPLOYEE RELATIONSHIP 2.1 P a r a m e t e r s t o d e t e r m i n e e m p l o y e r - e m p l o y e e r e l a t i o n s h i p 8 2.1.1 R i g h t t o c o n t r o l t h e m a n n e r i n w h i c h w o r k i s t o b e d o n e 9 2.1.2 R i g h t o f t h e e s t a b l i s h m e n t t o d i s m i s s o r s u s p e n d 10 2.1.3 U l t i m a t e a u t h o r i t y o n p e r f o r m a n c e o f w o r k e r s 12 2.1.4 O b l i g a t i o n o f p a y m e n t o f s a l a r y o r r i g h t t o r e c o v e r s a l a r y 12 2.1.5 A p p l i c a b i l i t y o f s e r v i c e r u l e s o f e s t a b l i s h m e n t s 12 2.1.6 C o n t r i b u t i o n t o s o c i a l s e c u r i t y b e n e fi t s s u c h a s p r o v i - d e n t f u n d s , g r a t u i t y e t c . 13

- 9. C O N T E N T S I-14 2.1.7 L i e n o n e m p l o y m e n t 13 2.1.8 I s s u e o f a p p o i n t m e n t l e t t e r s w i t h t e r m s a n d c o n d i - t i o n s o f a p p o i n t m e n t 14 2.2 I n g r e d i e n t s o f s e c o n d m e n t c o n t r a c t 14 PART II IMPLICATIONS IN THE HANDS OF EMPLOYEE CHAPTER 3 IMMIGRATION LAWS 3.1 G e n e r a l 19 3.2 P e r i o d o f v a l i d i t y o f p a s s p o r t a n d v i s a 20 3.3 T y p e s o f v i s a 20 3.4 E m p l o y m e n t v i s a 23 3.4.1 C o n d i t i o n s 23 3.4.2 D o c u m e n t s / i n f o r m a t i o n 25 3.4.3 E x t e n s i o n 26 3.4.4 C h a n g e o f E m p l o y e r 27 3.4.5 C o n v e r s i o n 27 3.5 B u s i n e s s V i s a 28 3.5.1 C o n d i t i o n s 28 3.5.2 D o c u m e n t s / i n f o r m a t i o n 30 3.5.3 E x t e n s i o n 31 3.5.4 C o n v e r s i o n 31 3.6 R e g i s t r a t i o n o f f o r e i g n e r s 32 3.7 S u r r e n d e r o f c e r t i fi c a t e o f r e g i s t r a t i o n 34 3.8 P e n a l c o n s e q u e n c e s 35 CHAPTER 4 PERSONAL INCOME TAX 4.1 G e n e r a l 36 4.1.1 S c o p e o f t o t a l i n c o m e 37 4.1.2 A c c r u e o r a r i s e 37 4.1.3 S i t u s o f a c c r u a l o f s a l a r y 38 P A G E

- 11. C O N T E N T S I-16 4.4.5.1 I m p l i c a t i o n u p o n w i t h d r a w a l o f s o c i a l s e c u r i t y c o n t r i b u t i o n 72 4.4.6 E m p l o y e e s s t o c k o p t i o n p l a n 74 4.4.6.1 T y p e s o f E S O P 74 4.4.6.2 A c c e l e r a t e d E S O P s 76 4.4.6.3 G r a n t o f E S O P b y G r o u p C o m p a n y 77 4.4.6.4 V e s t i n g o f E S O P i n m u l t i p l e c o u n t r i e s 78 4.4.6.5 S h a r e s w i t h l o c k i n p e r i o d 79 4.4.6.6 T r a n s f e r o f E S O P s 81 4.4.6.7 B u y b a c k o f E S O P s 81 4.5 S h o r t s t a y e x e m p t i o n 81 4.5.1 S t a y i n I n d i a i s u p t o 9 0 d a y s 81 4.5.2 S t a y i n I n d i a i s u p t o 1 8 3 d a y s 83 4.5.2.1 M e a n i n g o f d e r i v e d 84 4.5.2.2 E x e r c i s e o f e m p l o y m e n t i n t h e h o s t c o u n t r y 85 4.5.2.3 C o m p u t a t i o n o f 1 8 3 d a y s 86 4.5.2.4 M e a n i n g o f ‘ p a i d b y ’ 87 4.5.2.5 M e a n i n g o f ‘ b o r n e b y ’ 87 4.6 F o r e i g n t a x c r e d i t 90 4.7 T a x c l e a r a n c e c e r t i fi c a t e 91 4.8 C o m p l i a n c e s 92 4.9 P e n a l c o n s e q u e n c e 93 CHAPTER 5 CUSTOMS BAGGAGE RULES u C u s t o m s B a g g a g e R u l e s 94 PART III IMPLICATIONS IN THE HANDS OF COMPANY CHAPTER 6 SOCIAL SECURITY LAWS 6.1 M e a n i n g o f e m p l o y e e 100 P A G E

- 12. I-17 C O N T E N T S 6.2 M o n t h l y p a y 101 6.3 C o n t r i b u t i o n ( d o m e s t i c w o r k e r s ) 105 6.4 I n t e r n a t i o n a l w o r k e r s 106 6.4.1 C o n t r i b u t i o n 107 6.4.2 S p l i t p a y 109 6.4.3 W i t h d r a w a l 109 6.5 S o c i a l S e c u r i t y A g r e e m e n t 110 6.5.1 G e n e r a l 110 6.5.2 D e t a c h m e n t 112 6.5.3 E x p o r t a b i l i t y 114 6.5.4 T o t a l i s a t i o n 114 6.6 C o m p l i a n c e s 115 6.7 P e n a l C o n s e q u e n c e s 117 CHAPTER 7 EXCHANGE CONTROL LAWS 7.1 P e r s o n r e s i d e n t i n I n d i a 120 7.1.1 N o n - I n d i v i d u a l s 120 7.1.2 I n d i v i d u a l s 120 7.1.2.1 O u t b o u n d 121 7.1.2.2 I n b o u n d 121 7.1.2.3 R e s i d e n t b u t n o t p e r m a n e n t l y r e s i d e n t 125 7.2 R e s i d e n t u n d e r F E M A vis-a-vis I n c o m e T a x 125 7.3 P a y m e n t o f s a l a r y t o e x p a t r i a t e 126 7.4 R e p a t r i a t i o n o f f u n d s 128 7.4.1 S a l a r y 129 7.4.2 S o c i a l s e c u r i t y a c c u m u l a t i o n s 129 7.5 R e i m b u r s e m e n t o f e x p e n s e 130 7.5.1 I n c u r r e d b y f o r e i g n c o m p a n y o n b e h a l f o f I n d i a n c o m p a n y 130 7.5.1.1 S a l a r y 130 7.5.1.2 S o c i a l s e c u r i t y c o n t r i b u t i o n 130 P A G E

- 13. C O N T E N T S I-18 7.5.2 I n c u r r e d b y I n d i a n c o m p a n y o n b e h a l f o f f o r e i g n c o m p a n y 131 7.6 P a y m e n t t o w a r d s s e r v i c e s p r o v i d e d b y f o r e i g n e n t i t y 133 7.7 E m p l o y e e s s t o c k o p t i o n p l a n b y f o r e i g n c o m p a n y 134 7.7.1 I s s u a n c e o f E S O P 134 7.7.2 T r a n s f e r o f E S O P 135 7.7.3 B u y b a c k o f E S O P 135 7.8 P e n a l c o n s e q u e n c e 136 CHAPTER 8 CORPORATE INCOME TAX 8.1 R e i m b u r s e m e n t o f e x p e n s e i n c u r r e d b y f o r e i g n c o m p a n y ( s a y s a l a r y ) 138 8.2 I n c o m e i n t h e n a t u r e o f f e e s f o r t e c h n i c a l s e r v i c e s 140 8.2.1 M a k e a v a i l a b l e 143 8.2.2 A b s e n c e o f F T S c l a u s e i n D T A A 145 8.3 I n c o m e i n t h e n a t u r e o f b u s i n e s s 146 8.3.1 B u s i n e s s c o n n e c t i o n 146 8.3.2 P e r m a n e n t E s t a b l i s h m e n t 148 8.3.2.1 F i x e d P l a c e P E 148 8.3.2.2 S e r v i c e P E 156 8.3.2.3 A g e n c y P E 165 8.4 D o c u m e n t / i n f o r m a t i o n - T o a v a i l D T A A b e n e fi t 168 8.5 W i t h h o l d i n g o f t a x 169 8.6 C o m p l i a n c e s 172 8.7 P e n a l C o n s e q u e n c e s 175 CHAPTER 9 TRANSFER PRICING 9.1 G e n e r a l 177 9.2 T r a n s a c t i o n s b e t w e e n f o r e i g n c o m p a n y a n d I n d i a n c o m p a n y 183 9.2.1 P r o v i s i o n o f s e r v i c e s b y f o r e i g n c o m p a n y t o I n d i a n g r o u p c o m p a n y 183 P A G E

- 14. P A G E 9.2.2 A s s i g n m e n t o f t e c h n i c a l e m p l o y e e s b y f o r e i g n c o m p a n y t o I n d i a n c o m p a n y 183 9.2.3 G r a n t o f E S O P s b y f o r e i g n c o m p a n y t o e m p l o y e e s o f I n d i a n c o m p a n y 185 9.2.4 S o c i a l s e c u r i t y c o n t r i b u t i o n b y f o r e i g n c o m p a n y t o w a r d s e m p l o y e e s o f I n d i a n c o m p a n y 185 9.2.5 S e c o n d m e n t a g r e e m e n t 186 9.3 C o m p l i a n c e s 186 9.4 P e n a l c o n s e q u e n c e s 188 CHAPTER 10 GOODS AND SERVICES TAX 10.1 G e n e r a l 190 10.2 P r o v i s i o n o f s e r v i c e s 191 10.2.1 S e r v i c e p r o v i d e d b y e m p l o y e e t o i t s e m p l o y e r 191 10.2.1.1 E x p a t r i a t e i s e m p l o y e e o f I n d i a n e n t i t y 191 10.2.1.2 E x p a t r i a t e i s e m p l o y e e o f F o r e i g n e n t i t y 192 10.2.2 S e r v i c e p r o v i d e d b y e m p l o y e r t o e m p l o y e e 193 10.2.3 S e r v i c e p r o v i d e d b y f o r e i g n e n t i t y t o I n d i a n e n t i t y 193 10.2.3.1 R e v e r s e c h a r g e s u p p l i e s 193 10.2.3.2 F i x e d E s t a b l i s h m e n t 194 10.3 V a l u a t i o n o f s u p p l y b e t w e e n r e l a t e d p e r s o n s 195 10.3.1 O p e n m a r k e t v a l u e 196 10.3.2 V a l u e o f s u p p l y o f l i k e k i n d a n d q u a l i t y 196 10.3.3 V a l u e o f s u p p l y b a s e d o n c o s t 196 10.3.4 B e s t j u d g m e n t m e t h o d 196 10.3.5 S p e c i fi c c a s e s 197 10.4 I n t e r p l a y b e t w e e n t r a n s f e r p r i c i n g a n d G S T 197 10.5 R e i m b u r s e m e n t o f e x p e n s e i n c u r r e d b y f o r e i g n c o m p a n y ( s a y s a l a r y ) 198 CHAPTER 11 CORPORATE LAW 11.1 G e n e r a l 199 I-19 C O N T E N T S

- 15. P A G E 11.1.1 O r d i n a r y c o u r s e o f b u s i n e s s 200 11.1.2 A r m ’ s l e n g t h 200 11.1.3 C o n s e n t o f B o a r d o f D i r e c t o r s 201 11.1.4 A p p r o v a l o f S h a r e h o l d e r s 201 11.2 C o m p l i a n c e s 202 Case Study I 203 Case Study II 205 Case Study III 207 C O N T E N T S I-20

- 16. 3.1 GENERAL A n y p e r s o n e n t e r i n g 4 9 i n t o I n d i a f r o m a n y p l a c e o u t s i d e I n d i a s h o u l d b e i n p o s s e s s i o n o f v a l i d p a s s p o r t 5 0 e x c e p t c e r t a i n c l a s s o f p e r s o n s w h o a r e e x e m p t e d . 5 1 T h e c o n d i t i o n s 5 2 o f v a l i d p a s s p o r t i s a s f o l l o w s : a. i s s u e d b y o r o n b e h a l f o f t h e G o v e r n m e n t o f t h e c o u n t r y o f w h i c h t h e p e r s o n t o w h o m i t r e l a t e s i s a n a t i o n a l ; b. s h a l l b e w i t h i n t h e p e r i o d o f i t s v a l i d i t y ; c. a p h o t o g r a p h o f t h e p e r s o n t o w h o m i t r e l a t e s s h a l l b e a f f i x e d 5 3 a n d d u l y a u t h e n t i c a t e d b y t h e a u t h o r i t y i s s u i n g t h e p a s s p o r t ; d. 5 4 s h a l l h a v e b e e n e n d o r s e d b y a p p r o p r i a t e a u t h o r i t y b y w a y o f v i s a 5 5 f o r I n d i a i n o n e o r o t h e r o f t h e f o l l o w i n g k i n d s : Immigration Laws 3 C H A P T E R N o t e : T h e c h a p t e r i s b a s e d u p o n t h e i m m i g r a t i o n l a w , v i s a g u i d e l i n e s / c l a r i fi c a t i o n s i s s u e d b y r e l e v a n t a u t h o r i t i e s a s a v a i l a b l e i n p u b l i c d o m a i n ( u p t o 3 1 . 0 7 . 2 0 2 0 ) . 4 9 . b y w a t e r , l a n d o r a i r . 5 0 . S . 3 ( 1 ) , T P E I A r w R . 3 ( a ) a n d R . 5 , T P E I R . 5 1 . R . 4 , T P E I R . 5 2 . R . 5 , T P E I R . 5 3 . E x c e p t i n c e r t a i n c a s e s [ R. 5 ( ii ) , TPEIR ] . 5 4 . N o t a p p l i c a b l e t o t h e f o l l o w i n g : a . P a s s p o r t i s s u e d b y G o v e r n m e n t o f P a k i s t a n , B a n g l a d e s h a n d N e p a l . b . a n y p e r s o n t h e d u r a t i o n o f w h o s e s t a y i n I n d i a d o e s n o t e x c e e d n i n e t y d a y s ( s h a l l i n c l u d e a n y p r i o r p e r i o d o f s t a y o f s u c h p e r s o n i n I n d i a d u r i n g a p e r i o d o f s i x m o n t h s i m m e d i a t e l y b e f o r e t h e d a t e o f h i s e n t r y i n t o I n d i a ) a n d w h o i s i n p o s s e s s i o n o f a p a s s p o r t i s s u e d b y , o r o n b e h a l f o f , t h e G o v e r n m e n t o f M a l d i v e s . c . a n y p e r s o n h o l d i n g P I O C a r d ( i s s u e d t o p e r s o n b e i n g a f o r e i g n c i t i z e n o f I n d i a n O r i g i n s e t t l e d o u t s i d e I n d i a ) b y a p p r o p r i a t e a u t h o r i t y . 5 5 . A n a p p l i c a n t f o r a v i s a s h a l l h a v e t o s u b m i t a n a p p l i c a t i o n o n t h e o n - l i n e s y s t e m i n t h e s t a n d a r d v i s a a p p l i c a t i o n f o r m . F o r t h i s p u r p o s e , t h e a p p l i c a n t s m a y l o g o n t o h t t p s : / / i n d i a n v i s a o n l i n e . g o v . i n / v i s a / t v o a . h t m l . 19

- 17. Para 3.3 I M M I G R A T I O N L A W S 20 i. s i n g l e j o u r n e y v i s a ; ii. t r a n s i t v i s a ; iii. o r d i n a r y v i s a ; iv. m u l t i e n t r y l i f e l o n g v i s a ; 5 6 v. 5 7 n o n - d i p l o m a t i c v i s a f o r m u l t i p l e e n t r i e s , o f f i c i a l v i s a f o r s i n g l e e n t r y , v i s i t o r v i s a f o r s i n g l e a s w e l l a s m u l t i p l e e n t r y , a t r a n s i t v i s a f o r s i n g l e e n t r y ; vi. 5 8 a n o f f i c i a l v i s a f o r s i n g l e j o u r n e y o r a s p e c i f i e d n u m b e r o f j o u r n e y s , a s h o r t - t e r m v i s a f o r a s i n g l e j o u r n e y t o I n d i a , a l o n g - t e r m v i s a f o r a s i n g l e j o u r n e y o r a s p e c i f i e d n u m b e r o f j o u r n e y s , a t r a n s i t v i s a f o r o n e d i s t r i c t j o u r n e y , a r e - e n t r y v i s a v a l i d f o r r e - e n t r y i n t o I n d i a e. 5 9 s p e c i f i c a l l y , v a l i d f o r e n t r y i n t o I n d i a o r s h a l l h a v e b e e n s p e c i f i c a l l y e n d o r s e d b y a c o m p e t e n t a u t h o r i t y a s v a l i d f o r e n t r y i n t o I n d i a ; a n d f. s h a l l n o t h a v e b e e n o b t a i n e d b y m i s r e p r e s e n t a t i o n o r f r a u d . 3.2 PERIOD OF VALIDITY OF PASSPORT AND VISA P a s s p o r t s h o u l d h a v e a t l e a s t s i x m o n t h s v a l i d i t y a t t h e t i m e o f m a k i n g a p - p l i c a t i o n f o r g r a n t o f v i s a a n d i t s h o u l d h a v e a t l e a s t t w o b l a n k p a g e s 6 0 f o r s t a m p i n g b y t h e a p p r o p r i a t e o f fi c e r . T h e v a l i d i t y o f a l l v i s a s w i l l c o m m e n c e f r o m t h e d a t e o f i s s u e o f v i s a a n d n o t f r o m t h e d a t e o f e n t r y i n t o I n d i a . 3.3 TYPES OF VISA T h e p r o p e r I n d i a n d i p l o m a t i c c o n s u l a r o r p a s s p o r t a u t h o r i t y i . e . I n d i a n E m b a s s y / H i g h C o m m i s s i o n l o c a t e d i n v a r i o u s c o u n t r i e s i s s u e d i f f e r e n t t y p e s o f v i s a t o f o r e i g n n a t i o n a l s d e p e n d i n g u p o n t h e i r p r o p o s e d a c t i v i t i e s i n I n d i a . B e l o w i s a n i l l u s t r a t i v e l i s t o f v i s a s g r a n t e d i n o r d e r t o e n t e r I n d i a b a s i s t h e p u r p o s e t o v i s i t I n d i a : 5 6 . A p p l i c a b l e o n l y f o r p e r s o n s r e g i s t e r e d a s O C I u n d e r t h e p r o v i s i o n s o f C i t i z e n s h i p A c t , 1 9 5 5 . 5 7 . A p p l i c a b l e o n l y f o r n a t i o n a l o f P a k i s t a n . 5 8 . A p p l i c a b l e o n l y f o r n a t i o n a l o f B a n g l a d e s h . 5 9 . A p p l i c a b l e o n l y f o r n a t i o n a l o f N e p a l . I n c a s e o f a p e r s o n e n t e r i n g I n d i a o v e r t h e T i b e t a n o r B h u t a n e s e f r o n t i e r , i t s h a l l a l s o b e e n d o r s e d b y a p r o p e r I n d i a n D i p l o m a t i c , c o n s u l a r o r p a s s p o r t a u t h o r i t y b y w a y o f a v i s a o r a t r a n s i t v i s a . F u r t h e r , a c i t i z e n o f N e p a l o r B h u t a n m u s t h a v e a v i s a f o r I n d i a i f h e / s h e i s e n t e r i n g I n d i a f r o m C h i n a , M a c a u , H o n g K o n g , P a k i s t a n a n d M a l d i v e s . 6 0 . T h e l a s t t w o o b s e r v a t i o n p a g e s a r e n o t c o n s i d e r e d .

- 19. Para 3.3 I M M I G R A T I O N L A W S 22 Sl. No. Type of Visa Eligibility 8 J o u r n a l i s t V i s a G r a n t e d t o ( a ) a f o r e i g n e r w h o i s a p r o f e s s i o n a l j o u r n a l i s t , p h o t o g r a p h e r , d o c u m e n t a r y fi l m p r o d u c e r o r d i r e c t o r ( o t h e r t h a n o f c o m m e r c i a l fi l m s ) , a r e p r e s e n t a t i v e o f a r a d i o a n d / o r t e l e v i s i o n o r g a n i z a t i o n , t r a v e l w r i t e r / t r a v e l p r o m o t i o n p h o t o g r a p h e r e t c . , ( b ) p r o f e s s i o n a l j o u r n a l i s t w o r k i n g f o r a n a s s o c i a t i o n o r a c o m p a n y e n g a g e d i n t h e p r o d u c t i o n o r b r o a d c a s t o f a u d i o n e w s o r a u d i o v i s u a l n e w s o r c u r r e n t a f f a i r s p r o g r a m m e s t h r o u g h t h e p r i n t m e d i a , e l e c t r o n i c o r a n y o t h e r m o d e o f m a s s c o m m u n i c a t i o n , ( c ) c o r r e s p o n d e n t / c o l u m n i s t / c a r t o o n i s t / e d i t o r / o w n e r o f t h e a s s o c i a t i o n o r c o m p a n y r e f e r r e d i n ( a ) / ( b ) a b o v e . 9 F i l m V i s a G r a n t e d t o a f o r e i g n e r f o r s h o o t i n g o f a f e a t u r e fi l m / r e a l i t y T V s h o w a n d / o r c o m m e r c i a l T V s e r i a l s . 1 0 M i s s i o n a r y V i s a G r a n t e d t o a f o r e i g n e r w h o s e s o l e o b j e c t i v e o f v i s i t i n g I n d i a i s M i s s i o n a r y w o r k n o t i n v o l v i n g p r o s e l y t i z a t i o n . 1 1 E m p l o y - m e n t V i s a G r a n t e d t o a f o r e i g n n a t i o n a l w h o i s a h i g h l y s k i l l e d a n d / o r q u a l i fi e d p r o f e s s i o n a l a n d i s n o t b e g r a n t e d ( i ) f o r j o b s f o r w h i c h q u a l i fi e d I n d i a n s a r e a v a i l a b l e a n d ( ii ) f o r r o u t i n e , o r d i n a r y o r s e c r e t a r i a l / c l e r i c a l j o b s . E m p l o y m e n t v i s a i s a l s o g r a n t e d t o a f o r e i g n n a t i o n a l c o m i n g t o I n d i a f o r e x e c u t i o n o f p r o j e c t s i n t h e p o w e r a n d s t e e l s e c t o r s s u b j e c t t o t h e specified c o n d i t i o n s . 6 5 1 2 B u s i n e s s V i s a G r a n t e d t o a f o r e i g n n a t i o n a l w h o w i s h t o v i s i t I n d i a t o e s t a b l i s h a n i n d u s t r i a l / b u s i n e s s v e n t u r e o r t o e x p l o r e p o s - s i b i l i t i e s t o s e t u p a n i n d u s t r i a l / b u s i n e s s v e n t u r e . B u s i n e s s v i s a i s a l s o g r a n t e d t o f o r e i g n e r s w h o a r e m e m b e r s o f s p o r t s t e a m s . 6 6 The foreign nationals are required to strictly adhere to the purpose of visit declaredwhilesubmittingthevisaapplication.Iftheactivitiesundertakenby the foreigner in India is not in consonance with the visa category, the same may be treated as contravention. For illustration, if a correct visa category for a particular activity is business visa but the individual comes on tourist visa or conference visa etc., the same will amount to contravention. Simi- lar will be the implications where the correct visa category is employment visa (say execution of projects in power sector) but the individual visits on business visa (say monitoring of projects). 6 5 . P r o j e c t v i s a i s n o w m e r g e d w i t h E m p l o y m e n t v i s a . 6 6 . S p o r t s v i s a i s n o w m e r g e d w i t h B u s i n e s s v i s a .

- 20. 23 E M P L O Y M E N T V I S A Para 3.4 H a v i n g d i s c u s s e d t h e b r o a d c a t e g o r i e s o f V i s a g r a n t e d b y t h e G o v e r n m e n t o f I n d i a , l e t u s n o w u n d e r s t a n d t h e r e l e v a n t v i s a c a t e g o r i e s f o r s e c o n d m e n t v i z . , E m p l o y m e n t V i s a a n d B u s i n e s s V i s a i n d e t a i l . 3.4 EMPLOYMENT VISA 3.4.1 Conditions A n E m p l o y m e n t v i s a i s g r a n t e d t o a f o r e i g n e r 6 7 d r a w i n g a g r o s s s a l a r y 6 8 i n e x c e s s o f ` 1 6 . 2 5 6 9 | 7 0 l a k h s p e r a n n u m 7 1 w h o i s a h i g h l y s k i l l e d a n d / o r q u a l i fi e d p r o f e s s i o n a l except f o r j o b s f o r w h i c h q u a l i fi e d I n d i a n s a r e a v a i l a b l e a n d / o r f o r r o u t i n e , o r d i n a r y o r s e c r e t a r i a l / c l e r i c a l j o b s . F u r t h e r , e m p l o y m e n t v i s a i s a l s o g r a n t e d i n f o l l o w i n g c a s e s : a. F o r e i g n s k i l l e d / h i g h l y s k i l l e d n a t i o n a l s c o m i n g t o I n d i a f o r e x e c u t i o n o f p r o j e c t s i n t h e p o w e r a n d s t e e l s e c t o r s b. C o n t r a c t c o n s u l t a n t o n c o n t r a c t f o r w h o m t h e I n d i a n c o m p a n y p a y s a f i x e d 7 2 r e m u n e r a t i o n c. F o r e i g n a r t i s t e s e n g a g e d t o c o n d u c t r e g u l a r p e r f o r m a n c e s f o r t h e d u r a t i o n o f t h e e m p l o y m e n t c o n t r a c t g i v e n b y h o t e l s , c l u b s , o t h e r o r g a n i z a t i o n s d. F o r e i g n n a t i o n a l s w h o a r e c o m i n g t o I n d i a t o t a k e u p e m p l o y m e n t a s c o a c h e s o f n a t i o n a l / s t a t e l e v e l t e a m s o r r e p u t e d s p o r t s c l u b s 6 7 . N o t a c i t i z e n o f P a k i s t a n . 6 8 . S a l a r y a n d a l l o t h e r a l l o w a n c e s i n c a s h a s w e l l a s k i n d l i k e r e n t f r e e a c c o m m o d a t i o n e t c . i n c l u d e d i n s a l a r y f o r t h e p u r p o s e o f c a l c u l a t i n g i n c o m e t a x . F u r t h e r , t h e p e r q u i s i t e s s h o u l d b e q u a n t i fi e d a n d i n d i c a t e d i n t h e e m p l o y m e n t c o n t r a c t . 6 9 . N o t a p p l i c a b l e t o f o l l o w i n g j o b s : a . E t h n i c c o o k s e m p l o y e d b y f o r e i g n M i s s i o n s i n I n d i a ( n o t a p p l i c a b l e t o e t h n i c c o o k s e m p l o y e d i n c o m m e r c i a l v e n t u r e ) , b . L a n g u a g e t e a c h e r s ( o t h e r t h a n E n g l i s h l a n g u a g e t e a c h e r s ) / t r a n s l a t o r s ( t h i s w i l l n o t i n c l u d e t e a c h e r s e m p l o y e d t o t e a c h p a r t i c u l a r s u b j e c t s i n f o r e i g n l a n g u a g e ) , c . S t a f f w o r k i n g f o r t h e c o n c e r n e d E m b a s s y / H i g h C o m m i s s i o n i n I n d i a , d . F o r e i g n e r s , e l i g i b l e f o r ‘ E ’ v i s a f o r h o n o r a r y w o r k w i t h t h e N G O s r e g i s t e r e d i n t h e c o u n t r y w i t h o u t s a l a r y , e . F o r e i g n t e a c h i n g f a c u l t y e m p l o y e d i n t h e S o u t h A s i a n U n i v e r s i t y a n d t h e N a l a n d a U n i v e r s i t y , a n d f . C i r c u s a r t i s t s . 7 0 . ` 9 . 1 0 l a k h s p e r a n n u m f o r p e o p l e e n g a g e d a s a s s i s t a n t p r o f e s s o r a n d a b o v e b y t h e C e n t r a l H i g h e r E d u c a t i o n a l I n s t i t u t i o n s v i z . , I I T s , C U s , N I T s , I I M s a n d I I S E R s or B a n g l a d e s h i n a t i o n a l s m a r r i e d t o I n d i a n n a t i o n a l s b u t n o t e l i g i b l e f o r r e g i s t r a t i o n a s O C I c a r d h o l d e r . 7 1 . F o r v i s a p e r i o d o f l e s s t h a n o n e y e a r t h e m i n i m u m s a l a r y r e q u i r e m e n t t o b e w o r k e d o u t o n p r o - r a t a b a s i s . 7 2 . M a y n o t b e i n t h e f o r m o f a m o n t h l y s a l a r y .

- 21. Para 3.4 I M M I G R A T I O N L A W S 24 e. F o r e i g n s p o r t s m e n 7 3 w h o a r e g i v e n c o n t r a c t f o r a s p e c i f i e d p e r i o d b y t h e I n d i a n C l u b s / o r g a n i z a t i o n s f. S e l f - e m p l o y e d f o r e i g n n a t i o n a l s c o m i n g t o I n d i a f o r p r o v i d i n g e n g i - n e e r i n g , m e d i c a l , a c c o u n t i n g , l e g a l o r s u c h o t h e r h i g h l y s k i l l e d s e r v i c e s i n t h e i r c a p a c i t y a s i n d e p e n d e n t c o n s u l t a n t s p r o v i d e d t h e p r o v i s i o n o f s u c h s e r v i c e s b y f o r e i g n n a t i o n a l s i s p e r m i t t e d u n d e r l a w g. F o r e i g n l a n g u a g e t e a c h e r s / i n t e r p r e t e r s h. F o r e i g n s p e c i a l i s t c h e f s i. F o r e i g n c i r c u s a r t i s t s j. F o r e i g n e n g i n e e r s / t e c h n i c i a n s c o m i n g t o I n d i a f o r i n s t a l l a t i o n a n d c o m m i s s i o n i n g o f e q u i p m e n t / m a c h i n e s / t o o l s i n t e r m s o f t h e c o n t r a c t f o r s u p p l y o f s u c h e q u i p m e n t / m a c h i n e s / t o o l s k. F o r e i g n n a t i o n a l s d e p u t e d f o r p r o v i d i n g t e c h n i c a l s u p p o r t / s e r v i c e s , t r a n s f e r o f k n o w - h o w / s e r v i c e s f o r w h i c h t h e I n d i a n c o m p a n y p a y s f e e s / r o y a l t y t o t h e f o r e i g n c o m p a n y l. F o r e i g n j o u r n a l i s t s , w h o i n t e n d t o t r a v e l t o I n d i a t o w o r k i n I n d i a n m e d i a o r g a n i z a t i o n s m. E m p l o y e e s / m a n a g e r s c o m i n g t o I n d i a f o r n o n - j o u r n a l i s t i c a c t i v i t i e s w i t h i n m e d i a o r g a n i z a t i o n s T h e e m p l o y m e n t v i s a m u s t b e i s s u e d f r o m t h e c o u n t r y o f o r i g i n o r f r o m t h e c o u n t r y o f d o m i c i l e o f t h e f o r e i g n e r p r o v i d e d t h e p e r i o d o f p e r m a n e n t r e s i d e n c e o f t h e a p p l i c a n t i n t h a t p a r t i c u l a r c o u n t r y i s m o r e t h a n 2 y e a r s . 7 4 T h e e m p l o y m e n t v i s a i s g r a n t e d f o r a s p e c i fi c d u r a t i o n d e p e n d i n g u p o n t h e n a t u r e o f a c t i v i t i e s p r o p o s e d t o b e u n d e r t a k e n b y t h e f o r e i g n e r i n I n d i a . T h e v i s a 7 5 d u r a t i o n v i s - à - v i s n a t u r e o f a c t i v i t i e s t o b e u n d e r t a k e n b y t h e f o r e i g n n a t i o n a l 7 6 i s m e n t i o n e d a s u n d e r : 7 3 . F o r e i g n n a t i o n a l s w h o a r e e n g a g e d i n c o m m e r c i a l s p o r t s e v e n t s i n I n d i a o n c o n t r a c t ( i n c l u d i n g c o a c h e s ) a r e n o t i n c l u d e d . 7 4 . A n s w e r t o q u e s t i o n 5 , F A Q s R e l a t i n g t o w o r k r e l a t e d V I S A s i s s u e d b y I n d i a . T h e F A Q s c a n b e a c c e s s e d a t h t t p s : / / w w w . m h a . g o v . i n / s i t e s / d e f a u l t / fi l e s / w o r k _ v i s a _ f a q . p d f . 7 5 . W i t h m u l t i p l e e n t r y f a c i l i t y . 7 6 . O t h e r t h a n J a p a n e s e n a t i o n a l . T h e v i s a ( w i t h m u l t i p l e e n t r i e s ) d u r a t i o n v i s - à - v i s n a t u r e o f a c t i v i t i e s t o b e u n d e r t a k e n b y t h e J a p a n e s e n a t i o n a l i s m e n t i o n e d a s u n d e r : Nature of activities Duration J a p a n e s e t e c h n i c i a n o r e x p e r t c o m i n g t o I n d i a i n p u r s u a n c e o f a b i l a t e r a l a g r e e m e n t b e t w e e n t h e G o v e r n m e n t o f I n d i a a n d G o v e r n m e n t o f J a p a n , o r i n p u r s u a n c e o f a r r a n g e m e n t s b e t w e e n n o n - g o v e r n m e n t a l o r g a n i s a t i o n s a p p r o v e d b y t h e G o v e r n m e n t o f I n d i a 5 y e a r s or d u r a t i o n s t a t e d i n a g r e e m e n t , w h i c h e v e r i s l e s s H i g h l y s k i l l e d f o r e i g n p e r s o n n e l b e i n g e m p l o y e d i n t h e I T s o f t w a r e a n d I T e n a b l e d s e c t o r s 3 y e a r s A n y a c t i v i t y o t h e r t h a n a b o v e 3 y e a r s

- 22. 25 E M P L O Y M E N T V I S A Para 3.4 Nature of activities Duration (lower of the two) A f o r e i g n t e c h n i c i a n / e x p e r t c o m i n g t o I n d i a i n p u r s u a n c e o f a b i l a t e r a l a g r e e m e n t b e t w e e n t h e G o v e r n m e n t o f I n d i a a n d t h e f o r e i g n g o v e r n m e n t , o r i n p u r s u a n c e o f a c o l l a b o r a t i o n a g r e e m e n t t h a t h a s b e e n a p p r o v e d b y t h e G o v e r n m e n t o f I n d i a 5 y e a r s or d u r a t i o n o f a g r e e m e n t H i g h l y s k i l l e d f o r e i g n p e r s o n n e l b e i n g e m p l o y e d i n t h e I T s o f t w a r e a n d I T e n a b l e d s e c t o r s 3 y e a r s or t e r m o f a s s i g n m e n t A n y a c t i v i t y o t h e r t h a n a b o v e 2 y e a r s or t e r m o f a s s i g n m e n t 3.4.2 Documents/information T h e f o l l o w i n g d o c u m e n t s / i n f o r m a t i o n i s r e q u i r e d w h i l e a p p l y i n g f o r e m - p l o y m e n t v i s a : a. O r i g i n a l p a s s p o r t b. P r o o f o f n a m e c h a n g e , i f a n y c. O n e 7 7 p h o t o g r a p h , t o b e p a s t e d o n t h e a p p l i c a t i o n d. C o p y o f t h e p r o o f o f r e s i d e n c e / a d d r e s s t h a t m a t c h e s w i t h t h e p r e s e n t a d d r e s s o n t h e v i s a a p p l i c a t i o n e. A p p o i n t m e n t l e t t e r f r o m t h e e m p l o y e r a l o n g w i t h s a l a r y d e t a i l s f. C o p y o f d u l y s i g n e d 7 8 e m p l o y m e n t c o n t r a c t g. C o p y o f a p p l i c a n t ’ s r e s u m e a l o n g w i t h a c o p y o f e d u c a t i o n a l q u a l i - f i c a t i o n s a n d p r o f e s s i o n a l e x p e r t i s e h. P r o o f o f r e g i s t r a t i o n / i n c o r p o r a t i o n o f e m p l o y e r i n I n d i a i. T a x e l i g i b i l i t y l e t t e r c e r t i f y i n g t h a t t h e I n d i a n e m p l o y e r s h o u l d b e l i a b l e / t a k e r e s p o n s i b i l i t y f o r p a y i n g t a x e s o n b e h a l f o f t h e a p p l i c a n t j. P r o j e c t r e p o r t o n t h e I n d i a n e m p l o y e r ’ s l e t t e r h e a d d u l y s i g n e d b y t h e a u t h o r i s e d s i g n a t o r y o f t h e c o m p a n y 7 7 . C i t i z e n o f P a k i s t a n i s r e q u i r e d t o s u b m i t f o u r p h o t o g r a p h s . 7 8 . B y e m p l o y e r a s w e l l a s e m p l o y e e .

- 24. 27 E M P L O Y M E N T V I S A Para 3.4 j. L e t t e r o f u n d e r t a k i n g ( T D S , g e n e r a l e t c . ) f r o m c o m p a n y s i g n e d b y I n d i a n h o s t o r a u t h o r i z e d s i g n a t o r y w i t h n a m e a n d c o n t a c t n u m b e r k. F o r m 1 6 / i n c o m e t a x r e t u r n i n c a s e t h e a p p l i c a n t i s r e s i d i n g i n I n d i a f o r m o r e t h a n 1 y e a r o r p r o o f o f T D S w i t h b a n k c h a l l a n f o r t h e c u r - r e n t f i n a n c i a l y e a r l. R e g i s t r a t i o n c e r t i f i c a t e / r e s i d e n t i a l p e r m i t T h e v i s a m a y b e e x t e n d e d b y t h e a p p r o p r i a t e r e g i s t r a t i o n o f fi c e r , u p t o a t o t a l p e r i o d o f 5 y e a r s f r o m t h e d a t e o f i s s u e o f t h e i n i t i a l e m p l o y m e n t v i s a , o n a n a n n u a l b a s i s s u b j e c t t o t h e c o n d i t i o n t h a t m a x i m u m d u r a t i o n o f v i s a ( i n c l u d i n g i n i t i a l t e r m ) d o e s n o t e x c e e d 1 0 y e a r s . T h e e x t e n s i o n s h a l l b e g r a n t e d s u b j e c t t o g o o d c o n d u c t , p r o d u c t i o n o f n e c e s s a r y d o c u m e n t s i n s u p p o r t o f c o n t i n u e d e m p l o y m e n t , t a x c o m p l i a n c e s a n d n o a d v e r s e s e c u r i t y i n p u t s a b o u t t h e f o r e i g n e r . 3.4.4 Change of Employer A n e m p l o y m e n t v i s a h o l d e r c a n c h a n g e t h e e m p l o y e r o n c e d u r i n g t h e t e n u r e o f 5 y e a r o f t h e o r i g i n a l e m p l o y m e n t v i s a u p o n a p p r o v a l o f M H A . O n r e c e i p t o f t h e a p p l i c a t i o n r e g a r d i n g t h e c h a n g e o f e m p l o y e r , M H A m a y , o n t h e b a s i s o f t h e m e r i t s o f e a c h c a s e a l l o w t h e c h a n g e o f e m p l o y e r . T h e f o l l o w i n g c r i t e r i a a r e c o n s i d e r e d b y M H A w h i l e c o n s i d e r i n g t h e a p p l i c a t i o n : a. T h e a p p l i c a n t i s e m p l o y e d , a t t h e s e n i o r l e v e l e . g . m a n a g e r i a l o r a s e n i o r e x e c u t i v e p o s i t i o n a n d / o r , a t a s k i l l e d p o s i t i o n e . g . a t e c h n i c a l e x p e r t w i t h i n a n o r g a n i z a t i o n i n I n d i a ; b. T h e c h a n g e o f e m p l o y m e n t i s b e t w e e n a r e g i s t e r e d h o l d i n g c o m p a n y , J o i n t V e n t u r e s C o n s o r t i u m s a n d i t s s u b s i d i a r i e s a n d v i c e v e r s a o r b e t w e e n s u b s i d i a r i e s o f a r e g i s t e r e d h o l d i n g c o m p a n y , J o i n t V e n t u r e s C o n s o r t i u m s ; a n d c. T h e c o m p a n y t h a t o r i g i n a l l y e m p l o y e d t h e a p p l i c a n t i s s u e s a n o o b j e c t i o n l e t t e r t o w a r d s t h e c h a n g e . In cases not falling within above, the foreigner has to leave India and ap- ply for a fresh employment visa where the foreigner wants to change the employment to another company/organisation. 3.4.5 Conversion E m p l o y m e n t V i s a c a n n o t b e c o n v e r t e d t o a n y o t h e r k i n d o f v i s a d u r i n g t h e s t a y o f t h e f o r e i g n e r i n I n d i a e x c e p t i n t h e f o l l o w i n g c i r c u m s t a n c e s a n d w i t h t h e p r i o r a p p r o v a l o f t h e M H A :

- 25. Para 3.5 I M M I G R A T I O N L A W S 28 a. E m p l o y m e n t v i s a c a n b e c o n v e r t e d t o ‘ X ’ ( E n t r y ) V i s a i f a f o r e i g n e r w h o h a s c o m e t o I n d i a o n e m p l o y m e n t v i s a m a r r i e s a n I n d i a n n a t i o n a l d u r i n g t h e v a l i d i t y o f h i s / h e r v i s a a n d d o e s n o t i n t e n d t o c o n t i n u e o n e m p l o y m e n t v i s a . S u c h c o n v e r s i o n w o u l d b e c o n s i d e r e d s u b j e c t t o f u l f i l m e n t o f f o l l o w i n g c o n d i t i o n s : i. s u b m i s s i o n o f a c o p y o f r e g i s t e r e d m a r r i a g e c e r t i f i c a t e , a n d ii. r e p o r t f r o m t h e F R R O / F R O c o n c e r n e d a b o u t t h e i r m a r i t a l s t a t u s w h i c h w i l l i n t e r a l i a i n c l u d e h i s / h e r a n t e c e d e n t s , c o n - f i r m a t i o n a b o u t t h e i r l i v i n g t o g e t h e r a n d s e c u r i t y c l e a r a n c e b. E m p l o y m e n t v i s a i n c a s e o f P I O , w h o w e r e o t h e r w i s e e n t i t l e d f o r ‘ X ’ ( E n t r y ) V i s a b u t h a v e e n t e r e d i n t o I n d i a o n E m p l o y m e n t v i s a , c a n a l s o b e c o n v e r t e d t o ‘ X ’ V i s a c. E m p l o y m e n t v i s a o f t h e f o r e i g n e r s w h o f a l l i l l a f t e r t h e i r e n t r y i n t o I n d i a r e n d e r i n g t h e m u n f i t t o t r a v e l a n d r e q u i r e s p e c i a l i z e d m e d i c a l t r e a t m e n t c a n b e c o n v e r t e d t o m e d i c a l v i s a i f t h e y a r e e l i g i b l e f o r g r a n t o f m e d i c a l v i s a a n d m e d i c a l c e r t i f i c a t e i s o b t a i n e d f r o m g o v - e r n m e n t / g o v e r n m e n t - r e c o g n i z e d h o s p i t a l s . I n s u c h a c a s e , ‘ X ’ v i s a o f f a m i l y m e m b e r s / a t t e n d a n t a c c o m p a n y i n g t h e f o r e i g n e r ( w h o s e ‘ E m p l o y m e n t ’ v i s a i s c o n v e r t e d i n t o ‘ M e d i c a l V i s a ’ ) c a n a l s o b e c o n - v e r t e d i n t o m e d i c a l v i s a o f t h e f o r e i g n e r . 8 1 3.5. BUSINESS VISA 3.5.1 Conditions A b u s i n e s s v i s a i s g r a n t e d t o f o r e i g n e r s w h o h a v e e x p e r t i s e i n t h e a r e a o f i n t e n d e d b u s i n e s s a n d i s a p e r s o n o f s o u n d fi n a n c i a l s t a n d i n g . 8 2 T h e s a i d v i s a i s g r a n t e d f o r f o l l o w i n g a c t i v i t i e s ( o t h e r t h a n b u s i n e s s o f m o n e y l e n d i n g o r f o r r u n n i n g a p e t t y b u s i n e s s o r p e t t y t r a d e o r f u l l - t i m e e m p l o y m e n t ) i n I n d i a : a. E s t a b l i s h a n i n d u s t r i a l / b u s i n e s s v e n t u r e 8 3 o r t o e x p l o r e p o s s i b i l i t i e s t o s e t u p a n i n d u s t r i a l / b u s i n e s s v e n t u r e 8 4 , i n I n d i a 8 1 . O n c o n v e r s i o n o f E m p l o y m e n t v i s a i n t o ‘ X ’ v i s a / M e d i c a l v i s a / ‘ M e d X ’ v i s a , t h e f o l l o w i n g e n d o r s e m e n t s h a l l b e m a d e o n t h e P a s s p o r t / R e s i d e n t i a l P e r m i t - ‘ Employment/Business not permitted’ . 8 2 . S u f fi c i e n t p r o o f o f t h e fi n a n c i a l s t a n d i n g a n d e x p e r t i s e i n t h e fi e l d o f i n t e n d e d b u s i n e s s i s c h e c k e d t h o r o u g h l y w h i l e g r a n t i n g t h e v i s a . 8 3 . o t h e r t h a n p r o p r i e t o r s h i p fi r m s a n d / o r p a r t n e r s h i p fi r m s . 8 4 . ibid .

- 28. Description This book provides a comprehensive commentary to understand comply with the taxation and regulatory aspect of the cross-border movement of employees, that results in secondment. As with any cross-border arrangement, multiple complex laws are involved, this book serves as a primer to understand these complexities and related compliances. The discussion in this book starts with determining who is the employer of the expatriate, which is important to identify the correct laws to be complied with. This book aims at providing the reader, an insight into implications that typically arise in secondment arrangement(s), under various Indian laws in the hands of the expatriate company, such as: u Expatriate n Immigration Laws n Personal Income Tax n Custom Baggage Rules u Company n Social Security Laws n Exchange Control Laws n Corporate Income Tax n Transfer Pricing n Goods Services Tax n Corporate Law Rs. 995 Author : Ashish Karundia Edition : 2nd Edition ISBN No. : 9789390831418 Date of Publication : May 2021 Taxation of Expatriate Employees Regulatory Aspects ORDER NOW