Download free for 30 days

Sign in

Upload

Language (EN)

Support

Business

Mobile

Social Media

Marketing

Technology

Art & Photos

Career

Design

Education

Presentations & Public Speaking

Government & Nonprofit

Healthcare

Internet

Law

Leadership & Management

Automotive

Engineering

Software

Recruiting & HR

Retail

Sales

Services

Science

Small Business & Entrepreneurship

Food

Environment

Economy & Finance

Data & Analytics

Investor Relations

Sports

Spiritual

News & Politics

Travel

Self Improvement

Real Estate

Entertainment & Humor

Health & Medicine

Devices & Hardware

Lifestyle

Change Language

Language

English

Español

Português

Français

Deutsche

Cancel

Save

Submit search

EN

Uploaded by

huongquynhstudy

7 views

Slide_Chapter 3.pdf BALANCE SHEET UFM GOOD

PT TCDN CHAPTER 3

Business

◦

Read more

0

Save

Share

Embed

Embed presentation

Download

Download to read offline

1

/ 41

2

/ 41

3

/ 41

4

/ 41

5

/ 41

6

/ 41

7

/ 41

8

/ 41

9

/ 41

10

/ 41

11

/ 41

12

/ 41

13

/ 41

14

/ 41

15

/ 41

16

/ 41

17

/ 41

18

/ 41

19

/ 41

20

/ 41

21

/ 41

22

/ 41

23

/ 41

24

/ 41

25

/ 41

26

/ 41

27

/ 41

28

/ 41

29

/ 41

30

/ 41

31

/ 41

32

/ 41

33

/ 41

34

/ 41

35

/ 41

36

/ 41

37

/ 41

38

/ 41

39

/ 41

40

/ 41

41

/ 41

More Related Content

PPTX

IFR_ch03_Balance sheet.pptx

by

Habibullah Qayumi

PPTX

WRD 27e_SE PPT_Ch10_ADA (Accounting Long Term Assets: fixed and intangible).pptx

by

zeniatulnurk

PPTX

WRD-27e-SE-PPT-Ch10 (1) FIXED AND TANGIBLE.pptx

by

gowrikcom

PPT

Ch09 wrd12e instructor_final

by

fsuttonnnu

DOCX

Due WednesdayDiscussion Requirements Your weekly discussion p.docx

by

infantkimber

PPTX

Balance Sheet Presentation

by

Cameron Fen

PPTX

chapter_2.pptx__________________________relevatn documents

by

phdfinance

PPT

Depreciation and Accounting Concern.ppt

by

AliHadi319773

IFR_ch03_Balance sheet.pptx

by

Habibullah Qayumi

WRD 27e_SE PPT_Ch10_ADA (Accounting Long Term Assets: fixed and intangible).pptx

by

zeniatulnurk

WRD-27e-SE-PPT-Ch10 (1) FIXED AND TANGIBLE.pptx

by

gowrikcom

Ch09 wrd12e instructor_final

by

fsuttonnnu

Due WednesdayDiscussion Requirements Your weekly discussion p.docx

by

infantkimber

Balance Sheet Presentation

by

Cameron Fen

chapter_2.pptx__________________________relevatn documents

by

phdfinance

Depreciation and Accounting Concern.ppt

by

AliHadi319773

Similar to Slide_Chapter 3.pdf BALANCE SHEET UFM GOOD

PPTX

Balance Sheet

by

Alhya Khalid

PPT

Chap equity of business organizations3.ppt

by

Haider Ali

PPTX

accounting information system process for

by

support346674

PPTX

Final Accounts Lecture Notes For Business Mgmt

by

Julius Dennis Estavillo

PDF

Financial Accounting Information for Decisions 9th Edition Wild Solutions Manual

by

jsjumgkaza066

PDF

Financial Accounting Information for Decisions 9th Edition Wild Solutions Manual

by

izukuwadday

PDF

Financial Accounting Information for Decisions 9th Edition Wild Solutions Manual

by

mllanevah

PPT

02_Copy_of_Presentation_Title.ppt

by

Abeer Fouad Agami

PPSX

Credit training in English

by

Dejan Jeremic

PPTX

A4_Tangible non current assets class.pptx

by

srineshrrao

PPT

acctg MBA slide

by

koko20115

PPTX

Economic feasibility study Chapter 7

by

Abd ELRahman ALFar

PPT

Depreciation

by

Rabea Jamal

PPTX

Fixed Asset Process

by

Satish Narayan

PDF

IE 445 Chapter Lecture 8-Finance 2024.pdf

by

lincolnjames244

PPT

Financial Statement Analysis I Session 2

by

Credit Management Association

PPSX

Credit Training[Finall]

by

Dejan Jeremic

PDF

S2-3 (Ch2-4) - Accounting.pdf

by

ZahraHADDAOUI1

PPT

Financial accounting mgt101 power point slides lecture 17

by

Abdul Wadood Ansary

PPTX

AnF 1 _ Basics of Financial Statements (1).pptx

by

tapesh0702

Balance Sheet

by

Alhya Khalid

Chap equity of business organizations3.ppt

by

Haider Ali

accounting information system process for

by

support346674

Final Accounts Lecture Notes For Business Mgmt

by

Julius Dennis Estavillo

Financial Accounting Information for Decisions 9th Edition Wild Solutions Manual

by

jsjumgkaza066

Financial Accounting Information for Decisions 9th Edition Wild Solutions Manual

by

izukuwadday

Financial Accounting Information for Decisions 9th Edition Wild Solutions Manual

by

mllanevah

02_Copy_of_Presentation_Title.ppt

by

Abeer Fouad Agami

Credit training in English

by

Dejan Jeremic

A4_Tangible non current assets class.pptx

by

srineshrrao

acctg MBA slide

by

koko20115

Economic feasibility study Chapter 7

by

Abd ELRahman ALFar

Depreciation

by

Rabea Jamal

Fixed Asset Process

by

Satish Narayan

IE 445 Chapter Lecture 8-Finance 2024.pdf

by

lincolnjames244

Financial Statement Analysis I Session 2

by

Credit Management Association

Credit Training[Finall]

by

Dejan Jeremic

S2-3 (Ch2-4) - Accounting.pdf

by

ZahraHADDAOUI1

Financial accounting mgt101 power point slides lecture 17

by

Abdul Wadood Ansary

AnF 1 _ Basics of Financial Statements (1).pptx

by

tapesh0702

Recently uploaded

DOCX

How to Buy Verified OnlyFans Accounts Work in 2026.docx

by

https://pvaisback.com/product/buy-old-gmail-accounts/

PDF

apidays Australia 2025 | Value Dynamics Mapping - Making Value Visible

by

apidays

PDF

Equinox Gold - Corporate Presentation - Jan 2026

by

Equinox Gold Corp.

PDF

The threat to financial insitutions of quantum computing breaking all encrypt...

by

Chris Skinner

PDF

Camil Institutional Presentation_Dez25.pdf

by

CAMILRI

PDF

Jim Bologa - The CEO Of Porter And Chester Institute

by

Jim Bologa

PPTX

Keynote: The Modern CMO: Architect of Growth. Guardian of Credibility.

by

Armis Inc

DOCX

Podcast Promotion Schedule for Turntable News

by

slpalakovich

PDF

BendelPuertoRicoCubaGuyanaVenezuelaPetroleumRefineryPetrochemicalPetroAgroInd...

by

OsaJOkundayeODMDFAAO

PPTX

REVIEWER-3rd-quarter-exam-mathematics.pptx

by

dominicdaltoncaling2

PDF

17 Guide to Buying Verified Binance Accounts in the US.pdf

by

https://pvaisback.com/product/buy-old-gmail-accounts/

PDF

Top 5 Trusted Websites to Buy Verified PayPal Accounts Safely in 2026

by

Usaservicepoint

PDF

Best Top 3 Sites to Buy Google Reviews (5-Star & Non-Drop).pdf

by

https://pvaallit.com/product/buy-google-5-star-reviews/

PDF

PuertoRicoCubaGuyanaVenezuelaPetroleumRefineryPetrochemicalPetroAgroIndustria...

by

OsaJOkundayeODMDFAAO

PDF

Using-pension-savings-to-support-home-ownership.pdf

by

Henry Tapper

DOCX

How to Buy a Verified PayPal Account_ Step-by-Step Instructions.docx

by

https://pvaallit.com/product/buy-verified-apple-pay-accounts/

PDF

Top 1 0 Websites to Buy Verified Transfer Remitly Accounts ....pdf

by

Business

DOCX

Fast Delivery of Real Buy Twitter Accounts Available in 2026.docx

by

Business

PDF

OIL CHECK 500 Portable - Air Quality Monitoring System

by

CS Instruments

PDF

Kirill Klip GEM Royalty TNR Gold Lithium Presentation

by

Kirill Klip

How to Buy Verified OnlyFans Accounts Work in 2026.docx

by

https://pvaisback.com/product/buy-old-gmail-accounts/

apidays Australia 2025 | Value Dynamics Mapping - Making Value Visible

by

apidays

Equinox Gold - Corporate Presentation - Jan 2026

by

Equinox Gold Corp.

The threat to financial insitutions of quantum computing breaking all encrypt...

by

Chris Skinner

Camil Institutional Presentation_Dez25.pdf

by

CAMILRI

Jim Bologa - The CEO Of Porter And Chester Institute

by

Jim Bologa

Keynote: The Modern CMO: Architect of Growth. Guardian of Credibility.

by

Armis Inc

Podcast Promotion Schedule for Turntable News

by

slpalakovich

BendelPuertoRicoCubaGuyanaVenezuelaPetroleumRefineryPetrochemicalPetroAgroInd...

by

OsaJOkundayeODMDFAAO

REVIEWER-3rd-quarter-exam-mathematics.pptx

by

dominicdaltoncaling2

17 Guide to Buying Verified Binance Accounts in the US.pdf

by

https://pvaisback.com/product/buy-old-gmail-accounts/

Top 5 Trusted Websites to Buy Verified PayPal Accounts Safely in 2026

by

Usaservicepoint

Best Top 3 Sites to Buy Google Reviews (5-Star & Non-Drop).pdf

by

https://pvaallit.com/product/buy-google-5-star-reviews/

PuertoRicoCubaGuyanaVenezuelaPetroleumRefineryPetrochemicalPetroAgroIndustria...

by

OsaJOkundayeODMDFAAO

Using-pension-savings-to-support-home-ownership.pdf

by

Henry Tapper

How to Buy a Verified PayPal Account_ Step-by-Step Instructions.docx

by

https://pvaallit.com/product/buy-verified-apple-pay-accounts/

Top 1 0 Websites to Buy Verified Transfer Remitly Accounts ....pdf

by

Business

Fast Delivery of Real Buy Twitter Accounts Available in 2026.docx

by

Business

OIL CHECK 500 Portable - Air Quality Monitoring System

by

CS Instruments

Kirill Klip GEM Royalty TNR Gold Lithium Presentation

by

Kirill Klip

Slide_Chapter 3.pdf BALANCE SHEET UFM GOOD

1.

Chapter 3 Balance Sheet ©

2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

2.

Chapter 3, Slide

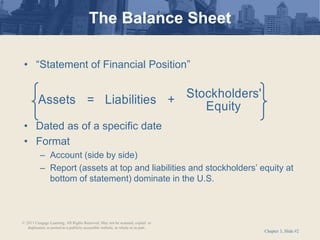

#2 • “Statement of Financial Position” • Dated as of a specific date • Format – Account (side by side) – Report (assets at top and liabilities and stockholders’ equity at bottom of statement) dominate in the U.S. Stockholders' Assets = Liabilities + Equity The Balance Sheet © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

3.

Chapter 3, Slide

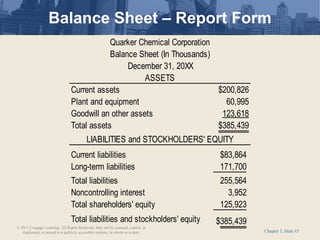

#3 Balance Sheet – Report Form Current assets $200,826 Plant and equipment 60,995 Goodwill an other assets 123,618 Total assets $385,439 Current liabilities $83,864 Long-term liabilities 171,700 Total liabilities 255,564 Noncontrolling interest 3,952 Total shareholders' equity 125,923 Total liabilities and stockholders' equity $385,439 LIABILITIES and STOCKHOLDERS' EQUITY Quarker Chemical Corporation Balance Sheet (In Thousands) December 31, 20XX ASSETS © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

4.

Chapter 3, Slide

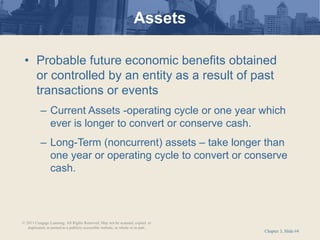

#4 • Probable future economic benefits obtained or controlled by an entity as a result of past transactions or events – Current Assets -operating cycle or one year which ever is longer to convert or conserve cash. – Long-Term (noncurrent) assets – take longer than one year or operating cycle to convert or conserve cash. Assets © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

5.

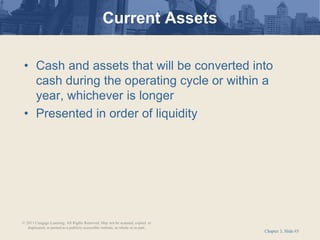

Chapter 3, Slide

#5 • Cash and assets that will be converted into cash during the operating cycle or within a year, whichever is longer • Presented in order of liquidity Current Assets © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

6.

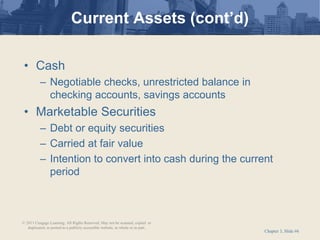

Chapter 3, Slide

#6 • Cash – Negotiable checks, unrestricted balance in checking accounts, savings accounts • Marketable Securities – Debt or equity securities – Carried at fair value – Intention to convert into cash during the current period Current Assets (cont’d) © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

7.

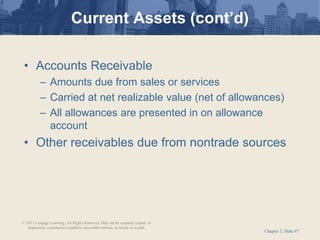

Chapter 3, Slide

#7 • Accounts Receivable – Amounts due from sales or services – Carried at net realizable value (net of allowances) – All allowances are presented in on allowance account • Other receivables due from nontrade sources Current Assets (cont’d) © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

8.

Chapter 3, Slide

#8 • Inventories – Carried at lower of cost or market – Categories • Merchandise on hand- Retail or wholesale firms • Raw materials • Work in process • Finished goods Manufacturer Current Assets (cont’d) © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

9.

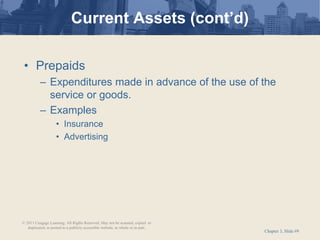

Chapter 3, Slide

#9 • Prepaids – Expenditures made in advance of the use of the service or goods. – Examples • Insurance • Advertising Current Assets (cont’d) © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

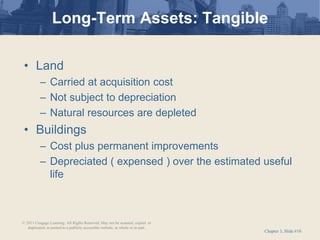

10.

Chapter 3, Slide

#10 • Land – Carried at acquisition cost – Not subject to depreciation – Natural resources are depleted • Buildings – Cost plus permanent improvements – Depreciated ( expensed ) over the estimated useful life Long-Term Assets: Tangible © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

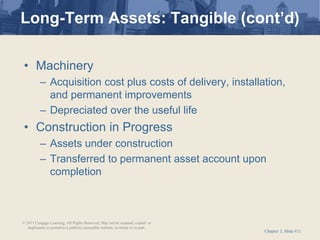

11.

Chapter 3, Slide

#11 • Machinery – Acquisition cost plus costs of delivery, installation, and permanent improvements – Depreciated over the useful life • Construction in Progress – Assets under construction – Transferred to permanent asset account upon completion Long-Term Assets: Tangible (cont’d) © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

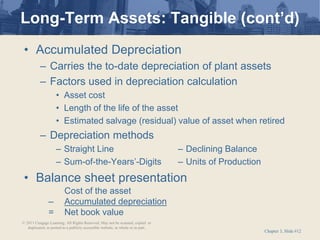

12.

Chapter 3, Slide

#12 • Accumulated Depreciation – Carries the to-date depreciation of plant assets – Factors used in depreciation calculation • Asset cost • Length of the life of the asset • Estimated salvage (residual) value of asset when retired – Depreciation methods – Straight Line – Declining Balance – Sum-of-the-Years’-Digits – Units of Production • Balance sheet presentation Cost of the asset – Accumulated depreciation = Net book value Long-Term Assets: Tangible (cont’d) © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

13.

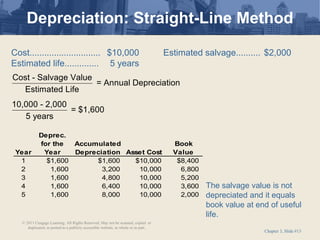

Chapter 3, Slide

#13 Depreciation: Straight-Line Method Cost - Salvage Value = Annual Depreciation Estimated Life 10,000 - 2,000 = $1,600 5 years Cost............................. $10,000 Estimated salvage.......... $2,000 Estimated life.............. 5 years Year Deprec. for the Year Accumulated Depreciation Asset Cost Book Value 1 $1,600 $1,600 $10,000 $8,400 2 1,600 3,200 10,000 6,800 3 1,600 4,800 10,000 5,200 4 1,600 6,400 10,000 3,600 5 1,600 8,000 10,000 2,000 The salvage value is not depreciated and it equals book value at end of useful life. © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

14.

Chapter 3, Slide

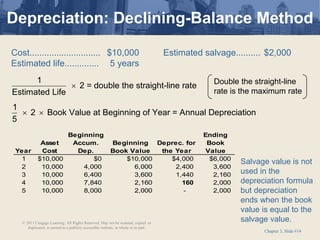

#14 Depreciation: Declining-Balance Method 1 2 = double the straight-line rate Estimated Life 1 2 Book Value at Beginning of Year = Annual Depreciation 5 Year Asset Cost Beginning Accum. Dep. Beginning Book Value Deprec. for the Year Ending Book Value 1 $10,000 $0 $10,000 $4,000 $6,000 2 10,000 4,000 6,000 2,400 3,600 3 10,000 6,400 3,600 1,440 2,160 4 10,000 7,840 2,160 160 2,000 5 10,000 8,000 2,000 - 2,000 Salvage value is not used in the depreciation formula but depreciation ends when the book value is equal to the salvage value. Cost............................. $10,000 Estimated salvage.......... $2,000 Estimated life.............. 5 years Double the straight-line rate is the maximum rate © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

15.

Chapter 3, Slide

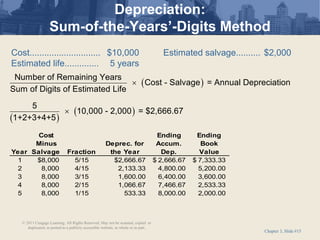

#15 Depreciation: Sum-of-the-Years’-Digits Method Cost............................. $10,000 Estimated salvage.......... $2,000 Estimated life.............. 5 years ( ) ( ) ( ) Number of Remaining Years Cost - Salvage = Annual Depreciation Sum of Digits of Estimated Life 5 10,000 - 2,000 = $2,666.67 1+2+3+4+5 Year Cost Minus Salvage Fraction Deprec. for the Year Ending Accum. Dep. Ending Book Value 1 $8,000 5/15 $2,666.67 2,666.67 $ 7,333.33 $ 2 8,000 4/15 2,133.33 4,800.00 5,200.00 3 8,000 3/15 1,600.00 6,400.00 3,600.00 4 8,000 2/15 1,066.67 7,466.67 2,533.33 5 8,000 1/15 533.33 8,000.00 2,000.00 © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

16.

Chapter 3, Slide

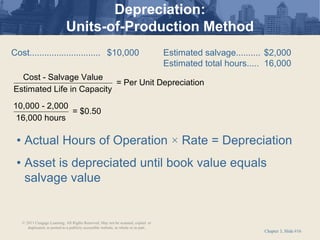

#16 Depreciation: Units-of-Production Method Cost - Salvage Value = Per Unit Depreciation Estimated Life in Capacity 10,000 - 2,000 = $0.50 16,000 hours Cost............................. $10,000 Estimated salvage.......... $2,000 Estimated total hours..... 16,000 • Actual Hours of Operation × Rate = Depreciation • Asset is depreciated until book value equals salvage value © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

17.

Chapter 3, Slide

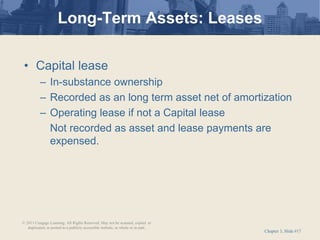

#17 Long-Term Assets: Leases • Capital lease – In-substance ownership – Recorded as an long term asset net of amortization – Operating lease if not a Capital lease Not recorded as asset and lease payments are expensed. © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

18.

Chapter 3, Slide

#18 • Debt or equity securities – Held to maintain business relationship or to exercise control • Debt classification – Held-to-maturity carried at amortized cost – Available-for-sale carried at fair value Long-Term Assets: Investments © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

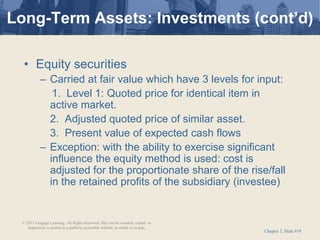

19.

Chapter 3, Slide

#19 Long-Term Assets: Investments (cont’d) • Equity securities – Carried at fair value which have 3 levels for input: 1. Level 1: Quoted price for identical item in active market. 2. Adjusted quoted price of similar asset. 3. Present value of expected cash flows – Exception: with the ability to exercise significant influence the equity method is used: cost is adjusted for the proportionate share of the rise/fall in the retained profits of the subsidiary (investee) © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

20.

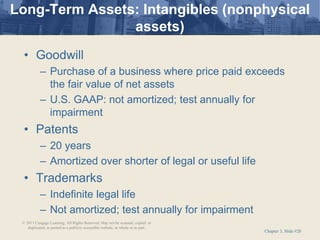

Chapter 3, Slide

#20 • Goodwill – Purchase of a business where price paid exceeds the fair value of net assets – U.S. GAAP: not amortized; test annually for impairment • Patents – 20 years – Amortized over shorter of legal or useful life • Trademarks – Indefinite legal life – Not amortized; test annually for impairment Long-Term Assets: Intangibles (nonphysical assets) © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

21.

Chapter 3, Slide

#21 Long-Term Assets: Intangibles (cont’d) • Franchises – Life based on contract – Amortize over shorter of legal or useful life • Copyrights – Life of the creator plus 70 years – Amortize over shorter of legal or useful life © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

22.

Chapter 3, Slide

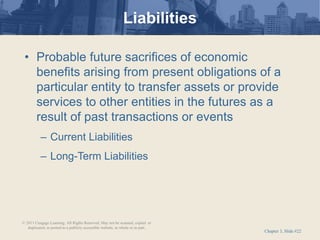

#22 • Probable future sacrifices of economic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the futures as a result of past transactions or events – Current Liabilities – Long-Term Liabilities Liabilities © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

23.

Chapter 3, Slide

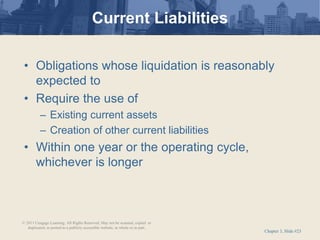

#23 Current Liabilities • Obligations whose liquidation is reasonably expected to • Require the use of – Existing current assets – Creation of other current liabilities • Within one year or the operating cycle, whichever is longer © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

24.

Chapter 3, Slide

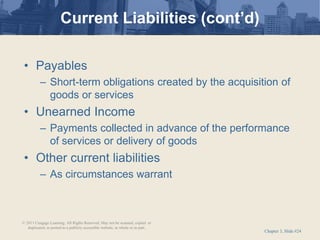

#24 Current Liabilities (cont’d) • Payables – Short-term obligations created by the acquisition of goods or services • Unearned Income – Payments collected in advance of the performance of services or delivery of goods • Other current liabilities – As circumstances warrant © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

25.

Chapter 3, Slide

#25 Long-Term Liabilities • Due in a period beyond one year or operating cycle • Related to – Financing arrangements – Operational obligations © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

26.

Chapter 3, Slide

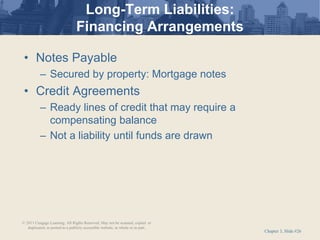

#26 Long-Term Liabilities: Financing Arrangements • Notes Payable – Secured by property: Mortgage notes • Credit Agreements – Ready lines of credit that may require a compensating balance – Not a liability until funds are drawn © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

27.

Chapter 3, Slide

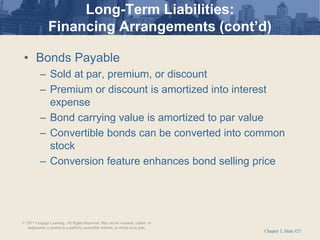

#27 Long-Term Liabilities: Financing Arrangements (cont’d) • Bonds Payable – Sold at par, premium, or discount – Premium or discount is amortized into interest expense – Bond carrying value is amortized to par value – Convertible bonds can be converted into common stock – Conversion feature enhances bond selling price © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

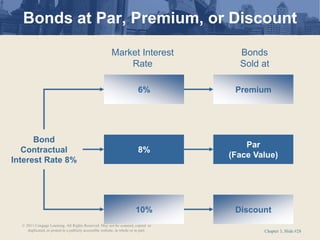

28.

Chapter 3, Slide

#28 Bonds at Par, Premium, or Discount Bond Contractual Interest Rate 8% 6% 8% 10% Premium Par (Face Value) Discount Market Interest Rate Bonds Sold at © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

29.

Chapter 3, Slide

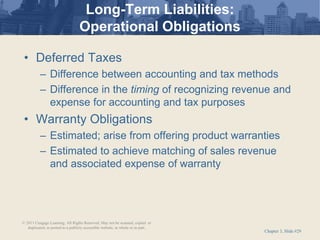

#29 Long-Term Liabilities: Operational Obligations • Deferred Taxes – Difference between accounting and tax methods – Difference in the timing of recognizing revenue and expense for accounting and tax purposes • Warranty Obligations – Estimated; arise from offering product warranties – Estimated to achieve matching of sales revenue and associated expense of warranty © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

30.

Chapter 3, Slide

#30 Long-Term Liabilities: Operational Obligations (cont’d) • Noncontrolling Interest (was minority interest) – Reported on consolidated financial statements as equity, but separate from parents equity – Represents the interest in the equity of a partially- held subsidiary by the nonmajority owners – Analysis can be twice if material-once as a liability (conservative) and then as equity. • Other Noncurrent Liabilities – As circumstances warrant • Redeemable Preferred Stock – Excluded from stockholders’ equity – For analysis, treat as a liability © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

31.

Chapter 3, Slide

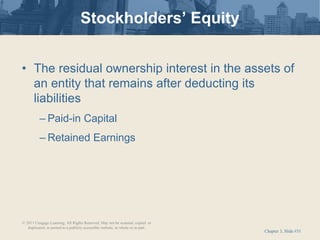

#31 • The residual ownership interest in the assets of an entity that remains after deducting its liabilities – Paid-in Capital – Retained Earnings Stockholders’ Equity © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

32.

Chapter 3, Slide

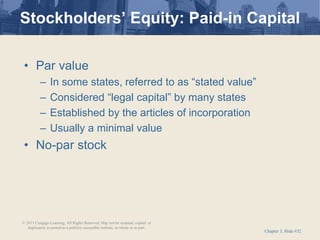

#32 Stockholders’ Equity: Paid-in Capital • Par value – In some states, referred to as “stated value” – Considered “legal capital” by many states – Established by the articles of incorporation – Usually a minimal value • No-par stock © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

33.

Chapter 3, Slide

#33 Stockholders’ Equity: Paid-in Capital (cont’d) • Additional paid-in capital – Issue price in excess of par (stated) value – Other sources • Treasury stock transactions • Stock dividend transactions • Donated capital © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

34.

Chapter 3, Slide

#34 Stockholders’ Equity: Paid-in Capital (cont’d) • Common Stock – Shareholder ownership – Voting rights • Election of board of directors • Major corporate decisions – Liquidation rights secondary to • Creditors • Preferred stock © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

35.

Chapter 3, Slide

#35 Stockholders’ Equity: Paid-in Capital (cont’d) • Preferred Stock – Does not normally convey voting rights – May carry any or all of these features: • Preference as to dividends • Accumulation of dividends • Participation in dividend beyond stated dividend rate • Convertibility into common stock at holder’s discretion • Preference in liquidation secondary to creditors • Callable at issuer discretion • Redemption at future maturity value • Donated Capital – Donated by outside entities – Shareholder surrender of stock © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

36.

Chapter 3, Slide

#36 Stockholders’ Equity: Retained Earnings • Undistributed earnings of the corporation – Net income for all prior periods – Less dividends declared to shareholders for all prior periods © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

37.

Chapter 3, Slide

#37 Stockholders’ Equity: Other • Quasi-Reorganization – Eliminates a deficit balance of retained earnings – Retained earnings are dated for 5-10 years • Accumulated Other Comprehensive Income - Represents retained earnings for other comprehensive income as a separate component on the face of the balance sheet. © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

38.

Chapter 3, Slide

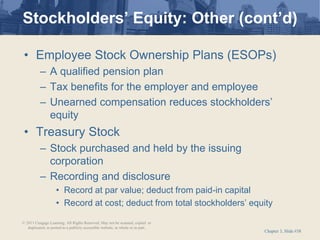

#38 Stockholders’ Equity: Other (cont’d) • Employee Stock Ownership Plans (ESOPs) – A qualified pension plan – Tax benefits for the employer and employee – Unearned compensation reduces stockholders’ equity • Treasury Stock – Stock purchased and held by the issuing corporation – Recording and disclosure • Record at par value; deduct from paid-in capital • Record at cost; deduct from total stockholders’ equity © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

39.

Chapter 3, Slide

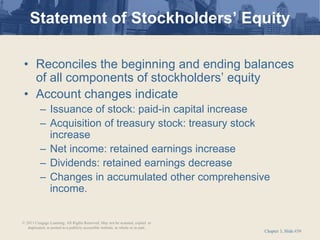

#39 • Reconciles the beginning and ending balances of all components of stockholders’ equity • Account changes indicate – Issuance of stock: paid-in capital increase – Acquisition of treasury stock: treasury stock increase – Net income: retained earnings increase – Dividends: retained earnings decrease – Changes in accumulated other comprehensive income. Statement of Stockholders’ Equity © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

40.

Chapter 3, Slide

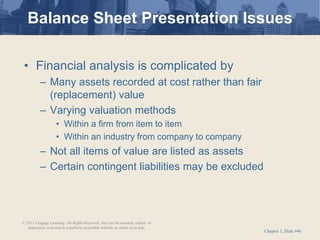

#40 • Financial analysis is complicated by – Many assets recorded at cost rather than fair (replacement) value – Varying valuation methods • Within a firm from item to item • Within an industry from company to company – Not all items of value are listed as assets – Certain contingent liabilities may be excluded Balance Sheet Presentation Issues © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

41.

Chapter 3, Slide

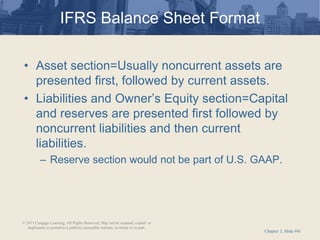

#41 IFRS Balance Sheet Format • Asset section=Usually noncurrent assets are presented first, followed by current assets. • Liabilities and Owner’s Equity section=Capital and reserves are presented first followed by noncurrent liabilities and then current liabilities. – Reserve section would not be part of U.S. GAAP. © 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Download

![Credit Training[Finall]](https://cdn.slidesharecdn.com/ss_thumbnails/credittrainingfinall-091227073414-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)