Download free for 30 days

Sign in

Upload

Language (EN)

Support

Business

Mobile

Social Media

Marketing

Technology

Art & Photos

Career

Design

Education

Presentations & Public Speaking

Government & Nonprofit

Healthcare

Internet

Law

Leadership & Management

Automotive

Engineering

Software

Recruiting & HR

Retail

Sales

Services

Science

Small Business & Entrepreneurship

Food

Environment

Economy & Finance

Data & Analytics

Investor Relations

Sports

Spiritual

News & Politics

Travel

Self Improvement

Real Estate

Entertainment & Humor

Health & Medicine

Devices & Hardware

Lifestyle

Change Language

Language

English

Español

Português

Français

Deutsche

Cancel

Save

EN

Uploaded by

AnhTrnQunh6

273 views

sensor_tower__state_of_mobile_2025__en.pdf

sensor_tower__state_of_mobile_2025__en.pdf

Software

◦

Read more

0

Save

Share

Embed

Embed presentation

Download

Download to read offline

1

/ 95

2

/ 95

3

/ 95

4

/ 95

5

/ 95

6

/ 95

7

/ 95

8

/ 95

Most read

9

/ 95

10

/ 95

Most read

11

/ 95

12

/ 95

13

/ 95

14

/ 95

15

/ 95

16

/ 95

17

/ 95

18

/ 95

Most read

19

/ 95

20

/ 95

21

/ 95

22

/ 95

23

/ 95

24

/ 95

25

/ 95

26

/ 95

27

/ 95

28

/ 95

29

/ 95

30

/ 95

31

/ 95

32

/ 95

33

/ 95

34

/ 95

35

/ 95

36

/ 95

37

/ 95

38

/ 95

39

/ 95

40

/ 95

41

/ 95

42

/ 95

43

/ 95

44

/ 95

45

/ 95

46

/ 95

47

/ 95

48

/ 95

49

/ 95

50

/ 95

51

/ 95

52

/ 95

53

/ 95

54

/ 95

55

/ 95

56

/ 95

57

/ 95

58

/ 95

59

/ 95

60

/ 95

61

/ 95

62

/ 95

63

/ 95

64

/ 95

65

/ 95

66

/ 95

67

/ 95

68

/ 95

69

/ 95

70

/ 95

71

/ 95

72

/ 95

73

/ 95

74

/ 95

75

/ 95

76

/ 95

77

/ 95

78

/ 95

79

/ 95

80

/ 95

81

/ 95

82

/ 95

83

/ 95

84

/ 95

85

/ 95

86

/ 95

87

/ 95

88

/ 95

89

/ 95

90

/ 95

91

/ 95

92

/ 95

93

/ 95

94

/ 95

95

/ 95

More Related Content

PDF

sensor_tower__state_of_mobile_2025__Vietnam.pdf

by

AnhTrnQunh6

PDF

App Annie: The State of Mobile 2021

by

Léo Xavier

PDF

App annie-2015-retrospective-en

by

Eytan Lerba

PDF

App annie-2015-retrospective-en

by

Thomas Pham

PDF

App Annie: The State of the App Economy in 2017

by

krystinedinh

PDF

2020 Mobile Apps Downloads and Usage Statistics

by

SwagSoft

PDF

202111_App_Annie_2022_Mobile_Predictions.pdf

by

ManiSood3

PDF

App annie state of mobile 2022

by

Shereen Badr

sensor_tower__state_of_mobile_2025__Vietnam.pdf

by

AnhTrnQunh6

App Annie: The State of Mobile 2021

by

Léo Xavier

App annie-2015-retrospective-en

by

Eytan Lerba

App annie-2015-retrospective-en

by

Thomas Pham

App Annie: The State of the App Economy in 2017

by

krystinedinh

2020 Mobile Apps Downloads and Usage Statistics

by

SwagSoft

202111_App_Annie_2022_Mobile_Predictions.pdf

by

ManiSood3

App annie state of mobile 2022

by

Shereen Badr

Similar to sensor_tower__state_of_mobile_2025__en.pdf

PDF

2017 Retrospective: A Monumental Year for the App Economy

by

Filipp Paster

PDF

5 Mobile App Predictions

by

Harsha MV

PDF

Sensor tower-q2-2021-data-digest

by

MarketingTrips

PDF

What Mobile Privacy Changes Mean for Your Holiday Strategy

by

Tinuiti

PPTX

Wonk Mobile Future of Mobile

by

Wonk Mobile

DOCX

Global Mobile App Stores Market 2013 – Explosive growth continues till 2017

by

Rajesh Prabhakar

PPTX

Using Market Data to Make Strategic Decisions (Priori Data presentation at th...

by

Priori Data

PPTX

Future of mobile Apps in India & Global market

by

Tapas Das

PDF

R 13-bii appmarketingreport-2013_freeappmkt

by

Centrum Adama Smitha

PDF

Latest Trends in the App Ecosystem

by

AppCoins

PDF

Mobile Trends | October 2013

by

space150

PDF

Annual state of_global_mobile_industry_2012_chetan_sharma_consulting

by

Chetan Sharma

PPTX

157 Mobile App Stats You Should Know About

by

Stuart Dredge

PDF

Mobile applications

by

MyPeepal Technologies Pvt. Ltd.

PDF

The State of App Downloads and Monetization Report : Latin America Q3 2015

by

InMobi

PDF

The State of App Downloads and Monetization Infographic : North America 2015

by

InMobi

PDF

Тенденции мобильных приложений 2021 года.

by

CPAex

PDF

The State of App Downloads and Monetization Report : North America Q2 2015

by

InMobi

PDF

The

by

ReportLinker.com

PDF

Priori Data Global Insights Report for iOS - November 2013

by

Priori Data

2017 Retrospective: A Monumental Year for the App Economy

by

Filipp Paster

5 Mobile App Predictions

by

Harsha MV

Sensor tower-q2-2021-data-digest

by

MarketingTrips

What Mobile Privacy Changes Mean for Your Holiday Strategy

by

Tinuiti

Wonk Mobile Future of Mobile

by

Wonk Mobile

Global Mobile App Stores Market 2013 – Explosive growth continues till 2017

by

Rajesh Prabhakar

Using Market Data to Make Strategic Decisions (Priori Data presentation at th...

by

Priori Data

Future of mobile Apps in India & Global market

by

Tapas Das

R 13-bii appmarketingreport-2013_freeappmkt

by

Centrum Adama Smitha

Latest Trends in the App Ecosystem

by

AppCoins

Mobile Trends | October 2013

by

space150

Annual state of_global_mobile_industry_2012_chetan_sharma_consulting

by

Chetan Sharma

157 Mobile App Stats You Should Know About

by

Stuart Dredge

Mobile applications

by

MyPeepal Technologies Pvt. Ltd.

The State of App Downloads and Monetization Report : Latin America Q3 2015

by

InMobi

The State of App Downloads and Monetization Infographic : North America 2015

by

InMobi

Тенденции мобильных приложений 2021 года.

by

CPAex

The State of App Downloads and Monetization Report : North America Q2 2015

by

InMobi

The

by

ReportLinker.com

Priori Data Global Insights Report for iOS - November 2013

by

Priori Data

Recently uploaded

PDF

Phone Tracker App for Family (2026)_ The Safe, Legit Way to Protect Loved One...

by

Mia Taylor

PDF

2026 Safety Roadmap: Systems, Skills, and Scale for EHS Leaders

by

TECH EHS Solution

PDF

AI-native development: from Prompt to Platform

by

Maxim Salnikov

PDF

Water Delivery App Development Solutions.pdf

by

eSiteWorld TechnoLabs Pvt. Ltd.

PDF

LogiNext Media Kit & Company Overview 2025

by

sanikaroy72

PPTX

Edison MuleSoft Meetup : Vibe Coding | MuleSoft Meetups

by

Sravan Lingam

PPTX

HackYourBrain_JFokusConference_03022026.pptx

by

SimonedeGijt

PDF

Visualizing Your Data Lake with Grafana - Amsterdam

by

Imma Valls Bernaus

PPTX

Best eCommerce Development Agency in USA | The Dataflux

by

Key Medsolutions Inc

PDF

ChampionMATES – Compete With Friends. Predict Sports. Become the Champion.

by

Rafal Ksiazek

PDF

Build a Scalable On-Demand Courier Service App.pdf

by

V3CUBE TECHNOLABS

DOCX

The Rise of Headless CMS in Modern Web Development.docx

by

work4noahmiller

PDF

LogiNext Media Kit & Company Overview 2025

by

nidhisharmaq7184

PDF

LogiNext Media Kit & Company Overview 2025

by

priyajoshi2929

PDF

Windows Server 2025 Administration Fundamentals 4ED

by

raynasolomon136

PDF

Smart ways to se AI in your business , presentation

by

AI n Dot Net

PDF

Why I Volunteer at FOSDEM and You Should Too

by

Imma Valls Bernaus

PDF

Figma systems development services

by

davidjohansen1597

PDF

Artificial Intelligence Planning (Harinath Palavalli)

by

Harinath Palavalli

PDF

LogiNext Media Kit & Company Overview 2025

by

smritipatil055

Phone Tracker App for Family (2026)_ The Safe, Legit Way to Protect Loved One...

by

Mia Taylor

2026 Safety Roadmap: Systems, Skills, and Scale for EHS Leaders

by

TECH EHS Solution

AI-native development: from Prompt to Platform

by

Maxim Salnikov

Water Delivery App Development Solutions.pdf

by

eSiteWorld TechnoLabs Pvt. Ltd.

LogiNext Media Kit & Company Overview 2025

by

sanikaroy72

Edison MuleSoft Meetup : Vibe Coding | MuleSoft Meetups

by

Sravan Lingam

HackYourBrain_JFokusConference_03022026.pptx

by

SimonedeGijt

Visualizing Your Data Lake with Grafana - Amsterdam

by

Imma Valls Bernaus

Best eCommerce Development Agency in USA | The Dataflux

by

Key Medsolutions Inc

ChampionMATES – Compete With Friends. Predict Sports. Become the Champion.

by

Rafal Ksiazek

Build a Scalable On-Demand Courier Service App.pdf

by

V3CUBE TECHNOLABS

The Rise of Headless CMS in Modern Web Development.docx

by

work4noahmiller

LogiNext Media Kit & Company Overview 2025

by

nidhisharmaq7184

LogiNext Media Kit & Company Overview 2025

by

priyajoshi2929

Windows Server 2025 Administration Fundamentals 4ED

by

raynasolomon136

Smart ways to se AI in your business , presentation

by

AI n Dot Net

Why I Volunteer at FOSDEM and You Should Too

by

Imma Valls Bernaus

Figma systems development services

by

davidjohansen1597

Artificial Intelligence Planning (Harinath Palavalli)

by

Harinath Palavalli

LogiNext Media Kit & Company Overview 2025

by

smritipatil055

sensor_tower__state_of_mobile_2025__en.pdf

1.

The industry's leading

report Stateof Mobile2025 Report

2.

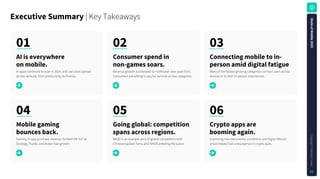

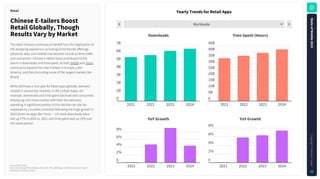

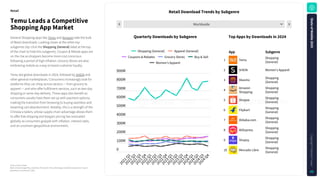

S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 02 ExecutiveSummary| Key Takeaways 04 02 05 03 06 Mobilegaming bouncesback. Consumerspendin non-gamessoars. Goingglobal:competition spansacrossregions. Connectingmobiletoin- personamiddigitalfatigue Cryptoappsare boomingagain. Gaming

in-app purchase revenue climbed 4% YoY as Strategy, Puzzle, and Action fuel growth. Revenue growth accelerated to +25% year-over-year (YoY). Consumers are willing to pay for services across categories. Retail is an example area of global competition with Chinese-backed Temu and SHEIN entering the space. Many of the fastest growing categories connect users across devices or to their in-person experiences. Improving macroeconomic conditions and higher Bitcoin prices helped fuel a resurgence in crypto apps. 01 AIiseverywhere onmobile. AI apps continued to soar in 2024, and use cases spread across verticals, from productivity to finance.

3.

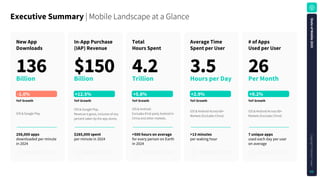

ExecutiveSummary| Mobile Landscape

at a Glance NewApp Downloads YoYGrowth iOS & Google Play 258,000apps downloaded per minute in 2024 136 Billion -1.0% In-AppPurchase (IAP)Revenue $150 Billion YoYGrowth iOS & Google Play. Revenue is gross, inclusive of any percent taken by the app stores. $285,000spent per minute in 2024 +12.5% Total HoursSpent 4.2 Trillion YoYGrowth iOS & Android. Excludes third-party Android in China and other markets. >500hoursonaverage for every person on Earth in 2024 +5.8% AverageTime SpentperUser 3.5 HoursperDay YoYGrowth iOS & Android Across 60+ Markets (Excludes China) >13minutes per waking hour +2.9% #ofApps UsedperUser 26 PerMonth YoYGrowth iOS & Android Across 60+ Markets (Excludes China) 7uniqueapps used each day per user on average +9.2% S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 03

4.

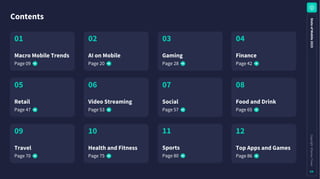

Contents S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 04 01 01 MacroMobileTrends Page 09 02 AIonMobile Page 20 03 Gaming Page

28 04 Finance Page 42 01 05 Retail Page 47 06 VideoStreaming Page 53 07 Social Page 57 08 FoodandDrink Page 65 11 Sports Page 80 10 HealthandFitness Page 75 01 09 Travel Page 70 12 TopAppsandGames Page 86

5.

Note: Top publishers

by app store revenue | Source: Sensor Tower SensorTower| Our Customers Top publishers trust Sensor Tower insights to grow their business. S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 05

6.

Next level insights. data.aiisnowpart ofSensorTower

7.

Aboutthisdata: Methodology SensorTower’sInsightsteamcompiledthedownloadandIAP revenueestimatesprovidedinthisreportusingtheSensor TowerMobileAppInsightsplatform. FigurescitedinthisreportreflectiOSAppStoreandGoogle PlaydownloadandrevenueestimatesforJanuary1,2014 throughDecember31,2024. Downloadestimatespresentedareonaper-userbasis, meaningthatonlyonedownloadperAppleorGoogle accountiscountedtowardsthetotal. Downloadsofthesameappbythesameusertomultiple devices,updates,orre-installsofthesameappbythesame userarenotcountedtowardsthetotal. Androidappdownloadandrevenueestimatesrepresent downloadsandrevenuefromtheGooglePlayStoreonly. SensorTowerdoesnotprovidedownloadestimatesforthird- partyAndroidstores. In-apppurchase(IAP)revenueestimatesaregross—inclusive ofanypercenttakenbytheappstores.Revenueincludespaid downloads,in-apppurchases,andsubscriptionsfromtheiOS AppStoreandGooglePlay.Thisdoesnotincludeanyrevenue fromadvertisementsorthird-partypurchases. ViewDetailedReportMethodologyHere. S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 07

8.

InterestedinourDigital MarketInsightsSolutions? If you want

to learn more about Sensor Tower, please request a demo: Get the latest insights on our blog: sensortower.com/blog Requestafreedemo!

9.

01 S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 09 Macro MobileTrends At Scopely, we

are driven by a culture of iteration and innovation - known as a ‘Learning Machine' - that empowers us to constantly analyze data, apply insights across our portfolio, and quickly pivot where needed. Sensor Tower plays a key role in fueling our ‘learning machine’ by helping us deeply understand the market and stay ahead of the curve in such a rapidly changing industry. JessicaZestar-Postrk SVP Strategy & Business Operations Scopely A maturing mobile market. Growth in time spent on mobile devices is slowing, while revenue continues to soar, particularly in non-games. Apps have consumers' attention — now they are monetizing it.

10.

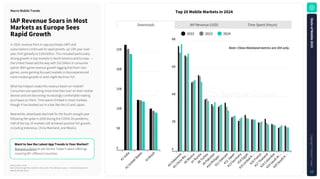

Source: Sensor Tower Note:

iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. Top20MobileMarketsin2024 WanttoSeetheLatestAppTrendsinYourMarket? Request a demo to see Sensor Tower's latest offerings covering 90+ different countries. IAPRevenueSoarsinMost MarketsasEuropeSees RapidGrowth In 2024, revenue from in-app purchases (IAP) and subscriptions continued its rapid growth, up 13% year-over- year (YoY) globally to $150 billion. This included particularly strong growth in top markets in North America and Europe — the United States led the way with $52 billion in consumer spend. With game revenue growth lagging that from non- games, some gaming-focused markets in Asia experienced more modest growth or even slight declines YoY. What has helped create this revenue boom on mobile? Consumers are spending more time than ever on their mobile devices and are becoming increasingly comfortable making purchases on them. Time spent climbed in most markets, though it has leveled out in a few like the US and Japan. Meanwhile, downloads declined for the fourth straight year following the spike in 2020 during the COVID-19 pandemic. Half of the top 10 markets still achieved positive YoY growth, including Indonesia, China Mainland, and Mexico. MacroMobileTrends Downloads IAP Revenue (USD) Time Spent (Hours) Rank 1 25B 20B 15B 10B 5B 0 # 1 I n d i a # 2 U n i t e d S t a t e s # 3 B r a z i l 8B 6B 4B 2B 0 # 4 I n d o n e s i a # 5 C h i n a M a … # 6 M e x i c o # 7 R u s s i a # 8 T u r k e y # 9 P a k i s t a n # 1 0 P h i l i p p i … # 1 1 V i e t n a m # 1 2 J a p a n # 1 3 G e r m a n y # 1 4 E g y p t # 1 5 U n i t e d K … # 1 6 F r a n c e # 1 7 T h a i l a n d # 1 8 C o l o m b i a # 1 9 S a u d i A r … # 2 0 S o u t h K … Note:ChinaMainlandmetricsareiOSonly. 2022 2024 2023 S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 10

11.

Source: Sensor Tower Note:

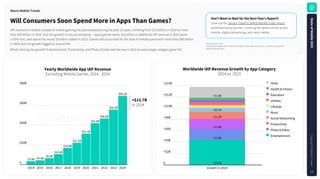

iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. YearlyWorldwideAppIAPRevenue Excluding Mobile Games, 2014 - 2024 WorldwideIAPRevenueGrowthbyAppCategory 2024 vs. 2023 Don'tWanttoWaitfortheNextYear'sReport? Look out for Sensor Tower's Digital Market Index report published every quarter, covering the latest trends across mobile, digital advertising, and retail media. WillConsumersSoonSpendMoreinAppsThanGames? IAP revenue on mobile outside of mobile gaming has skyrocketed during the past 10 years, climbing from $3.5 billion in 2014 to more than $69 billion in 2024. And this growth is only accelerating — apps gained nearly $14 billion in additional IAP revenue in 2024 alone (+25% YoY), well above the nearly $9 billion added in 2023. Games still accounted for the bulk of mobile spend with more than $80 billion in 2024, but YoY growth lagged at around 4%. What's driving the growth? Entertainment, Productivity, and Photo & Video led the way in 2024 as every single category grew YoY. MacroMobileTrends $80B $60B $40B $20B 0 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 $3.5B $4.4B $6.5B $10.6B $16.8B $22.1B $31.3B $41.8B $46.6B $55.5B $69.2B +$14B +$12B +$10B +$8B +$6B +$4B +$2B 0 Growth in 2024 +$4.4B +$1.9B +$1.8B +$1.2B +$0.7B +$1.9B Other Health&Fitness Education Utilities Lifestyle Music SocialNetworking Productivity Photo&Video Entertainment +$13.7B in 2024 S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 11

12.

Source: Sensor Tower Note:

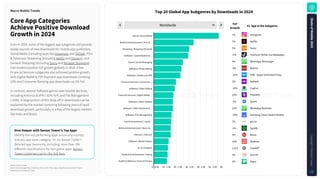

iOS and Google Play combined. iOS only for China. Apps classified using Sensor Tower's taxonomy as of January 5, 2025. Top20GlobalAppSubgenresbyDownloadsin2024 DiveDeeperwithSensorTower'sTopApps Identify the top performing apps across any country and any app store category. Or, try Sensor Tower's detailed app taxonomy, including more than 180 different classifications for non-game apps. Sensor Tower customers can try the link here. CoreAppCategories AchievePositiveDownload Growthin2024 MacroMobileTrends 1% Instagram 7% Netflix 5% Temu -5% TickTock-TikTok Live Wallpaper 4% WhatsApp Messenger -8% Remini -32% VPN - Super Unlimited Proxy 2% Nubank -10% CapCut 10% PhonePe -5% Quark 12% WhatsApp Business -24% Samsung Smart Switch Mobile 7% gov.br -6% Spotify 3% MyJio 10% DDMusic 112% ChatGPT 5% OmeTV 3% fitpro Worldwide Social | Social Media Media & Entertainment | Film &… Shopping | Shopping (General) Software | Customization &… Social | Social Messaging Software | Photo Editing Software | Antivirus & VPN Financial Services | Consumer… Software | Video Editing Financial Services | Digital Wallet… Software | Other Utilities Software | Other Business &… Software | File Management Law & Government | Law &… Media & Entertainment | Music &… Telecom | Telecom Software | Media Players AI | AI Chatbots Media & Entertainment | Dating Health & Wellness | Gyms & Fitness 0 0.5B 1B 1.5B 2B 2.5B 3B 3.5B 4B 4.5B 5B 5.5B 6B YoY Growth #1 AppintheSubgenre Even in 2024, some of the biggest app subgenres still provide stable sources of new downloads for mobile app publishers. Social Media (including apps like Instagram and TikTok), Film & Television Streaming (including Netflix and Disney+), and General Shopping (including Temu and Amazon Shopping) had modest positive YoY growth globally in 2024. A few Financial Services subgenres also achieved positive growth, with Digital Wallet & P2P Payment app downloads climbing 10% and Consumer Banking app downloads up 2% YoY. In contrast, several Software genres saw notable declines, including Antivirus & VPN (-32% YoY) and File Management (-24%). A large portion of this drop off in downloads can be explained by the market correcting following years of rapid download growth, particularly in a few of the largest markets like India and Brazil. S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 12

13.

Source: Sensor Tower Note:

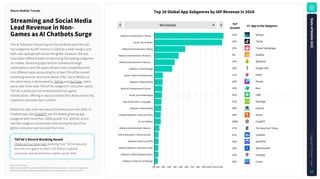

iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. Apps classified using Sensor Tower's taxonomy as of January 5, 2025. Top20GlobalAppSubgenresbyIAPRevenuein2024 TikTok'sRecord-BreakingAscent Check out our blog post studying how TikTok became the first non-game to reach $15 billion in global consumer spend and how it stacks up all-time. StreamingandSocialMedia LeadRevenueinNon- GamesasAIChatbotsSurge MacroMobileTrends 31% Disney+ 29% TikTok 13% Tinder Dating App 9% Audible 18% QQ Music 29% Google One 11% ESPN 16% Picsart 16% Azar 14% LINE 31% Duolingo 59% CapCut 18% Strava 209% ChatGPT 27% The New York Times 22% LinkedIn 20% NordVPN 10% MyFitnessPal 12% FaceApp 26% Canva Worldwide Media & Entertainment | Film &… Social | Social Media Media & Entertainment | Dating Media & Entertainment | Books &… Media & Entertainment | Music &… Software | Cloud Storage Sports | Sports Entertainment Software | Photo Editing Media & Entertainment | Social… Social | Social Messaging Jobs & Education | Language… Software | Video Editing Health & Wellness | Gyms & Fitness AI | AI Chatbots Media & Entertainment | News &… Jobs & Education | Jobs & Educati… Software | Antivirus & VPN Health & Wellness | Nutrition & Diet Software | Selfie & Beauty Editors Software | Poster & Card Design 0 $1B $2B $3B $4B $5B $6B $7B $8B $9B $10B $11B $12B YoY Growth Film & Television Streaming and Social Media were the top two subgenres by IAP revenue in 2024 by a wide margin, and both saw rapid growth across the globe. However, the two have taken different paths to becoming the leading subgenres on mobile. Streaming apps tend to monetize through subscriptions, and the space remains very competitive with nine different apps accounting for at least 3% of the overall streaming revenue (and none above 15%). Social Media, on the other hand, is dominated by TikTok and YouTube, which alone take more than 70% of the subgenre's consumer spend. TikTok in particular has revolutionized non-game monetization, offering in-app purchases that allow users to tip creators or promote their content. Mobile has also risen the wave of AI enthusiasm into 2024. AI Chatbot apps like ChatGPT was the fastest growing app subgenre with more than 200% growth YoY, and the at this rate the subgenre could easily rank among the top 10 by global consumer spend a year from now. #1 AppintheSubgenre S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 13

14.

Source: Sensor Tower Note:

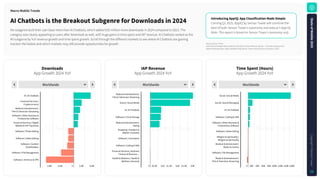

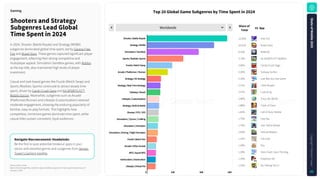

iOS and Google Play combined. iOS only for China. Apps classified using Sensor Tower's taxonomy as of January 5, 2025. Top20GlobalAppSubgenresbyTotalTimeSpent(Hours)in2024 UnlockSensorTower'sAppUsageMetrics Sensor Tower's usage metrics let you dive deep into in- app usage behavior. Based on the world’s largest proprietary mobile app panel, benchmark time spent, sessions, active users, and more. Check it out here. ConsumersSpentNearly 2.4TrillionHoursonSocial MediaAppsin2024—or6.6 BillionHoursEachDay MacroMobileTrends Worldwide Social | Social Media Social | Social Messaging Software | Browsers Media & Entertainment | Film &… Software | Calling & SMS Media & Entertainment | Music &… Shopping | Shopping (General) Software | Other Business &… Software | Customization &… Software | Other Utilities Software | Media Players Software | Photo Galleries Software | Email Media & Entertainment | Books &… Travel & Tourism | Navigation &… Software | Cloud Storage AI | AI Chatbots Financial Services | Consumer… Media & Entertainment | Dating Financial Services | Digital Wallet… 0 0.2T 0.4T 0.6T 0.8T 1T 1.2T 1.4T 1.6T 1.8T 2T 2.2T 2.4T 6% TikTok 2% WhatsApp Messenger 1% Google Chrome -5% Disney+ Hotstar 16% Truecaller 6% Spotify 9% Shopee 15% WhatsApp Business 21% HiOS Launcher 22% Clock 9% PLAYit 14% Google Photos 3% Gmail -8% WEBTOON 2% Google Maps 3% Google Drive 347% Character AI 7% SberBank Online 3% Badoo 21% Google Pay YoY Growth Mobile users spent nearly 2.4 trillion hours on Social Media apps in 2024 across iOS and Android devices, up 6% YoY. This was equivalent to 6.6 billion hours per day, or roughly an average of 50 minutes for every person on Earth. Messaging apps were a distant second at 607 billion hours, followed by Browsers at 330 billion hours. Time spent growth in AI Chatbot apps even outpaced the downloads, with more than 300% YoY growth. Consumers spent more than 7 billion hours in apps like Character AI and ChatGPT. Another fast growing subgenre was Digital Wallets & P2P Payments, which saw time spent climb 21% YoY. This included strong growth across many APAC and Latin America markets such as India, Indonesia, South Korea, and Argentina. #1 AppintheSubgenre S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 14

15.

Source: Sensor Tower Note:

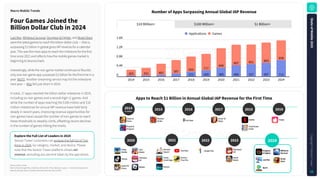

iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. Apps classified using Sensor Tower's taxonomy as of January 5, 2025. Downloads App Growth 2024 YoY IAPRevenue App Growth 2024 YoY TimeSpent(Hours) App Growth 2024 YoY IntroducingAppIQ:AppClassificationMadeSimple Coming Q1 2025, AppIQ by Sensor Tower will combine the best of both Sensor Tower’s taxonomy and data.ai’s App IQ. Note: This report is based on Sensor Tower's taxonomy only. AIChatbotsistheBreakoutSubgenreforDownloadsin2024 No subgenre built their user base more than AI Chatbots, which added 635 million more downloads in 2024 compared to 2023. The category was clearly appealing to users after download as well, with huge gains in time spent and IAP revenue. AI Chatbots ranked as the #3 subgenre by YoY revenue growth and time spent growth. Scroll through the different markets to see where AI Chatbots are gaining traction the fastest and which markets may still provide opportunities for growth. MacroMobileTrends Worldwide AI | AI Chatbots Financial Services | Cryptocurrency Media & Entertainment | Film & Television Streaming Software | Other Business & Productivity Software Financial Services | Digital Wallets & P2P Payments Software | Photo Editing Software | Video Editing Software | Content Downloaders Software | File Management Software | Antivirus & VPN -0.8B -0.4B 0 0.4B 0.8B Worldwide Media & Entertainment | Film & Television Streaming Social | Social Media AI | AI Chatbots Software | Cloud Storage Media & Entertainment | Dating Shopping | Sneakers & Athletic Footwear Software | Calculators Software | Calling & SMS Financial Services | Business Finance & Business… Health & Wellness | Health & Wellness (General) 0 $0.5B $1B $1.5B $2B $2.5B $3B Worldwide Social | Social Media Social | Social Messaging AI | AI Chatbots Software | Calling & SMS Software | Other Business & Productivity Software Software | Video Editing Religion & Spirituality | Religion & Spirituality Media & Entertainment | Books & Comics Software | File Management Media & Entertainment | Film & Television Streaming 0 20B 40B 60B 80B 100B 120B 140B 160B S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 15

16.

Source: Sensor Tower Note:

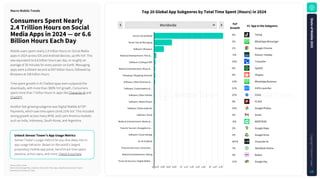

iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. Includes estimates since the start of 2014. NumberofAppsSurpassingAnnualGlobalIAPRevenue ExploretheFullListofLeadersin2024 Sensor Tower customers can explore the full list of Top Apps in 2024, by category, market, and device. Please note that the Sensor Tower platform shows net revenue, excluding any percent taken by the app stores. FourGamesJoinedthe BillionDollarClubin2024 LastWar,WhiteoutSurvival,Dungeon&Fighter,andBrawlStars werethelatestgamestoreachthebilliondollarclub—thatis, surpassing$1billioninglobalgrossIAPrevenueforacalendar year.Thiswasthemostappstoreachthemilestoneforthefirst timesince2021andreflectshowthemobilegamesmarketis beginningtobounceback. Interestingly,whilethenon-gamemarketcontinuestoflourish, onlyonenon-gameappsurpassed$1billionforthefirsttimeina year:WeTV. Another streaming service may hit the milestone next year — Max fell just short in 2024. In total, 17 apps reached the billion dollar milestone in 2024, including six non-games and a record-high 11 games. And while the number of apps reaching the $100 million and $10 million milestones for annual IAP revenue have held fairly steady in recent years, improving revenue opportunities for non-games have caused the number of non-games to reach these thresholds to steadily climb, offsetting recent declines in the number of games hitting the marks. MacroMobileTrends AppstoReach$1BillioninAnnualGlobalIAPRevenuefortheFirstTime $10 Million+ $100 Million+ $1 Billion+ 1.6K 1.2K 0.8K 0.4K 0 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 265 331 482 587 211 655 269 717 385 848 489 897 537 851 597 883 711 858 Applications Games 2014 orearlier 0NewApps 2015 2016 2017 2019 2018 2020 2021 2022 2023 Clashof Clans Puzzle& Dragons Monster Strike Honorof Kings Fate/Grand Order Netflix Tinder Coin Master PUBG Mobile Pokémon GO TikTok Gamefor Peace Roblox YouTube Genshin Impact Garena FreeFire Candy CrushSaga Disney+ GoogleOne Monopoly GO Royal Match 2024 Whiteout Survival Dungeon &Fighter LastWar Brawl Stars WeTV S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 16

17.

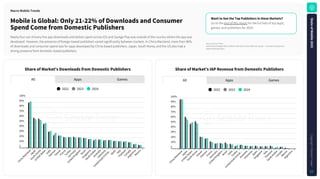

Source: Sensor Tower Note:

iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. ShareofMarket'sDownloadsfromDomesticPublishers ShareofMarket'sIAPRevenuefromDomesticPublishers MobileisGlobal:Only21-22%ofDownloadsandConsumer SpendComefromDomesticPublishers Nearly four out of every five app downloads and dollars spent across iOS and Goolge Play was outside of the country where the app was developed. However, the presence of foreign-based publishers varied significantly between markets. In China Mainland, more than 90% of downloads and consumer spend was for apps developed by China-based publishers. Japan, South Korea, and the US also had a strong presence from domestic-based publishers. MacroMobileTrends All Apps Games 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0 C h i n a M a i n l a n d J a p a n S o u t h K o r e a U n i t e d S t a t e s I n d i a V i e t n a m T a i w a n F r a n c e T u r k e y G e r m a n y U n i t e d K i n g d o m B r a z i l S i n g a p o r e S a u d i A r a b i a A u s t r a l i a I n d o n e s i a U n i t e d A r a b E m i r a t … S p a i n I t a l y T h a i l a n d C a n a d a A r g e n t i n a M e x i c o 2022 2023 2024 All Apps Games 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0 C h i n a M a i n l a n d J a p a n U n i t e d S t a t e s S o u t h K o r e a T a i w a n V i e t n a m F r a n c e G e r m a n y U n i t e d K i n g d o m B r a z i l I n d i a T u r k e y U n i t e d A r a b E m i r a t … A u s t r a l i a I n d o n e s i a S p a i n S i n g a p o r e I t a l y T h a i l a n d S a u d i A r a b i a C a n a d a M e x i c o A r g e n t i n a 2022 2023 2024 WanttoSeetheTopPublishersintheseMarkets? Go to the end of this report for the full lists of top apps, games, and publishers for 2024. S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 17

18.

Source: Sensor Tower Note:

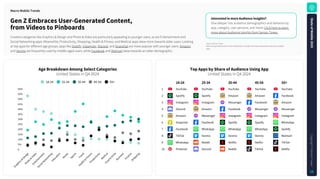

Among Android users in the United States. Includes YouTube and excludes other pre-installed apps. AgeBreakdownAmongSelectCategories United States in Q4 2024 InterestedinmoreAudienceInsights? Dive deeper into audience demographics and behavior by app, category, user persona, and more! Click here to learn more about Audience Insights from Sensor Tower. GenZEmbracesUser-GeneratedContent, fromVideostoPinboards Creative categories like Graphics & Design and Photo & Video are particularly appealing to younger users, as are Entertainment and Social Networking apps. Meanwhile, Productivity, Shopping, Health & Fitness, and Medical apps skew more towards older users. Looking at top apps for different age groups, apps like Spotify, Instagram, Discord, and Snapchat are more popular with younger users. Amazon and Venmo are frequently used by middle-aged users, while Facebook and Walmart skew towards an older demographic. MacroMobileTrends TopAppsbyShareofAudienceUsingApp United States in Q4 2024 YouTube YouTube YouTube YouTube YouTube Spotify Spotify Amazon Amazon Facebook Instagram Instagram Messenger Facebook Amazon Discord Amazon Facebook Messenger Messenger Amazon Messenger Instagram Instagram Instagram Snapchat Facebook Spotify Spotify WhatsApp Facebook WhatsApp WhatsApp WhatsApp Spotify TikTok Venmo Venmo Venmo Walmart WhatsApp Reddit Netflix Netflix TikTok Pinterest Discord Reddit TikTok Netflix 1 2 3 4 5 6 7 8 9 10 18-24 25-34 35-44 45-54 55+ 0 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60% G r a p h i c s & D e s i g n P h o t o & V i d e o E n t e r t a i n m e n t S o c i a l N e t w o r k i n g E d u c a t i o n B o o k s S p o r t s T r a v e l H e a l t h & F i t n e s s P r o d u c t i v i t y M e d i c a l F o o d & D r i n k B u s i n e s s F i n a n c e S h o p p i n g 18-24 25-34 35-44 45-54 55+ S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 18

19.

Source: Sensor Tower Note:

Among Android users in the United States. Includes YouTube and excludes other pre-installed apps. Gender represented as Men and Women only and is not representative of all gender identities. GenderBreakdownAmongSelectCategories United States in Q4 2024 S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 19 Graphics&DesignandShoppingSkewTowardsWomen For the Graphics & Design, Shopping, and Books categories, women outnumber men by at least two to one in the United States on average. Sports, Finance, Travel, and Business are more commonly used by men on average. Top apps tend to have a large user base with both men and women, but a few apps rank among the top 10 for one gender. Discord and Reddit are among the top 10 for men only, while Pinterest and TikTok rank among the top 10 for women. MacroMobileTrends 0 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% G r a p h i c s & D e s i g n S h o p p i n g B o o k s E n t e r t a i n m e n t M e d i c a l F o o d & D r i n k S o c i a l N e t w o r k i n g H e a l t h & F i t n e s s P r o d u c t i v i t y E d u c a t i o n P h o t o & V i d e o T r a v e l B u s i n e s s F i n a n c e S p o r t s Men Women TopAppsbyShareofAudienceUsingApp United States in Q4 2024 YouTube YouTube Spotify Instagram Instagram Spotify Amazon Amazon Facebook Pinterest WhatsApp Facebook Messenger Messenger Discord WhatsApp Reddit TikTok Snapchat Venmo 1 2 3 4 5 6 7 8 9 10 Men Women SensorTowerCustomersCanExploreMore! Sensor Tower customer? Check out Audience Insights here for more categories, user personas, and so much more.

20.

02 S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 20 AIon Mobile AI continued its

rapid ascent on mobile in 2024. Generative AI was the breakout mobile genre, and market leaders across verticals found creative new ways to integrate AI into their mobile solutions. Fetch is America’s Rewards App because we’re obsessed with innovation that delivers real value to both brands and consumers. As mobile apps continue to drive the rise of e-commerce, Fetch is leading the way by expanding our rewards ecosystem into new consumer categories and introducing groundbreaking features like Fetch Play and Fetch Shop. Powered by patented AI and ML integrations, our mobile platform transforms everyday purchases and activities into highly personalized, rewarding experiences. We're redefining how people connect with the brand they love and find new ones to fall in love with, by creating a first-of-its-kind, rewards-based advertising ecosystem that delivers both rational and emotional value. AyoJimoh Chief Product Officer Fetch

21.

Worldwide 1 Rank Source: Sensor Tower Note:

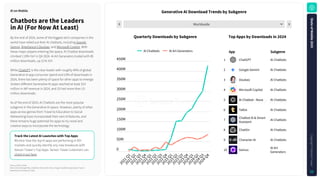

iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. AI apps classified using Sensor Tower's taxonomy as of January 5, 2025. YearlyTrendsforGenerativeAIApps WantMoreAIInsights? Check out our report covering the AI app market from 2024. And since the AI app market is ever evolving, look out for more AI-related content on our blog. AIAppsareAlready aBillionDollarIndustry Generative AI apps exploded onto the scene in late 2022 with interest in the technology surging following the release of ChatGPT. Other competitors quickly attempted to capture some of this market. IAP revenue from AI Chatbot and AI Art Generators climbed from $30 million in 2022 to $455 million in 2023 to nearly $1.3 billion in 2024. Downloads saw a similar trajectory, approaching 1.5 billion in 2024. The United States is the clear top market for Generative AI apps in 2024, accounting for 45% of global revenue. The United Kingdom is second with around 4% of total revenue, followed by Germany (4%), Japan (3%), and Canada (3%). The genre is also quite popular in Brazil, which ranks #7 for Generative AI (and outside the top 10 markets by overall mobile consumer spend). Generative AI revenue is lagging a bit in China Mainland, which accounted for less than 2% of the genre's IAP revenue in 2024. AIonMobile Downloads IAPRevenue 1.6B 1.4B 1.2B 1B 0.8B 0.6B 0.4B 0.2B 0 2021 2022 2023 2024 $1.2B $1B $0.8B $0.6B $0.4B $0.2B 0 2021 2022 2023 2024 600% 450% 300% 150% 0 2021 2022 2023 2024 YoYGrowth 1.6K% 1.2K% 0.8K% 0.4K% 0 2021 2022 2023 2024 YoYGrowth S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 21

22.

Source: Sensor Tower Note:

iOS and Google Play combined. iOS only for China. AI apps classified using Sensor Tower's taxonomy as of January 5, 2025. GenerativeAIDownloadTrendsbySubgenre TracktheLatestAILauncheswithTopApps Monitor how the top AI apps are performing in 90+ markets and quickly identify any new breakouts with Sensor Tower's Top Apps. Sensor Tower customers can check it out here. ChatbotsaretheLeaders inAI(ForNowAtLeast) By the end of 2024, some of the biggest tech companies in the world have rolled out their AI chatbots, including Google Gemini, ByteDance's Doubao, and Microsoft Copilot. With these major players entering the space, AI Chatbot downloads climbed 119% YoY in Q4 2024. AI Art Generators trailed with 85 million downloads, up 21% YoY. While ChatGPT is the clear leader with roughly 40% of global Generative AI app consumer spend and 23% of downloads in 2024, there has been plenty of space for other apps to emerge. Sixteen different Generative AI apps reached at least $10 million in IAP revenue in 2024, and 25 had more than 10 million downloads. As of the end of 2024, AI Chatbots are the most popular subgenre in the Generative AI space. However, plenty of other apps across genres from Travel to Education to Social Networking have incorporated their own AI features, and there remains huge potential for apps to try novel and creative ways to incorporate the technology AIonMobile Worldwide 1 Rank 0 50M 100M 150M 200M 250M 300M 350M 400M 450M 2 0 2 1 Q 1 2 0 2 1 Q 2 2 0 2 1 Q 3 2 0 2 1 Q 4 2 0 2 2 Q 1 2 0 2 2 Q 2 2 0 2 2 Q 3 2 0 2 2 Q 4 2 0 2 3 Q 1 2 0 2 3 Q 2 2 0 2 3 Q 3 2 0 2 3 Q 4 2 0 2 4 Q 1 2 0 2 4 Q 2 2 0 2 4 Q 3 2 0 2 4 Q 4 AI Chatbots AI Art Generators ChatGPT AI Chatbots Google Gemini AI Chatbots Doubao AI Chatbots Microsoft Copilot AI Chatbots AI Chatbot - Nova AI Chatbots Talkie AI Chatbots Chatbot AI & Smart Assistant AI Chatbots ChatOn AI Chatbots Character AI AI Chatbots Genius AI Art Generators 1 2 3 4 5 6 7 8 9 10 App Subgenre TopAppsbyDownloadsin2024 QuarterlyDownloadsbySubgenre S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 22

23.

Source: Sensor Tower Note:

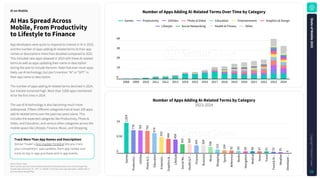

Includes apps with at least 50,000 worldwide all-time downloads across iOS and Google Play. Includes apps mentioning "AI", "GPT", or "OpenAI" in their app name, app description, subtitle (iOS), or short description (Google Play). NumberofAppsAddingAI-RelatedTermsOverTimebyCategory TrackMoreThanAppNamesandDescriptions Sensor Tower's App Update Timeline lets you track your competitors' app updates, from app names and icons to top in-app purchase and in-app events. AIHasSpreadAcross Mobile,FromProductivity toLifestyletoFinance AIonMobile NumberofAppsAddingAI-RelatedTermsbyCategory 2023-2024 4K 3K 2K 1K 0 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 Games Productivity Utilities Photo & Video Education Entertainment Graphics & Design Lifestyle Social Networking Health & Fitness Other 1K 0.5K 0 G a m e s P r o d u c t i v i … U t i l i t i e s P h o t o & V … E d u c a t i o n E n t e r t a i n … G r a p h i c s & … L i f e s t y l e S o c i a l N e … H e a l t h & F … F i n a n c e B u s i n e s s M u s i c S h o p p i n g S p o r t s R e f e r e n c e B o o k s N a v i g a t i o n M e d i c a l N e w s T r a v e l F o o d & D r … W e a t h e r D e v e l o p e r … 1 , 0 2 4 7 7 8 7 6 3 7 5 2 6 7 4 5 4 3 4 8 4 4 5 9 3 0 3 3 0 2 2 6 5 2 6 4 2 0 8 1 2 2 1 0 4 9 2 8 3 6 9 6 8 6 7 6 1 5 3 3 5 6 App developers were quick to respond to interest in AI in 2023, and the number of apps adding AI-related terms to their app names or descriptions more than doubled compared to 2022. This included new apps released in 2023 with these AI-related terms as well as apps updating their name or description during the year to include the term. Note that even more apps likely use AI technology, but don't mention "AI" or "GPT" in their app name or description. The number of apps adding AI-related terms declined in 2024, but interest remained high. More than 3,000 apps mentioned AI for the first time in 2024. The use of AI technology is also becoming much more widespread. Fifteen different categories had at least 100 apps add AI-related terms over the past two years alone. This includes the expected categories like Productivity, Photo & Video, and Education, and various other categories across the mobile space like Lifestyle, Finance, Music, and Shopping. S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 23

24.

Source: Sensor Tower Note:

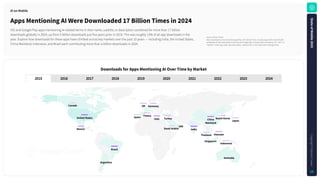

Downloads across iOS and Google Play. iOS only for China. Includes apps with at least 50,000 worldwide all-time downloads across iOS and Google Play. Includes apps mentioning "AI", "GPT", or "OpenAI" in their app name, app description, subtitle (iOS), or short description (Google Play). DownloadsforAppsMentioningAIOverTimebyMarket AppsMentioningAIWereDownloaded17BillionTimesin2024 iOS and Google Play apps mentioning AI-related terms in their name, subtitle, or description combined for more than 17 billion downloads globally in 2024, up from 5 billion downloads just five years prior in 2019. This was roughly 13% of all app downloads in the year. Explore how downloads for these apps have climbed across key markets over the past 10 years — including India, the United States, China Mainland, Indonesia, and Brazil each contributing more than a billion downloads in 2024. AIonMobile 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 India Brazil Mexico Canada Argentina Italy France Spain UAE SaudiArabia Australia Singapore UnitedStates Germany UK Turkey Indonesia Thailand Vietnam China Mainland Japan SouthKorea S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 24

25.

Source: Sensor Tower Note:

iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. DuolingoWorldwideMonthlyIAPRevenue StayAheadofCompetitors withAIInnovations AIonMobile UserRatingDistributionforReviewsMentioningNewAIFeatures United States on iOS Explain My Answer Video Call 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 5 Stars 4 Stars 3 Stars 2 Stars 1 Star In today's competitive mobile market, there is a growing trend of integrating AI-powered features into applications to attract tech-savvy users and enhance overall convenience. App developers should think carefully about how to integrate the technology in ways that will improve the user experience, rather than selling minor adjustments to existing features. Duolingo is an example of an app that was quick to embrace AI features, launching several GPT-4 powered offerings in March 2023 with Duolingo Max. However, many users did not see the improvements from AI and viewed this as charging a higher price for features that used to be provided under the cheaper Super subscription. Duolingo took a significant step forward by launching AI- powered video calls in September 2024. This new feature received positive feedback from users, highlighting its effectiveness in enhancing language practice through simulated real-life conversations and leaning on positive sentiment about a character in the app, Lily. The new offerings appear to be boosting revenue as well, with the app achieving its highest monthly YoY revenue growth since 2023. September2024: Duolingo introduced AI-powered features at Duocon, including AI-Powered Conversations: Video Call with Lily 0 $20M $40M $60M $80M 0 20% 40% 60% 80% J a n - 2 0 2 2 F e b - 2 0 2 2 M a r - 2 0 2 2 A p r - 2 0 2 2 M a y - 2 0 2 2 J u n - 2 0 2 2 J u l - 2 0 2 2 A u g - 2 0 2 2 S e p - 2 0 2 2 O c t - 2 0 2 2 N o v - 2 0 2 2 D e c - 2 0 2 2 J a n - 2 0 2 3 F e b - 2 0 2 3 M a r - 2 0 2 3 A p r - 2 0 2 3 M a y - 2 0 2 3 J u n - 2 0 2 3 J u l - 2 0 2 3 A u g - 2 0 2 3 S e p - 2 0 2 3 O c t - 2 0 2 3 N o v - 2 0 2 3 D e c - 2 0 2 3 J a n - 2 0 2 4 F e b - 2 0 2 4 M a r - 2 0 2 4 A p r - 2 0 2 4 M a y - 2 0 2 4 J u n - 2 0 2 4 J u l - 2 0 2 4 A u g - 2 0 2 4 S e p - 2 0 2 4 O c t - 2 0 2 4 N o v - 2 0 2 4 D e c - 2 0 2 4 I A P R e v e n u e Y o Y G r o w t h IAP Revenue YoY Growth March2023: Duolingo introduced a higher-priced subscription tier, Duolingo Max, offering GPT-4 powered features like Explain My Answer and Roleplay DiscoverHowUsersReacttoNewFeatures Review Analysis from Sensor Tower's App Performance Insights lets you search reviews by keyword AverageRating 2.7Stars 4.1Stars S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 25

26.

Source: Sensor Tower Note:

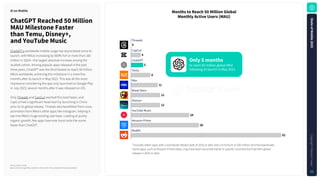

iOS and Google Play combined. iOS only for China. Excludes third-party Android. MonthstoReach50MillionGlobal MonthlyActiveUsers(MAU) AIonMobile ChatGPTReached50Million MAUMilestoneFaster thanTemu,Disney+, andYouTubeMusic ChatGPT's worldwide mobile usage has skyrocketed since its launch, with MAUs increasing by 500% YoY or more than 160 million in 3Q24—the largest absolute increase among the studied cohort. Among popular apps released in the past three years, ChatGPT was the third-fastest to reach 50 million MAUs worldwide, achieving this milestone in a mere five months after its launch in May 2023. This was all the more impressive considering the app only launched on Google Play in July 2023, several months after it was released on iOS. Only Threads and CapCut reached this level faster, and CapCut had a significant head start by launching in China prior to its global release. Threads also benefitted from cross- promotion from Meta's other apps like Instagram, helping it tap into Meta's huge existing user base. Looking at purely organic growth, few apps have ever burst onto the scene faster than ChatGPT. Threads CapCut ChatGPT Temu Max Brawl Stars Disney+ YouTube Music Amazon Prime Reddit 0 4 5 8 11 12 12 24 28 62 *Includes select apps with a worldwide release date of 2016 or later and a minimum of 100 million all-time downloads. Some apps, such as Amazon Prime Video, may have been launched earlier in specific countries but had their global release in 2016 or later. S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 26 to reach 50 million global MAU following its launch in May 2023 Only5months

27.

Source: Sensor Tower Note:

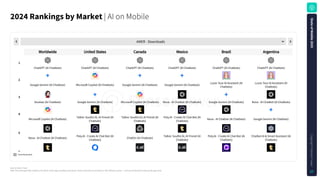

iOS and Google Play combined. iOS only for China. Apps classified using Sensor Tower's taxonomy as of January 5, 2025. Revenue is gross — inclusive of any percent taken by the app stores. 2024RankingsbyMarket| AI on Mobile Download data AMER - Downloads ChatGPT (AI Chatbots) ChatGPT (AI Chatbots) ChatGPT (AI Chatbots) ChatGPT (AI Chatbots) ChatGPT (AI Chatbots) ChatGPT (AI Chatbots) Google Gemini (AI Chatbots) Microsoft Copilot (AI Chatbots) Google Gemini (AI Chatbots) Google Gemini (AI Chatbots) Luzia: Your AI Assistant (AI Chatbots) Luzia: Your AI Assistant (AI Chatbots) Doubao (AI Chatbots) Google Gemini (AI Chatbots) Microsoft Copilot (AI Chatbots) Nova - AI Chatbot (AI Chatbots) Google Gemini (AI Chatbots) Nova - AI Chatbot (AI Chatbots) Microsoft Copilot (AI Chatbots) Talkie: Soulful AI, AI Friend (AI Chatbots) Talkie: Soulful AI, AI Friend (AI Chatbots) Poly.AI - Create AI Chat Bot (AI Chatbots) Nova - AI Chatbot (AI Chatbots) Google Gemini (AI Chatbots) Nova - AI Chatbot (AI Chatbots) Poly.AI - Create AI Chat Bot (AI Chatbots) ChatOn (AI Chatbots) Talkie: Soulful AI, AI Friend (AI Chatbots) Poly.AI - Create AI Chat Bot (AI Chatbots) Chatbot AI & Smart Assistant (AI Chatbots) 1 2 3 4 5 6 Worldwide United States Canada Mexico Brazil Argentina S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 27

28.

03 S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 28 Gaming Mobile gaming bounced

back with positive year-over-year IAP revenue growth for the first time since 2021. However, the landscape has changed over the past few years, with Strategy and Puzzle driving growth while RPG continued to decline. Data is paramount to everything we do internally at Kwalee, and at gaming companies in general, the sheer amount of data points we capture is mind-boggling. Sensor Tower adds the external dimension which gives us the comparable we need to understand if what we're doing is working? Has a market fit? And equally important, is potential trends for us to innovate on. JohnWright VP of Mobile Games Kwalee

29.

MobileGameIAPRevenueGrowth WanttoSeetheLatestGamingTrends? Monitor market movements

day-by-day with a Sensor Tower account to get the scoop on the latest shifts and emerging opportunities. MobileGameRevenueHits $80.9Billionin2024Amid ShiftingMarketDynamics Mobile game IAP revenue rose to $80.9 billion in 2024, up 4% YoY, even as downloads declined by 6% to 49.6 billion. This decline reflects market stabilization amid industry consolidation and broader tech sector pressures. Despite this, consumers are spending more time on mobile devices and increasingly making purchases, driven by improved gaming experiences and enhanced monetization strategies. Emerging markets like Mexico, India, and Thailand fueled much of the growth, with spending rising 21%, 17%, and 16%, respectively. Turkey led with a 28% increase, while Saudi Arabia posted a 14% rise. Established markets such as the US and EMEAR regions saw steady growth, while North Asia faced headwinds, with Japan experiencing a 7% decline due to economic and currency challenges. While most markets saw a decline in downloads, regions like Indonesia and Saudi Arabia provided bright spots of growth. Looking ahead to 2025, consumer spending is expected to climb further as developers prioritize retention and high- quality gaming experiences. Gaming MobileGameDownloadGrowth Worldwide $80B $60B $40B $20B 0 2021 2021-2022 Growth 2022-2023 Growth 2023-2024 Growth 2024 $86.8B -$8.1B -$0.5B $2.8B $80.9B Worldwide 60B 40B 20B 0 2021 2021-2022 Growth 2022-2023 Growth 2023-2024 Growth 2024 55.4B -0.2B -2.2B -3.3B 49.6B (+4% YoY) $80.9Billion 2024IAPRevenue (-6% YoY) 49.6Billion 2024Downloads Source: Sensor Tower App Performance Insights as of January 5, 2025. Note: iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 29

30.

Worldwide 2020 - Dec

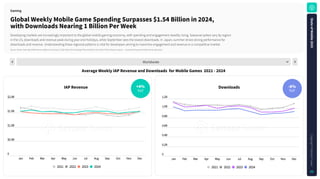

1.12 2021 - Jan 1.65 2021 - Feb 1.74 2021 - Mar 1.68 2021 - Apr 1.67 2021 - May 1.63 2021 - Jun 1.62 2021 - Jul 1.64 2021 - Aug 1.72 2021 - Sep 1.63 2021 - Oct 1.56 2021 - Nov 1.63 2021 - Dec 1.7 2022 - Jan 1.69 2022 - Feb 1.63 Week IAP Revenue Downloads Source: Sensor Tower App Performance Insights as of January 5, 2025. Note: iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. GlobalWeeklyMobileGameSpendingSurpasses$1.54Billionin2024, withDownloadsNearing1BillionPerWeek Developing markets are increasingly important to the global mobile gaming economy, with spending and engagement steadily rising. Seasonal spikes vary by region: in the US, downloads and revenue peak during year-end holidays, while September sees the lowest downloads. In Japan, summer drives strong performance for downloads and revenue. Understanding these regional patterns is vital for developers aiming to maximize engagement and revenue in a competitive market. Gaming IAPRevenue AverageWeeklyIAPRevenueandDownloads forMobileGames 2021-2024 -6% +4% YoY YoY 0 $0.5B $1.0B $1.5B $2.0B Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2021 2022 2023 2024 0 0.2B 0.4B 0.6B 0.8B 1.0B 1.2B Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2021 2022 2023 2024 S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 30

31.

Source: Sensor Tower.

Note: iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. Apps classified using Sensor Tower's Game taxonomy as of January 5, 2025. SimulationandPuzzleDominate2024MobileDownloads,StrategyShowingStrongMomentum In 2024, Simulation and Puzzle genres led global mobile game downloads, each capturing 20% of the total, with Simulation seeing slight growth (+0.4%) and Puzzle experiencing a modest decline (-3%). Arcade games, despite a significant 12.5% drop, maintained 19% of all downloads, reflecting their enduring popularity. Lifestyle and Action genres faced steeper declines, while Strategy games achieved notable growth (+14.5%) in downloads. Notably, Strategy games punched above their weight, commanding 21.4% of revenue despite accounting for only 4% of total downloads. These trends highlight a market where established genres continue to dominate, but emerging growth in niche categories offers new opportunities. Gaming 2024|WorldwideTopMobileGameGenresbyDownloads|PoweredbySensorTowerGameTaxonomy Worldwide S i m u l a t i o n Puzzle A r c a d e Lifestyle Tabletop Action Shooter Strategy S p o r t s R a c i n g R P G C a s i n o S i m u l a t o r D r i v i n g / F l i g h t S i m u l a t o r S a n d b o x Idler Tycoon/Crafting TimeManagement Others Riddle Physics Match Swap Sort Word MatchPair Environmental Block MatchMerge2 Others P l a t f o r m e r / R u n n e r O t h e r A r c a d e A r c a d e D r i v i n g M u s i c / R h y t h m A r c a d e C o m b a t . i o C u s t o m i z a t i o n VirtualPet Ultracasual Board Drawing&Coloring Others Action Sandbox Others FPS/3PS BattleRoyale Others 4XStrategy Others R e a l i s t i c S p o r t s A r c a d e S p o r t s A r c a d e R a c i n g O t h e r s O t h e r s O t h e r s #6 - Action #7 - Shooter #8 - Strategy #5 - Tabletop #2 - Puzzle #3 - Arcade #4 - Lifestyle #1 - Simulation YoY Downloads -7.3% YoY IAP Revenue +1.1% 5% of All Downloads 1.8% of All IAP Revenue 2.4 B in Downloads YoY Downloads -7.9% YoY IAP Revenue +46.0% 5% of All Downloads 4.4% of All IAP Revenue 2.4 B in Downloads YoY Downloads +1.5% YoY IAP Revenue +3.4% 5% of All Downloads 5.3% of All IAP Revenue 2.1 B in Downloads YoY Downloads +14.5% YoY IAP Revenue +16.2% 4% of All Downloads 21.4% of All IAP Revenue 2.6 B in Downloads YoY Downloads +0.4% YoY IAP Revenue +8.8% 20% of All Downloads 7.4% of All IAP Revenue 9.7 B in Downloads YoY Downloads -3.0% YoY IAP Revenue +14.0% 20% of All Downloads 14.9% of All IAP Revenue 9.6 B in Downloads YoY Downloads -12.5% YoY IAP Revenue -22.6% 19% of All Downloads 2.0% of All IAP Revenue 4.0 B in Downloads YoY Downloads -10.0% YoY IAP Revenue +51.4% 8% of All Downloads 2.5% of All IAP Revenue 9.8 B in Downloads S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 31

32.

Source: Sensor Tower Note:

iOS and Google Play combined. iOS only for China. Excludes third-party Android. Apps classified using Sensor Tower's Game taxonomy as of January 5, 2025. Top20GlobalGameSubgenresbyDownloadsin2024 ArcadePlatformerand SimulationSubgenresLed MobileGameDownloads in2024 Arcade Platformer/Runner games led global mobile game downloads in 2024, capturing 8.34% of the share, driven by the enduring popularity of Subway Surfers. Simulation subgenres followed closely, with Simulator (6.17%) and Driving/Flight Simulator (4.98%) reflecting strong interest in immersive, task- based gameplay exemplified by My Supermarket Simulator 3D and Vehicle Masters. Lifestyle Customization titles, led by Avatar World, gained traction, showcasing the growing appeal of personalization. Puzzle Riddle games, including Brain Test: Tricky Puzzles, maintained a steady 3.43% share. Meanwhile, Shooters such as Call of Duty: Mobile held competitive positions, underscoring sustained demand for action-packed experiences. The diverse performance across genres highlights a balanced demand for casual and immersive games, offering developers opportunities to innovate and adapt to evolving global player preferences. Gaming Worldwide Arcade | Platformer / Runner Simulation | Simulator Simulation | Driving / Flight Simulator Lifestyle | Customization Puzzle | Riddle Arcade | Other Arcade Racing | Arcade Racing Simulation | Sandbox Sports | Realistic Sports Action | Action Sandbox Lifestyle | Virtual Pet Shooter | FPS / 3PS Tabletop | Board Simulation | Idler Arcade | Arcade Driving Tabletop | Drawing & Coloring Arcade | Music / Rhythm Puzzle | Physics Puzzle | Match Swap Arcade | Arcade Combat 0 1,000M 2,000M 3,000M 4,000M 8.34% Subway Surfers 6.17% My Superstore Simulator 4.97% Vehicle Masters 4.11% Avatar World Games for Kids 3.43% Brain Test: Tricky Puzzles 3.39% Offline Games - No Wifi Games 2.81% Car Race 2.72% ROBLOX 2.43% 8 Ball Pool 2.29% Indian Bikes Driving 3D 2.27% My Talking Tom 2 2.25% Call of Duty: Mobile 2.19% Ludo King 2.11% My Perfect Hotel 2.00% Hill Climb Racing 1.88% Coloring Alphabet ASMR 1.85% Magic Tiles 3 1.77% Wood Nuts & Bolts Puzzle 1.61% Royal Match 1.60% Agent Hunt Shareof Total #1 App S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 32

33.

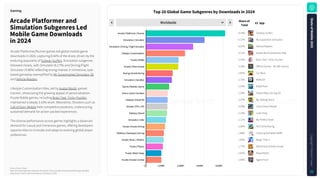

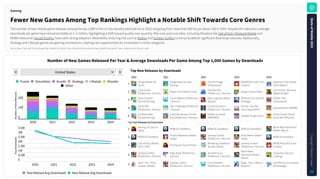

Source: Sensor Tower

Note: iOS and Google Play combined. iOS only for China. Excludes third-party Android. Apps classified using Sensor Tower's taxonomy as of January 5, 2025. FewerNewGamesAmongTopRankingsHighlightaNotableShiftTowardsCoreGenres The number of new mobile game releases among the top 1,000 in the US has steadily declined since 2020, dropping from more than 200 to just above 100 in 2024. Despite this reduction, average downloads per game have remained stable at 1–2 million, highlighting a shift toward quality over quantity. Mid-core and core titles, including Shooters like Call of Duty: Warzone Mobile and MOBA newcomer Squad Busters, have seen strong adoption. Meanwhile, enduring hits such as Roblox and Subway Surfers continue to deliver significant download volumes. Additionally, Strategy and Lifestyle games are gaining momentum, creating new opportunities for innovation in niche categories. Gaming NumberofNewGamesReleasedPerYear&AverageDownloadsPerGameAmongTop1,000GamesbyDownloads TopNewReleasesbyDownloads United States 200 100 0 2020 2021 2022 2023 2024 N u m b e r o f N e w R e l e a s e s Puzzle Simulation Arcade Strategy Lifestyle Shooter Other 0 0.5M 1M 1.5M 2M 2.5M 3M 3.5M 2020 2021 2022 2023 2024 A v g D o w n l o a d s Past Release Avg Downloads New Release Avg Downloads 1 Tangle Master 3D (Sort) Bridge Race (Arcade Racing) Fill The Fridge (Ultracasual) MONOPOLY GO! (Coin Looters) Pokémon TCG Pocket (Card Battler) 2 Cube Surfer (Platformer / Runner) Paper Fold (Other Puzzle) Tall Man Run (Platformer / Runner) Burger Please (Idler) Call of Duty: Warzone (Battle Royale) 3 Draw Climber (Arcade Racing) Count Masters (Platformer / Runner) Apex Legends (Battle Royale) Whiteout Survival (4X Strategy) Perfect Tidy (Ultracasual) 4 Spiral Roll (Platformer / Runner) Hair Challenge (Platformer / Runner) Crowd Evolution (Platformer / Runner) Honkai: Star Rail (Turn-based RPG) Squad Busters (MOBA) 5 Scribble Rider (Arcade Racing) Crash Bandicoot: On the Run (Platformer / Runner) Diablo Immortal (MMORPG) Twisted Tangle (Sort) Screw Puzzle: Wood Nut & Bolt (Physics) Top Past Releases by Downloads 1 Among Us! (Social Party) ROBLOX (Sandbox) ROBLOX (Sandbox) ROBLOX (Sandbox) Block Blast Adventure Master (Block) 2 ROBLOX (Sandbox) Project Makeover (Match Swap) Subway Surfers (Platformer / Runner) Royal Match (Match Swap) ROBLOX (Sandbox) 3 Call of Duty: Mobile (FPS / 3PS) Among Us! (Social Party) Wordle by Goldfinch Studios (Word) Subway Surfers (Platformer / Runner) MONOPOLY GO! (Coin Looters) 4 Subway Surfers (Platformer / Runner) High Heels (Platformer / Runner) Stumble Guys (Platformer / Runner) Block Blast Adventure Master (Block) Township (Tycoon / Crafting) 5 Brain Test: Tricky Puzzles (Riddle) Subway Surfers (Platformer / Runner) Count Masters (Platformer / Runner) Magic Tiles 3 (Music / Rhythm) Last War:Survival Game (4X Strategy) 2020 2021 2022 2023 2024 S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 33

34.

Worldwide 1 Rank Source: Sensor TowerNote:

iOS and Google Play combined. iOS only for China. Excludes third-party Android. Apps classified using Sensor Tower's taxonomy as of January 5, 2025. GeolocationShowsHighestMarketConcentrationWhileSportsandArcadeLeadinLongevity Gaming 2024|TopGenrePerMarketConcentrationbyDownloads Geolocation Shooter Sports Racing Strategy Tabletop Casino Action Lifestyle RPG Simulation Arcade Puzzle 0% 20% 40% 60% 80% 100% 72.1% 72.1% 72.1% 25.1% 25.1% 25.1% 21.5% 21.5% 21.5% 22.0% 22.0% 22.0% 56.5% 56.5% 56.5% 14.8% 14.8% 14.8% 25.1% 25.1% 25.1% 60.0% 60.0% 60.0% 13.4% 13.4% 13.4% 31.9% 31.9% 31.9% 54.8% 54.8% 54.8% 13.0% 13.0% 13.0% 35.4% 35.4% 35.4% 51.6% 51.6% 51.6% 12.7% 12.7% 12.7% 20.9% 20.9% 20.9% 66.4% 66.4% 66.4% 11.5% 11.5% 11.5% 20.1% 20.1% 20.1% 68.4% 68.4% 68.4% 9.4% 9.4% 9.4% 23.5% 23.5% 23.5% 67.0% 67.0% 67.0% 7.3% 7.3% 7.3% 19.7% 19.7% 19.7% 73.1% 73.1% 73.1% 17.9% 17.9% 17.9% 76.5% 76.5% 76.5% 8.6% 8.6% 8.6% 86.2% 86.2% 86.2% 13.0% 13.0% 13.0% 82.3% 82.3% 82.3% 9.7% 9.7% 9.7% 85.7% 85.7% 85.7% Top 3 Game Share of Market Top 20 Share of Market Rest of Market Top3Games 20% 40% 60% 80% 100% 86.7% 15.0% 79.6% 9.8% 85.0% 21.4% 70.2% 9.4% 13.2% 72.5% 15.1% 77.5% 8.4% 15.1% 74.2% 20.2% 70.5% 8.6% 22.0% 66.9% 11.5% 19.9% 20.7% 47.9% 10.1% 21.7% 62.9% 17.0% 73.9% 12.7% 23.0% 59.2% < 6 Mths 6 Mths to 1 Yr 1 to 2 Yrs > 2 Yrs ShareofDownloadsbyTimeSinceRelease TopGenrebyMarketConcentration In 2024, Geolocation games exhibited the highest market concentration, with the top three titles accounting for 72.1% of downloads, significantly outpacing Shooter (21.5%) and Sports (14.8%), which faced broader competition. Meanwhile, Simulation, Arcade, and Puzzle genres remained highly fragmented, with more than 80% of downloads distributed across smaller games. Geolocation and Sports genres also leaned heavily on older titles. In contrast, RPG games saw less than 50% of downloads driven by older titles, highlighting the competitive momentum and appeal of newer releases. S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 34

35.

Gaming 2024|WorldwideTopMobileGameGenresbyIAPRevenue|PoweredbySensorTowerGameTaxonomy Worldwide S t r a t e g y RPG P u z z l e Casino Simulation Shooter Action S p o r t s L i f e s t y l e A r c a d e T a b l e t o p 4 X S t r a t e g y MOBA Real-TimeStrategy CardBattler TowerDefense Others Squad RPG MMORPG PuzzleRPG Turn-basedRPG I d l e R P G M a t c h S w a p M a t c h M e r g e 2 M a t c h P a i r O t h e r s S l o t s CoinLooters Others Tycoon /

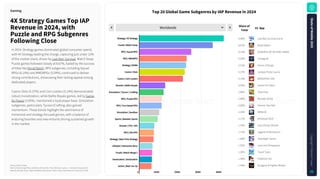

Crafting Sandbox Others BattleRoyale FPS/3PS Beat'emUp Others R e a l i s t i c S p o r t s O t h e r s I n t e r a c t i v e S t o r y O t h e r s O t h e r s G e o l o c a t i o n StrategyandRPGLeadGlobalConsumerSpendin2024 In 2024, Strategy games topped global consumer spending with $17.5 billion, closely followed by RPGs at $16.8 billion. Puzzle and Casino genres secured third and fourth positions, contributing $12.2 billion and $11.7 billion, respectively, with Puzzle games showcasing robust monetization despite declining downloads. Action, Simulation, and Shooter genres recorded significant growth, with Action leading the way in revenue gains (+46%). Sports games, though facing a drop in downloads, still generated $2.7 billion. These trends underline the strong monetization potential of competitive and immersive genres such as Strategy, RPG, and Action, which continue to captivate players globally. #2 - RPG #3 - Puzzle #4 - Casino #1 - Strategy #6 - Shooter #7 - Action #8 - Sports #5 - Simulation YoY IAP Revenue +16.2% YoY Downloads +14.5% 21.4% of All IAP Revenue 4% of All Downloads $16.8 B in IAP Revenue YoY IAP Revenue -17.3% YoY Downloads -6.1% 20.5% of All IAP Revenue 3% of All Downloads $12.2 B in IAP Revenue YoY IAP Revenue +14.0% YoY Downloads -3.0% 14.9% of All IAP Revenue 20% of All Downloads $11.7 B in IAP Revenue YoY IAP Revenue +8.9% YoY Downloads -39.6% 14.3% of All IAP Revenue 2% of All Downloads $17.5 B in IAP Revenue YoY IAP Revenue +8.8% YoY Downloads +0.4% 7.4% of All IAP Revenue 20% of All Downloads $4.3 B in IAP Revenue YoY IAP Revenue +3.4% YoY Downloads +1.5% 5.3% of All IAP Revenue 5% of All Downloads $3.6 B in IAP Revenue YoY IAP Revenue +46.0% YoY Downloads -7.9% 4.4% of All IAP Revenue 5% of All Downloads $2.7 B in IAP Revenue YoY IAP Revenue -6.3% YoY Downloads -10.6% 3.4% of All IAP Revenue 4% of All Downloads $6.1 B in IAP Revenue Source: Sensor Tower. Note: iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. Apps classified using Sensor Tower's Game taxonomy as of January 5, 2025. S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 35

36.

Source: Sensor Tower. Note:

iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. Apps classified using Sensor Tower's Game taxonomy as of January 5, 2025. Top20GlobalGameSubgenresbyIAPRevenuein2024 4XStrategyGamesTopIAP Revenuein2024,with PuzzleandRPGSubgenres FollowingClose In 2024, Strategy games dominated global consumer spend, with 4X Strategy leading the charge, capturing just under 10% of the market share, driven by Last War: Survival. Match Swap Puzzle games followed closely at 8.67%, fueled by the success of titles like Royal Match. RPG subgenres, including Squad RPGs (6.14%) and MMORPGs (5.59%), continued to deliver strong contributions, showcasing their lasting appeal among dedicated players. Casino Slots (5.37%) and Coin Looters (5.14%) demonstrated robust monetization, while Battle Royale games, led by Game for Peace (3.05%), maintained a loyal player base. Simulation subgenres, particularly Tycoon/Crafting, also gained momentum. These trends highlight the dominance of immersive and strategy-focused genres, with a balance of enduring favorites and new entrants driving sustained growth in the market. Gaming Worldwide Strategy | 4X Strategy Puzzle | Match Swap RPG | Squad RPG RPG | MMORPG Strategy | MOBA Casino | Slots Casino | Coin Looters Shooter | Battle Royale Simulation | Tycoon / Crafting RPG | Puzzle RPG RPG | Turn-based RPG Simulation | Sandbox Sports | Realistic Sports Shooter | FPS / 3PS RPG | Idle RPG Strategy | Real-Time Strategy Lifestyle | Interactive Story Puzzle | Match Merge 2 Geolocation | Geolocation Action | Beat 'em Up 0 $2KM $4KM $6KM $8KM 9.98% Last War:Survival Game 8.67% Royal Match 6.14% GODDESS OF VICTORY: NIKKE 5.59% Lineage M 5.52% Honor of Kings 5.37% Jackpot Party Casino 5.14% MONOPOLY GO! 3.05% Game For Peace 2.86% Township 2.66% Monster Strike 2.62% Honkai: Star Rail 2.34% ROBLOX 2.17% eFootball 2024 1.76% Call of Duty: Mobile 1.72% Legend of Mushroom 1.68% Teamfight Tactics 1.55% Love and Deepspace 1.50% Travel Town 1.48% Pokémon GO 1.44% Dungeon & Fighter Mobile Shareof Total #1 App S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 36

37.

Source: Sensor Tower.

Note: iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. Apps classified using Sensor Tower's Game taxonomy as of January 5, 2025. StableNewReleasesintheUSHighlightStrongPerformanceinRPGandStrategyGenres In the United States, the number of new mobile games among the top 1,000 by revenue remained stable, with RPG and Strategy genres leading the charge. New hits like Pokémon TCG Pocket and Sea of Conquest drove notable consumer spend, while RPGs such as AFK Journey and Top Heroes delivered strong and consistent revenues. Meanwhile, established Puzzle games like Royal Match and Candy Crush Saga continued to excel in monetization, showcasing their lasting appeal and ability to engage loyal players. The rising average consumer spend per game in 2023 highlights the growing success of high-quality new releases, supported by enduring hits like MONOPOLY GO! and Whiteout Survival, which sustained strong engagement and revenue growth throughout the year. Gaming NumberofNewGamesReleasedPerYear&AverageRevenuePerGameAmongTop1,000GamesbyIAPRevenue TopNewReleasesbyIAPRevenue United States 100 50 0 2020 2021 2022 2023 2024 N u m b e r o f N e w R e l e a s e s Puzzle RPG Strategy Simulation Action Arcade Other 0 $5M $10M $15M $20M 2020 2021 2022 2023 2024 A v g R e v e n u e Past Release Avg IAP Revenue New Release Avg IAP Revenue 1 The Seven Deadly Sins: Hikari to Yami no Grand Cross (Squad RPG) Royal Match (Match Swap) Diablo Immortal (MMORPG) MONOPOLY GO! (Coin Looters) Pokémon TCG Pocket (Card Battler) 2 Genshin Impact (Open World Adventure) Cookie Run: Kingdom (Squad RPG) Dislyte (Squad RPG) Whiteout Survival (4X Strategy) AFK Journey (Squad RPG) 3 MLB Tap Sports Baseball 2020 (Realistic Sports) MLB Tap Sports Baseball 2021 (Realistic Sports) Survivor!.io (Shoot 'em Up) Honkai: Star Rail (Turn-based RPG) Sea of Conquest (Other Strategy) 4 Redecor (Customization) My Hero Academia: Strongest Hero (Action RPG) GODDESS OF VICTORY: NIKKE (Squad RPG) Call of Dragons (4X Strategy) Top Heroes (Squad RPG) 5 Arknights (Tower Defense) Family Farm Adventure (Tycoon / Crafting) MLB Tap Sports Baseball 2022 (Realistic Sports) Street Fighter: Duel (Squad RPG) Love and Deepspace (Interactive Story) Top Past Releases by Downloads 1 ROBLOX (Sandbox) ROBLOX (Sandbox) Candy Crush Saga (Match Swap) Candy Crush Saga (Match Swap) MONOPOLY GO! (Coin Looters) 2 Candy Crush Saga (Match Swap) Candy Crush Saga (Match Swap) ROBLOX (Sandbox) Royal Match (Match Swap) Royal Match (Match Swap) 3 Coin Master (Coin Looters) Coin Master (Coin Looters) Coin Master (Coin Looters) ROBLOX (Sandbox) ROBLOX (Sandbox) 4 Pokémon GO (Geolocation) Free Fire (Battle Royale) Royal Match (Match Swap) Coin Master (Coin Looters) Candy Crush Saga (Match Swap) 5 Gardenscapes by Playrix Pokémon GO Pokémon GO Pokémon GO Last War:Survival 2020 2021 2022 2023 2024 S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 37

38.

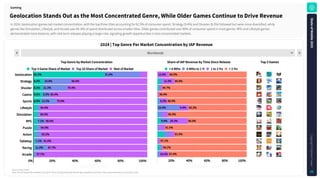

Worldwide 1 Rank Source: Sensor Tower Note:

iOS and Google Play combined. iOS only for China. Excludes third-party Android. Apps classified using Sensor Tower's game taxonomy as of January 5, 2025. GeolocationStandsOutastheMostConcentratedGenre,WhileOlderGamesContinuetoDriveRevenue Gaming 2024|TopGenrePerMarketConcentrationbyIAPRevenue Geolocation Strategy Shooter Casino Sports Lifestyle Simulation RPG Puzzle Action Tabletop Racing Arcade 0% 20% 40% 60% 80% 100% 62.5% 31.6% 9.4% 23.8% 66.8% 8.3% 21.3% 70.4% 8.0% 6.5% 85.4% 6.9% 13.2% 79.9% 94.4% 94.5% 7.1% 89.6% 94.0% 93.2% 7.1% 91.6% 11.0% 87.7% 97.7% Top 3 Game Share of Market Top 20 Share of Market Rest of Market Top3Games 20% 40% 60% 80% 100% 12.6% 86.9% 12.3% 80.9% 94.7% 98.4% 8.5% 88.9% 24.4% 9.9% 65.3% 88.3% 9.9% 20.3% 66.0% 91.5% 81.0% 97.1% 94.1% 10.2% 87.4% < 6 Mths 6 Mths to 1 Yr 1 to 2 Yrs > 2 Yrs ShareofIAPRevenuebyTimeSinceRelease TopGenrebyMarketConcentration In 2024, Geolocation games led market concentration, with the top three titles accounting for 62.5% of consumer spend. Strategy (9.4%) and Shooter (8.3%) followed but were more diversified, while genres like Simulation, Lifestyle, and Arcade saw 94–8% of spend distributed across smaller titles. Older games contributed over 80% of consumer spend in most genres. RPG and Lifestyle games demonstrated more balance, with mid-term releases playing a larger role, signaling growth opportunities in less concentrated markets. S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 38

39.

Source: Sensor Tower. Note:

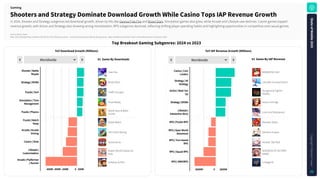

iOS and Google Play combined. iOS only for China. Revenue is gross — inclusive of any percent taken by the app stores. Apps classified using Sensor Tower's Game taxonomy as of January 5, 2025. ShootersandStrategyDominateDownloadGrowthWhileCasinoTopsIAPRevenueGrowth TopBreakoutGamingSubgenres:2024vs2023 Worldwide Shooter | Battle Royale Strategy | MOBA Puzzle | Sort Simulation | Time Management Puzzle | Physics Puzzle | Match Swap Arcade | Arcade Driving Casino | Slots Lifestyle | Customization Arcade | Platformer / Runner -600M -400M -200M 0 200M Free Fire Brawl Stars Traffic Escape! Pizza Ready Wood Nuts & Bolts Puzzle Royal Match Hill Climb Racing Slotomania Avatar World Games for Kids Subway Surfers #1 GameByDownloads YoYDownloadGrowth(Millions) #1 GameByIAPRevenue YoYIAPRevenueGrowth(Millions) Worldwide Casino | Coin Looters Strategy | 4X Strategy Action | Beat 'em Up Strategy | MOBA Lifestyle | Interactive Story RPG | Puzzle RPG RPG | Open World Adventure RPG | Turn-based RPG RPG | Squad RPG RPG | MMORPG -$600M 0 $600M In 2024, Shooter and Strategy subgenres led download growth, driven by hits like Garena Free Fire and Brawl Stars. Simulation games also grew, while Arcade and Lifestyle saw declines. Casino games topped revenue growth, with Action and Strategy also showing strong monetization. RPG subgenres declined, reflecting shifting player spending habits and highlighting opportunities in competitive and casual genres. Gaming MONOPOLY GO! Last War:Survival Game Dungeon & Fighter Mobile Honor of Kings Love and Deepspace Monster Strike Genshin Impact Honkai: Star Rail GODDESS OF VICTORY: NIKKE Lineage M S t a t e o f M o b i l e 2 0 2 5 C o p y r i g h t © S e n s o r T o w e r 39

40.

Source: Sensor Tower Note: