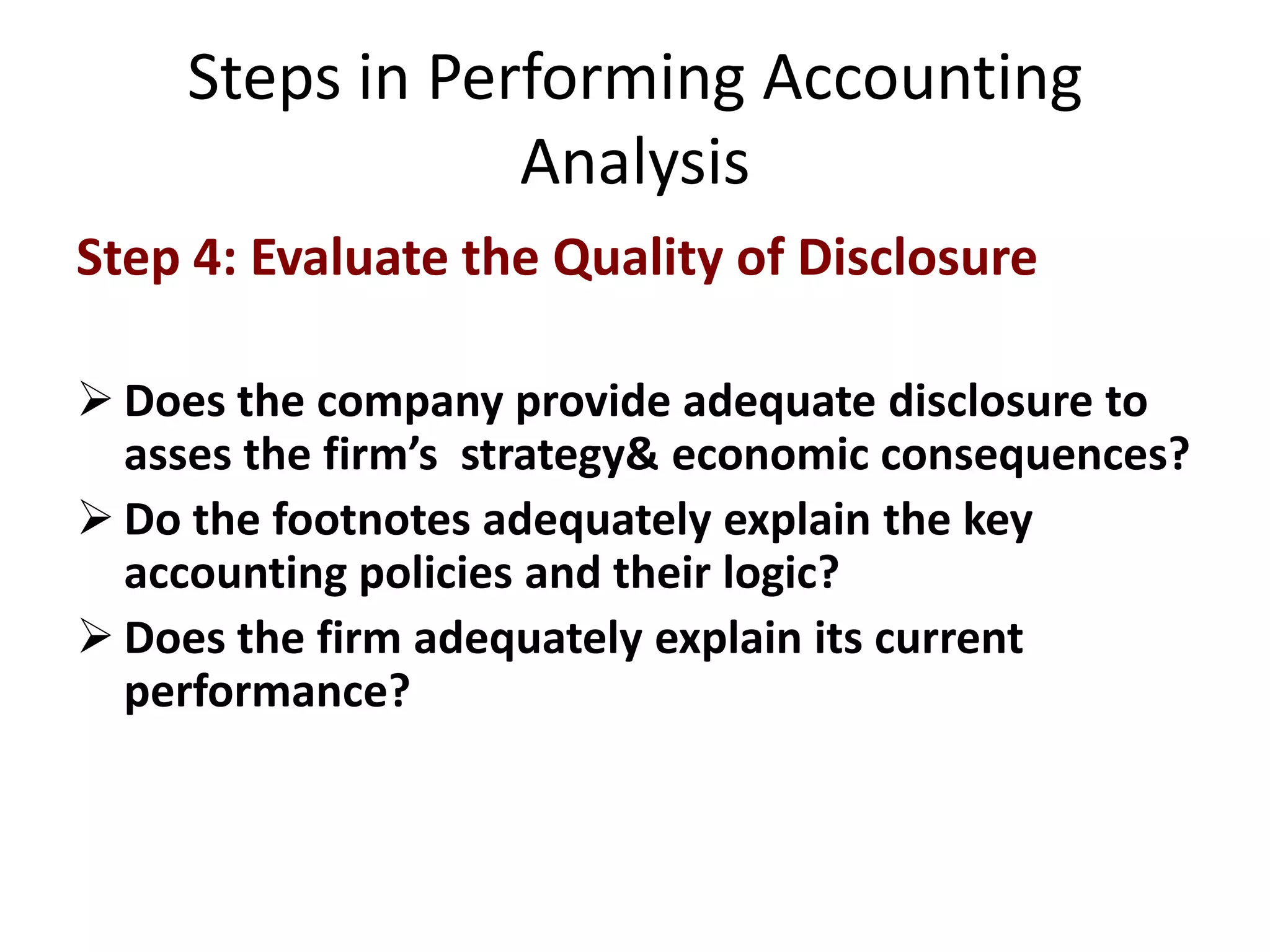

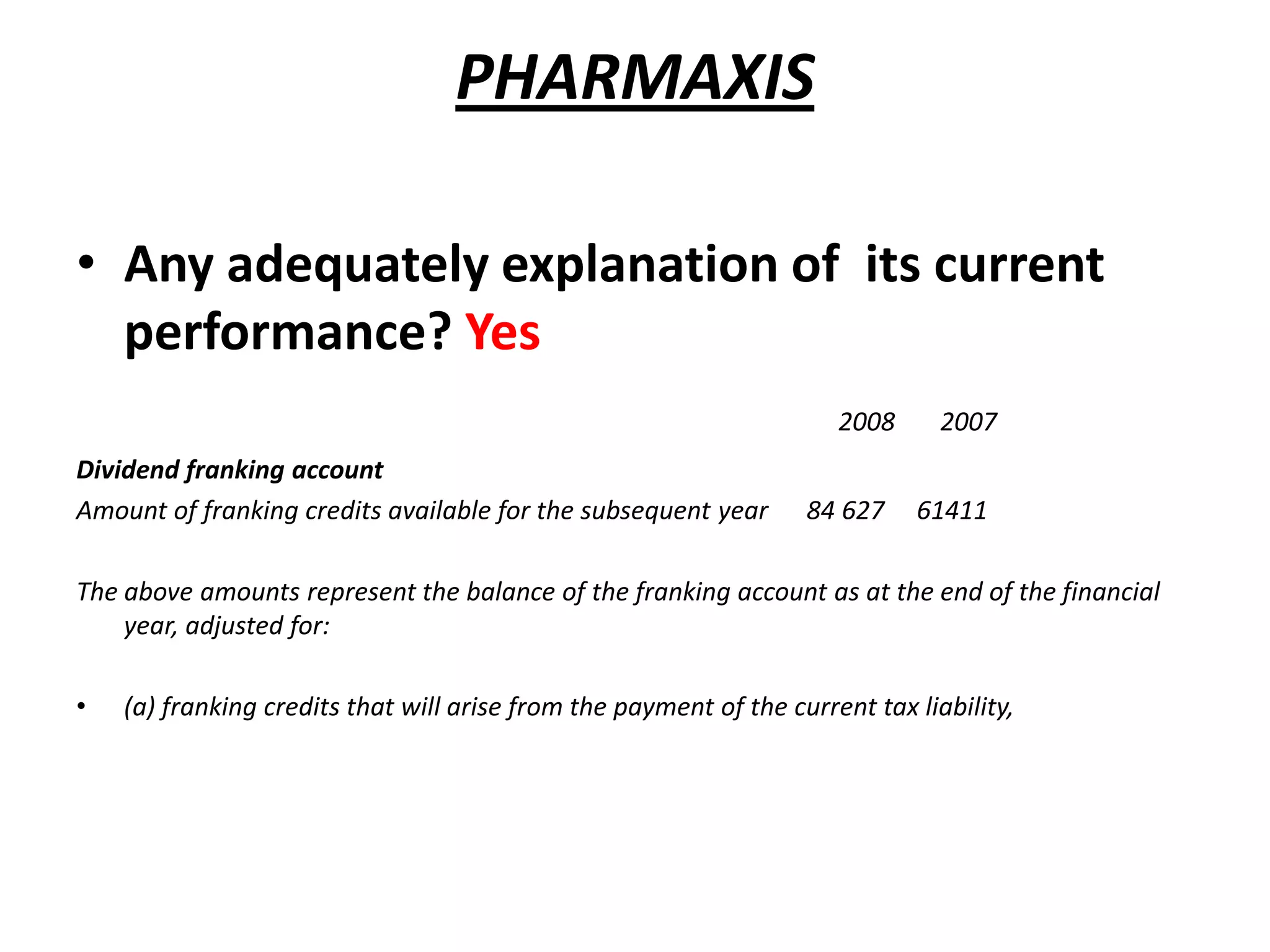

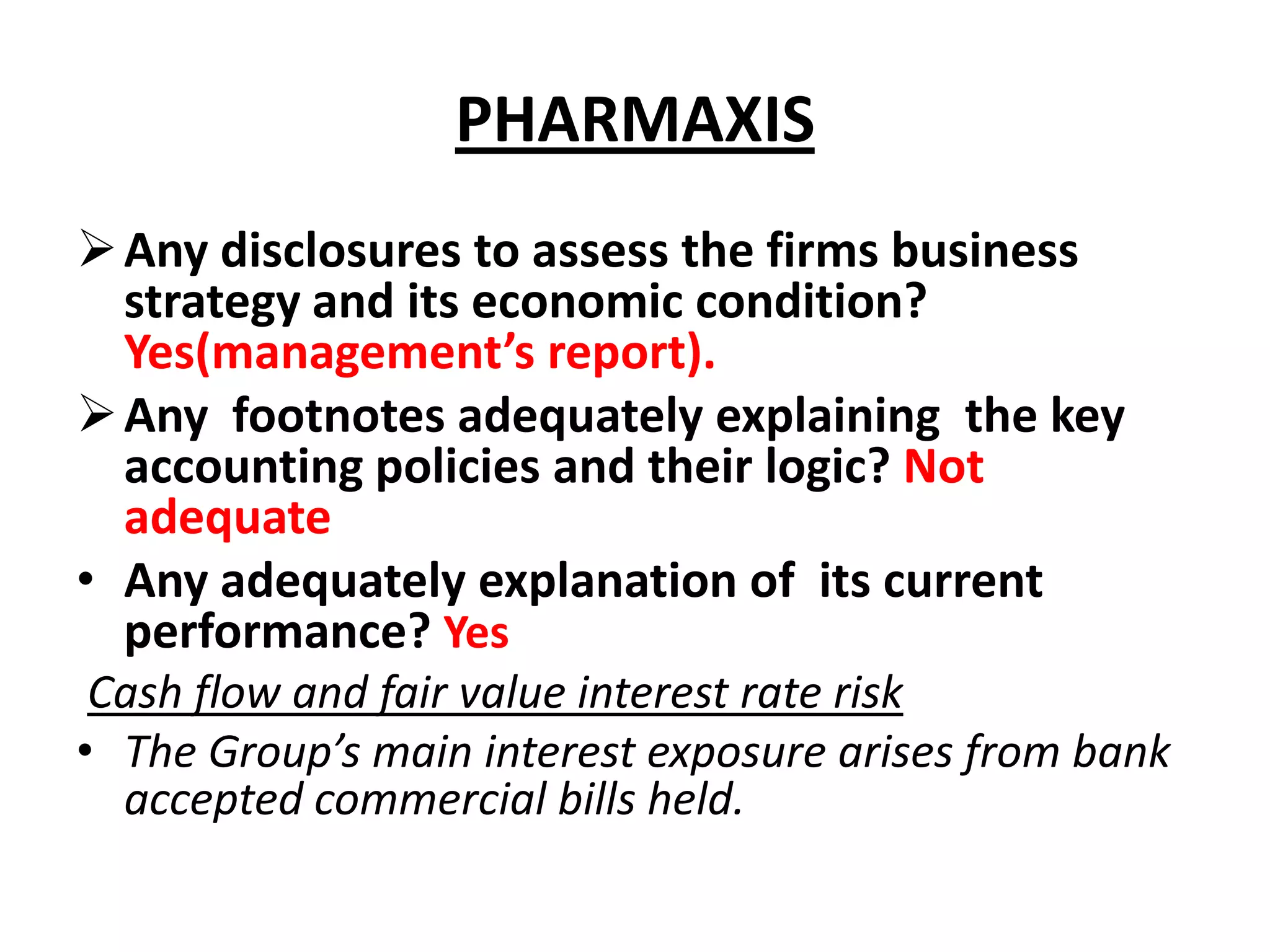

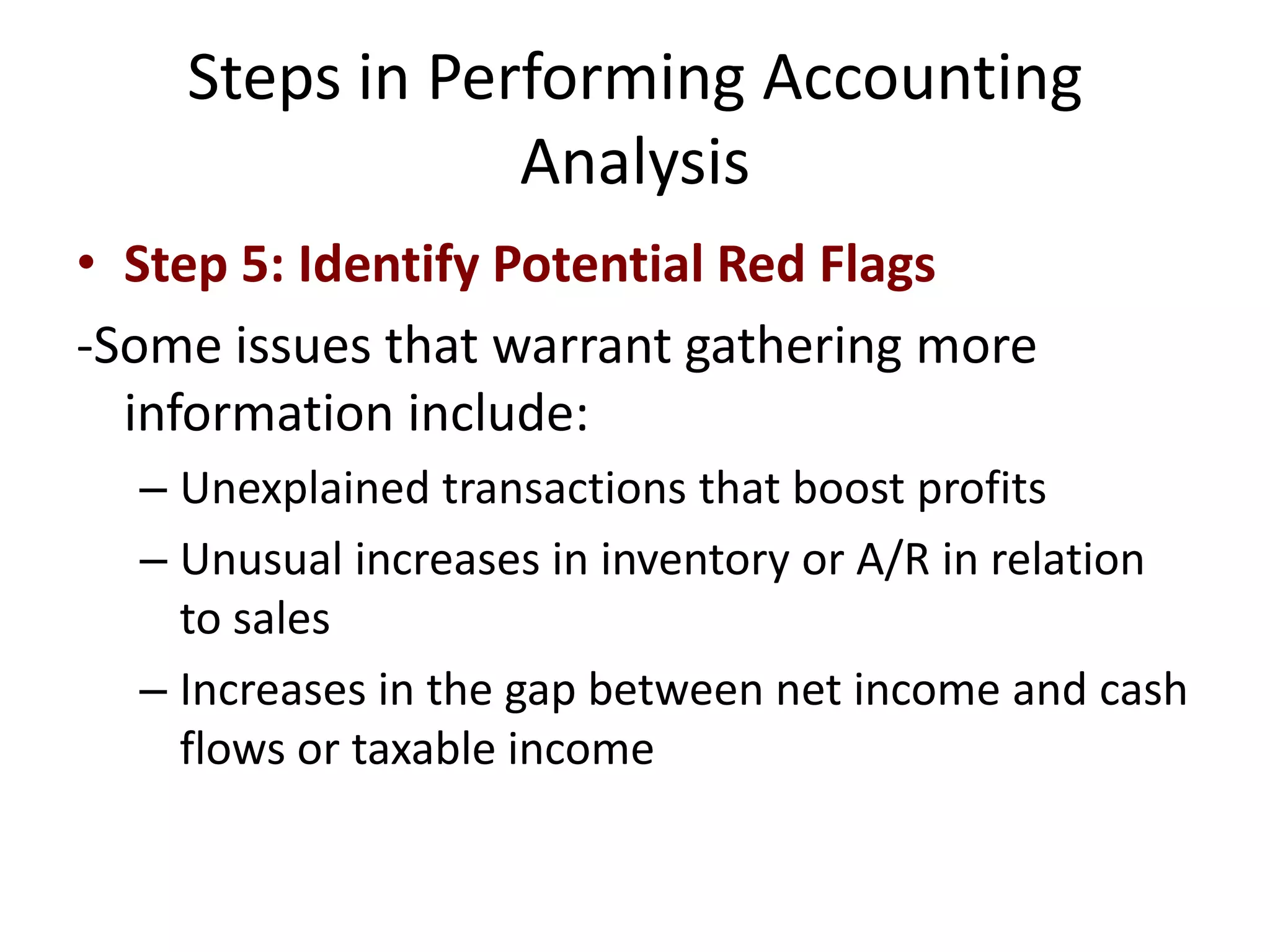

Step 1 through 5 outline the steps in performing accounting analysis. Step 4 evaluates the quality of disclosure by companies, determining if they adequately explain business strategy, accounting policies, and current performance. Step 5 identifies potential red flags in a company's accounting, such as unexplained transactions, unusual increases in inventory/receivables, and gaps between net income and cash flows.