Solution Manual for Auditing and Assurance Services 17th by Arens

Solution Manual for Auditing and Assurance Services 17th by Arens

Solution Manual for Auditing and Assurance Services 17th by Arens

Solution Manual for Auditing and Assurance Services 17th by Arens

Solution Manual for Auditing and Assurance Services 17th by Arens

1.

Download the fullversion and explore a variety of test banks

or solution manuals at https://testbankbell.com

Solution Manual for Auditing and Assurance

Services 17th by Arens

_____ Tap the link below to start your download _____

http://testbankbell.com/product/solution-manual-for-

auditing-and-assurance-services-17th-by-arens/

Find test banks or solution manuals at testbankbell.com today!

2.

Here are somerecommended products for you. Click the link to

download, or explore more at testbankbell.com

Test Bank for Auditing and Assurance Services 17th by

Arens

http://testbankbell.com/product/test-bank-for-auditing-and-assurance-

services-17th-by-arens/

Auditing and Assurance Services 16th Edition Arens

Solutions Manual

http://testbankbell.com/product/auditing-and-assurance-services-16th-

edition-arens-solutions-manual/

Solution manual for Auditing and Assurance Services Arens

Elder Beasley 15th edition

http://testbankbell.com/product/solution-manual-for-auditing-and-

assurance-services-arens-elder-beasley-15th-edition/

Test Bank for Contemporary Advertising and Integrated

Marketing Communications, 14th Edition : Arens

http://testbankbell.com/product/test-bank-for-contemporary-

advertising-and-integrated-marketing-communications-14th-edition-

arens/

3.

Human Resource ManagementNoe 8th Edition Solutions Manual

http://testbankbell.com/product/human-resource-management-noe-8th-

edition-solutions-manual/

Test Bank for Principles of Auditing and Other Assurance

Services, 21st Edition, Whittington

http://testbankbell.com/product/test-bank-for-principles-of-auditing-

and-other-assurance-services-21st-edition-whittington/

Test Bank for Precalculus: Concepts Through Functions, A

Unit Circle Approach to Trigonometry 4th Edition by

Sullivan

http://testbankbell.com/product/test-bank-for-precalculus-concepts-

through-functions-a-unit-circle-approach-to-trigonometry-4th-edition-

by-sullivan/

Test Bank for Business Essentials 9th Edition by Ebert

http://testbankbell.com/product/test-bank-for-business-essentials-9th-

edition-by-ebert/

Test Bank for C++ Programming: From Problem Analysis to

Program Design, 6th Edition – D.S. Malik

http://testbankbell.com/product/test-bank-for-c-programming-from-

problem-analysis-to-program-design-6th-edition-d-s-malik/

4.

Solution Manual forTerrorism and Homeland Security, 9th

Edition

http://testbankbell.com/product/solution-manual-for-terrorism-and-

homeland-security-9th-edition/

5.

1-1

Solution Manual forAuditing and Assurance

Services 17th by Arens

Full download link at: https://testbankbell.com/product/solution-

manual-for-auditing-and-assurance-services-17th-by-arens/

Chapter 1

The Demand for Audit and Other Assurance Services

Concept Checks

P. 8

1. To do an audit, there must be information in a verifiable form and some

standards (criteria) by which the auditor can evaluate the information.

Determining the degree of correspondence between information and

established criteria is determining whether a given set of information is in

accordance with the established criteria. For an audit of a company’s financial

statements the criteria are U.S. generally accepted accounting principles or

International Financial Reporting Standards.

2. The four primary causes of information risk are remoteness of information,

biases and motives of the provider, voluminous data, and the existence of complex

exchange transactions.

The three main ways to reduce information risk are:

1. User verifies the information.

2. User shares the information risk with management.

3. Audited financial statements are provided.

P. 16

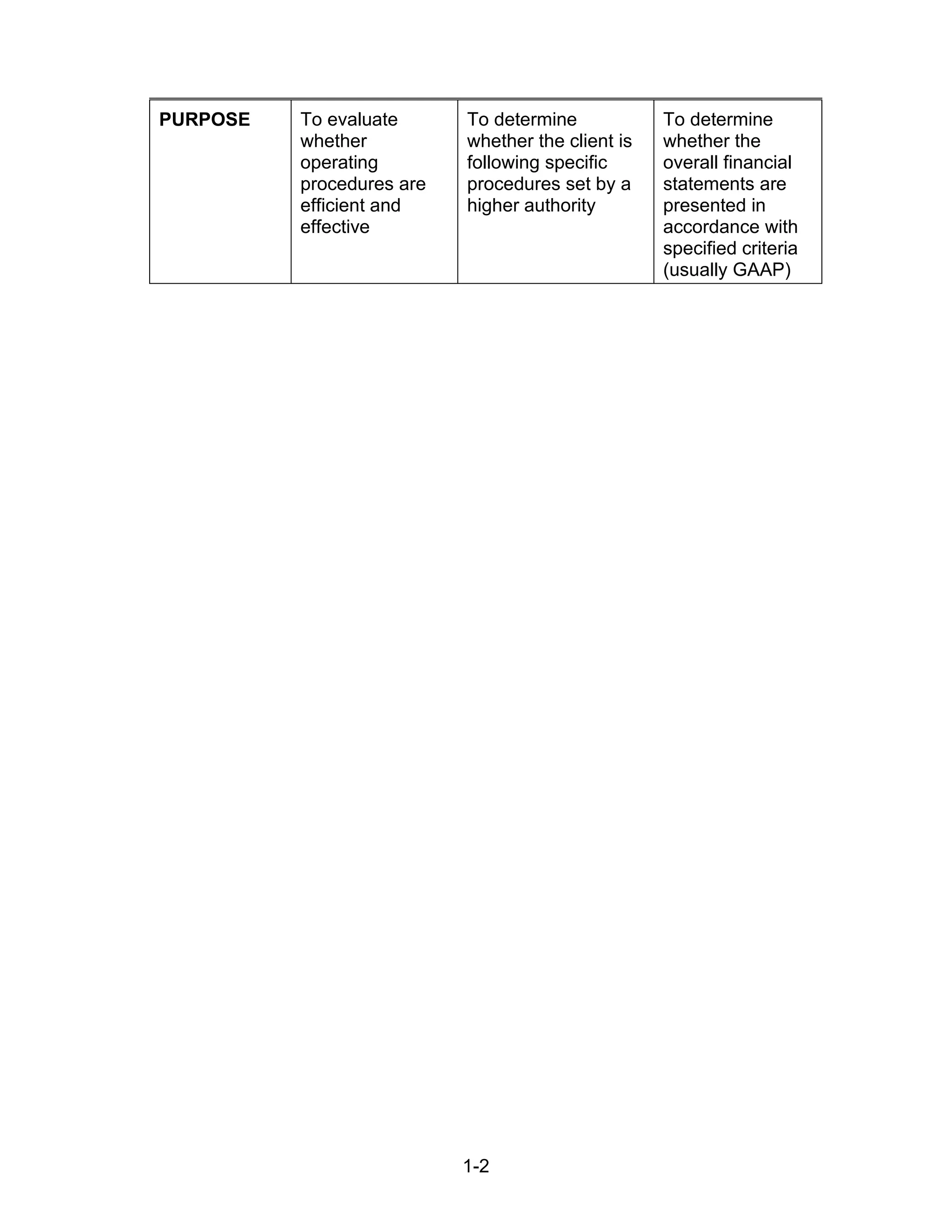

1. The three main types of audits are operational audits, compliance audits, and

financial statement audits. The table below summarizes the purposes and

nature of each type of audit.

OPERATIONAL

AUDITS

COMPLIANCE

AUDITS

AUDITS OF

FINANCIAL

STATEMENTS

6.

1-2

PURPOSE To evaluate

whether

operating

proceduresare

efficient and

effective

To determine

whether the client is

following specific

procedures set by a

higher authority

To determine

whether the

overall financial

statements are

presented in

accordance with

specified criteria

(usually GAAP)

7.

1-3

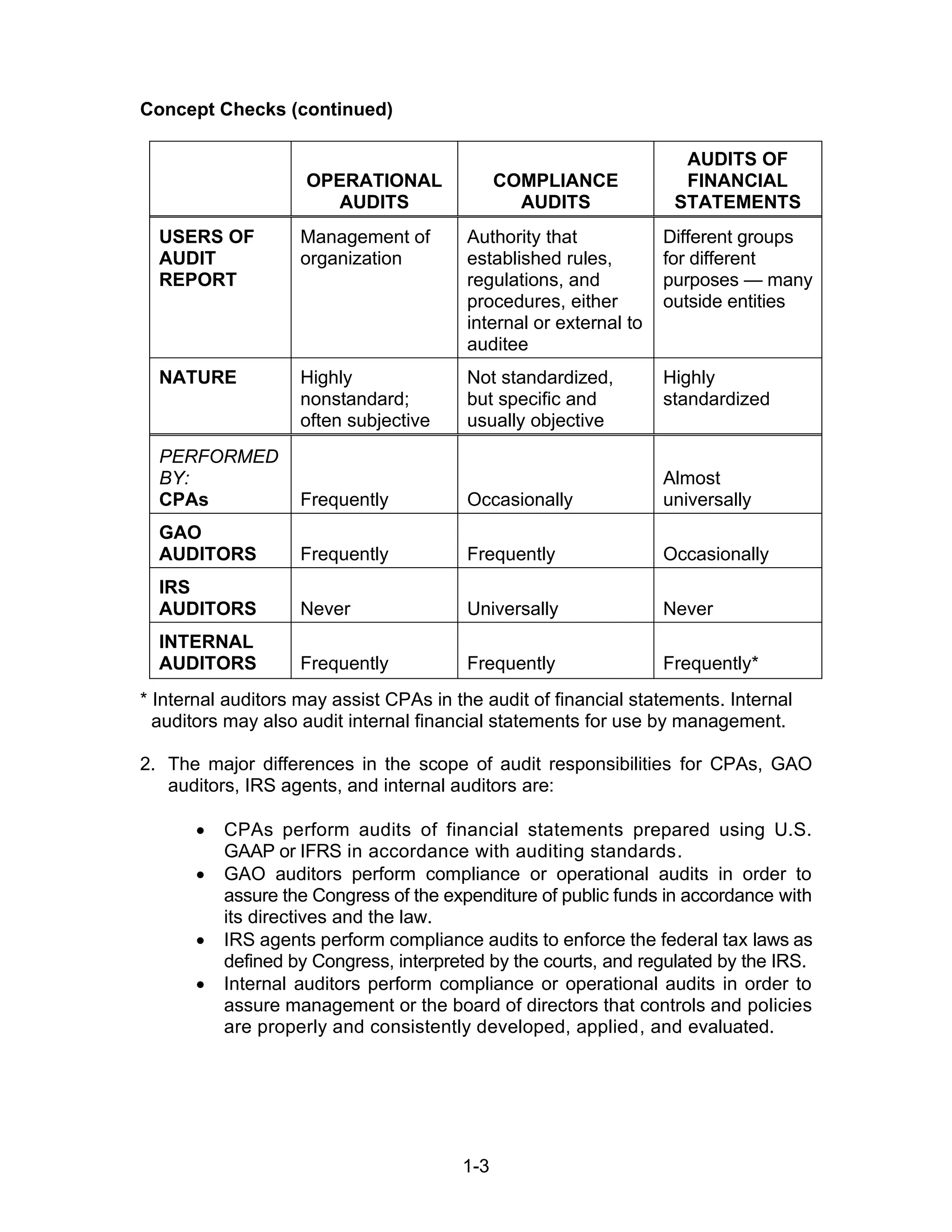

Concept Checks (continued)

OPERATIONAL

AUDITS

COMPLIANCE

AUDITS

AUDITSOF

FINANCIAL

STATEMENTS

USERS OF

AUDIT

REPORT

Management of

organization

Authority that

established rules,

regulations, and

procedures, either

internal or external to

auditee

Different groups

for different

purposes — many

outside entities

NATURE Highly

nonstandard;

often subjective

Not standardized,

but specific and

usually objective

Highly

standardized

PERFORMED

BY:

CPAs Frequently Occasionally

Almost

universally

GAO

AUDITORS Frequently Frequently Occasionally

IRS

AUDITORS Never Universally Never

INTERNAL

AUDITORS Frequently Frequently Frequently*

* Internal auditors may assist CPAs in the audit of financial statements. Internal

auditors may also audit internal financial statements for use by management.

2. The major differences in the scope of audit responsibilities for CPAs, GAO

auditors, IRS agents, and internal auditors are:

• CPAs perform audits of financial statements prepared using U.S.

GAAP or IFRS in accordance with auditing standards.

• GAO auditors perform compliance or operational audits in order to

assure the Congress of the expenditure of public funds in accordance with

its directives and the law.

• IRS agents perform compliance audits to enforce the federal tax laws as

defined by Congress, interpreted by the courts, and regulated by the IRS.

• Internal auditors perform compliance or operational audits in order to

assure management or the board of directors that controls and policies

are properly and consistently developed, applied, and evaluated.

8.

1-4

Review Questions

1-1To do an audit, there must be information in a verifiable form and some

standards (criteria) by which the auditor can evaluate the information. The

information for Jones Company's tax return is the federal tax returns filed by the

company. The established criteria are found in the Internal Revenue Code

and all interpretations. For the audit of Jones Company's financial statements

the information is the financial statements being audited and the established

criteria are U.S. GAAP or IFRS.

1-2 This apparent paradox arises from the distinction between the function of

auditing and the function of accounting. The accounting function is the recording,

classifying, and summarizing of economic events to provide relevant information

to decision makers. The rules of accounting are the criteria used by the auditor for

evaluating the presentation of economic events for financial statements and he or

she must therefore have an understanding of accounting standards, as well as

auditing standards. The accountant need not, and frequently does not, understand

what auditors do, unless he or she is involved in doing audits, or has been trained

as an auditor.

1-3 An independent audit is a means of satisfying the need for reliable

information on the part of decision makers. Recent changes in accounting and

business operations include:

1. Increased global activities of many businesses

a. Multiple product lines and transaction locations

b. Foreign exchange affects transactions

2. Complex accounting and exchange transactions

a. Increasing use of derivatives and hedging activities

b. Increasingly complex accounting standards in areas such as

revenue recognition

3. More complex information systems

a. Possibly millions of transactions processed daily through on-

line and traditional sales channels

b. Voluminous data requires interpretation

1-4 1. Risk-free interest rate This is approximately the rate the bank could

earn by investing in U.S. treasury notes for the same length of time

as the business loan.

2. Business risk for the customer This risk reflects the possibility that

the business will not be able to repay its loan because of economic

or business conditions such as a recession, poor management

decisions, or unexpected competition in the industry.

3. Information risk This risk reflects the possibility that the information

upon which the business risk decision was made was inaccurate. A

likely cause of the information risk is the possibility of inaccurate

financial statements.

9.

1-5

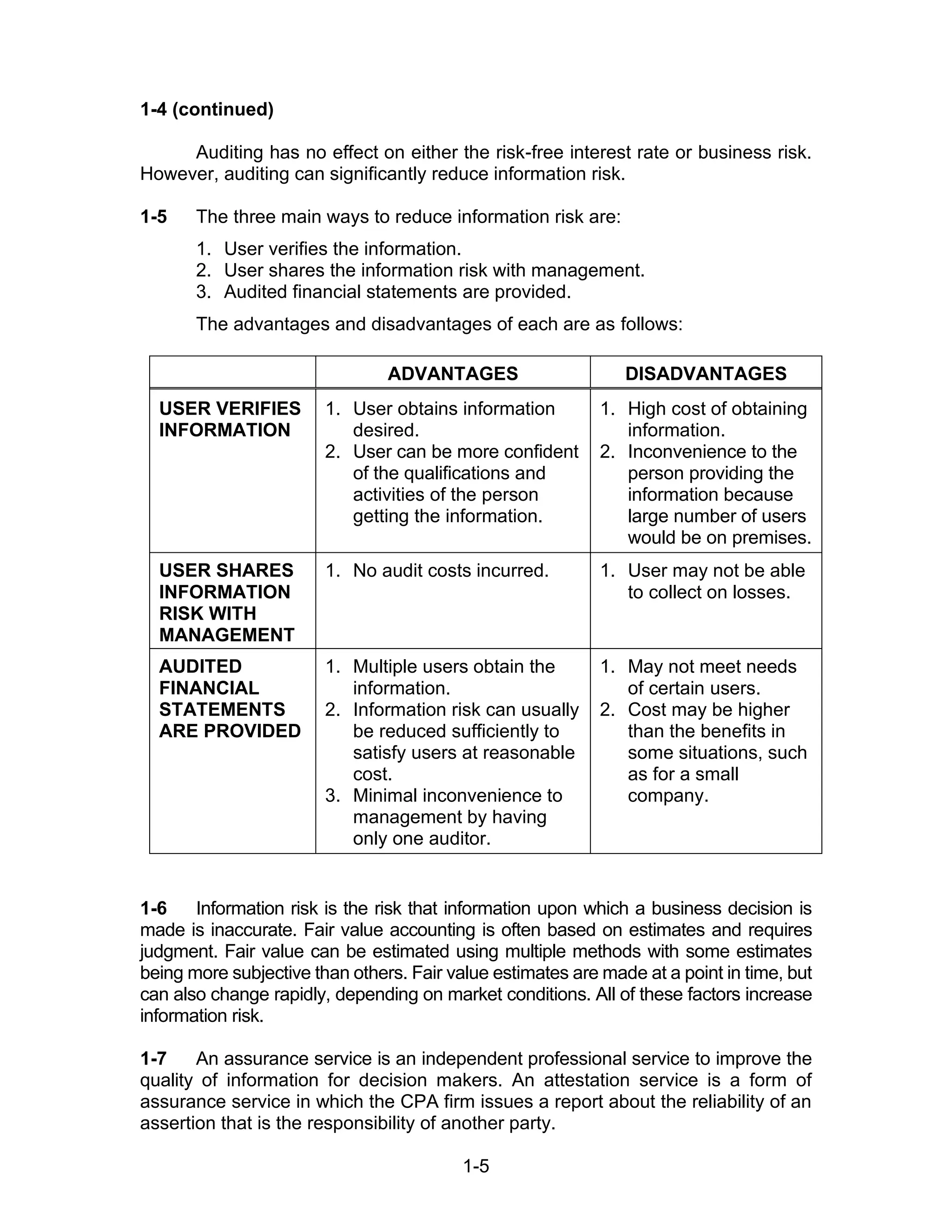

1-4 (continued)

Auditing hasno effect on either the risk-free interest rate or business risk.

However, auditing can significantly reduce information risk.

1-5 The three main ways to reduce information risk are:

1. User verifies the information.

2. User shares the information risk with management.

3. Audited financial statements are provided.

The advantages and disadvantages of each are as follows:

ADVANTAGES DISADVANTAGES

USER VERIFIES

INFORMATION

1. User obtains information

desired.

2. User can be more confident

of the qualifications and

activities of the person

getting the information.

1. High cost of obtaining

information.

2. Inconvenience to the

person providing the

information because

large number of users

would be on premises.

USER SHARES

INFORMATION

RISK WITH

MANAGEMENT

1. No audit costs incurred. 1. User may not be able

to collect on losses.

AUDITED

FINANCIAL

STATEMENTS

ARE PROVIDED

1. Multiple users obtain the

information.

2. Information risk can usually

be reduced sufficiently to

satisfy users at reasonable

cost.

3. Minimal inconvenience to

management by having

only one auditor.

1. May not meet needs

of certain users.

2. Cost may be higher

than the benefits in

some situations, such

as for a small

company.

1-6 Information risk is the risk that information upon which a business decision is

made is inaccurate. Fair value accounting is often based on estimates and requires

judgment. Fair value can be estimated using multiple methods with some estimates

being more subjective than others. Fair value estimates are made at a point in time, but

can also change rapidly, depending on market conditions. All of these factors increase

information risk.

1-7 An assurance service is an independent professional service to improve the

quality of information for decision makers. An attestation service is a form of

assurance service in which the CPA firm issues a report about the reliability of an

assertion that is the responsibility of another party.

10.

1-6

1-7 (continued)

The mostcommon form of audit service is an audit of historical financial

statements, in which the auditor expresses a conclusion as to whether the

financial statements are presented in accordance with an applicable financial

reporting framework such as U.S. GAAP or IFRS. An example of an attestation

service is a report on the effectiveness of an entity’s internal control over financial

reporting. There are many possible forms of assurance services, including services

related to business performance measurement, health care performance, and

information system reliability.

1-8 Some organizations issue sustainability reports to highlight the work they

are doing related to the environment, social issues, and governance (often referred

to as ESG). These reports include different types of data that reflect the

organization’s overall performance related to their sustainability efforts. For

example, some organizations provide data related to carbon emissions, resource

usage, and waste generation to highlight their impact on the environment. Others

report demographic data about the types of individuals they hire as employees or

serve as customers. Investors and other users of these sustainability reports may

desire assurance from CPAs about the accuracy and reliability of these data items.

1-9 The primary evidence the internal revenue agent will use in the audit of the

Jones Company's tax return include all available documentation and other

information available in Jones’ office or from other sources. For example, when the

internal revenue agent audits taxable income, a major source of information will be

bank statements, the cash receipts journal and deposit slips. The internal revenue

agent is likely to emphasize unrecorded receipts and revenues. For expenses,

major sources of evidence are likely to be cancelled checks and electronic funds

transfers, vendors' invoices, and other supporting documentation.

1-10 Five examples of specific operational audits that could be conducted by an

internal auditor in a manufacturing company are:

1. Examine employee time records and personnel records to determine

if sufficient information is available to maximize the effective use of

personnel.

2. Review the processing of sales invoices to determine if it could be

done more efficiently.

3. Review the acquisitions of goods, including costs, to determine if

they are being purchased at the lowest possible cost considering the

quality needed.

4. Review and evaluate the efficiency of the manufacturing process.

5. Review the processing of cash receipts to determine if they are

deposited as quickly as possible.

11.

1-7

1-11 When auditinghistorical financial statements, an auditor must have a

thorough understanding of the client and its environment, including knowledge

about the client’s regulatory and operating environment, business strategies and

processes, and measurement indicators. This strategic understanding is also

useful in other assurance or consulting engagements. For example, an auditor

performing an assurance service on information technology would need to

understand the client’s business strategies and processes related to information

technology, including such things as purchases and sales via the Internet.

Similarly, a practitioner performing a consulting engagement to evaluate the

efficiency and effectiveness of a client’s manufacturing process would likely start

with an analysis of various measurement indicators, including ratio analysis and

benchmarking against key competitors.

1-12 The four parts of the Uniform CPA Examination are: Auditing and Attestation,

Financial Accounting and Reporting, Regulation, and Business Environment and

Concepts.

Multiple Choice Questions From CPA Examinations

1-13 a. (1) b. (4) c. (1)

1-14 a. (3) b. (4) c. (1)

Multiple Choice Questions From Becker CPA Exam Review

1-15 a. (4) b. (3) c. (3)

Discussion Questions And Problems

1-16 a. Audit services are a form of attestation service, and attestation

services are a form of assurance service. In a diagram, audit

services are located within the attestation service area, and

attestation services are located within the assurance service area.

b. 1. (2) An attestation service other than an audit service

2. (2) An attestation service other than an audit service

3. (1) An audit of historical financial statements

4. (3) An assurance or nonassurance service that is not an

attestation service

5. (2) An attestation service other than an audit service

6. (2) An attestation service other than an audit service

7. (2) An attestation service other than an audit service

(Review services are a form of attestation, but are

performed according to Statements on Standards for

Accounting and Review Services.)

8. (2) An attestation service other than an audit service

9. (2) An attestation service other than an audit service

12.

1-8

11-16 (continued)

10. (2)An attestation service other than an audit service

11. (3) An assurance or nonassurance service that is not an

attestation service

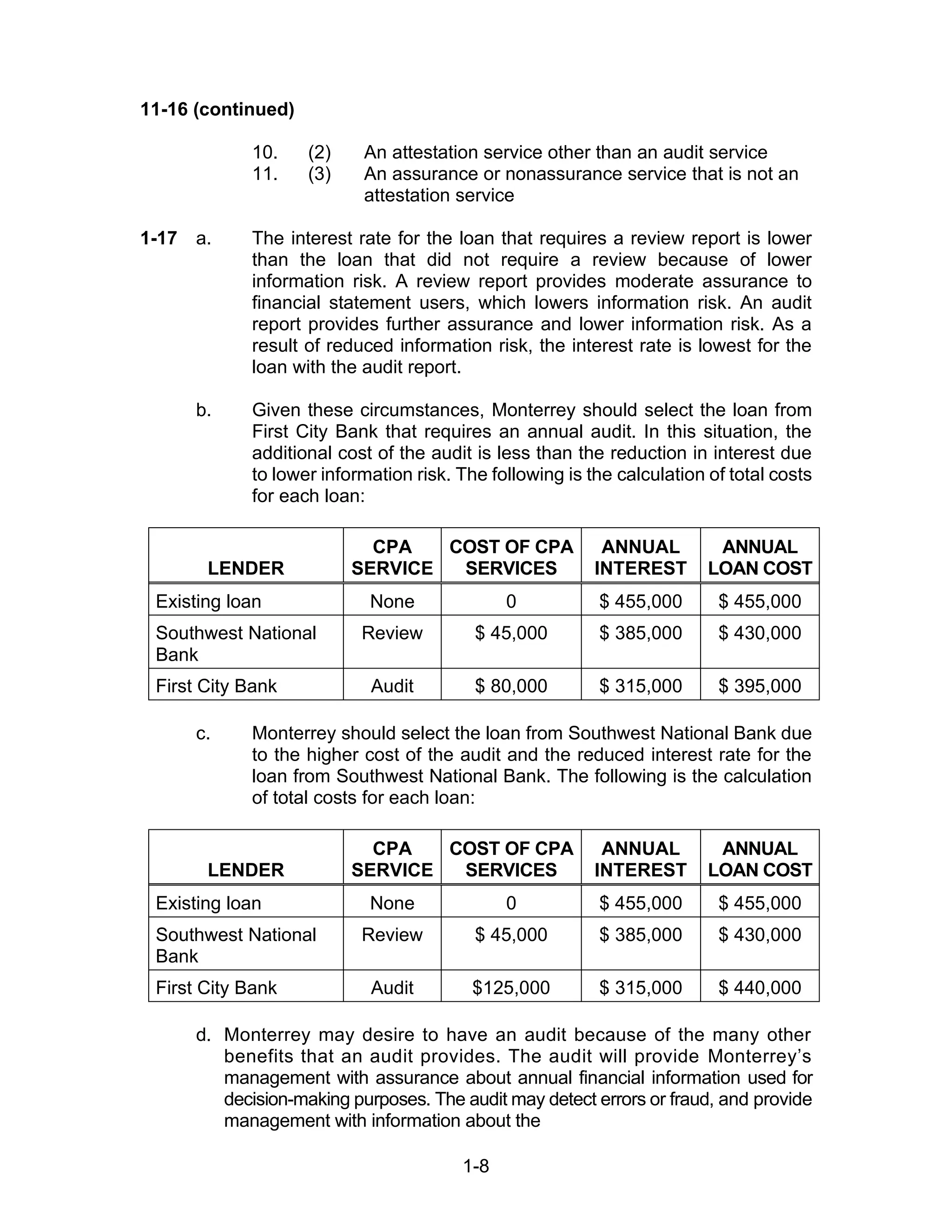

1-17 a. The interest rate for the loan that requires a review report is lower

than the loan that did not require a review because of lower

information risk. A review report provides moderate assurance to

financial statement users, which lowers information risk. An audit

report provides further assurance and lower information risk. As a

result of reduced information risk, the interest rate is lowest for the

loan with the audit report.

b. Given these circumstances, Monterrey should select the loan from

First City Bank that requires an annual audit. In this situation, the

additional cost of the audit is less than the reduction in interest due

to lower information risk. The following is the calculation of total costs

for each loan:

LENDER

CPA

SERVICE

COST OF CPA

SERVICES

ANNUAL

INTEREST

ANNUAL

LOAN COST

Existing loan None 0 $ 455,000 $ 455,000

Southwest National

Bank

Review $ 45,000 $ 385,000 $ 430,000

First City Bank Audit $ 80,000 $ 315,000 $ 395,000

c. Monterrey should select the loan from Southwest National Bank due

to the higher cost of the audit and the reduced interest rate for the

loan from Southwest National Bank. The following is the calculation

of total costs for each loan:

LENDER

CPA

SERVICE

COST OF CPA

SERVICES

ANNUAL

INTEREST

ANNUAL

LOAN COST

Existing loan None 0 $ 455,000 $ 455,000

Southwest National

Bank

Review $ 45,000 $ 385,000 $ 430,000

First City Bank Audit $125,000 $ 315,000 $ 440,000

d. Monterrey may desire to have an audit because of the many other

benefits that an audit provides. The audit will provide Monterrey’s

management with assurance about annual financial information used for

decision-making purposes. The audit may detect errors or fraud, and provide

management with information about the

13.

1-9

1-17 (continued)

effectiveness ofcontrols. In addition, the audit may result in

recommendations to management that will improve efficiency or

effectiveness.

e. The auditor must have a thorough understanding of the client and its

environment, including the client’s e-commerce technologies, industry,

regulatory and operating environment, suppliers, customers, creditors,

and business strategies and processes. This thorough analysis helps

the auditor identify risks associated with the client’s strategies that

may affect whether the financial statements are fairly stated. This

strategic knowledge of the client’s business often helps the auditor

identify ways to help the client improve business operations, thereby

providing added value to the audit function.

1-18 a. The services provided by Consumers Union are very similar to

assurance services provided by CPA firms. The services provided by

Consumers Union and assurance services provided by CPA firms

are designed to improve the quality of information for decision

makers. CPAs are valued for their independence, and the reports

provided by Consumers Union are valued because Consumers

Union is independent of the products tested.

b. The concepts of information risk for the buyer of an automobile and

for the user of financial statements are essentially the same. They

are both concerned with the problem of unreliable information being

provided. In the case of the auditor, the user is concerned about

unreliable information being provided in the financial statements. The

buyer of an automobile is likely to be concerned about the

manufacturer or dealer providing unreliable information.

c. The four causes of information risk are essentially the same for a

buyer of an automobile and a user of financial statements:

(1) Remoteness of information It is difficult for a user to obtain

much information about either an automobile manufacturer or

the automobile itself without incurring considerable cost. The

automobile buyer does have the advantage of possibly

knowing other users who are satisfied or dissatisfied with a

similar automobile, and the ability to perform online research

of new vehicles.

(2) Biases and motives of provider There is a conflict between

the automobile buyer and the manufacturer. The buyer wants

to buy a high quality product at minimum cost whereas the seller

wants to maximize the selling price and quantity sold.

(3) Voluminous data There is a large amount of available

information about automobiles that users might like to have in

14.

1-10

1-18 (continued)

order toevaluate an automobile. Either that information is not

available or too costly to obtain.

(4) Complex exchange transactions The acquisition of an

automobile is expensive and certainly a complex decision

because of all the components that go into making a good

automobile and choosing between a large number of

alternatives.

d. The three ways users of financial statements and buyers of

automobiles reduce information risk are also similar:

(1) User verifies information him or herself That can be obtained by

driving different automobiles, examining the specifications of the

automobiles, talking to other users and doing research in

various magazines.

(2) User shares information risk with management The

manufacturer of a product has a responsibility to meet its

warranties and to provide a reasonable product. The buyer of

an automobile can return the automobile for correction of

defects. In some cases a refund may be obtained.

(3) Examine the information prepared by Consumer Reports

This is similar to an audit in the sense that independent

information is provided by an independent party. The

information provided by Consumer Reports is comparable to

that provided by a CPA firm in an audit of financial statements.

1-19 a. The following parts of the definition of auditing are related to the

narrative:

(1) Altman is being asked to issue a report about qualitative and

quantitative information for trucks. The trucks are therefore

the information with which the auditor is concerned.

(2) There are four established criteria which must be evaluated

and reported by Altman: existence of the trucks on the night

of June 30, 2019, ownership of each truck by Regional

Delivery Service, physical condition of each truck and fair

market value of each truck.

(3) Samantha Altman will accumulate and evaluate four types of

evidence:

(a) Count the trucks to determine their existence.

(b) Use registration documents held by Burrow for

comparison to the serial number on each truck to

determine ownership.

(c) Examine the trucks to determine each truck's physical

condition.

(d) Examine the blue book to determine the fair market

value of each truck.

15.

1-11

1-19 (continued)

(4) SamanthaAltman, CPA, appears qualified, as a competent,

independent person. She is a CPA, and she spends most of

her time auditing used automobile and truck dealerships and

has extensive specialized knowledge about used trucks that

is consistent with the nature of the engagement.

(5) The report results are to include:

(a) which of the 25 trucks are parked in Regional's

parking lot the night of June 30.

(b) whether all of the trucks are owned by Regional

Delivery Service.

(c) the condition of each truck, using established

guidelines.

(d) fair market value of each truck using the current blue

book for trucks.

b. The only parts of the audit that will be difficult for Altman are:

(1) Evaluating the condition, using the guidelines of poor, good,

and excellent. It is highly subjective to do so. If she uses a

different criterion than the "blue book," the fair market value

will not be meaningful. Her experience will be essential in

using this guideline.

(2) Determining the fair market value, unless it is clearly defined

in the blue book for each condition.

1-20 a. The major advantages and disadvantages of a career as an IRS

agent, CPA, GAO auditor, or an internal auditor are:

EMPLOYMENT ADVANTAGES DISADVANTAGES

INTERNAL

REVENUE

AGENT

1. Extensive training in

individual, corporate, gift,

trust and other taxes is

available with concentration

in area chosen.

2. Hands-on experience with

sophisticated selection

techniques.

1. Experience limited to

taxes.

2. No experience with

operational or financial

statement auditing.

3. Training is not extensive

with any business

enterprise.

16.

1-12

1-20 (continued)

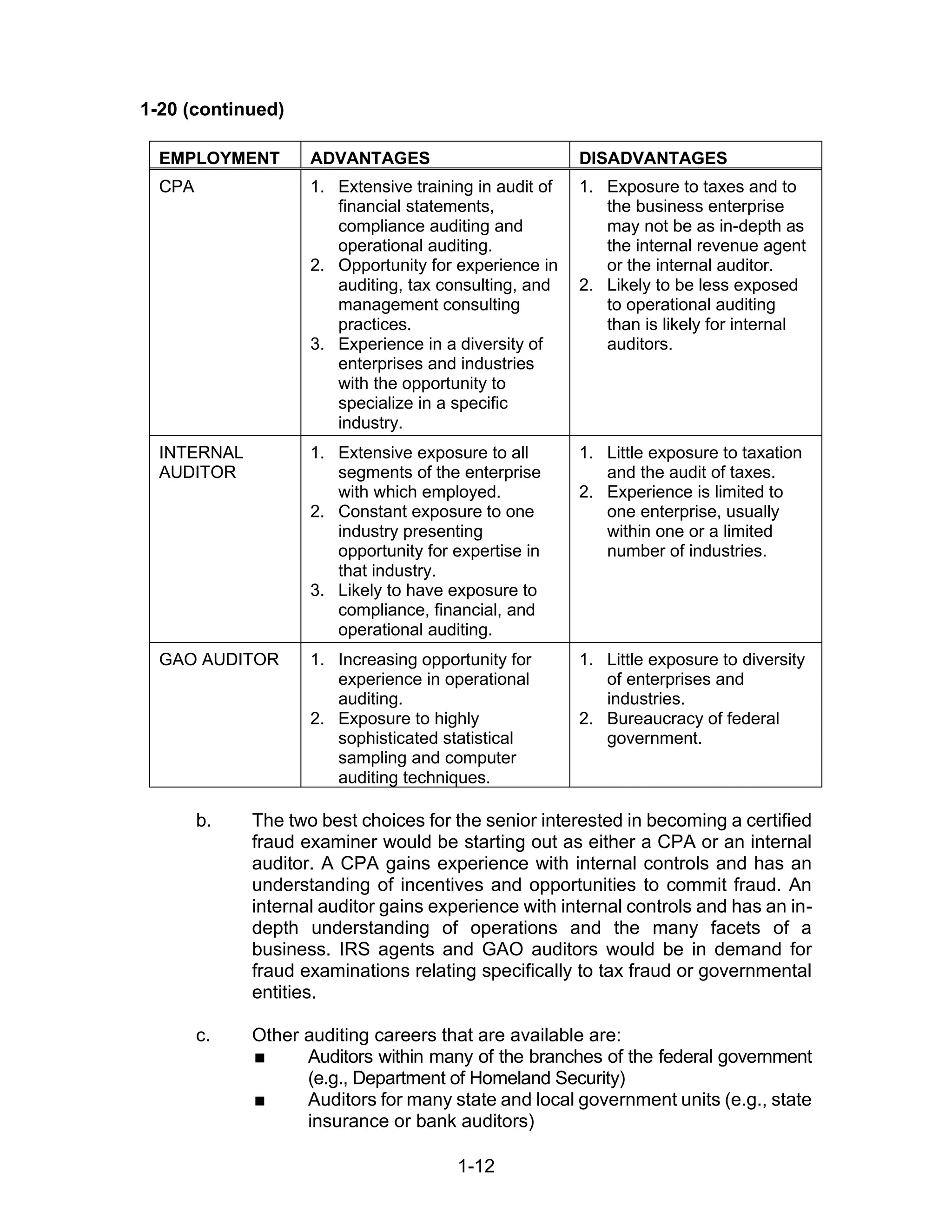

EMPLOYMENT ADVANTAGESDISADVANTAGES

CPA 1. Extensive training in audit of

financial statements,

compliance auditing and

operational auditing.

2. Opportunity for experience in

auditing, tax consulting, and

management consulting

practices.

3. Experience in a diversity of

enterprises and industries

with the opportunity to

specialize in a specific

industry.

1. Exposure to taxes and to

the business enterprise

may not be as in-depth as

the internal revenue agent

or the internal auditor.

2. Likely to be less exposed

to operational auditing

than is likely for internal

auditors.

INTERNAL

AUDITOR

1. Extensive exposure to all

segments of the enterprise

with which employed.

2. Constant exposure to one

industry presenting

opportunity for expertise in

that industry.

3. Likely to have exposure to

compliance, financial, and

operational auditing.

1. Little exposure to taxation

and the audit of taxes.

2. Experience is limited to

one enterprise, usually

within one or a limited

number of industries.

GAO AUDITOR 1. Increasing opportunity for

experience in operational

auditing.

2. Exposure to highly

sophisticated statistical

sampling and computer

auditing techniques.

1. Little exposure to diversity

of enterprises and

industries.

2. Bureaucracy of federal

government.

b. The two best choices for the senior interested in becoming a certified

fraud examiner would be starting out as either a CPA or an internal

auditor. A CPA gains experience with internal controls and has an

understanding of incentives and opportunities to commit fraud. An

internal auditor gains experience with internal controls and has an in-

depth understanding of operations and the many facets of a

business. IRS agents and GAO auditors would be in demand for

fraud examinations relating specifically to tax fraud or governmental

entities.

c. Other auditing careers that are available are:

Auditors within many of the branches of the federal government

(e.g., Department of Homeland Security)

Auditors for many state and local government units (e.g., state

insurance or bank auditors)

17.

1-13

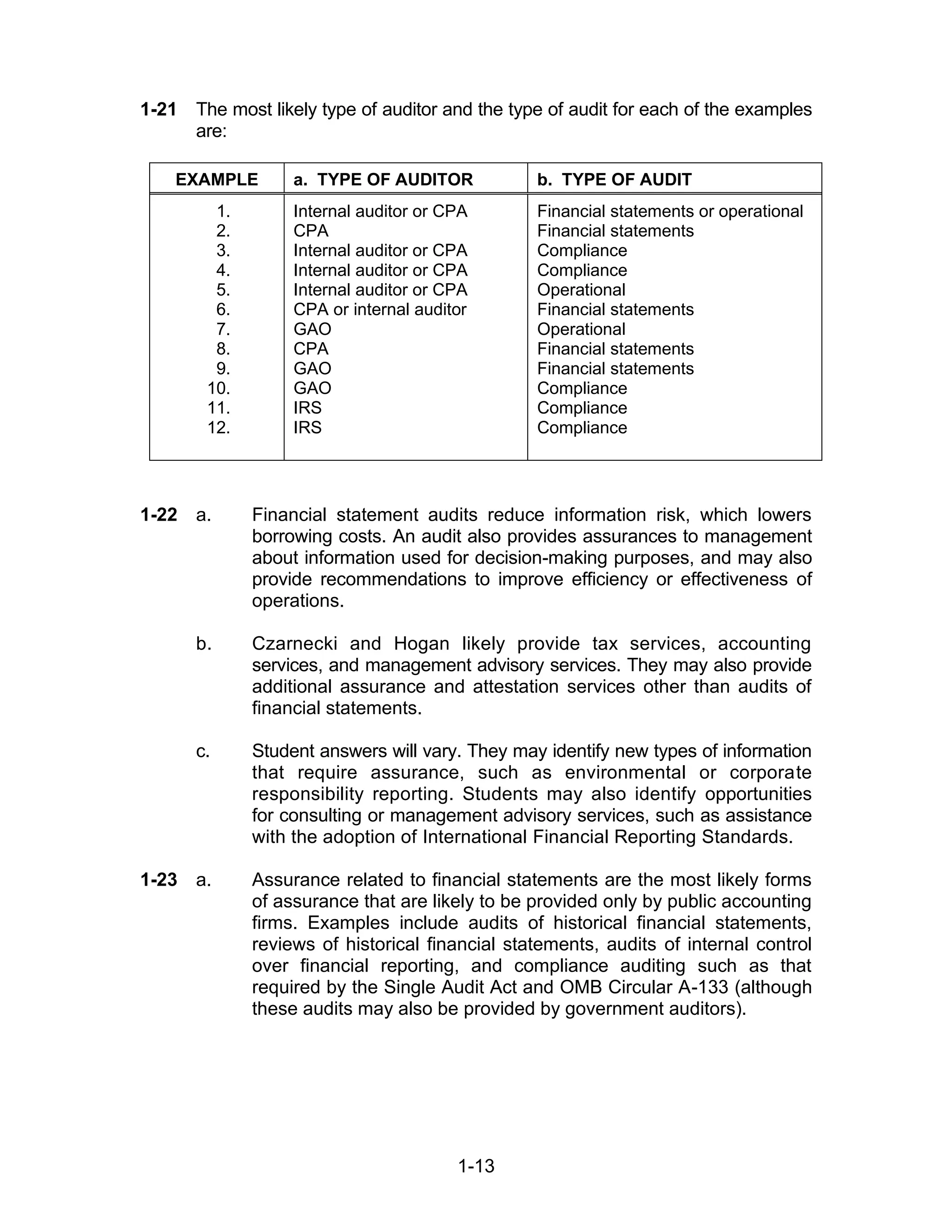

1-21 The mostlikely type of auditor and the type of audit for each of the examples

are:

EXAMPLE a. TYPE OF AUDITOR b. TYPE OF AUDIT

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

Internal auditor or CPA

CPA

Internal auditor or CPA

Internal auditor or CPA

Internal auditor or CPA

CPA or internal auditor

GAO

CPA

GAO

GAO

IRS

IRS

Financial statements or operational

Financial statements

Compliance

Compliance

Operational

Financial statements

Operational

Financial statements

Financial statements

Compliance

Compliance

Compliance

1-22 a. Financial statement audits reduce information risk, which lowers

borrowing costs. An audit also provides assurances to management

about information used for decision-making purposes, and may also

provide recommendations to improve efficiency or effectiveness of

operations.

b. Czarnecki and Hogan likely provide tax services, accounting

services, and management advisory services. They may also provide

additional assurance and attestation services other than audits of

financial statements.

c. Student answers will vary. They may identify new types of information

that require assurance, such as environmental or corporate

responsibility reporting. Students may also identify opportunities

for consulting or management advisory services, such as assistance

with the adoption of International Financial Reporting Standards.

1-23 a. Assurance related to financial statements are the most likely forms

of assurance that are likely to be provided only by public accounting

firms. Examples include audits of historical financial statements,

reviews of historical financial statements, audits of internal control

over financial reporting, and compliance auditing such as that

required by the Single Audit Act and OMB Circular A-133 (although

these audits may also be provided by government auditors).

18.

1-14

1-23 (continued)

b. Thereare many types of information that are assured by providers

other than public accounting firms. Some of these assurances are

provided by government entities, such as food inspections, elevator

inspections, and pumps at gasoline stations. Other assurances are

provided by nonprofit and for-profit assurance providers, such as ISO

9000 certifications.

c. Table 1-1 on p. 11 includes some examples of assurance that may

be provided by public accounting firms or other assurance providers.

For example, assurance on corporate responsibility and

sustainability may be provided by public accounting firms or other

assurance providers. Other examples included assurance on

website controls, and information such as website traffic or

newspaper circulation.

1-24 a. The vision of the Global Reporting Initiative (GRI) is a sustainable

global economy where organizations manage their economic,

environmental, social and governance performance and impacts

responsibly, and report transparently. Its mission is to make

sustainability reporting standard practice by providing guidance and

support to organizations.

b. According to the GRI “A sustainability report is a report published by

a company or organization about the economic, environmental, and

social impacts caused by its everyday activities. A sustainability

report also presents the organization's values and governance

model, and demonstrates the link between its strategy and its

commitment to a sustainable global economy.”

In an integrated report, sustainability information is included

along with financial information. These reports emphasize the links

between financial and non-financial performance. An integrated

report also presents the risks and opportunities the company faces,

integrated with disclosure of environmental, social, and governance

issues.

c. GRI offers two “in accordance” reporting options, Core and

Comprehensive. For each option, there is a corresponding claim, or

statement of use, that the organization is required to include in the

report. The Core report provides the essential elements of a

sustainability report. The Comprehensive report includes additional

disclosures of the organization’s strategy and analysis, governance,

and ethics and integrity. The GRI recommends external assurance,

but it is not required for either type of “in accordance” report.

19.

1-15

1-25 a. Answerswill vary by state. Most states require 150 hours of

education, with specific requirements for number of accounting hours

and credit hours in other subject areas.

b. Answers will vary by state. Many states require one or two years of

work experience gained in public practice, or possibly government,

academia or industry, depending on the state. In many states,

experience in industry or internal audit is sufficient, depending on the

type of work performed.

c. Most states have frequently addressed questions. Many of these

address education requirements, as well as information on how to

prepare for the exam, as well as information on applying for licensure.

d. The Elijah Watt Sells award program was established in 1923 by

the American Institute of Certified Public Accountants (AICPA)

to recognize outstanding performance on the Uniform CPA

Examination. The award is presented to candidates who obtained a

cumulative average score above 95.50 across all four sections of the

Uniform CPA Examination, completed testing during the previous

calendar year, and passed all four sections of the Examination on

their first attempt.

e. Passing information is available on the CPA Examination portion of

the AICPA web site. Recent passing rates have ranged from

approximately 42% to 60% across the four sections.

This pamphlet wasnot published until 1646 but seems to have been

composed about the year 1606[579]. The writer is a converted

highwayman who is anxious for the reformation of his fellow-sinners.

He states "that Beggerie and Theeverie did never more abound,"

and he complains that the branding and whipping parts of the

statutes are put in execution long before any place is provided

where the poor could have work. He thought that this was most

unfair to the vagrants for many of them would work if they could

and go voluntarily to workhouses if they were in existence. He

therefore urges the establishment of places where men could have

work in all the larger parishes of the kingdom[580].

Another pamphlet complaining of the bad execution of the law was

entitled "Greevous Grones for the Poore" and was published in 1622.

The writer of this states that "though the number of the Poore do

dailie increase all things worketh for the worst in their behalfe. For

there hath beene no collection for them, no not these seven yeares

in many parishes of this land especiallie in countrie townes; but

many of those parishes turneth forth their Poore, yea and their lustie

labourers that will not worke or for any misdemeenor want worke, to

begge, filtch, and steale, for their maintenance so that the country is

pittifully pestered with them[581]."

Another document of 1624 gives precisely the same information.

This is a letter from a Mr Williamson to Sir Julius Caesar, the Master

of the Rolls, who was one of the most charitably disposed gentlemen

of the time. The writer thinks the neglect of the overseers to

apprentice children is the true cause of vagrancy. He tells us that the

seventeenth century vagrant like the modern tramp was very seldom

a man who knew a trade[582]. The existence of these untrained men

was due to the fault of the administrators of the Poor Law. For these

"intollerable offences haue originally growen from the Ou(er)seers of

the poore who heretofore and att this day haue and doe so

ou(er)see as though they did not see at all[583]."

These writings would therefore lead us to believe that justices soon

grew careless; the poor were not relieved and in many places there

22.

was very littleexecution of the law at all. All these statements are

made by writers who are vigorously supporting only one side of the

case but the official evidence of the period confirms their view of the

matter. The reasons given for the appointment of the commission

suggested in 1619/20 show that the unofficial writers had not

exaggerated the existing neglect in the administration of the poor

laws. Good laws have been made but they are not executed because

the justices are negligent and the judges of Assize have not time to

fully investigate the matter. The laws in consequence "are in many

partes of our Realme laid aside or little regarded as lawes not in

force or of small consequence, whereas in some other counties and

partes of this kingdome in wch

by the diligence and industrye of

sume justices of the peace and other magistrates the said lawes

haue bine dulye putt in execucon there hath evidentlye appeared

much good and benefitt to haue redowned to the Comon welth by

the same[584]." At this time therefore there was a real likelihood that

the poor law would become obsolete.

However the season of scarcity in 1622-3 was accompanied by a

crisis in the cloth trade and the Privy Council was active in enforcing

measures of relief. A great improvement was consequently then

effected in the execution of temporary measures of corn relief, and

some reports indicate that this was accompanied by a better

administration of the ordinary poor law also.

Thus from Burnham in Buckinghamshire the justices report, "We

have alsoe looked into and have caused the poore to bee well

provided for in every parrish within this diuision both by stocks to

sett them on worke as alsoe by weekely contributions[585]." From

several of the hundreds of Suffolk there are similar reports. Thus in

every "towne" of Lackford and Exning the rates had been

augmented and the "poorer sorte of people within the seurall townes

and places are ordered to be sett on worke[586]." From other

districts in both East and West we have like accounts[587].

Between the years 1605 and 1629 therefore the administration of

poor relief was on the whole negligent and in many districts the poor

23.

6. Action ofthe

Privy Council and

administration

between 1629 and

1644.

6. a. State of affairs

in 1631.

law was already considered to be of little importance. The

government was however still anxious to secure its enforcement and

the measures taken to relieve distress in 1622-3 effected an

improvement in a few districts.

But from 1629 to 1644 we have a different state

of things. We know already that during this period

the action of the Privy Council was continuous and

constant, and it is in this period therefore that we

shall be able to see how far it was effective. The

justices' reports, to which we have already often referred are the

main sources of our information.

We will endeavour to see how far the evidence of the early part of

the period confirms the view we have already formed as to the

administration of the law at the beginning of the time, and we will

secondly try to estimate the evidence as to improvement during this

period.

The condition of affairs before 1631 is indicated by

the preamble to the commission of Jan. 1631/2

and by some of the earlier reports of 1631. The

reasons given for the appointment of the commission of 1631/2 are

almost exactly the same as those given in the draft of 1619/20. The

justices are said as before to be negligent so that the laws were

almost obsolete in some parts of the country, and this alone shows

that there had been little permanent improvement since 1620. The

preamble also refers to an earlier time "vpon the present making of

the said lawes," when they were duly executed and thus confirms

the evidence as to the good execution of the laws after 1597[588].

The justices' reports of 1631 give us more detailed information of

the same kind. One of these was sent from three of the hundreds of

Hampshire, Fawley, Bountisborough and Mainsborough. The justices

say that they sent an abstract of the act to the officials concerned

and ordered constables, tithingmen, and overseers to bring

presentments to them. But they "for the most parte" replied, "that

they haue noe poore that wanted worke or releife, that they had noe

24.

rogues but sucheas were punished." The justices thought this state

of things too good to be true; they made further enquiries and found

that the highways were out of repair, that no monthly meetings had

been held by the overseers and that there were no stocks for setting

the poor to work. They also heard that some of the poor were "in

noe small want" but did not complain because of ignorance or fear.

They hoped to effect improvement by exacting fines for negligence,

by publishing the particulars of their monthly meetings, and by

sending a series of definite questions to the overseers as to the

names of the poor relieved or set to work and of the children over

ten years of age who were not bound apprentice[589]. In this way

they tried to obtain detailed statements so that there could be no

evasion of the law. There is a later report from Fawley concerning

corn and apprentices, and the part of the law relating to apprentices

was certainly then carried out[590].

But there are other districts in which the justices do not tell us of

negligent officials, but rather seem proud of their vigour and yet

seem to imply that it was only recently the law had come into force.

This is particularly the case in Radnorshire and Cheshire. In two

divisions of Radnor the justices say they have appointed overseers,

and have given particular directions as to the provision of stocks and

return of the names of the poor relieved[591]. The reports suggest

that the justices were now energetic, but that little had been done

before; the mention of the appointment of overseers is

unaccompanied by the word new or by any statement as to the

rendering of the accounts of the old overseers, so that it is possible

that these were the first overseers appointed in that district.

In two of the divisions of Cheshire the same state of things is

implied more definitely. The justices say that they have ordered the

collection of a stock for the setting the poor to work and for the

relief of the impotent, but they find the people poor and averse to

paying money for any purpose of the kind. They fear some time will

elapse before these orders can be properly executed. At present

these divisions have not got a House of Correction, and the justices

wish to have one in the Castle in order that they may be able to

25.

6. b. Improvement

effectedin 1631

and 1632.

subdue the people to subjection[592]. These reports seem to reveal a

very primitive state of things, and recall the difficulties in the West

Riding of Yorkshire in 1597, when poor relief seems to have been

first enforced there, and the people greatly objected to the

imposition of rates.

Other reports show that the Book of Orders strengthened the hands

of reformers; thus in the town of Wells, charities had been

negligently administered, but after the issue of the orders the

Recorder was able to procure information formerly withheld, and

hoped to effect farther improvement by obtaining a commission of

charitable uses[593].

It is thus fairly clear that before 1631 the law had not been well

administered. We will now examine the evidence as to the

improvement between 1631 and 1640.

The greater number of the reports of 1631 and

1632 point to some execution of the law before

1631 and suggest improvement rather than entire

innovation. The justices generally state they have "raised rates" or

have bound many more children apprentices or that stocks had been

provided in the parishes where there were none before. Two reports

enable us to trace the process of improvement in detail, and seem to

throw considerable light on the general statements of other

documents of the kind. They do not however present so favourable a

view as to the execution of the law as most of the other returns.

These reports relate to the district of Braughing in Hertfordshire. The

overseers of thirteen places in the half hundred of Braughing made

returns to the justices at six successive monthly meetings held in

accordance with the provisions of the Book of Orders, between Feb.

7th and June 27, 1631. Abstracts of these returns were sent in by

the justices in two documents, one of which was forwarded in April

and the other in July 1631[594]. We can thus see exactly when the

improvement was effected. At the first meeting four parishes

provided corn at reduced rates for the poor. The Book of Orders

relating to scarcity had been issued since September, and we should

26.

expect some improvementwould already have been made. Six sets

of overseers had already placed some children apprentices, but not

very many, and only two of the largest places had stocks for setting

the poor to work. At the last meeting on June 27th relief was much

more extensively administered. Two other places provided corn at

reduced rates: the six parishes which formerly had placed a few

apprentices now bound many more, while five other townships also

provided for the children in this manner. A much better provision for

the employment of the poor was also made. In five places instead of

two there were now stocks for this purpose and most of the others

give reasons for the want of one. In three cases we are told there is

plenty of employment, at Eastwick the inhabitants set the poor to

work, and at Westmill the general statement only is made that the

poor are relieved according to their necessities. Three places do not

provide stocks or give any reason for not doing so. We can also see

that these funds might often have disappeared, for the ten pounds

stock at Hunsdon had "decayed" to only five pounds at the end of

the period. In the district of Braughing therefore the law was

executed in the larger places before 1630 but negligently even there.

Immediately however after the receipt of the Book of Orders the

justices set themselves to work, held the monthly meetings,

stimulated the overseers, and in five months succeeded in effecting

a very considerable improvement.

This was only typical of what was going on all over the country. It is

of course impossible to quote all the reports of the period; it is only

possible to give particular cases, and to state that they are not

isolated instances, but are typical of the documents of that time.

Thus in April, 1631, we hear that meetings had been rapidly held

and that they had been partially successful, but that the justices

were still in the midst of their activity; they had done a good deal to

make matters better and were still doing more. For example in the

account sent from the New Forest the justices write "the rates for

the poore where neede most requireth wee haue caused to be rised

for reliefe of the poore people wth

in that part, and haue given strict

order to the ouerseers for providing necessary releife for such as are

27.

6. c. Improvement

maintainedbetween

1631 and 1640.

ympotent and such as are able to sett them to worke, and haue

alreadie placed many poore children apprentizes and doe proceede

in placinge of more[595]."

In the returns sent later in the year the organisation appears to be

more settled and we hear that not only the rates are raised but that

they have had a good effect. Thus in Monslow in Shropshire the

justices state "and as for the late booke of orders for the reliefe of

the poore and the punishing of rogues and vagabonds wee have had

severalle monthlye meetings in the said hundred and wee have long

since worked such effect thereby as they have not any rogues or

vagabonds appeared amongst vs or walked abroade as wee can

heare of since our first meetings, and the impotent poore are

relieved in such sort by their parishoners as wee have noe

complaints and there are stocks in all parishes more or lesse as the

charge of the parishes require to set the able poore on worke[596]."

Not all the reports are as favourable as this, but on the whole they

indicate that improved order followed the execution of the Book of

Orders. It thus is clear that the Orders of 1631 had a very

considerable immediate effect both in bringing the law into operation

in places where it had been almost or altogether neglected and still

more in improving the administration in those districts in which the

system was already to some extent administered though not yet

effectually.

We have now to see whether this improved

administration was maintained. The reports are

certainly less frequent after 1631 but those that

remain shew that the efficiency is preserved and there is much to

indicate a farther improvement.

We will first examine a few documents which seem to indicate that

the area of administration was extending into backward districts, we

will then investigate a few cases in which we have reports both in

1631 and in 1638 or 1639, and we will lastly consider a special

department of the poor law system, namely the placing of

apprentices.

28.

We have alreadynoted the fact that in the earlier years of the period

there were few reports from Westmoreland and Lancashire.

But in 1638 there are a series of documents from Westmoreland[597]

and several reports from Lancashire. In 1638 some of the Lancashire

parishes adopted the system of billeting the poor in need of relief on

the richer inhabitants. This plan does not seem to have long

continued as an exclusive system of relief, and the facts that it was

still employed and that these are the earliest reports from

Westmoreland seem to indicate that a compulsory system of poor

relief had only lately been established in the northern counties.

Moreover in 1637 we are told that at the meeting of the justices in

Rochdale in Sept. 1637, the churchwardens of Middleton confessed

that they had never before levied a tax for the relief of the poor

there; they now however proceeded to levy one, and in March in the

following year the tax provided the necessary relief[598]. All this

seems to show that the area of the administration of the poor law

was extending and that in 1638 there was little danger of the system

of poor relief becoming obsolete but that it was obtaining a firmer

hold over the country.

We will now examine a few of the cases in which we have reports

from the same district both in 1631 and 1638 or 1639. We have

already noted the detailed returns from Braughing. It happens that

one of the latest documents of the series returned in August 1639

comes from the hundreds of Hertford and Braughing. The justices

tell us that our "ympotent poore are weekelie releiued by a certein

pencon and the rates increased as necessitie requires. And those of

able bodies are plentifullie stored with work for the maynteynance of

their families"; five apprentices had also lately been bound[599].

From this we see that the improved administration there lasted

throughout the period.

We have several other places from which we have similar reports.

Skenfreth, one of the hundreds of Monmouth, often sent accounts of

the proceedings of the justices. One belongs to May, 1631. The

justices state some of the things they did both before the

29.

Commission and afterwards.Before the Commission they provided

weekly stipends for all the aged and impotent people, "sithence the

said commission" they "have taken order that the same stipends

shalbe contineually paied soe that none of any such poore people

have made any complaint unto us for any mainetenance." Both

before and after the commission they had punished rogues and

since they had also placed apprentices and suppressed alehouses.

Moreover the highways had been last year in better condition than

for twenty years before[600].

Thus the immediate improvement effected by the commission was

that the pensions were paid as well as ordered, apprentices were

bound and alehouses suppressed.

In May, 1637, we have a report from the same district together with

the hundreds of Ragland and Trellech. At that time apprentices were

bound, rogues punished and efforts made to secure the observance

of fasting days. The justices have also "taken course for provision of

stock to sett the poore on worke," and have "caused to be

sufficiently relieved all the aged lame and ympotent people[601]."

Thus if these documents are to be believed the improvement

effected in 1631 was maintained and even increased in this hundred

of Skenfreth.

There are many other cases in which reports are sent in several

times from the same place and all show that the improvement made

in 1631 was continued in 1637, 1638 or 1639[602].

We will now examine a few of the reports which relate especially to

the placing of apprentices. Before May 1635 the Privy Council or the

commissioners seem to have urged the justices to see especially that

this part of the law was carried out, and to have asked them to

report the names of the apprentices and those of their masters[603].

The reports sent in 1634 and 1635 therefore relate especially to the

placing of apprentices and the monthly meetings of the justices.

Reports from twenty-one places were sent in between July 17th and

July 31st, 1634. In almost every case the justices expressly state

30.

that they holdmonthly meetings and bind poor children

apprentice[604]. In the year 1635 the statements are more detailed.

Between May 20th and May 30th replies were sent from ten places

in eight of which the names of both apprentices and masters were

given[605]. Sometimes these were numerous; thus at Blandford in

Dorset one hundred and nineteen apprentices were bound in the

course of two years[606]; in one district of Somerset the names of

one hundred and sixty-six are returned[607], while in all ten districts

a fair amount of work was done. Thus in 1634 and 1635

apprenticeship was more insisted upon than other methods of poor

relief and it seems to have been very generally well administered.

We hear of some complaints but not many in proportion to the

number of reports.

We thus see that during the years 1630 to 1639 we have a large

amount of information concerning the administration of the Poor

Law. We find that a great improvement was effected in 1631. We

also find that the area of administration continued to extend into the

Northern counties after 1631: the difference is indicated by the fact

that in 1638 it is exceptional to find a place without a poor rate,

whereas in 1631 the Government spoke of the laws as being almost

obsolete in many places. We see further that sometimes the later

reports come from the same places as the earlier, and that then the

administration continues to be reported as good. Lastly, in regard to

apprentices we are told that the Privy Council made special efforts to

enforce the law, and that all over the country there is evidence that

it was enforced though occasionally without favourable results.

There is thus reason to believe that the efforts made by the central

government to enforce the law were at last successful, and that the

period to which we owe the survival of our English system of poor

relief is that of the personal government of Charles I.

But we have already noticed that not only is this period the critical

time in the history of the poor relief that survived, but in one respect

the poor relief of this period was unique. Many efforts were made to

find work for the unemployed. Relief of this kind was so much a part

31.

7. The improvement

effectedin 1631

especially

concerned the

unemployed.

of the general system of the time that we have already examined

many instances in which it was administered.

We will first investigate a few more of the reports of 1631, and we

shall find that the improvement effected in all parts of the

administration of poor relief especially concerned the relief of the

ablebodied; we will then examine a detailed report in order to see

what light it throws on the interpretation of the general statements

of other justices, and we will lastly try to find out if relief of this kind

was confined to a few districts, or was administered all over the

country, and also in what parts of the country there was the greatest

need of employment.

To begin with cases in which improvement was

reported in April 1631. From a large district of

Hertfordshire we hear "we haue already raysed a

stocke in some parishes, and are raysing stocks

for the rest to sett all the poore on worke in this

division[608]." In Essex, Richmond, Bedford and Beverley fresh taxes

for this purpose had just been raised, and at Agbrigg they were still

"setlinge such a course for raysinge of stocke to sett ye

people of

able bodies on work[609]."

At Winchester the same thing is implied: the stock has been put in a

clothier's hands, so that now the poor do not want work[610].

Twenty-eight reports relating not only to measures for corn, but also

for the poor were sent in between April 21st and April 30th 1631. In

seventeen of these the poor were set to work, and in many cases we

can see that the measures have been taken since the receipt of the

Book of Orders of January 1631/2[611].

In the answers sent in May we have the same kind of information. In

Brixton and Wallington we have a report similar to that from

Hertfordshire; "stockes of mony," we are told, "are raised in moste of

the parishes wth

in the said hundrede and burrow and the reste not

yet raised are wth

as much expedicon as may bee to bee raised for

buyinge of flax, hempe and other materialls to set the poore to

32.

8. The detailed

reportfrom

Bassetlaw throws

light upon the more

general statements

of the justices.

worke[612]." From Arundel there is a like account, "we haue caused

the taxations for the releefe of the poor to be raised in euery parish

in this time of scarsitye, and haue likewise caused stocks of mony to

be raised in euery parish to buy materialls to sett the poor a warke,

and we haue caused the Statute of Laborors to be inquired after and

to be putt in execution[613]."

We can thus see that in 1631 the justices were busy raising stocks to

provide work for the poor, and that in seventeen documents, or

more than half of the reports of the last ten days of April 1631, we

are informed that measures had been taken with this object.

We will now examine a more detailed report

relating to sixty parishes of Bassetlaw in County

Nottingham and sent in during March 1636/7[614].

In most cases information is given under four

headings, first we are told how many of the

impotent poor are relieved, secondly the amount

of the town stock, thirdly how many rogues have been punished,

and lastly how many apprentices have been bound. This document is

important because it seems to indicate the number of parochial

officials who provided work for the unemployed in the district of

Bassetlaw. This is not directly stated in the report, but the overseers

return the amount of the town stock of their parish whenever a town

stock existed. From the method in which the return is made it seems

that this town stock was always used for finding employment for the

able-bodied poor[615]. Other methods of dealing with those out of

work are also noted, so that it appears that in forty-five out of sixty

parishes the parochial authorities provided employment for those

poor who could work. The amount of the stock was often quite

small; in one case only sixteen shillings, but it is very possible that in

this instance the parish also was small; in another place the stock

consisted of a sum of about thirty pounds, and the average amount

was about three pounds. This document from Bassetlaw only states

in detail what many of the other reports imply, but the detail is much

more convincing, and it is confirmed by the overseers' accounts from

Barnet and Elstree which we have already examined[616]. It is

33.

9. Local variations

inthe provision for

the unemployed.

a. Not so extensive

in the parts North of

the Humber and in

the extreme West.

9 b. Provision of

work more

necessary in the

towns than in the

country.

perhaps worth while to notice that as early as 1623 the justices

wrote from Bassetlaw that work for the poor was wanting, and they

even then ordered that the labourers should be set to work by the

town's stock and the impotent relieved by the public

contribution[617].

We have now to try to find out if

it was only in a few counties

that work was found for the

unemployed, or if it was all over England. We have

already noted that in the counties north of the Humber, and in the

three western counties of Devonshire, Cornwall, and Wiltshire the

poor law was apparently less well administered than in other parts of

the country. In these counties with the exception of Yorkshire

therefore there are few instances in which stocks are found for

providing work for the unemployed. We hear however that in

Ashton-under-Line there existed a "small stocke of money which is

disposed on for the setting of poore to worke[618]". Moreover, in two

Yorkshire reports of 1635 it is stated that the justices have been

"verie carefull to raise stockes for setting our

poore on worke[619]."

There are other Yorkshire returns containing information of the same

kind, but still the plan of finding work for the unemployed of the

North seems to be comparatively unusual.[620]

But with regard to the rest of England this is not the case. In every

county except Northampton some justices state that they have

found employment for the poor. As we might expect this was done

most frequently in the towns and in the manufacturing counties,

both because in these places there were more rich people and

because there were also more unemployed owing to the greater

fluctuations of trade.

A report from Reading and Theale illustrates this:

"Wee finde that the able poore in boddy to worke

and wch

are in country villages and hambletts

haue theire ymploymt in husbondrie and by that

meanes are mayntayned; other lyen in such

34.

countrie townes, populer,incorporate, where heretofore multitudes

of such able persons haue lived by worke from the clothier, now

through the defect and decaye of that trade and soe consequently of

the clothier, thousands of these poore formerlie relieved by worke

liue in much want and could hardlie subsist this deere yeare did not

many extend theire charity even beyond their meanes[621]."

Newbury and Abingdon were also towns in the same neighbourhood

subject to similar conditions, and we know already that workhouses

were founded in both these places and in Reading itself also[622].

Shrewsbury and Hereford are fair examples of more westernly

towns. At Shrewsbury the justices report in June 1631 that they "are

aboute a course to sett all the poore on worke within our Towne and

Libertyes[623]," and in 1638 an order was made for regulating a

workhouse there[624]. About the same time the Mayor of Hereford

records that "there is a colleccon made in euerie severall parish wth

in

the said Cyttie, and competent somes raysed for to releive the

impotent and needy, and a stocke for the setting of poore able

people to worke and for the placeing of youth apprentices[625]."

Other magistrates report in like manner: thus in the rape of Hastings

they have caused the officers "as much as in them lyeth to see the

said poore inhabitants bee duely kept to worke and haue fitting

materialls provided for them[626]." In the hundred of Hertford the

justices state in 1631 that the more populous places have already

raised stocks of money to set the poor to work, and that they are

still trying to induce all the others to do so though a few are not rich

enough to bear the necessary taxation[627]. From St Albans, Reigate,

Ipswich, Maidstone, Lynn, and Norwich, as well as from more inland

towns we have similar information: the magistrates of Bedford write

that "we haue raysed divers extraordenary taxes for the reliefe of

our poore and settinge them on worke and therby they are set to

worke[628]." But perhaps the Buckingham report indicates the most

thorough organisation. There the poor had been visited apparently

in the same way as at Norwich. Five hundred people were examined;

the age and occupation of each were noted, and whether they had

work or not. Afterwards employment was provided for those who

35.

(d) Provision of

workin many

districts in most

counties of the

east.

needed it and we are told that the poor "of good disposicon are glad

they are thus settled wth

out begging and settle themselves seriouslie

to their labor

." This good result however was not obtained without

complaints from the ratepayers[629].

In the country districts also employment seems to have been

provided as well as in the towns whenever the poor suffered much

from the want of work. In the western counties, however, there were

few complaints of lack of employment, except from the cloth-

workers when the trade in cloth was slack. Some justices expressly

state that there is no want of work in their part of the country. Thus

from a large district of Somerset we hear that there are "none lefte

unplaced but such as doe mainetaine their charge by their

labor[630]." Therefore, as we should expect, in many reports from

the West nothing is said about finding employment for the able-

bodied poor. There are, however, also a fair number of cases in

which work is said to be provided. This is especially the case in the

counties of Shropshire and Stafford; thus from Staffordshire three

reports were sent in 1634, and in all three we are told that the poor

were set to work[631]. Moreover, the Worcester justices write that

"wee are carefull ... that the able poore bee well provided of

worke[632]" and in almost all[633] the other western counties, at

least one instance of the kind is reported[634].

But in the east and south-east there was at any

rate sometimes a chronic want of employment,

and consequently numerous efforts to provide for

the able-bodied poor. In the country round

Hitchen we are told, as in the Reading district,

that it is the poor in the town that are distressed, but in the hamlets

the farmers find work for the inhabitants. The justices say they have

no manufacture, and they do not know how to find a remedy for the

people in the town. At one time they make the richer people employ

the poor, but they do not find the experiment successful[635]. We

have also an account of a permanent want of employment in a large

district of Norfolk. In the hundreds of South Greenhoe, Wayland, and

36.

10. Summary.

Grimshoe provisionhad been made by raising a stock to set the

able-bodied poor to work, and besides the magistrates write, "Wee

have manie young people wch

live out of service by reason of the

multitude of them, there not being services for them, but worke is

provided for them in their seuerall parishes[636]."

There are very many reports of stocks for the provision of work in

other country districts of the east. In Hertfordshire, Suffolk, Norfolk,

and Cambridge there is much to make us think the system was

nearly general[637], and in each of the other eastern counties there

are many cases of the kind.

In a district of Middlesex the unemployed were sent to fight for

Gustavus Adolphus[638], but in most parishes materials were

provided for them to work up. Thus in several hundreds in Kent

"stocks of materialls" were provided in every parish[639]; in

Nottinghamshire those out of service and able to work were set to

work "on the towne stock[640]," while at Horncastle sessions, in

Lincolnshire, the justices take "special care ... that the abler sort bee

constantly sett on worke by the stocke of the parishe[641]."

Sometimes the sum expended was very considerable if we take into

account the great difference in the value of money. Thus in

Wallington, Surrey, more than £120 was used for providing work,

while nearly fifty pounds remained in hand[642]. On the whole

therefore in the eastern counties, between 1631 and 1640, it seems

that considerable sums of money were raised and employed in most

districts[643] with the object of setting to work the able-bodied poor.

We have thus seen that in 1631 the improvement

in the administration of poor relief concerned

especially the relief of the able-bodied poor, and we have noted

many instances in which taxes were raised for this purpose at that

time. We have also examined a detailed report from a particular

district in the county of Nottingham in which in forty-five out of sixty

parishes some provision seems to have been made for finding

employment for the poor. Moreover, we find that the plan of

providing work for the unemployed was reported from some district

37.

of every countysouth of the Humber except Cornwall, Northampton,

Devon, and Wilts; and in Devon and Wilts also the same plan was

tried, although no report of the justices has been preserved. This

form of poor relief thus seems to have been frequently in use in the

towns of both east and west, and in the country districts of the

eastern counties also. It was not quite so general in the country

districts of the west, but still was not infrequent even there.

We may, therefore, say that from 1631 to 1640 we had more poor

relief in England than we ever had before or since. We shall try to

estimate later how far this system was successful. But we will now

see what happened to the organisation of English poor relief during

the Civil War. We will also trace the history of poor relief in France

and Scotland during the sixteenth and seventeenth centuries, in

order that we may see that the history of poor relief in England is

unique.

39.

CHAPTER XIII.

POOR RELIEFIN FRANCE, SCOTLAND, AND

ENGLAND DURING THE CIVIL WAR AND

COMMONWEALTH.

§ 1. Lax administration of poor relief in

England during the years of Civil War.

a. Decline of charitable institutions.

b. Neglect in execution of ordinary law.

c. Instances of corrupt practices.

§ 2. Attempts to regain a good

organisation of poor relief under the

Commonwealth.

§ 3. Reasons why disorganisation

especially affected the provision of

work for the unemployed.

§ 4. State of poor relief after the

Restoration.

§ 5. Reasons for failure under the

Commonwealth to restore the old state

of things.

§ 6. History of legislation on poor relief in

Scotland,

a. Before 1597.

b. Between 1597—1680.

§ 7. Failure of administration of poor relief

in Scotland during the seventeenth

century.

40.

a. Responses ofthe Scotch justices to

the orders of Council in 1623 show

that they were unable or unwilling to

enforce the poor law themselves and

left it to the kirk sessions.

b. Inadequate poor relief granted by the

kirk sessions of Banff.

c. Relief of the poor in Aberdeen shows

that the relief considered sufficient

by the municipal rulers was double

that which could be granted from the

funds at the disposal of the kirk

sessions.

d. Infrequency of assessment in

Scotland before 1818.

e. Insufficiency of relief during the years

1692-1699.

f. Prevalence of begging in Scotland.

g. Reasons for the failure of Scotch

administration.

§ 8. The history of poor relief in France.

§ 9. Comparison between the history of

poor relief in England and that in

France and Scotland.

The histories of poor relief in England after the Civil War, and in

France and in Scotland throughout the sixteenth and seventeenth

centuries, both compare and contrast with the history of English

poor relief in the period from 1529 to 1644. While in each of these

cases like circumstances produced similar attempts to afford relief, in

none did both an energetic Privy Council and a vigorous system of

local officials coexist, and consequently in each case poor laws were

in existence but were badly administered. The course of events in all

these instances will therefore confirm the view that the survival of

the English system of poor relief is owing to the organisation which

41.

Welcome to ourwebsite – the perfect destination for book lovers and

knowledge seekers. We believe that every book holds a new world,

offering opportunities for learning, discovery, and personal growth.

That’s why we are dedicated to bringing you a diverse collection of

books, ranging from classic literature and specialized publications to

self-development guides and children's books.

More than just a book-buying platform, we strive to be a bridge

connecting you with timeless cultural and intellectual values. With an

elegant, user-friendly interface and a smart search system, you can

quickly find the books that best suit your interests. Additionally,

our special promotions and home delivery services help you save time

and fully enjoy the joy of reading.

Join us on a journey of knowledge exploration, passion nurturing, and

personal growth every day!

testbankbell.com

![This pamphlet was not published until 1646 but seems to have been

composed about the year 1606[579]. The writer is a converted

highwayman who is anxious for the reformation of his fellow-sinners.

He states "that Beggerie and Theeverie did never more abound,"

and he complains that the branding and whipping parts of the

statutes are put in execution long before any place is provided

where the poor could have work. He thought that this was most

unfair to the vagrants for many of them would work if they could

and go voluntarily to workhouses if they were in existence. He

therefore urges the establishment of places where men could have

work in all the larger parishes of the kingdom[580].