Download to read offline

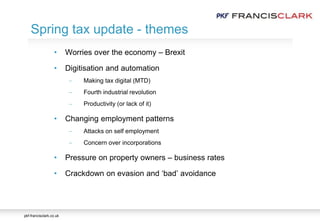

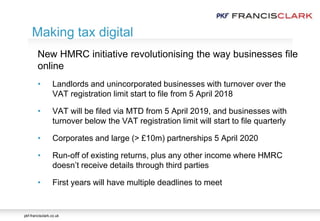

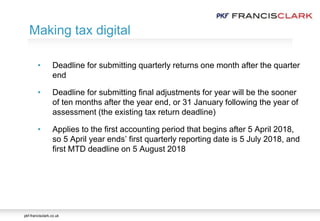

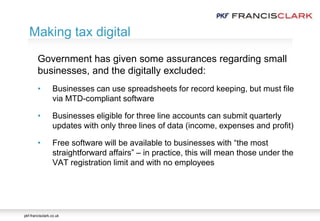

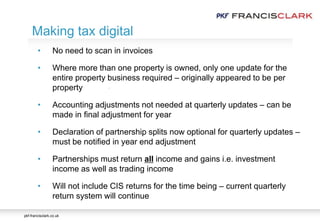

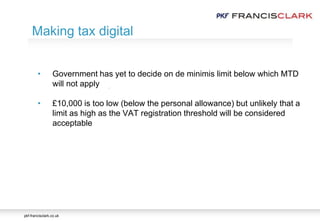

The document is a tax update from PKF Francis Clark, detailing recent staff appointments, upcoming changes to tax legislation, and the impact of Brexit on tax policies. Key topics include the implementation of Making Tax Digital, changes to corporation tax rates, and new measures affecting business rates and residential property taxation. It highlights the importance of compliance with evolving tax regulations and the need for businesses to adapt to digital filing requirements.