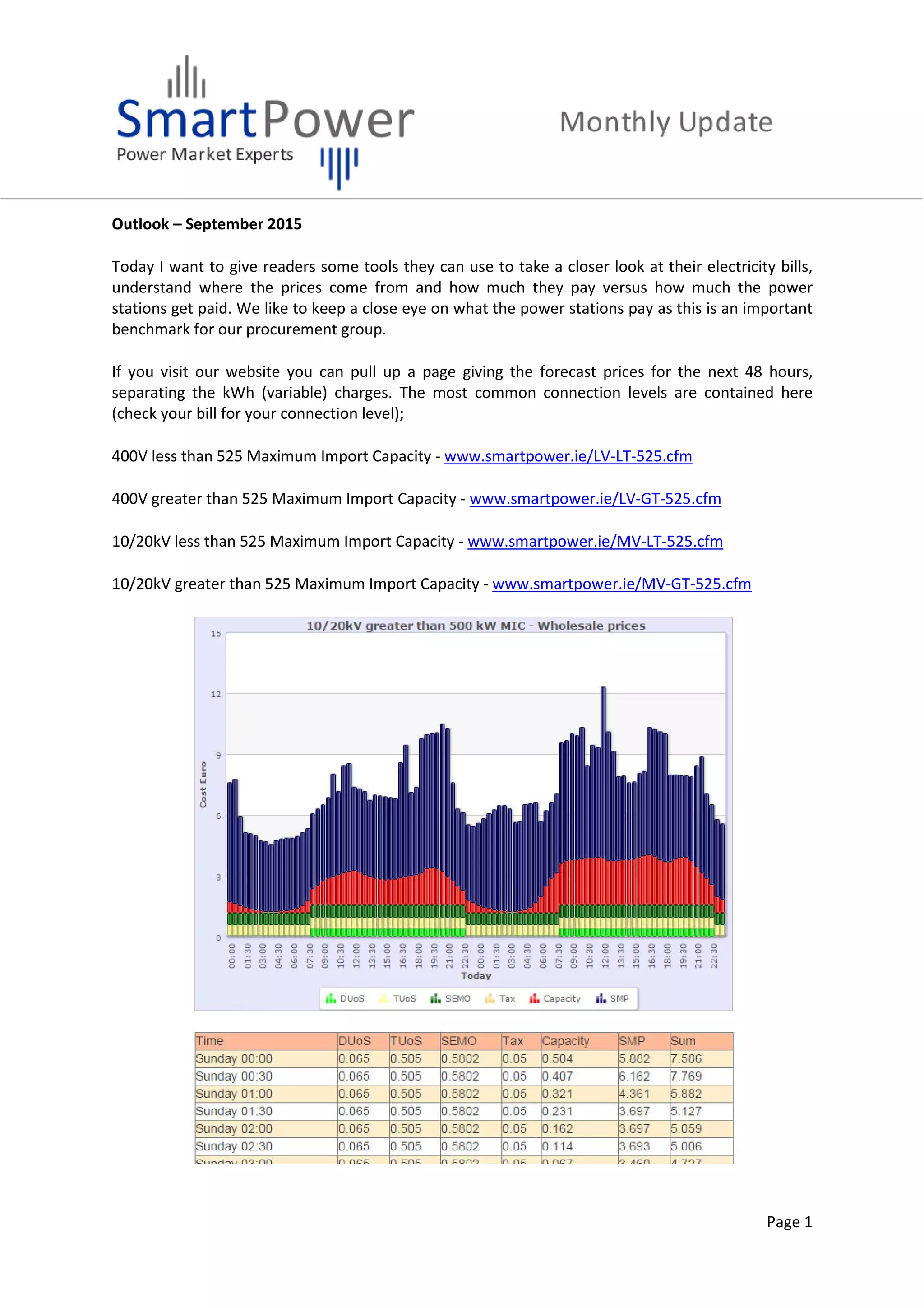

This document provides an overview of Ireland's electricity market and bills, including how power station prices are set half-hourly and impact variable consumer charges. It also discusses factors influencing the Public Service Obligation levy, outlook for weak global energy prices, trends in Irish wholesale electricity prices, and services offered by SmartPower to help businesses optimize electricity procurement and generation.