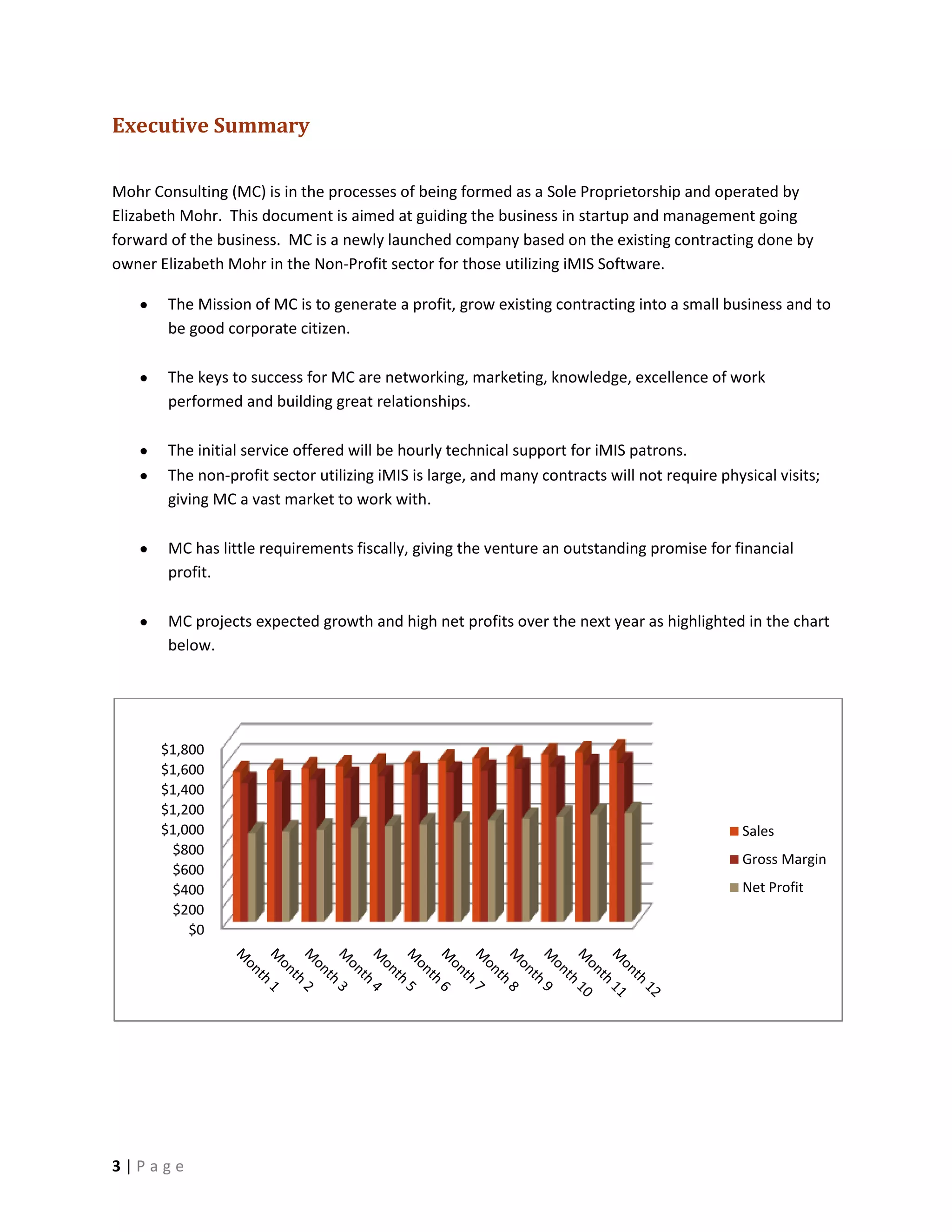

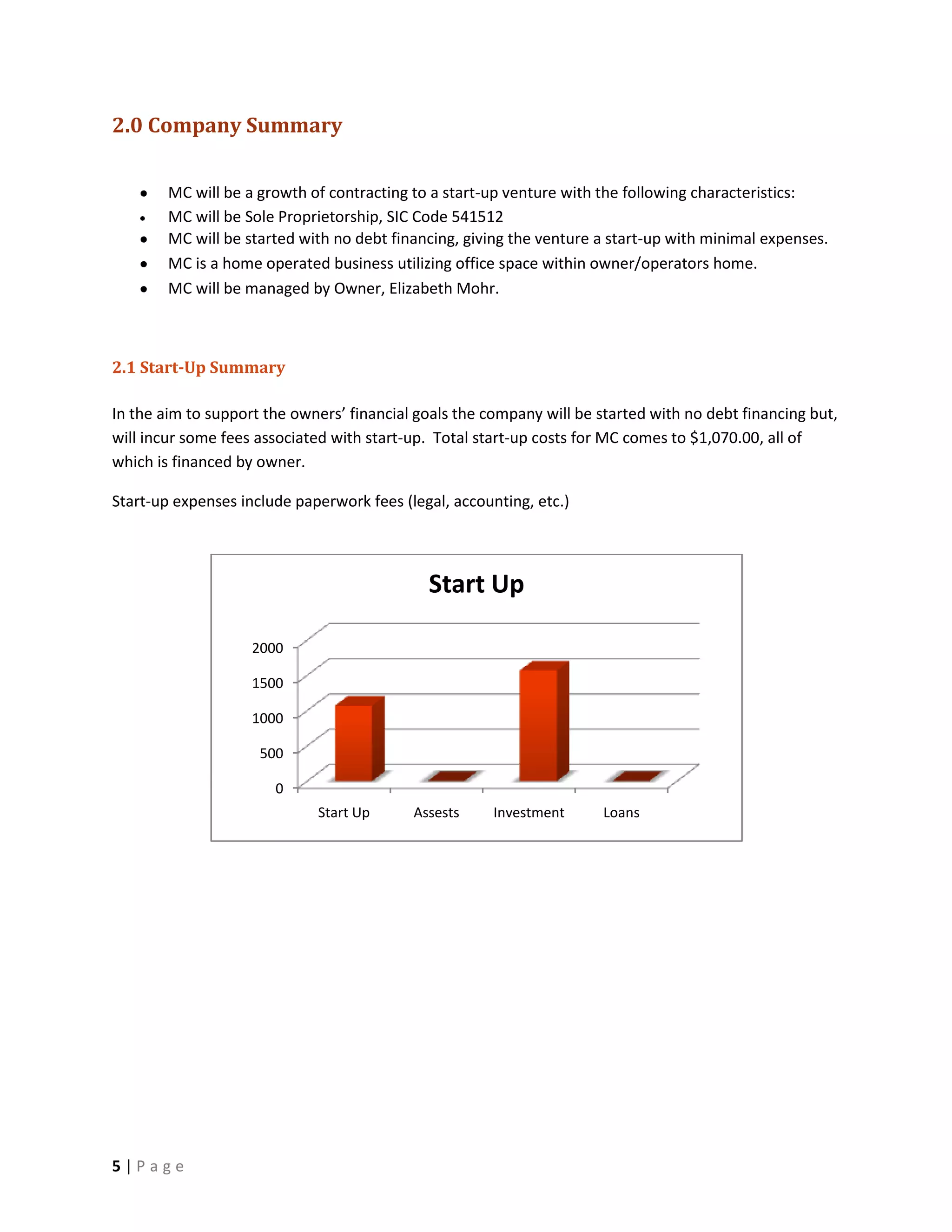

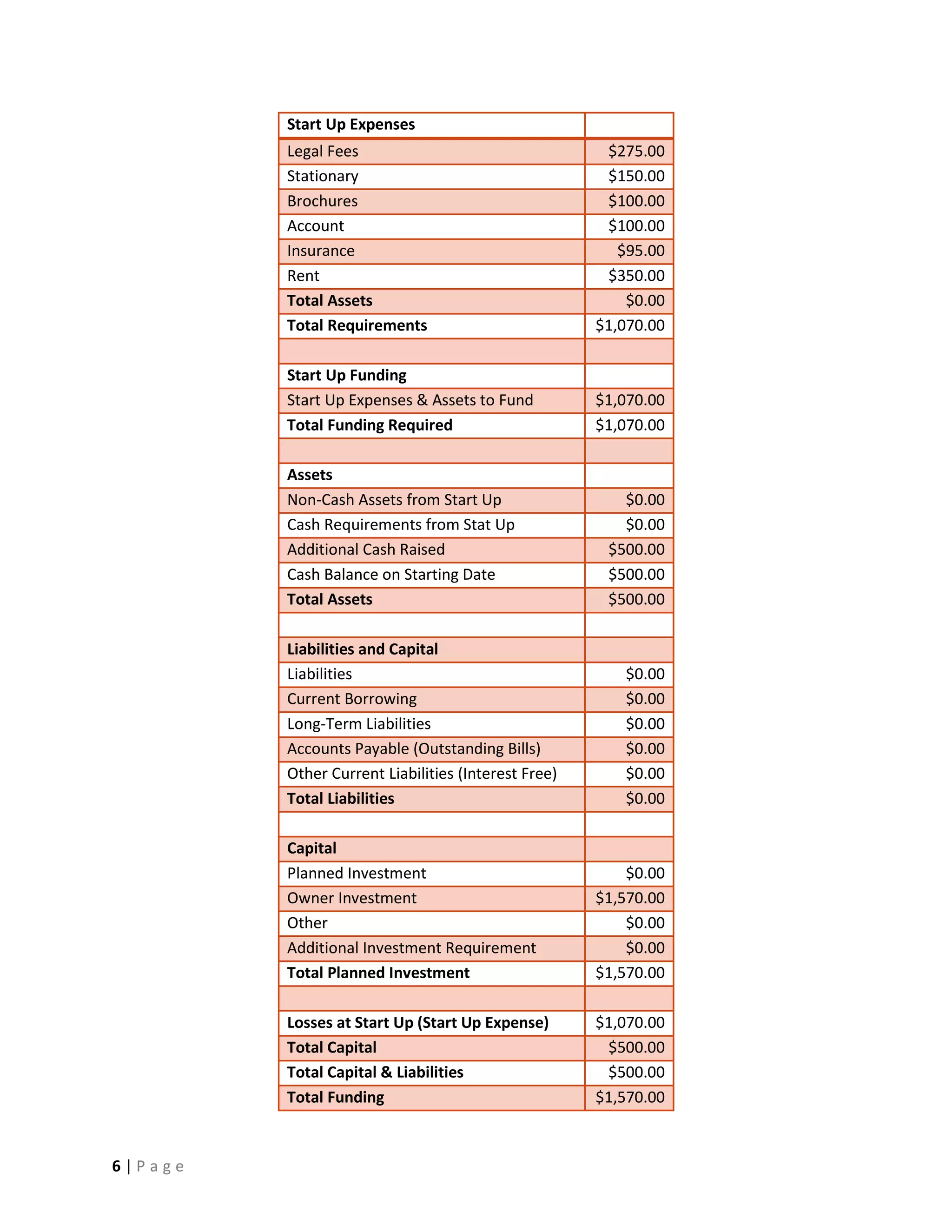

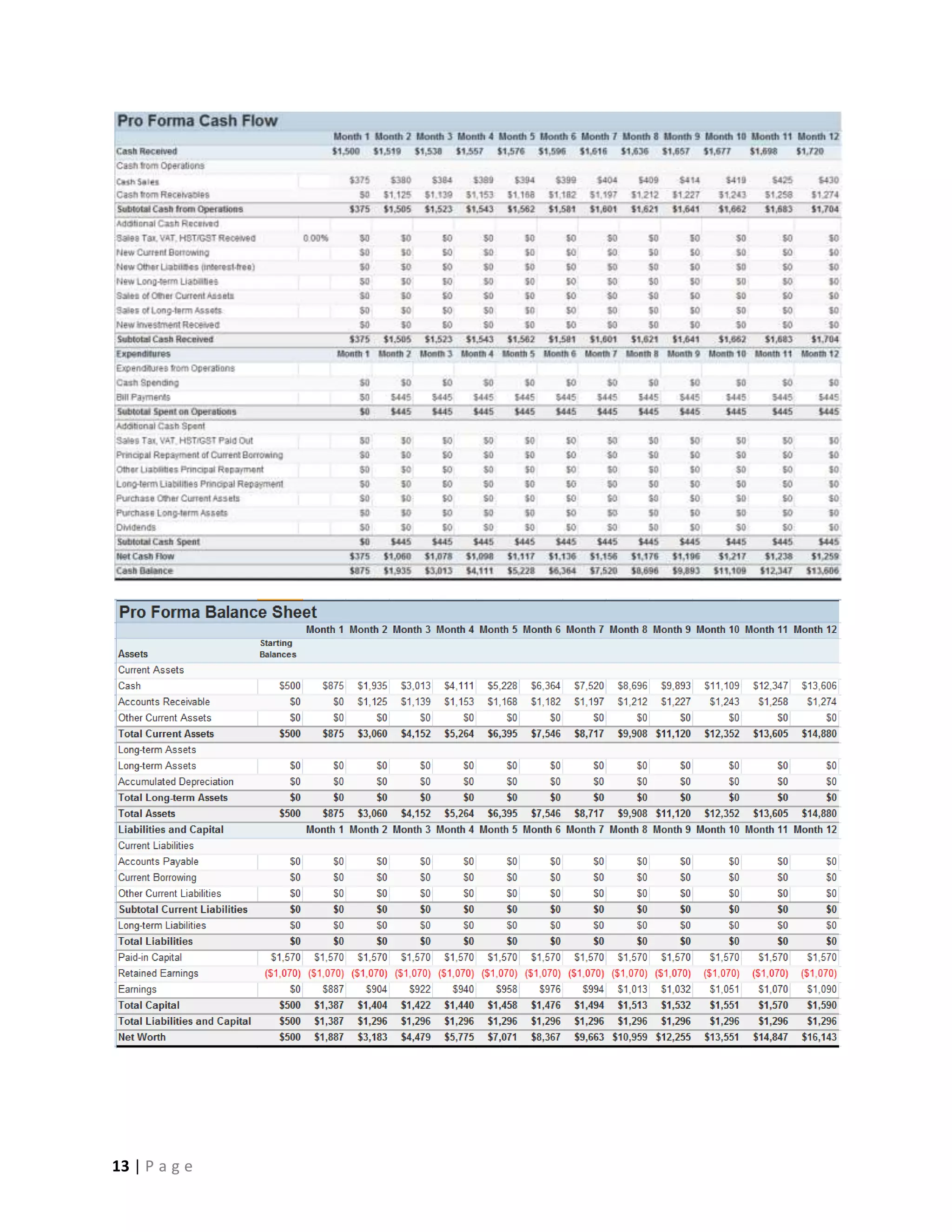

Mohr Consulting (MC) is a newly formed sole proprietorship that provides technical support services for non-profits using iMIS software. MC was started with $1,070 in startup costs funded by the owner. MC will operate out of the owner's home and offer hourly technical support and project-based consulting. MC projects strong sales growth and profits over the next year by focusing on networking within the iMIS user community. Key competitors include larger support firms and individual iMIS consultants, but MC aims to compete based on personalized service, quick response times, and competitive rates.

![Allstate Agent Opportunity Choose Your Own Direction 2010[1]](https://cdn.slidesharecdn.com/ss_thumbnails/allstateagentopportunitychooseyourowndirection20101-12729948829992-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)