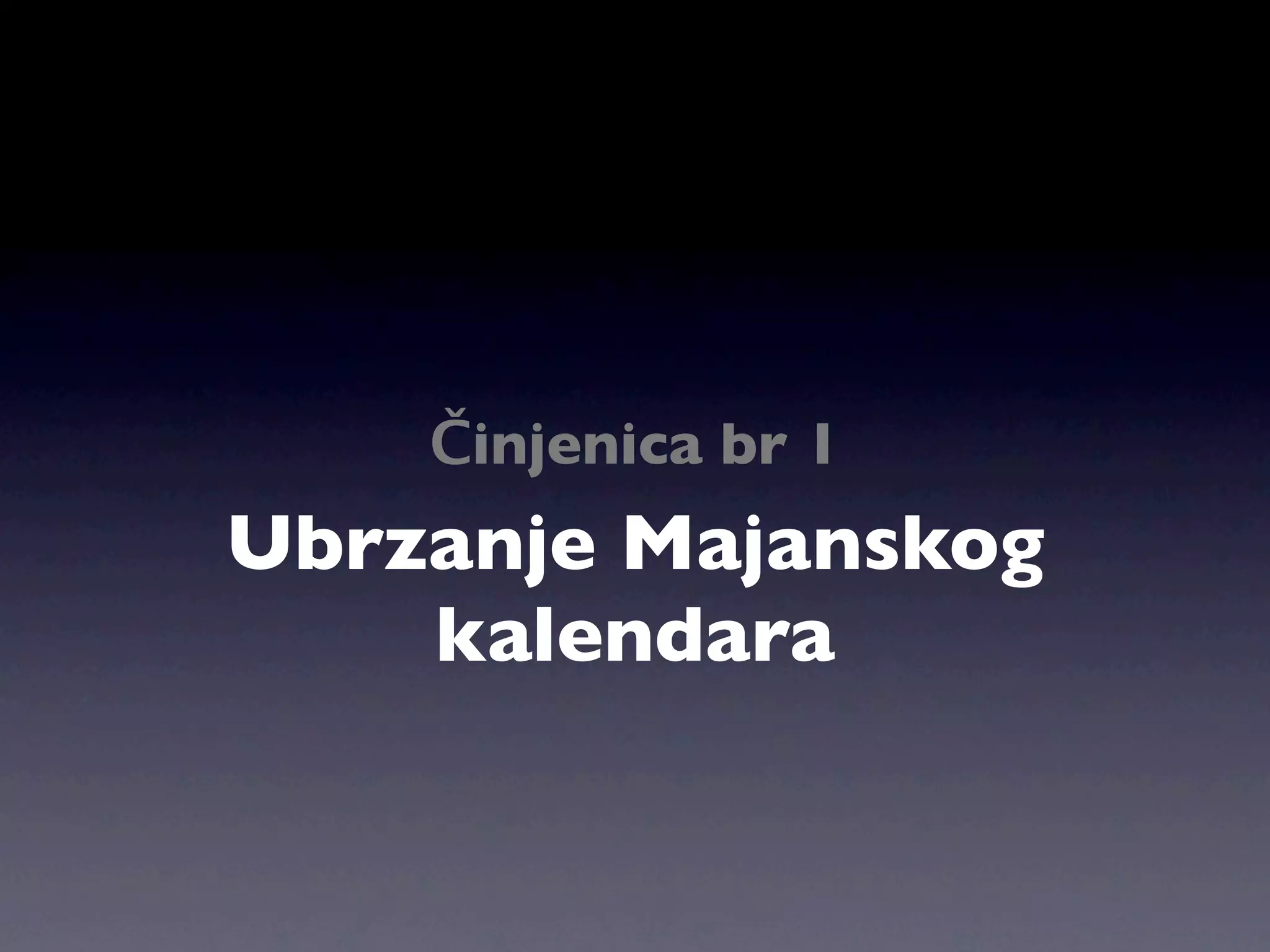

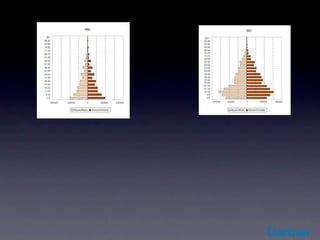

Vremenski period (sastele

Koba): 13* 20=260=Ha’ab-a

Nivo 1 = 256 godina

Trajanje intencije: 19.7 godina

256 god (poč 1756 god)

Industrija počela Planetarni PS

5125 god (poč 3,113 PNE)

Početa prvog pisma Nacionalni podzemni svet

102,575 god Regionalni podzemni svet

Prvi jezik

2,05 Mil g

Plemenski podzemni svet

Prvi ljudi

41.03 Mil

Familijarni podzemni svet

Prvi majmuni

820.602 Mil g Podzemni svet sisara

Prve životinje

16.4 milrd Ćelijski podzemni svet

Veliki

prasak 1 2 3 4 5 6 7

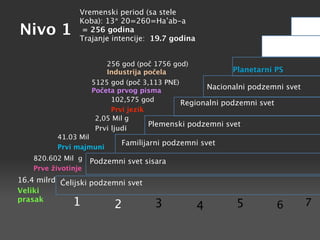

Nivo 0

Vremenski period(sa stele

Koba): 13=Ha’ab-a 12.82 god

= 12.82 godina Početak(5. januar 1999)

Galaktički PS

www počeo

Trajanje intencije: 0.99 godina

256 god (poč 1756 g)

Industrija počela Planetarni PS

5125 god (poč 3,113 PNE)

Prva pisma Nacionalni podzemni svet

102,575 god Regionalni podzemni svet

Prvi jezici

2,05 Mil g

Plemenski podzemni svet

Prvi ljudi

41.03 Mil god

Familijarni podzemni svet

Prvi majmuni

820.602 Mil g Podzemni svet sisara

Prve životinje

16.4 Bil Ćelijski podzemni svet

Veliki prasak

1 2 3 4 5 6 7

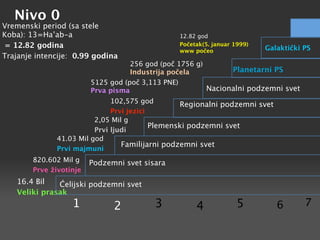

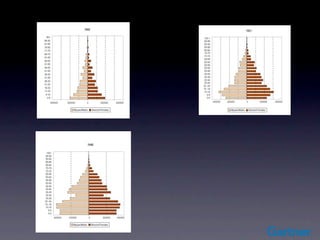

5.

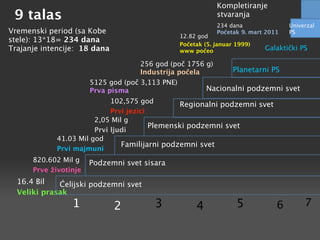

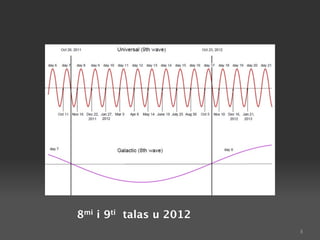

9 talas

234 dana Univerzal

Vremenski period (sa Kobe Početak 9. mart 2011 PS

12.82 god

stele): 13*18= 234 dana Početa k(5. januar 1999)

Trajanje intencije: 18 dana www počeo Galaktički PS

256 god (poč 1756 g)

Industrija počela Planetarni PS

5125 god (poč 3,113 PNE) Nacionalni podzemni

Prva pisma

102,575 god Regionalni podzemni svet

Prvi jezici

2,05 Mil g

Plemenski podzemni svet

Prvi ljudi

41.03 Mil god

Familijarni podzemni svet

Prvi majmuni

820.602 Mil g Podzemni svet sisara

Prve životinje

16.4 Bil Ćelijski podzemni svet

Veliki prasak

1 2 3 4 5 6 7

6.

Kompletiranje

9 talas stvaranja

234 dana Univerzal

Vremenski period (sa Kobe Početak 9. mart 2011 PS

12.82 god

stele): 13*18= 234 dana

Početak (5. januar 1999)

Trajanje intencije: 18 dana www počeo Galaktički PS

256 god (poč 1756 g)

Industrija počela Planetarni PS

5125 god (poč 3,113 PNE)

Prva pisma Nacionalni podzemni svet

102,575 god Regionalni podzemni svet

Prvi jezici

2,05 Mil g

Plemenski podzemni svet

Prvi ljudi

41.03 Mil god

Familijarni podzemni svet

Prvi majmuni

820.602 Mil g Podzemni svet sisara

Prve životinje

16.4 Bil Ćelijski podzemni svet

Veliki prasak

1 2 3 4 5 6 7

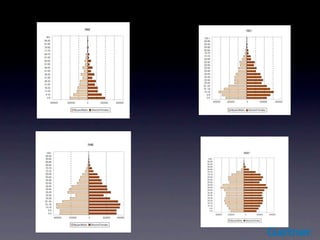

7.

Poslednji nivo

1)9. Mart2011 – 26. Mart 2011

2)27. Mart 2011 – 13. April 2011

3)14. April 2011 – 1. Maj 2011

4)2. Maj 2011 – 19. Maj 2011

5)20. Maj 2011 – 6. Jun 2011

6)7. Jun 2011 – 24. Jun 2011

7)25. Jun 2011 – 12. Jul 2011

8)13. Jul 2011 – 21. Jul 2011

9)22. Jul 2011 – 17. Avgust 2011

10)18. Avgust 2011 – 4. Septembar 2011

11)5. Septembar 2011 – 22. Septembar 2011

12)23. Septembar 2011 – 10. Oktobar 2011

13)11. Oktobar 2011 – 28. Oktobar 2011

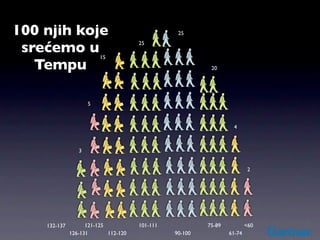

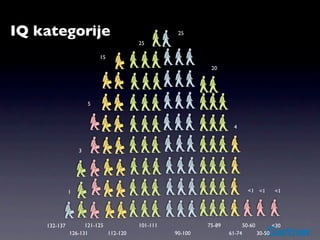

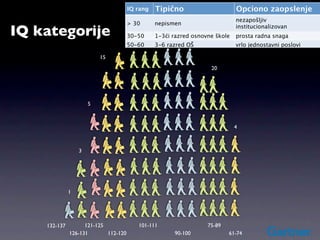

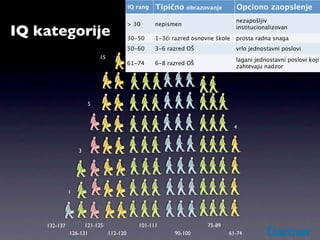

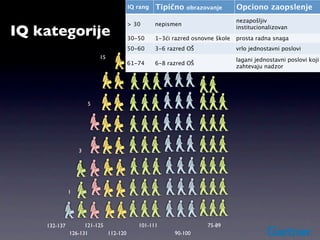

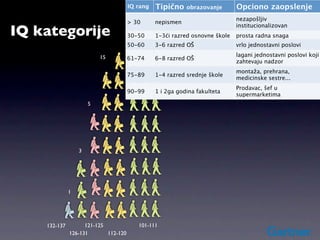

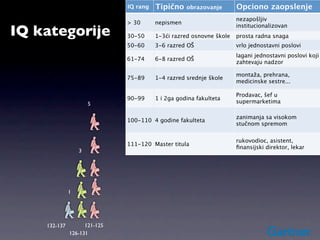

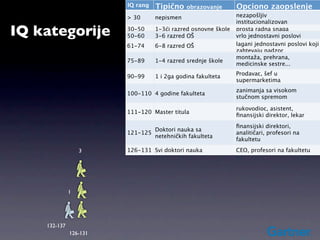

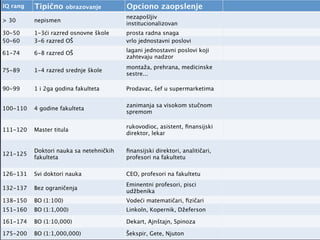

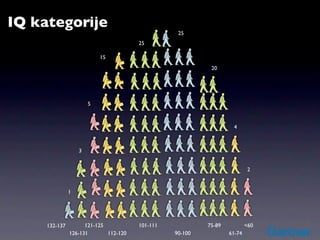

IQ rang Tipično Opciono zaopslenje

obrazovanje nezapošljiv

> 30 nepismen

IQ kategorije 30-50

25

1-3ći razred osnovne škole

institucionalizovan

prosta radna snaga

25

50-60 3-6 razred OŠ vrlo jednostavni poslovi

15

20

5

4

3

1

132-137 121-125 101-111 75-89

126-131 112-120 90-100 61-74

42.

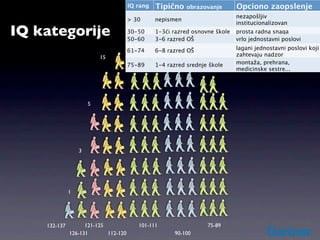

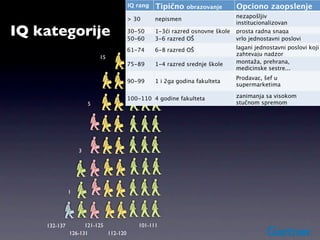

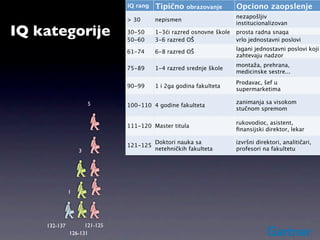

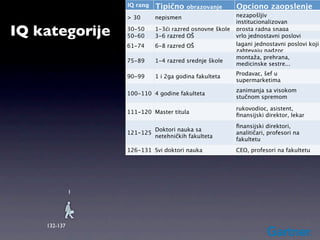

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

IQ kategorije 30-50

25

1-3ći razred osnovne škole

institucionalizovan

prosta radna snaga

25

50-60 3-6 razred OŠ vrlo jednostavni poslovi

15 lagani jednostavni poslovi koji

61-74 6-8 razred OŠ

20 zahtevaju nadzor

5

4

3

1

132-137 121-125 101-111 75-89

126-131 112-120 90-100 61-74

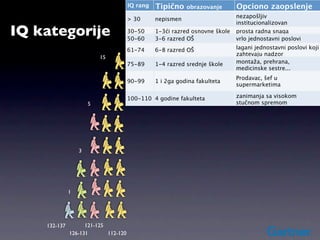

43.

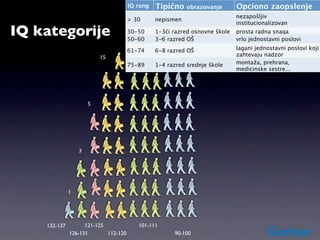

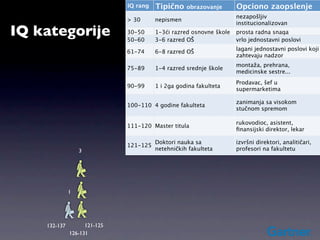

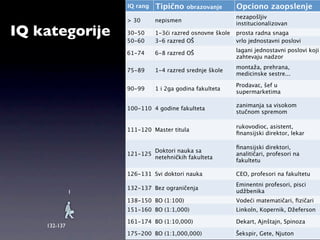

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

IQ kategorije 30-50

25

1-3ći razred osnovne škole

institucionalizovan

prosta radna snaga

25

50-60 3-6 razred OŠ vrlo jednostavni poslovi

15 lagani jednostavni poslovi koji

61-74 6-8 razred OŠ

20 zahtevaju nadzor

5

3

1

132-137 121-125 101-111 75-89

126-131 112-120 90-100

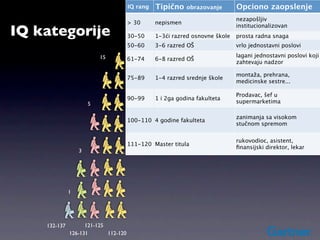

44.

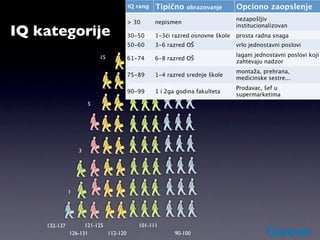

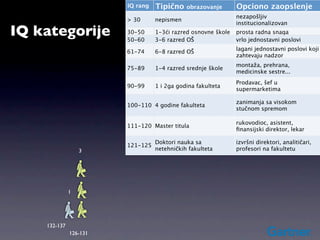

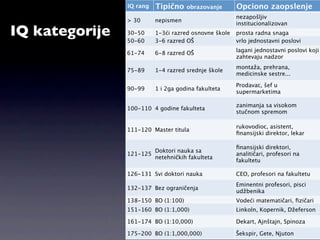

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

institucionalizovan

IQ kategorije 30-50

50-60

1-3ći razred osnovne škole

25

3-6 razred OŠ

prosta radna snaga

vrlo jednostavni poslovi

25

61-74 6-8 razred OŠ lagani jednostavni poslovi koji

15 zahtevaju nadzor

75-89 1-4 razred srednje škole montaža, prehrana,

20 medicinske sestre...

5

3

1

132-137 121-125 101-111 75-89

126-131 112-120 90-100

45.

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

institucionalizovan

IQ kategorije 30-50

50-60

1-3ći razred osnovne škole

25

3-6 razred OŠ

prosta radna snaga

vrlo jednostavni poslovi

25

61-74 6-8 razred OŠ lagani jednostavni poslovi koji

15 zahtevaju nadzor

75-89 1-4 razred srednje škole montaža, prehrana,

medicinske sestre...

5

3

1

132-137 121-125 101-111

126-131 112-120 90-100

46.

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

IQ kategorije

institucionalizovan

30-50 25

1-3ći razred osnovne škole prosta radna snaga

25

50-60 3-6 razred OŠ vrlo jednostavni poslovi

15 lagani jednostavni poslovi koji

61-74 6-8 razred OŠ

zahtevaju nadzor

montaža, prehrana,

75-89 1-4 razred srednje škole

medicinske sestre...

Prodavac, šef u

90-99 1 i 2ga godina fakulteta

supermarketima

5

3

1

132-137 121-125 101-111

126-131 112-120 90-100

47.

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

IQ kategorije

institucionalizovan

30-50 1-3ći razred osnovne škole prosta radna snaga

25

50-60 3-6 razred OŠ vrlo jednostavni poslovi

15 lagani jednostavni poslovi koji

61-74 6-8 razred OŠ

zahtevaju nadzor

montaža, prehrana,

75-89 1-4 razred srednje škole

medicinske sestre...

Prodavac, šef u

90-99 1 i 2ga godina fakulteta

supermarketima

5

3

1

132-137 121-125 101-111

126-131 112-120

48.

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

institucionalizovan

IQ kategorije 30-50

50-60

1-3ći razred osnovne škole

3-6 razred OŠ

prosta radna snaga

vrlo jednostavni poslovi

25

61-74 6-8 razred OŠ lagani jednostavni poslovi koji

zahtevaju nadzor

15

75-89 1-4 razred srednje škole montaža, prehrana,

medicinske sestre...

Prodavac, šef u

90-99 1 i 2ga godina fakulteta

supermarketima

100-110 4 godine fakulteta zanimanja sa visokom

5 stučnom spremom

3

1

132-137 121-125 101-111

126-131 112-120

49.

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

institucionalizovan

IQ kategorije 30-50

50-60

1-3ći razred osnovne škole

3-6 razred OŠ

prosta radna snaga

vrlo jednostavni poslovi

25

61-74 6-8 razred OŠ lagani jednostavni poslovi koji

zahtevaju nadzor

15

75-89 1-4 razred srednje škole montaža, prehrana,

medicinske sestre...

Prodavac, šef u

90-99 1 i 2ga godina fakulteta

supermarketima

100-110 4 godine fakulteta zanimanja sa visokom

5 stučnom spremom

3

1

132-137 121-125

126-131 112-120

50.

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

IQ kategorije

institucionalizovan

30-50 1-3ći razred osnovne škole prosta radna snaga

25

50-60 3-6 razred OŠ vrlo jednostavni poslovi

15 lagani jednostavni poslovi koji

61-74 6-8 razred OŠ

zahtevaju nadzor

montaža, prehrana,

75-89 1-4 razred srednje škole

medicinske sestre...

Prodavac, šef u

90-99 1 i 2ga godina fakulteta

5 supermarketima

zanimanja sa visokom

100-110 4 godine fakulteta

stučnom spremom

rukovodioc, asistent,

111-120 Master titula

finansijski direktor, lekar

3

1

132-137 121-125

126-131 112-120

51.

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

IQ kategorije

institucionalizovan

30-50 1-3ći razred osnovne škole prosta radna snaga

25

50-60 3-6 razred OŠ vrlo jednostavni poslovi

lagani jednostavni poslovi koji

61-74 6-8 razred OŠ

zahtevaju nadzor

montaža, prehrana,

75-89 1-4 razred srednje škole

medicinske sestre...

Prodavac, šef u

90-99 1 i 2ga godina fakulteta

5 supermarketima

zanimanja sa visokom

100-110 4 godine fakulteta

stučnom spremom

rukovodioc, asistent,

111-120 Master titula

finansijski direktor, lekar

3

1

132-137 121-125

126-131

52.

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

institucionalizovan

IQ kategorije 30-50

50-60

1-3ći razred osnovne škole

3-6 razred OŠ

prosta radna snaga

vrlo jednostavni poslovi

25

lagani jednostavni poslovi koji

61-74 6-8 razred OŠ

zahtevaju nadzor

montaža, prehrana,

75-89 1-4 razred srednje škole

medicinske sestre...

Prodavac, šef u

90-99 1 i 2ga godina fakulteta

supermarketima

5 zanimanja sa visokom

100-110 4 godine fakulteta

stučnom spremom

rukovodioc, asistent,

111-120 Master titula

finansijski direktor, lekar

Doktori nauka sa izvršni direktori, analitičari,

121-125

3 netehničkih fakulteta profesori na fakultetu

1

132-137 121-125

126-131

53.

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

institucionalizovan

IQ kategorije 30-50

50-60

1-3ći razred osnovne škole

3-6 razred OŠ

prosta radna snaga

vrlo jednostavni poslovi

25

lagani jednostavni poslovi koji

61-74 6-8 razred OŠ

zahtevaju nadzor

montaža, prehrana,

75-89 1-4 razred srednje škole

medicinske sestre...

Prodavac, šef u

90-99 1 i 2ga godina fakulteta

supermarketima

zanimanja sa visokom

100-110 4 godine fakulteta

stučnom spremom

rukovodioc, asistent,

111-120 Master titula

finansijski direktor, lekar

Doktori nauka sa izvršni direktori, analitičari,

121-125

3 netehničkih fakulteta profesori na fakultetu

1

132-137 121-125

126-131

54.

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

institucionalizovan

IQ kategorije 30-50

50-60

1-3ći razred osnovne škole

3-6 razred OŠ

prosta radna snaga

vrlo jednostavni poslovi

25

lagani jednostavni poslovi koji

61-74 6-8 razred OŠ

zahtevaju nadzor

montaža, prehrana,

75-89 1-4 razred srednje škole

medicinske sestre...

Prodavac, šef u

90-99 1 i 2ga godina fakulteta

supermarketima

zanimanja sa visokom

100-110 4 godine fakulteta

stučnom spremom

rukovodioc, asistent,

111-120 Master titula

finansijski direktor, lekar

Doktori nauka sa izvršni direktori, analitičari,

121-125

3 netehničkih fakulteta profesori na fakultetu

1

132-137

126-131

55.

IQ rang Tipično obrazovanje Opciono zaopslenje

> 30 nepismen nezapošljiv

institucionalizovan

IQ kategorije 30-50

50-60

1-3ći razred osnovne škole

3-6 razred OŠ

prosta radna snaga

vrlo jednostavni poslovi

25

61-74 6-8 razred OŠ lagani jednostavni poslovi koji

zahtevaju nadzor

montaža, prehrana,

75-89 1-4 razred srednje škole

medicinske sestre...

Prodavac, šef u

90-99 1 i 2ga godina fakulteta

supermarketima

zanimanja sa visokom

100-110 4 godine fakulteta

stučnom spremom

rukovodioc, asistent,

111-120 Master titula

finansijski direktor, lekar

finansijski direktori,

Doktori nauka sa

121-125 analitičari, profesori na

netehničkih fakulteta

fakultetu

3 126-131 Svi doktori nauka CEO, profesori na fakultetu

1

132-137

126-131

56.

IQ rang Tipično obrazovanje Opciono zaopslenje

> 30 nepismen nezapošljiv

institucionalizovan

IQ kategorije 30-50

50-60

1-3ći razred osnovne škole

3-6 razred OŠ

prosta radna snaga

vrlo jednostavni poslovi

25

61-74 6-8 razred OŠ lagani jednostavni poslovi koji

zahtevaju nadzor

montaža, prehrana,

75-89 1-4 razred srednje škole

medicinske sestre...

Prodavac, šef u

90-99 1 i 2ga godina fakulteta

supermarketima

zanimanja sa visokom

100-110 4 godine fakulteta

stučnom spremom

rukovodioc, asistent,

111-120 Master titula

finansijski direktor, lekar

finansijski direktori,

Doktori nauka sa

121-125 analitičari, profesori na

netehničkih fakulteta

fakultetu

126-131 Svi doktori nauka CEO, profesori na fakultetu

1

132-137

57.

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

institucionalizovan

IQ kategorije 30-50

50-60

1-3ći razred osnovne škole

3-6 razred OŠ

prosta radna snaga

vrlo jednostavni poslovi

25

lagani jednostavni poslovi koji

61-74 6-8 razred OŠ

zahtevaju nadzor

montaža, prehrana,

75-89 1-4 razred srednje škole

medicinske sestre...

Prodavac, šef u

90-99 1 i 2ga godina fakulteta

supermarketima

zanimanja sa visokom

100-110 4 godine fakulteta

stučnom spremom

rukovodioc, asistent,

111-120 Master titula

finansijski direktor, lekar

finansijski direktori,

Doktori nauka sa

121-125 analitičari, profesori na

netehničkih fakulteta

fakultetu

126-131 Svi doktori nauka CEO, profesori na fakultetu

Eminentni profesori, pisci

132-137 Bez ograničenja

1 udžbenika

138-150 BO (1:100) Vodeći matematičari, fizičari

151-160 BO (1:1,000) Linkoln, Kopernik, Džeferson

161-174 BO (1:10,000) Dekart, Ajnštajn, Spinoza

132-137

175-200 BO (1:1,000,000) Šekspir, Gete, Njuton

58.

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

institucionalizovan

IQ kategorije 30-50

50-60

1-3ći razred osnovne škole

3-6 razred OŠ

prosta radna snaga

vrlo jednostavni poslovi

25

lagani jednostavni poslovi koji

61-74 6-8 razred OŠ

zahtevaju nadzor

montaža, prehrana,

75-89 1-4 razred srednje škole

medicinske sestre...

Prodavac, šef u

90-99 1 i 2ga godina fakulteta

supermarketima

zanimanja sa visokom

100-110 4 godine fakulteta

stučnom spremom

rukovodioc, asistent,

111-120 Master titula

finansijski direktor, lekar

finansijski direktori,

Doktori nauka sa

121-125 analitičari, profesori na

netehničkih fakulteta

fakultetu

126-131 Svi doktori nauka CEO, profesori na fakultetu

Eminentni profesori, pisci

132-137 Bez ograničenja

udžbenika

138-150 BO (1:100) Vodeći matematičari, fizičari

151-160 BO (1:1,000) Linkoln, Kopernik, Džeferson

161-174 BO (1:10,000) Dekart, Ajnštajn, Spinoza

175-200 BO (1:1,000,000) Šekspir, Gete, Njuton

59.

IQ rang Tipično obrazovanje Opciono zaopslenje

nezapošljiv

> 30 nepismen

institucionalizovan

30-50 1-3ći razred osnovne škole prosta radna snaga

50-60 3-6 razred OŠ vrlo jednostavni poslovi

25

lagani jednostavni poslovi koji

61-74 6-8 razred OŠ

zahtevaju nadzor

montaža, prehrana, medicinske

75-89 1-4 razred srednje škole

sestre...

90-99 1 i 2ga godina fakulteta Prodavac, šef u supermarketima

zanimanja sa visokom stučnom

100-110 4 godine fakulteta

spremom

rukovodioc, asistent, finansijski

111-120 Master titula

direktor, lekar

Doktori nauka sa netehničkih finansijski direktori, analitičari,

121-125

fakulteta profesori na fakultetu

126-131 Svi doktori nauka CEO, profesori na fakultetu

Eminentni profesori, pisci

132-137 Bez ograničenja

udžbenika

138-150 BO (1:100) Vodeći matematičari, fizičari

151-160 BO (1:1,000) Linkoln, Kopernik, Džeferson

161-174 BO (1:10,000) Dekart, Ajnštajn, Spinoza

175-200 BO (1:1,000,000) Šekspir, Gete, Njuton

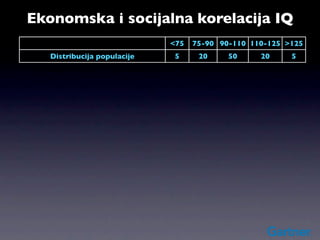

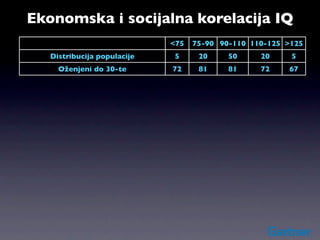

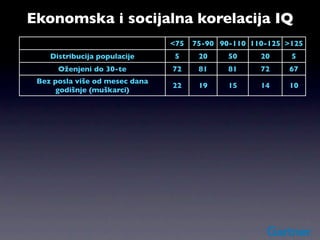

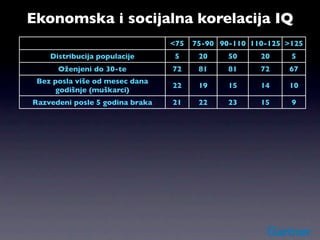

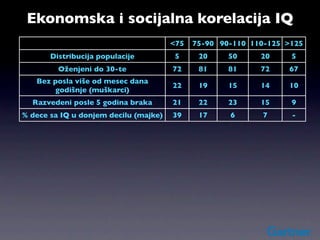

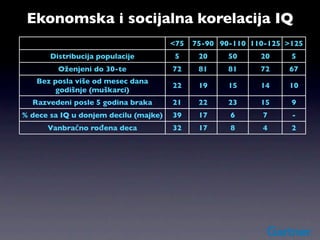

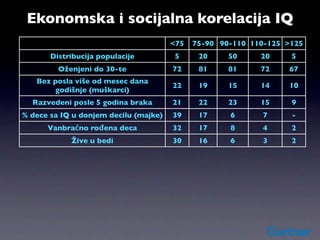

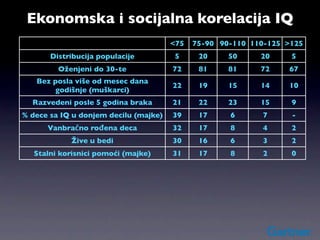

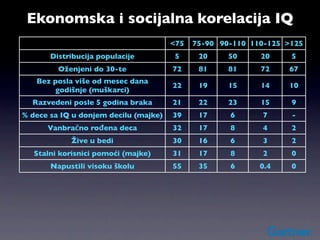

Ekonomska i socijalnakorelacija IQ

<75 75-90 90-110 110-125 >125

Distribucija populacije 5 20 50 20 5

Oženjeni do 30-te 72 81 81 72 67

Bez posla više od mesec dana

22 19 15 14 10

godišnje (muškarci)

Razvedeni posle 5 godina braka 21 22 23 15 9

% dece sa IQ u donjem decilu (majke) 39 17 6 7 -

Vanbračno rođena deca 32 17 8 4 2

Žive u bedi 30 16 6 3 2

Stalni korisnici pomoći (majke) 31 17 8 2 0

Napustili visoku školu 55 35 6 0.4 0

62.

Ekonomska i socijalnakorelacija IQ

<75 75-90 90-110 110-125 >125

Distribucija populacije 5 20 50 20 5

Oženjeni do 30-te 72 81 81 72 67

Bez posla više od mesec dana

22 19 15 14 10

godišnje (muškarci)

Razvedeni posle 5 godina braka 21 22 23 15 9

% dece sa IQ u donjem decilu (majke) 39 17 6 7 -

Vanbračno rođena deca 32 17 8 4 2

Žive u bedi 30 16 6 3 2

Stalni korisnici pomoći (majke) 31 17 8 2 0

Napustili visoku školu 55 35 6 0.4 0

63.

Ekonomska i socijalnakorelacija IQ

<75 75-90 90-110 110-125 >125

Distribucija populacije 5 20 50 20 5

Oženjeni do 30-te 72 81 81 72 67

Bez posla više od mesec dana

22 19 15 14 10

godišnje (muškarci)

Razvedeni posle 5 godina braka 21 22 23 15 9

% dece sa IQ u donjem decilu (majke) 39 17 6 7 -

Vanbračno rođena deca 32 17 8 4 2

Žive u bedi 30 16 6 3 2

Stalni korisnici pomoći (majke) 31 17 8 2 0

Napustili visoku školu 55 35 6 0.4 0

64.

Ekonomska i socijalnakorelacija IQ

<75 75-90 90-110 110-125 >125

Distribucija populacije 5 20 50 20 5

Oženjeni do 30-te 72 81 81 72 67

Bez posla više od mesec dana

22 19 15 14 10

godišnje (muškarci)

Razvedeni posle 5 godina braka 21 22 23 15 9

% dece sa IQ u donjem decilu (majke) 39 17 6 7 -

Vanbračno rođena deca 32 17 8 4 2

Žive u bedi 30 16 6 3 2

Stalni korisnici pomoći (majke) 31 17 8 2 0

Napustili visoku školu 55 35 6 0.4 0

65.

Ekonomska i socijalnakorelacija IQ

<75 75-90 90-110 110-125 >125

Distribucija populacije 5 20 50 20 5

Oženjeni do 30-te 72 81 81 72 67

Bez posla više od mesec dana

22 19 15 14 10

godišnje (muškarci)

Razvedeni posle 5 godina braka 21 22 23 15 9

% dece sa IQ u donjem decilu (majke) 39 17 6 7 -

Vanbračno rođena deca 32 17 8 4 2

Žive u bedi 30 16 6 3 2

Stalni korisnici pomoći (majke) 31 17 8 2 0

Napustili visoku školu 55 35 6 0.4 0

66.

Ekonomska i socijalnakorelacija IQ

<75 75-90 90-110 110-125 >125

Distribucija populacije 5 20 50 20 5

Oženjeni do 30-te 72 81 81 72 67

Bez posla više od mesec dana

22 19 15 14 10

godišnje (muškarci)

Razvedeni posle 5 godina braka 21 22 23 15 9

% dece sa IQ u donjem decilu (majke) 39 17 6 7 -

Vanbračno rođena deca 32 17 8 4 2

Žive u bedi 30 16 6 3 2

Stalni korisnici pomoći (majke) 31 17 8 2 0

Napustili visoku školu 55 35 6 0.4 0

67.

Ekonomska i socijalnakorelacija IQ

<75 75-90 90-110 110-125 >125

Distribucija populacije 5 20 50 20 5

Oženjeni do 30-te 72 81 81 72 67

Bez posla više od mesec dana

22 19 15 14 10

godišnje (muškarci)

Razvedeni posle 5 godina braka 21 22 23 15 9

% dece sa IQ u donjem decilu (majke) 39 17 6 7 -

Vanbračno rođena deca 32 17 8 4 2

Žive u bedi 30 16 6 3 2

Stalni korisnici pomoći (majke) 31 17 8 2 0

Napustili visoku školu 55 35 6 0.4 0

68.

Ekonomska i socijalnakorelacija IQ

<75 75-90 90-110 110-125 >125

Distribucija populacije 5 20 50 20 5

Oženjeni do 30-te 72 81 81 72 67

Bez posla više od mesec dana

22 19 15 14 10

godišnje (muškarci)

Razvedeni posle 5 godina braka 21 22 23 15 9

% dece sa IQ u donjem decilu (majke) 39 17 6 7 -

Vanbračno rođena deca 32 17 8 4 2

Žive u bedi 30 16 6 3 2

Stalni korisnici pomoći (majke) 31 17 8 2 0

Napustili visoku školu 55 35 6 0.4 0

69.

Ekonomska i socijalnakorelacija IQ

<75 75-90 90-110 110-125 >125

Distribucija populacije 5 20 50 20 5

Oženjeni do 30-te 72 81 81 72 67

Bez posla više od mesec dana

22 19 15 14 10

godišnje (muškarci)

Razvedeni posle 5 godina braka 21 22 23 15 9

% dece sa IQ u donjem decilu (majke) 39 17 6 7 -

Vanbračno rođena deca 32 17 8 4 2

Žive u bedi 30 16 6 3 2

Stalni korisnici pomoći (majke) 31 17 8 2 0

Napustili visoku školu 55 35 6 0.4 0

70.

Ekonomska i socijalnakorelacija IQ

<75 75-90 90-110 110-125 >125

Distribucija populacije 5 20 50 20 5

Oženjeni do 30-te 72 81 81 72 67

Bez posla više od mesec dana

22 19 15 14 10

godišnje (muškarci)

Razvedeni posle 5 godina braka 21 22 23 15 9

% dece sa IQ u donjem decilu (majke) 39 17 6 7 -

Vanbračno rođena deca 32 17 8 4 2

Žive u bedi 30 16 6 3 2

Stalni korisnici pomoći (majke) 31 17 8 2 0

Napustili visoku školu 55 35 6 0.4 0

Japan 105 Indonezija 89

Nemačka 102

Holandija 102 Irak 87

VelikaBritanija 100 Meksiko 87

SAD (belci) 100

Francuska 98 SAD (crnci) 85

Češka 97

Egipat 83

Grčka 92 Indija 81

Gvatemala 79

Malezija 92

79.

Japan 105 Indonezija 89

Nemačka 102 Hrvatska 88

Holandija 102 Irak 87

VelikaBritanija 100 Meksiko 87

SAD (belci) 100 Srbija 87

Francuska 98 SAD (crnci) 85

Češka 97 Bosna i Hercegovina 86

SFR Jugoslavija 95 Egipat 83

Grčka 94 Indija 81

Slovenija 93 Gvatemala 79

Malezija 92

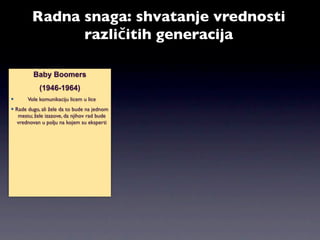

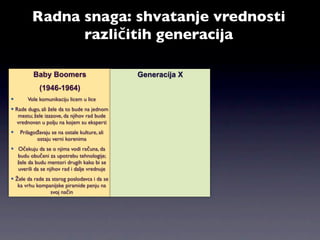

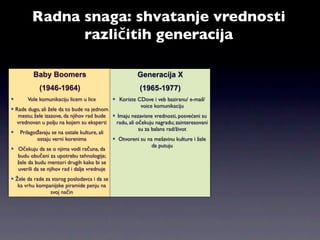

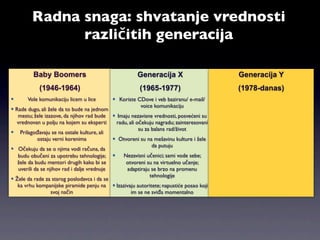

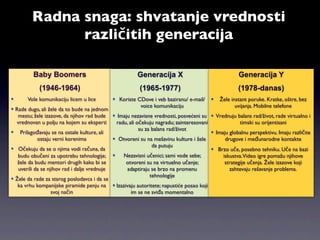

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers

(1946-1964)

Vole komunikaciju licem u lice

87.

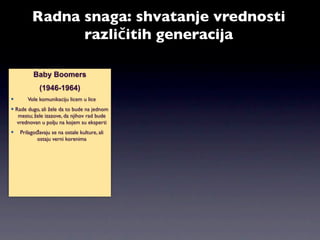

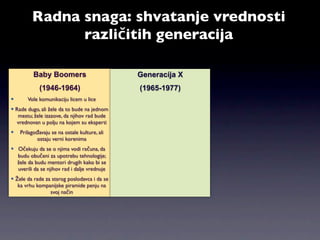

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers

(1946-1964)

Vole komunikaciju licem u lice

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude

vrednovan u polju na kojem su eksperti

88.

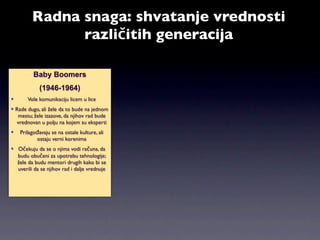

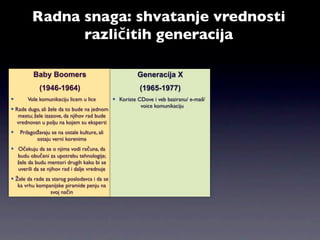

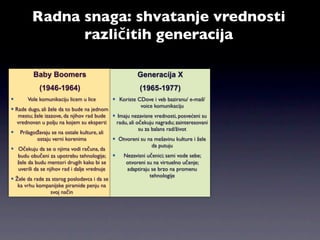

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers

(1946-1964)

Vole komunikaciju licem u lice

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude

vrednovan u polju na kojem su eksperti

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima

89.

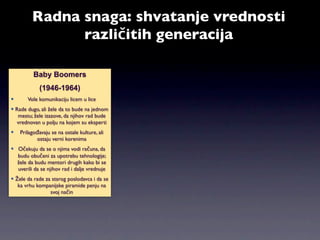

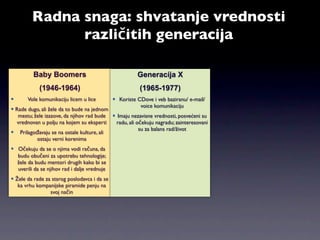

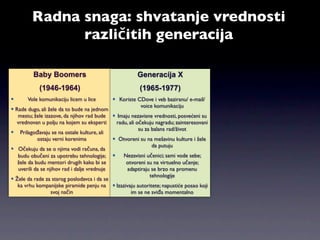

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers

(1946-1964)

Vole komunikaciju licem u lice

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude

vrednovan u polju na kojem su eksperti

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije;

žele da budu mentori drugih kako bi se

uverili da se njihov rad i dalje vrednuje

90.

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers

(1946-1964)

Vole komunikaciju licem u lice

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude

vrednovan u polju na kojem su eksperti

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije;

žele da budu mentori drugih kako bi se

uverili da se njihov rad i dalje vrednuje

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na

svoj način

91.

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X

(1946-1964)

Vole komunikaciju licem u lice

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude

vrednovan u polju na kojem su eksperti

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije;

žele da budu mentori drugih kako bi se

uverili da se njihov rad i dalje vrednuje

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na

svoj način

92.

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X

(1946-1964) (1965-1977)

Vole komunikaciju licem u lice

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude

vrednovan u polju na kojem su eksperti

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije;

žele da budu mentori drugih kako bi se

uverili da se njihov rad i dalje vrednuje

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na

svoj način

93.

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X

(1946-1964) (1965-1977)

Vole komunikaciju licem u lice Koriste CDove i veb baziranu/ e-mail/

voice komunikaciju

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude

vrednovan u polju na kojem su eksperti

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije;

žele da budu mentori drugih kako bi se

uverili da se njihov rad i dalje vrednuje

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na

svoj način

94.

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X

(1946-1964) (1965-1977)

Vole komunikaciju licem u lice Koriste CDove i veb baziranu/ e-mail/

voice komunikaciju

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude Imaju nezavisne vrednosti, posvećeni su

vrednovan u polju na kojem su eksperti radu, ali očekuju nagradu; zainteresovani

su za balans rad/život

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije;

žele da budu mentori drugih kako bi se

uverili da se njihov rad i dalje vrednuje

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na

svoj način

95.

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X

(1946-1964) (1965-1977)

Vole komunikaciju licem u lice Koriste CDove i veb baziranu/ e-mail/

voice komunikaciju

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude Imaju nezavisne vrednosti, posvećeni su

vrednovan u polju na kojem su eksperti radu, ali očekuju nagradu; zainteresovani

su za balans rad/život

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima Otvoreni su na mešavinu kulture i žele

da putuju

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije;

žele da budu mentori drugih kako bi se

uverili da se njihov rad i dalje vrednuje

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na

svoj način

96.

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X

(1946-1964) (1965-1977)

Vole komunikaciju licem u lice Koriste CDove i veb baziranu/ e-mail/

voice komunikaciju

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude Imaju nezavisne vrednosti, posvećeni su

vrednovan u polju na kojem su eksperti radu, ali očekuju nagradu; zainteresovani

su za balans rad/život

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima Otvoreni su na mešavinu kulture i žele

da putuju

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije; Nezavisni učenici; sami vode sebe;

žele da budu mentori drugih kako bi se otvoreni su na virtuelno učenje;

uverili da se njihov rad i dalje vrednuje adaptiraju se brzo na promenu

tehnologije

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na

svoj način

97.

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X

(1946-1964) (1965-1977)

Vole komunikaciju licem u lice Koriste CDove i veb baziranu/ e-mail/

voice komunikaciju

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude Imaju nezavisne vrednosti, posvećeni su

vrednovan u polju na kojem su eksperti radu, ali očekuju nagradu; zainteresovani

su za balans rad/život

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima Otvoreni su na mešavinu kulture i žele

da putuju

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije; Nezavisni učenici; sami vode sebe;

žele da budu mentori drugih kako bi se otvoreni su na virtuelno učenje;

uverili da se njihov rad i dalje vrednuje adaptiraju se brzo na promenu

tehnologije

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na Izazivaju autoritete; napustiće posao koji

svoj način im se ne sviđa momentalno

98.

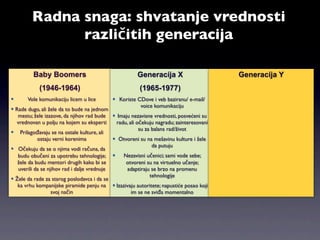

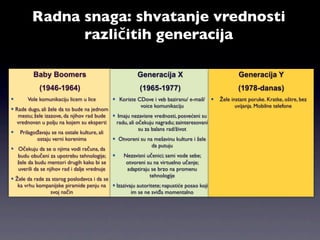

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X Generacija Y

(1946-1964) (1965-1977)

Vole komunikaciju licem u lice Koriste CDove i veb baziranu/ e-mail/

voice komunikaciju

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude Imaju nezavisne vrednosti, posvećeni su

vrednovan u polju na kojem su eksperti radu, ali očekuju nagradu; zainteresovani

su za balans rad/život

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima Otvoreni su na mešavinu kulture i žele

da putuju

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije; Nezavisni učenici; sami vode sebe;

žele da budu mentori drugih kako bi se otvoreni su na virtuelno učenje;

uverili da se njihov rad i dalje vrednuje adaptiraju se brzo na promenu

tehnologije

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na Izazivaju autoritete; napustiće posao koji

svoj način im se ne sviđa momentalno

99.

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X Generacija Y

(1946-1964) (1965-1977) (1978-danas)

Vole komunikaciju licem u lice Koriste CDove i veb baziranu/ e-mail/

voice komunikaciju

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude Imaju nezavisne vrednosti, posvećeni su

vrednovan u polju na kojem su eksperti radu, ali očekuju nagradu; zainteresovani

su za balans rad/život

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima Otvoreni su na mešavinu kulture i žele

da putuju

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije; Nezavisni učenici; sami vode sebe;

žele da budu mentori drugih kako bi se otvoreni su na virtuelno učenje;

uverili da se njihov rad i dalje vrednuje adaptiraju se brzo na promenu

tehnologije

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na Izazivaju autoritete; napustiće posao koji

svoj način im se ne sviđa momentalno

100.

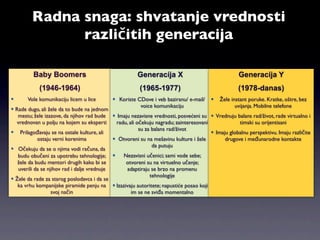

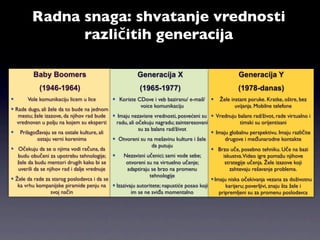

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X Generacija Y

(1946-1964) (1965-1977) (1978-danas)

Vole komunikaciju licem u lice Koriste CDove i veb baziranu/ e-mail/ Žele instant poruke. Kratke, oštre, bez

voice komunikaciju uvijanja. Mobilne telefone

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude Imaju nezavisne vrednosti, posvećeni su

vrednovan u polju na kojem su eksperti radu, ali očekuju nagradu; zainteresovani

su za balans rad/život

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima Otvoreni su na mešavinu kulture i žele

da putuju

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije; Nezavisni učenici; sami vode sebe;

žele da budu mentori drugih kako bi se otvoreni su na virtuelno učenje;

uverili da se njihov rad i dalje vrednuje adaptiraju se brzo na promenu

tehnologije

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na Izazivaju autoritete; napustiće posao koji

svoj način im se ne sviđa momentalno

101.

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X Generacija Y

(1946-1964) (1965-1977) (1978-danas)

Vole komunikaciju licem u lice Koriste CDove i veb baziranu/ e-mail/ Žele instant poruke. Kratke, oštre, bez

voice komunikaciju uvijanja. Mobilne telefone

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude Imaju nezavisne vrednosti, posvećeni su Vrednuju balans rad/život, rade virtualno i

vrednovan u polju na kojem su eksperti radu, ali očekuju nagradu; zainteresovani timski su orijentisani

su za balans rad/život

Prilagođavaju se na ostale kulture, ali

ostaju verni korenima Otvoreni su na mešavinu kulture i žele

da putuju

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije; Nezavisni učenici; sami vode sebe;

žele da budu mentori drugih kako bi se otvoreni su na virtuelno učenje;

uverili da se njihov rad i dalje vrednuje adaptiraju se brzo na promenu

tehnologije

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na Izazivaju autoritete; napustiće posao koji

svoj način im se ne sviđa momentalno

102.

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X Generacija Y

(1946-1964) (1965-1977) (1978-danas)

Vole komunikaciju licem u lice Koriste CDove i veb baziranu/ e-mail/ Žele instant poruke. Kratke, oštre, bez

voice komunikaciju uvijanja. Mobilne telefone

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude Imaju nezavisne vrednosti, posvećeni su Vrednuju balans rad/život, rade virtualno i

vrednovan u polju na kojem su eksperti radu, ali očekuju nagradu; zainteresovani timski su orijentisani

su za balans rad/život

Prilagođavaju se na ostale kulture, ali Imaju globalnu perspektivu. Imaju različite

ostaju verni korenima Otvoreni su na mešavinu kulture i žele drugove i međunarodne kontakte

da putuju

Očekuju da se o njima vodi računa, da

budu obučeni za upotrebu tehnologije; Nezavisni učenici; sami vode sebe;

žele da budu mentori drugih kako bi se otvoreni su na virtuelno učenje;

uverili da se njihov rad i dalje vrednuje adaptiraju se brzo na promenu

tehnologije

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na Izazivaju autoritete; napustiće posao koji

svoj način im se ne sviđa momentalno

103.

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X Generacija Y

(1946-1964) (1965-1977) (1978-danas)

Vole komunikaciju licem u lice Koriste CDove i veb baziranu/ e-mail/ Žele instant poruke. Kratke, oštre, bez

voice komunikaciju uvijanja. Mobilne telefone

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude Imaju nezavisne vrednosti, posvećeni su Vrednuju balans rad/život, rade virtualno i

vrednovan u polju na kojem su eksperti radu, ali očekuju nagradu; zainteresovani timski su orijentisani

su za balans rad/život

Prilagođavaju se na ostale kulture, ali Imaju globalnu perspektivu. Imaju različite

ostaju verni korenima Otvoreni su na mešavinu kulture i žele drugove i međunarodne kontakte

da putuju

Očekuju da se o njima vodi računa, da Brzo uče, posebno tehniku. Uče na bazi

budu obučeni za upotrebu tehnologije; Nezavisni učenici; sami vode sebe; iskustva.Video igre pomažu njihove

žele da budu mentori drugih kako bi se otvoreni su na virtuelno učenje; strategije učenja. Žele izazove koji

uverili da se njihov rad i dalje vrednuje adaptiraju se brzo na promenu zahtevaju rešavanje problema.

tehnologije

Žele da rade za starog poslodavca i da se

ka vrhu kompanijske piramide penju na Izazivaju autoritete; napustiće posao koji

svoj način im se ne sviđa momentalno

104.

Radna snaga: shvatanjevrednosti

različitih generacija

Baby Boomers Generacija X Generacija Y

(1946-1964) (1965-1977) (1978-danas)

Vole komunikaciju licem u lice Koriste CDove i veb baziranu/ e-mail/ Žele instant poruke. Kratke, oštre, bez

voice komunikaciju uvijanja. Mobilne telefone

Rade dugo, ali žele da to bude na jednom

mestu; žele izazove, da njihov rad bude Imaju nezavisne vrednosti, posvećeni su Vrednuju balans rad/život, rade virtualno i

vrednovan u polju na kojem su eksperti radu, ali očekuju nagradu; zainteresovani timski su orijentisani

su za balans rad/život

Prilagođavaju se na ostale kulture, ali Imaju globalnu perspektivu. Imaju različite

ostaju verni korenima Otvoreni su na mešavinu kulture i žele drugove i međunarodne kontakte

da putuju

Očekuju da se o njima vodi računa, da Brzo uče, posebno tehniku. Uče na bazi

budu obučeni za upotrebu tehnologije; Nezavisni učenici; sami vode sebe; iskustva.Video igre pomažu njihove

žele da budu mentori drugih kako bi se otvoreni su na virtuelno učenje; strategije učenja. Žele izazove koji

uverili da se njihov rad i dalje vrednuje adaptiraju se brzo na promenu zahtevaju rešavanje problema.

tehnologije

Žele da rade za starog poslodavca i da se Imaju niska očekivanja vezana za doživotnu

ka vrhu kompanijske piramide penju na Izazivaju autoritete; napustiće posao koji karijeru; poverljivi, znaju šta žele i

svoj način im se ne sviđa momentalno pripremljeni su za promenu poslodavca

110.

Što duže živim,to više osećam, da sve ono

što je bilo dobro za naše očeve, nije više

dobro za nas

Oscar Wilde (1854-1900)

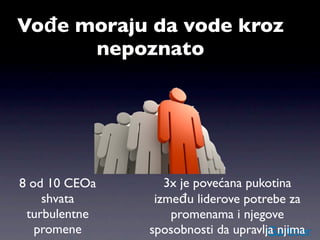

Vođe moraju davode kroz

nepoznato

8 od 10 CEOa 3x je povećana pukotina

shvata između liderove potrebe za

turbulentne promenama i njegove

promene sposobnosti da upravlja njima

174.

PONOVNO ZAMIŠLJANJE

IT

POSLOVANJE POSTMODERNE

POJEDNOSTAVLJIVANJE

KREATIVNA DESTRUKCIJA

Proširena stvarnost (Augmentedreality)

Pokaži mi organski sertifikat!

Pokaži mi GMO hranu!

Pokaži mi sadrćaj soli i masnoća!

230.

Theory of Everything

John Ellis (1946-) Britanski teorijski fizičar

The Superstring Theory of Everything or of Nothing

Nature, Vol 323, 595-598 (16 October 1986)

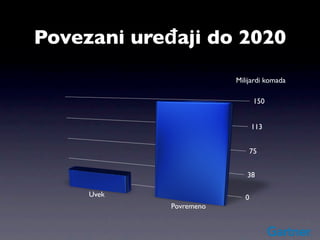

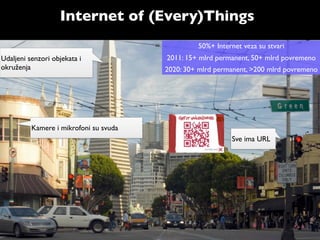

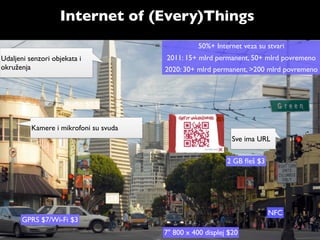

Internet of (Every)Things

50%+ Internet veza su stvari

2011: 15+ mlrd permanent, 50+ mlrd povremeno

2020: 30+ mlrd permanent, >200 mlrd povremeno

233.

Internet of (Every)Things

50%+ Internet veza su stvari

Udaljeni senzori objekata i 2011: 15+ mlrd permanent, 50+ mlrd povremeno

okruženja 2020: 30+ mlrd permanent, >200 mlrd povremeno

Kamere i mikrofoni su svuda

Sve ima URL

234.

Internet of (Every)Things

50%+ Internet veza su stvari

Udaljeni senzori objekata i 2011: 15+ mlrd permanent, 50+ mlrd povremeno

okruženja 2020: 30+ mlrd permanent, >200 mlrd povremeno

Audio $0.5

Kamere i mikrofoni su svuda

Sve ima URL

2 GB fleš $3

LTE

NFC

GPRS $7/Wi-Fi $3

7" 800 x 400 displej $20

235.

Internet of (Every)Things

50%+ Internet veza su stvari

Udaljeni senzori objekata i 2011: 15+ mlrd permanent, 50+ mlrd povremeno

okruženja 2020: 30+ mlrd permanent, >200 mlrd povremeno

Upravljanje

infrastrukturam

a i građevinama Nove putanje do

tržišta na osnovu QR

Audio $0.5 koda

Kamere i mikrofoni su svuda

Sve ima URL

2 GB fleš $3

Sadržaj i usluge putem

povezanih proizvoda

Augmented Situaciona podrška

LTE reality odlukama

NFC

GPRS $7/Wi-Fi $3

7" 800 x 400 displej $20

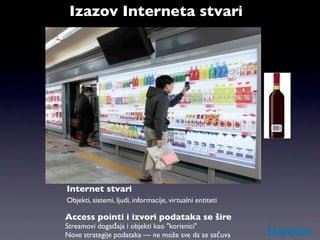

Izazov Interneta stvari

Internetstvari

Objekti, sistemi, ljudi, informacije, virtualni entiteti

Access pointi i izvori podataka se šire

238.

Izazov Interneta stvari

Internetstvari

Objekti, sistemi, ljudi, informacije, virtualni entiteti

Access pointi i izvori podataka se šire

Streamovi događaja i objekti kao "korisnici"

Nove strategije podataka — ne može sve da se sačuva

239.

Rej Kerzvejl (RayKurzweil)

“Pa, ono što je moglo da stane u zgradu, sada staje u naš džep, a ono što dans staje u naš

džep moći će da stane u krvnu ćeliju za 25 godina? Tako nešto još nismo videli.”

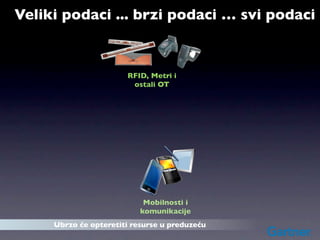

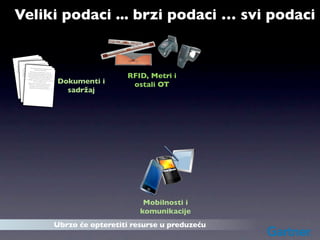

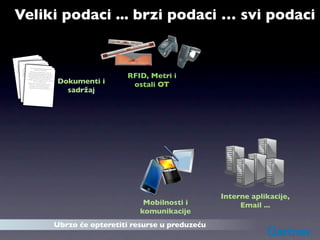

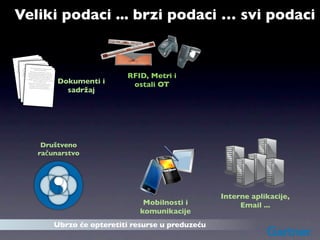

Veliki podaci ...brzi podaci … svi podaci

Ubrzo će opteretiti resurse u preduzeću

279.

Veliki podaci ...brzi podaci … svi podaci

Mobilnosti i

komunikacije

Ubrzo će opteretiti resurse u preduzeću

280.

Veliki podaci ...brzi podaci … svi podaci

RFID, Metri i

ostali OT

Mobilnosti i

komunikacije

Ubrzo će opteretiti resurse u preduzeću

281.

Veliki podaci ...brzi podaci … svi podaci

d

seball an

ckey, ba

aying ho s.

I like pl mountain

climbing th

ns in Nor at

civilizatio arvels th all and

baseb

I nt playi rin hockey,

The ancie like gineeng g m use

had en climbing mounca .s ce betains

America and Gree 700 year

d Rome t h

ancie ntabou ations in Nort

surpasse The the "0I"like playing hockn

civiliz "golde ey,

they invented discovered the g marvr baseball and

eerin theiels that

America had engin climbing mountains.

ey also aspect of ce because

eelier. Thsurpassed everyanci Gree

prove Rome The

and

RFID, Metri i

to im ring. ent civil 700 years

t

mean" they invented the had abou izations in North

Americ "0" eng ew "golden

enginee a

ed in N

discovered the

ineering marvels

eelier. They y invent Rom but t of their

all also

surpasse that

was actu improve dn food and e

every aspec

Pizzamean" tothey invented at, Greece because

Italia

y. It is not th "0" about

the

York cit N only

engineering.

Dokumenti i

earl ot

n food. ier. The China. in New

700 years

America wasinvented in y also discovered the

actually invented

"golden mean"

Pizzawas

i to n food but

spaghett city. It is not Italiaimprove every aspect

ostali OT

York of their engineethat, .

rican was Not only

AmePizza food.actu

ring

ted in China. in New

ally invented

spaghetti was inven

York city. It is

not Italian food

but

sadržaj

American food

. Not only that

spaghetti was ,

invented in Chin

a.

Mobilnosti i

komunikacije

Ubrzo će opteretiti resurse u preduzeću

282.

Veliki podaci ...brzi podaci … svi podaci

d

seball an

ckey, ba

aying ho s.

I like pl mountain

climbing th

ns in Nor at

civilizatio arvels th all and

baseb

I nt playi rin hockey,

The ancie like gineeng g m use

had en climbing mounca .s ce betains

America and Gree 700 year

d Rome t h

ancie ntabou ations in Nort

surpasse The the "0I"like playing hockn

civiliz "golde ey,

they invented discovered the g marvr baseball and

eerin theiels that

America had engin climbing mountains.

ey also aspect of ce because

eelier. Thsurpassed everyanci Gree

prove Rome The

and

RFID, Metri i

to im ring. ent civil 700 years

t

mean" they invented the had abou izations in North

Americ "0" eng ew "golden

enginee a

ed in N

discovered the

ineering marvels

eelier. They y invent Rom but t of their

all also

surpasse that

was actu improve dn food and e

every aspec

Pizzamean" tothey invented at, Greece because

Italia

y. It is not th "0" about

the

York cit N only

engineering.

Dokumenti i

earl ot

n food. ier. The China. in New

700 years

America wasinvented in y also discovered the

actually invented

"golden mean"

Pizzawas

i to n food but

spaghett city. It is not Italiaimprove every aspect

ostali OT

York of their engineethat, .

rican was Not only

AmePizza food.actu

ring

ted in China. in New

ally invented

spaghetti was inven

York city. It is

not Italian food

but

sadržaj

American food

. Not only that

spaghetti was ,

invented in Chin

a.

Interne aplikacije,

Mobilnosti i Email ...

komunikacije

Ubrzo će opteretiti resurse u preduzeću

283.

Veliki podaci ...brzi podaci … svi podaci

d

seball an

ckey, ba

aying ho s.

I like pl mountain

climbing th

ns in Nor at

civilizatio arvels th all and

baseb

I nt playi rin hockey,

The ancie like gineeng g m use

had en climbing mounca .s ce betains

America and Gree 700 year

d Rome t h

ancie ntabou ations in Nort

surpasse The the "0I"like playing hockn

civiliz "golde ey,

they invented discovered the g marvr baseball and

eerin theiels that

America had engin climbing mountains.

ey also aspect of ce because

eelier. Thsurpassed everyanci Gree

prove Rome The

and

RFID, Metri i

to im ring. ent civil 700 years

t

mean" they invented the had abou izations in North

Americ "0" eng ew "golden

enginee a

ed in N

discovered the

ineering marvels

eelier. They y invent Rom but t of their

all also

surpasse that

was actu improve dn food and e

every aspec

Pizzamean" tothey invented at, Greece because

Italia

y. It is not th "0" about

the

York cit N only

engineering.

Dokumenti i

earl ot

n food. ier. The China. in New

700 years

America wasinvented in y also discovered the

actually invented

"golden mean"

Pizzawas

i to n food but

spaghett city. It is not Italiaimprove every aspect

ostali OT

York of their engineethat, .

rican was Not only

AmePizza food.actu

ring

ted in China. in New

ally invented

spaghetti was inven

York city. It is

not Italian food

but

sadržaj

American food

. Not only that

spaghetti was ,

invented in Chin

a.

Društveno

računarstvo

Interne aplikacije,

Mobilnosti i Email ...

komunikacije

Ubrzo će opteretiti resurse u preduzeću

284.

Veliki podaci ...brzi podaci … svi podaci

d

seball an

ckey, ba

aying ho s.

I like pl mountain

climbing th

ns in Nor at

civilizatio arvels th all and

baseb

I nt playi rin hockey,

The ancie like gineeng g m use

had en climbing mounca .s ce betains

America and Gree 700 year

d Rome t h

ancie ntabou ations in Nort

surpasse The the "0I"like playing hockn

civiliz "golde ey,

they invented discovered the g marvr baseball and

eerin theiels that

America had engin climbing mountains.

ey also aspect of ce because

eelier. Thsurpassed everyanci Gree

prove Rome The

and

RFID, Metri i

to im ring. ent civil 700 years

t

mean" they invented the had abou izations in North

Americ "0" eng ew "golden

enginee a

ed in N

discovered the

ineering marvels

eelier. They y invent Rom but t of their

all also

surpasse that

was actu improve dn food and e

every aspec

Pizzamean" tothey invented at, Greece because

Italia

y. It is not th "0" about

the

York cit N only

engineering.

Dokumenti i

earl ot

n food. ier. The China. in New

700 years

America wasinvented in y also discovered the

actually invented

"golden mean"

Pizzawas

i to n food but

spaghett city. It is not Italiaimprove every aspect

ostali OT

York of their engineethat, .

rican was Not only

AmePizza food.actu

ring

ted in China. in New

ally invented

spaghetti was inven

York city. It is

not Italian food

but

sadržaj

American food

. Not only that

spaghetti was ,

invented in Chin

a.

Društveno

računarstvo

B2B

Interne aplikacije,

Mobilnosti i Email ...

komunikacije

Ubrzo će opteretiti resurse u preduzeću

285.

Veliki podaci ...brzi podaci … svi podaci

d

seball an

ckey, ba

aying ho s.

I like pl mountain

climbing th

ns in Nor at

civilizatio arvels th all and

baseb

I nt playi rin hockey,

The ancie like gineeng g m use

had en climbing mounca .s ce betains

America and Gree 700 year

d Rome t h

ancie ntabou ations in Nort

surpasse The the "0I"like playing hockn

civiliz "golde ey,

they invented discovered the g marvr baseball and

eerin theiels that

America had engin climbing mountains.

ey also aspect of ce because

eelier. Thsurpassed everyanci Gree

prove Rome The

and

RFID, Metri i

to im ring. ent civil 700 years

t

mean" they invented the had abou izations in North

Americ "0" eng ew "golden

enginee a

ed in N

discovered the

ineering marvels

eelier. They y invent Rom but t of their

all also

surpasse that

was actu improve dn food and e

every aspec

Pizzamean" tothey invented at, Greece because

Italia

y. It is not th "0" about

the

York cit N only

engineering.

Dokumenti i

earl ot

n food. ier. The China. in New

700 years

America wasinvented in y also discovered the

actually invented

"golden mean"

Pizzawas

i to n food but

spaghett city. It is not Italiaimprove every aspect

ostali OT

York of their engineethat, .

rican was Not only

AmePizza food.actu

ring

ted in China. in New

ally invented

spaghetti was inven

York city. It is

not Italian food

but

sadržaj

American food

. Not only that

spaghetti was ,

invented in Chin

a.

Računarstvo u oblaku i

podaci u oblaku

Društveno

računarstvo

B2B

Interne aplikacije,

Mobilnosti i Email ...

komunikacije

Ubrzo će opteretiti resurse u preduzeću

286.

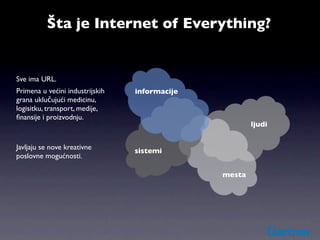

Šta je Internetof Everything?

Sve ima URL.

Primena u većini industrijskih

grana uklučujući medicinu,

logisitku, transport, medije,

finansije i proizvodnju.

Javljaju se nove kreativne

poslovne mogućnosti.

287.

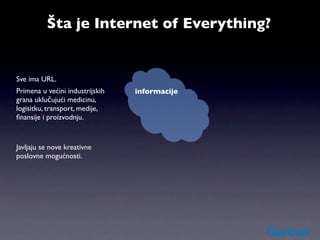

Šta je Internetof Everything?

Sve ima URL.

Primena u većini industrijskih informacije

grana uklučujući medicinu,

logisitku, transport, medije,

finansije i proizvodnju.

Javljaju se nove kreativne

poslovne mogućnosti.

288.

Šta je Internetof Everything?

Sve ima URL.

Primena u većini industrijskih informacije

grana uklučujući medicinu,

logisitku, transport, medije,

finansije i proizvodnju.

ljudi

Javljaju se nove kreativne

poslovne mogućnosti.

289.

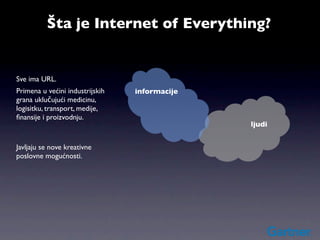

Šta je Internetof Everything?

Sve ima URL.

Primena u većini industrijskih informacije

grana uklučujući medicinu,

logisitku, transport, medije,

finansije i proizvodnju.

ljudi

Javljaju se nove kreativne

poslovne mogućnosti.

mesta

290.

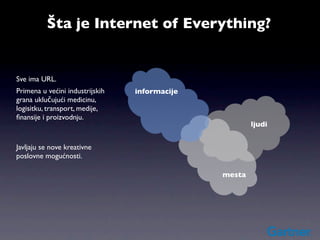

Šta je Internetof Everything?

Sve ima URL.

Primena u većini industrijskih informacije

grana uklučujući medicinu,

logisitku, transport, medije,

finansije i proizvodnju.

ljudi

Javljaju se nove kreativne sistemi

poslovne mogućnosti.

mesta

291.

Šta je Internetof Everything?

Sve ima URL.

fizički objekti

Primena u većini industrijskih informacije

grana uklučujući medicinu,

logisitku, transport, medije,

finansije i proizvodnju.

ljudi

Javljaju se nove kreativne sistemi

poslovne mogućnosti.

mesta

292.

Šta je Internetof Everything?

Sve ima URL.

fizički objekti

Primena u većini industrijskih informacije

grana uklučujući medicinu,

logisitku, transport, medije,

finansije i proizvodnju.

ljudi

Javljaju se nove kreativne sistemi

poslovne mogućnosti.

virtualni mesta

entiteti

293.

Šta je Internetof Everything?

sve

Sve ima URL.

fizički objekti

Primena u većini industrijskih informacije

grana uklučujući medicinu,

logisitku, transport, medije,

finansije i proizvodnju.

ljudi

Javljaju se nove kreativne sistemi

poslovne mogućnosti.

virtualni mesta

entiteti

#22 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#23 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#24 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#25 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#26 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#27 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#28 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#29 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#30 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#31 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#32 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#33 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#34 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#35 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#36 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#37 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#38 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#39 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n

#40 Key Issue: What are CEOs' views on their CIOs' current and next positions?\nWe ran this question in a form that was very close to this year's EXP CIO survey in order to compare and contrast for differences of opinion and expectation. Though the detail comparison analysis is not complete, it appears that responses from CEOs and CIOs were in fact quite well aligned.\nA few of points to note:\n About a quarter of CIOs come from a business background. Here we see about a fifth of CEOs anticipating their CIO moving on to a business leadership role internally. It's likely this represents the cycling of business background people through the CIO position and that relatively few IT background CIOs are seen by their CEOs as internal business leaders next.\n In total, 40% of CEOs see their CIO as moving to a CIO in another company in a different industry. This suggest many see the role as an industry agnostic, itinerant professional and that makes it much less likely to be a closely held relationship.\n Only one CEO out of 229 thinks their CIO could be his or her successor. We may be at the apex of the information age but CIO is not a strong CXO route to the top job. \n