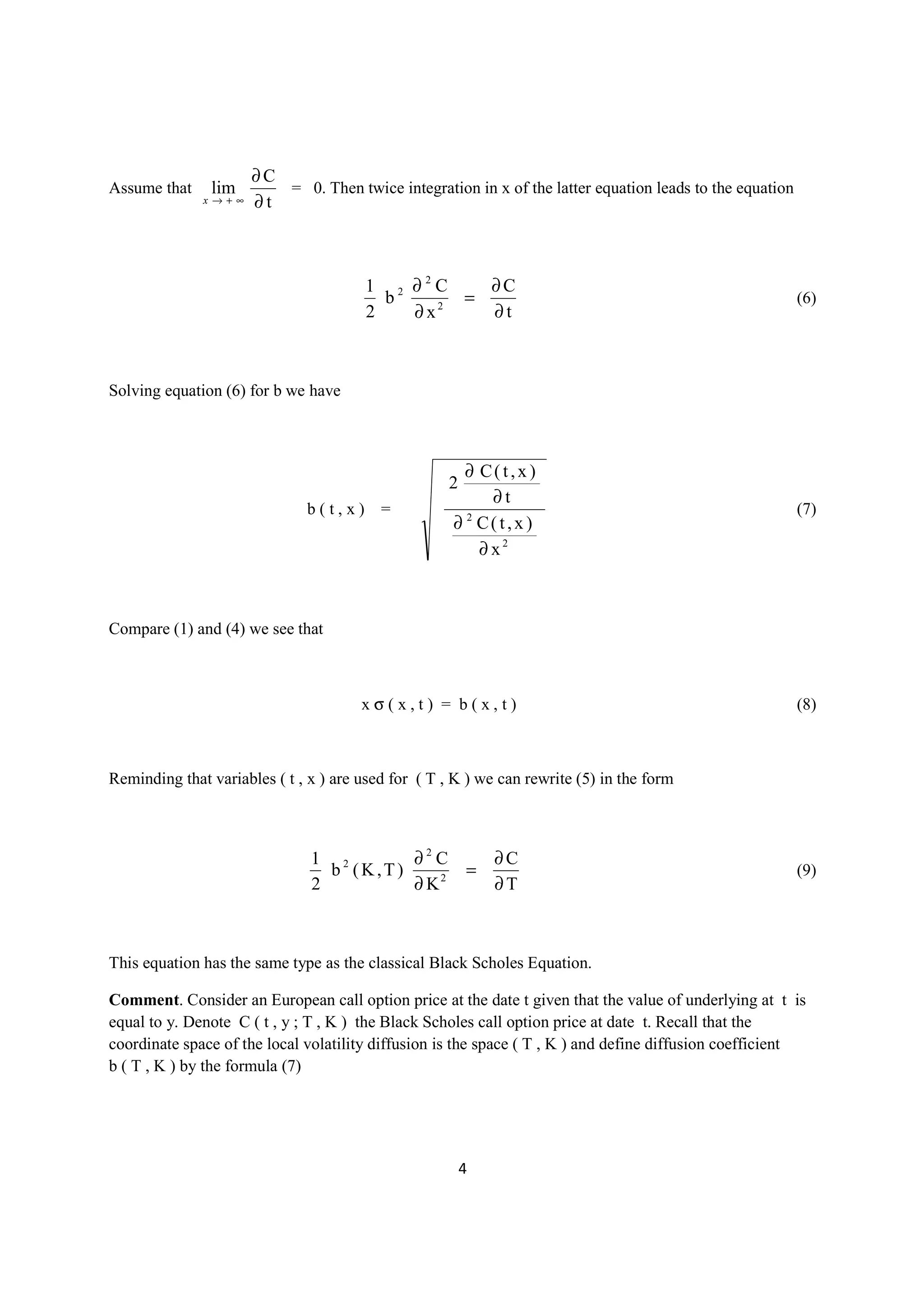

This document provides a summary and critique of the local volatility model. It begins by briefly recalling the construction of the local volatility concept, which aims to find an implied volatility function that matches option prices. However, the document argues that the local volatility model makes an error by replacing the real stock process with an auxiliary process, as they are defined on different coordinate spaces. While the goal of eliminating discrepancies between real and implied volatility is reasonable, the implementation of the local volatility concept ignores important initial conditions. Overall, the document presents both the theoretical basis of local volatility and a critical viewpoint of its mathematical derivation.

![A Supplement to Remark on Local Volatility.

Key words: derivatives pricing, local volatility, call option, dynamic hedging.

Abstract. The concept of the Local Volatility was developed in [1-3]. Later this concept was broadly

generalized and extends in particular to cover stochastic local volatility phenomena. A number of

companies offer their products which call for more accurate forecast of options pricing and one can check

that it is a quite significant business in financial world. In this paper we briefly outlined a critical point of

view on mathematical basics of the construction of the Local Volatility in [4]. Here we present the Local

Volatility concept in greater details.

1](https://image.slidesharecdn.com/supplementtolocalvoatility-120922123333-phpapp02/75/Supplement-to-local-voatility-1-2048.jpg)

![Let us briefly recall a construction of the local volatility concept. The starting point of the concept

is the fact that estimates of the volatility of the underlying security of an option demonstrates its

dependence on option strike price as well as time to the option expiration. One can consider the inverse

problem. Given option price to find a volatility function of the underlying security that correspond to the

Black Scholes ( BS ) option pricing theory. This estimate is called implied volatility and it can be found

as far as the BS price is an increasing function of volatility. Thus, the implied volatility estimate makes

sense regardless whether BS pricing is the correct price. The implied volatility lead to replacement

security volatility σ ( t ) in the BS risk – neutral security model

dS(t) = r(t)S(t)dt + σ(t)S(t)dw(t) (1)

on a nonlinear function σ ( t , S ) for the local volatility model

dS r ( t )

= r ( t ) d t + σ ( t , S r ( t )) d w ( t ) (1′)

Sr (t)

Function σ ( t , S ) is known as local volatility surface, also called the “volatility smile”. It depends on

time and therefore it primarily changes shape from day to day. For a fixed option’s expiration date T,

implied volatility depends on a strike price. The implied volatility increases for decreasing strike. On the

other hand for a fixed strike price implied volatility shows its dependence on time to maturity. We

discussed in details the theoretical failing of the BS option pricing in [5]. While BS drawbacks are

sufficient to raise doubts regarding local volatility our primary attention is the mathematical background

of the local volatility derivation.

Following [1] let us recall the construction of the derivation of the volatility surface σ ( t , S ). For

illustration we consider the case when risk-free interest rate r = 0. Introduce the probability density

f ( T , x ) = f ( t , y ; T , x ) of the solution of the equation

d S( t )

= σ ( t , S ( t )) d w ( t ) (1′′)

S( t )

In finance the only linear case σ ( t , S ) = σ ( t , S ) is admissible otherwise return on 2 stocks will not be

equal to the return on one stock and this does not make any sense. Then the Black Scholes call option

price C ( T , K ) = C ( t , y ; T , K ) is defined as

2](https://image.slidesharecdn.com/supplementtolocalvoatility-120922123333-phpapp02/75/Supplement-to-local-voatility-2-2048.jpg)

![Here µ is a constant expected real return and two random processes S r ( t ) , S ( t ) are defined on initial

probability space { Ω , F , P } that in financial applications is referred to as the real world. These two

processes have equal diffusion coefficients and therefore the measures associated with these processes are

absolutely continuous. This fact gives a possibility to establish connection between real and neutral

worlds by assuming that the real process S ( t ) is defined on the other probability space { Ω , F , Q }

which usually called risk neutral world. Measure Q is chosen such that the finite distributions of the

process S ( t ) with respect to Q coincides with the correspondent distributions of the process S r ( t ) with

respect to measure P. Note that this interpretation does not make sense as far as the stock price S ( t ) is

initially were defined on the real world { Ω , F , P } regardless whether options are existed or not.

Therefore, the risk neutral world leads us to a contradiction between financial sense of a stock stochastic

model and the heuristic connection between virtual process S r ( t ) that was used by Black and Scholes

for their derivatives pricing concept. Actually we do not need to use risk neutral world. More correctly is

to say that the real underlying of the BS pricing is the process S r ( t ) which replaces the real stock S ( t ).

Black and Scholes pricing is also closely related to arbitrage free concept. The arbitrage free

concept is based on assumption that the ‘fair’ or ’perfect’ derivatives price at the current moment is a

deterministic value. Indeed, in this case the equality of the expected present value, EPV lead us to the

formula (12). Recall that EPV concept is the primary concept of the modern finance theory used to justify

the equality of two arbitrary cash flows. The pricing based on equality of two EPVs is called arbitrage

free pricing. This is why BS pricing has been referred to as arbitrage free.

There exists another approach to determine equality of two cash flows. It is the pathwise equality

of the rates of return. This concept admits equality of the rates of return for each scenario and can be

shortly outlined as following. We call two investments are equal on [ 0 , T ] if their rates of return are

equal for each scenario ω ∈ Ω for any t ∈ [ 0 , T ]. Applying this principle for pricing of a European call

option we can write the equation

S( T; t , y ) max { S ( T ; t , y ) − K , 0 }

χ{S(T;t,y) > K} =

y C( t , y ; T, K )

0 ≤ t ≤ T. This equation suggests equal rate of return on the real stock and its call option for each

scenario over an interval [ t , T ]. On the other hand we suppose that the call option price at t is equal to 0

for any scenario ω ∈ Ω such that S ( T, ω ) ≤ K. This pricing is indeed represents the perfect replication.

The stochastic price C ( t , y ; T , K ; ω ) forms the market of the call option while the market spot price

c ( t , y ; T , K ) at date t of the call option can be modeled by different ways. One way to define spot

price is for example

c(t,y; T,K) = a(t)E{C(t,y ; T,K)|Ft} + q(t)

7](https://image.slidesharecdn.com/supplementtolocalvoatility-120922123333-phpapp02/75/Supplement-to-local-voatility-7-2048.jpg)

![Here F t denotes the minimal σ-algebra generating by the values of the real underlying stock on [ t , T ]

where a ( t ) , q ( t ) are deterministic or F t – measurable functions. In more general scheme one can

assume that spot price c ( t ) = c ( t , y ; T , K ) is F t – measurable function defined by SDE in the

form

t

c(t,y; T,K) = c(0) + ∫

0

a(s)E{C(s,y;T,K)|Fs}ds +

t

+ ∫

0

q(s)E{C(s,y;T,K)|Fs}dw(s)

where parameters of the problem c ( 0 ), a ( s ), q ( s ) have to be found from observations of historical

option prices.

8](https://image.slidesharecdn.com/supplementtolocalvoatility-120922123333-phpapp02/75/Supplement-to-local-voatility-8-2048.jpg)

![11.[104 111]analytical solution for telegraph equation by modified of sumudu ...](https://cdn.slidesharecdn.com/ss_thumbnails/11-104-111analyticalsolutionfortelegraphequationbymodifiedofsumudutransformelzakitransform-120513000219-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)