Downloaded 18 times

![89

SGS has started a process to understand

our value to society. Value to society is

based on the premise that all business

activities take place within a field

of social capital, which is contained

within the natural environment.

Social capital allows the development

of interpersonal relationships that in

turn enable the combination of human

capital, natural capital and intellectual

capital to produce goods and services

(i.e. manufactured capital). A key

component of the value to society

framework is determining the economic

values for respective capital stocks

and flows.This process of economic

evaluation, often termed monetisation,

is necessary to enable integration of the

full factors of production (i.e. the natural

capital, human capital, manufactured

capital, etc.) into a core financial-based

business decision-making system.

The first stage in the process has

involved the quantification and economic

valuation of the various capital stocks

and flows that comprehensively

represent the necessary inputs and

outputs of our business activities.

First, we identified the entire asset

base that underpins SGS’ operations.

Conceptually supported by the

International Integrated Reporting

Council’s [IRRC] guidelines, operations

require (directly and indirectly)

a complement of:

FINANCIAL CAPITAL

The medium for exchange, a store of

economic value and as a unit of account.

NATURAL CAPITAL

The economic functions

of the natural environment.

HUMAN CAPITAL

The economic functions

of the labour force.

INTELLECTUAL CAPITAL

The economic functions of knowledge.

SOCIAL CAPITAL

The economic functions of trust within

stakeholder networks.

MANUFACTURED (OR BUILT) CAPITAL

The economic functions of property,

plant, equipment, inventory and

intermediate inputs.

In future, we will start reporting around

the six capitals. A significant amount

of work has already been completed,

which indicates that the business

activities of SGS are net positive (which

means that we contribute more value

than we derive). There is further work

to be done to adapt the concept to our

business model using auditable data, but

we expect to be in a position to report

on this in detail in 2016. We are also

focusing on aligning our future reporting

to the IRRC framework. As such,

2016 will be a decisive year involving

high-level stakeholder dialogue and

consultation on our evolved reporting

approach. More details on how we

are measuring our value to society

can be found on our website:

www.sgs.com/cs-report2015

OUR VALUE

TO SOCIETY](https://image.slidesharecdn.com/sgs2015annualreporten-160224131412/85/SGS-2015-Annual-Report-93-320.jpg)

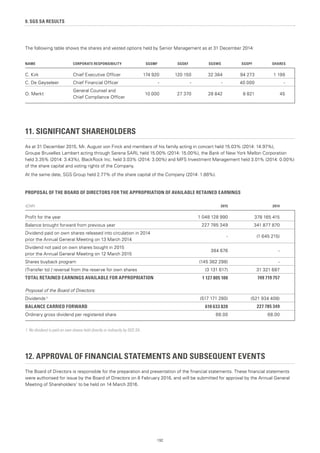

![Net change in deferred tax assets/(liabilities):

(CHF million) TOTAL

NET DEFERRED INCOME TAX ASSET (LIABILITY) AT 1 JANUARY 2014 107

(Charged)/credited to the income statement (11)

Credited/(charged) to the shareholders' equity 1

26

Exchange differences and other (1)

NET DEFERRED INCOME TAX ASSET (LIABILITY) AT 31 DECEMBER 2014 121

Credited/(charged) to the income statement 19

(Charged)/credited to the shareholders' equity 1

(15)

Exchange differences and other (12)

NET DEFERRED INCOME TAX ASSET (LIABILITY) AT 31 DECEMBER 2015 113

1. Relate to remeasurement gains and losses on pensions. (2015: CHF 9 million, 2014: CHF 26 million) and pension funds special contribution [2015: CHF (24) million,

2014: CHF 0 million].

(CHF million) 2015 2014

REFLECTED IN THE BALANCE SHEET AS FOLLOWS:

Deferred tax assets 173 195

Deferred tax liabilities (60) (74)

TOTAL 113 121

The Group has unrecognised tax losses carried forward amounting to CHF 46 million (2014: CHF 49 million) of which none will

expire within the next five years. No tax losses carried forward expired in 2015.

At 31 December 2015, the retained earnings of subsidiaries and foreign incorporated joint ventures consolidated by the Group include

approximately CHF 4 125 million (2014: CHF 3 912 million) of undistributed earnings that may be subject to tax if remitted to the

parent company. As a Group policy, no deferred tax is recognised in respect of these amounts until the point at which the distributable

earnings are determined and foreign statutory requirements, allowing the distribution, are fulfilled. Until that time, the Group is able to

control the reversal of the temporary differences and it is probable that they will not reverse in the foreseeable future.

9. EARNINGS PER SHARE

Basic earnings per share are calculated as follows:

2015 2014

Profit attributable to equity holders of SGS SA (CHF million) 549 629

Weighted average number of shares 7 626 002 7 670 752

BASIC EARNINGS PER SHARE (CHF) 71.99 81.99

Diluted earnings per share are calculated as basic earnings per share except that the weighted average number of shares includes

the dilutive effect of the Group’s share option plans (see note 31):

2015 2014

Profit attributable to equity holders of SGS SA (CHF million) 549 629

Diluted weighted average number of shares 7 630 172 7 702 444

DILUTED EARNINGS PER SHARE (CHF) 71.95 81.65

152

8. SGS GROUP RESULTS](https://image.slidesharecdn.com/sgs2015annualreporten-160224131412/85/SGS-2015-Annual-Report-156-320.jpg)

The annual report summarizes SGS's performance in 2015, including financial highlights, business segment highlights, and sustainability performance. It provides an overview of changes to SGS's structure and strategy to take advantage of market opportunities. Organic revenue growth was 2.0% and acquisitions contributed 1.6% growth. Operating cash flow exceeded CHF 1 billion for the first time. SGS remained the leader in sustainability indices and continued initiatives in emissions reductions, achieving carbon neutrality again in 2015. The report outlines SGS's strategic focus on innovation, expertise, and operational excellence across its industries.