Outline

• Fundamental andTechnical Analysis

• Random Walk

• Efficient Market Hypothesis (EHM) and Portfolio

Management

• Fixed Income Security Valuation and Analysis (Bond

Portfolio Management)

• Credit Rating and Development of Credit Rating

Regulations

• Analysis of fixed income investment in Ghana

• Municipal Bond and Sovereign Bonds

3.

What is aSecurity

Assets with some financial value

are called securities.

What is SecurityAnalysis ?

• The analysis of various tradable financial

instruments is called security analysis.

• Security analysis helps a financial expert or a

security analyst to determine the value of

assets in a portfolio.

7.

• Security analysisrefers to the analysis of

trading securities from the point of their

prices, returns and risks.

• All investments are risky and the expected

return is related to the quantum of risk. All

investors try to earn more return with low

level of risk or without risk. For this purpose

they are considering some objectives.

Classification of SecurityAnalysis

Security Analysis is broadly classified into three

categories:

•Fundamental Analysis

•Technical Analysis

•Quantitative Analysis

Technical Analysis

• Analystsand market technicians examine

prior price and volume data as well as other

market-related indicators to determine past

trends in the belief that they will help forecast

future ones.

• Technical analysis is the use of stock prices,

trading volume and other market data to

formulate rules telling the technician when to

buy or sell stocks.

12.

• The technicalanalysts are sometimes

called chartists because they study

records and charts of past stock prices

hoping to find patterns they can exploit

to make profit.

• Many of these technician do not even

consider the influence of other market or

company information to make their

investment decision.

13.

Assumptions of TechnicalAnalysis

• Market value is determined by the interaction of

demand and supply.

• It is assumed that though there are minor

fluctuations in the market, stock prices tend to

move in trends that persist for long periods.

• Reversals of trends are caused by shifts in

demand and supply

• Shifts in demand can be detected sooner or later

in charts.

• Many chart patterns tend to repeat themselves

14.

Tools of Technicalanalysts

• Some of the tools used by chartists to measure supply

and demand and to forecast security prices are the

• Dow theory chart: used to indicate reversals and trends

in the market as a whole or in individual securities

• Odd-lot theory: assumes that the common man is

usually wrong, and it is therefore advantageous to

pursue strategies opposite to his thinking.

• Confidence index, breadth-of-market indicators,

relative-strength analysis, and trading-volume data.

15.

Advantages of TechnicalAnalysis

• Once the technician has determined the

particular role to use in the technical strategy,

making the actual investment decision is easy

• Technical analysis is easy to learn and requires

no specialised financial knowledge

• Technicians have access to all the information

they require in their analysis. Stock prices,

and volume of activities are easily accessible

through the press or the Internet.

16.

Criticisms of TechnicalAnalysis

• Opponents of technical analysis claim that there is no real

objective, substantial evidence that it works. Indeed the wealth of

information supporting the weak form of efficient market

hypothesis (EMH) rejects technical analysis.

• Another criticism of the technical analysis is that it is self-fulfilling

prophecy. Consider several hundreds of technicians using the

same information and arriving at the same decision.

• By the time they have processed the stock price information and

acted, other technicians will have done same, the stock price will

have reached its new equilibrium and it will be too late to make

trading profit.

• The final criticism deals with the difficulty of discerning chart

patterns as they develop. A good instructional manual of charting

will show nice examples of all the standard chart patterns,

identifying the buy or sell points.

Fundamental Analysis

• Beforea security analyst can determine a proper price for

a firm’s stock, he/she has to forecast the earnings and

dividend that can be expected from the firm.

• Fundamental analysis uses earnings and dividend

prospects of a firm, expectation of future interest rates and

risk evaluation of the firm to determine stock prices.

• Fundamental analysis starts with a study of past earnings

and the examination of a company’s balance sheet,

ordinarily including an evaluation of the quality of

management of the firm, the firm’s standing in the

industry and prospect of the industry as a whole.

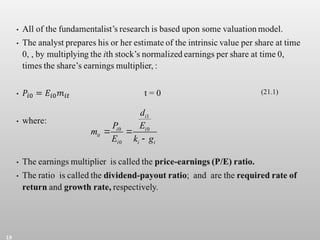

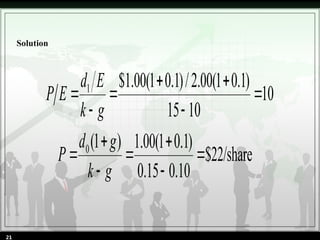

• The stockof XYZ Corporation is currently

paying a dividend of $1.00 per share. The firm’s

dividend growth rate is expected to be 10%. For

firms in the same risk class as XYZ, market

analysts agree that the capitalization rate is

approximately 15%. Current earnings for XYZ

are $2.00 per share and they are expected to

grow at 10%. What are the P/E ratio and the

price of XYZ shares given this information?

Sample Problem

20

• Fundamental analysisis therefore

conducted on three levels:

• The economy

• The industry and

• The firm

23.

• There aretwo types of fundamental analysis namely

• Top-down analysis and

• Bottom-up analysis.

• The top-down analysis starts with the broad economic

environment, examining the state of the aggregate

economy and even the international economy, the

firm’s position within the industry is examined by

looking at which firm(s) within the industry will

maximise investment return.

• The bottom-up analysis on the other hand, begins at

the micro-level (firm’s level) expand the analysis to the

company’s industry or sector and end with the analysis

of the economic environment.

24.

Economy Analysis

• Economicanalysis will be considered by

looking at both

• Global and

• The domestic economies.

25.

Global Economy

• Atop-down analysis must start with the global

economy. The international economy might affect

• A firm’s export prospects

• The price competition it faces from imported goods

(competitors)

• The profit it makes from investment abroad

• The political environment

• Exchange rate fluctuations

• Competition

• Social environment

• Economic environment etc

Industry Life Cycle

•An industry analysis helps place an industry on

the life cycle curve and in turn guides the analyst

towards decision on industry growth, the

duration of growth, profitability and potential

rate of return. The analyst can determine where

all companies in the industry are in the stage of

the life cycle and translate company differences

into various assumptions that will affect their

valuation.

• The life cycle of an industry is divided into 5

stages:

29.

Development Stage

• Thedevelopment stage includes

companies that are getting started in

business with new product development

or production technique that makes

them unique.

• At this stage it is difficult to predict which

firms will emerge as industry leaders.

30.

Growth Stage

• Itrepresents an industry or company

that has achieved a degree of market

acceptance for its products.

• At this stage earnings would be retained

for reinvestment.

• Companies will be dividend to

shareholders

31.

Expansion Stage

• Atthe expansion stage, sales and earnings

expansion continues at a decreasing rate.

Industrial leaders begin to emerge.

• The survivors in the industry are more stable

and market share is easier to predict.

• The performance of the surviving firms more

closely tracks the performance of the overall

industry.

32.

Mature

• At thisstage the product has reached its full

potential for use by consumers.

• The product has become standardised and

producers compete on the basis of price.

• This leads to narrower profit margin and

further pressure on profit.

• Sales grow at a rate equal to the economy as

measured by long-term trend in GDP.

33.

Decline

• At thisstage, the industry might grow at a rate

lower than the economy or it might even

shrink.

• Industries suffer decline in sales as a result of

competition from new products.

• It should be noted that it might not be the

whole industry that goes into decline but

rather weak firms within the industry.

![7.__Developing_a_Research_Proposal[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7-260131073037-df92dd7d-thumbnail.jpg?width=640&height=640&fit=bounds)

![Hacking-Uncovered-How-People-Get-Hacked-and-How-to-Stay-Safe[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/hacking-uncovered-how-people-get-hacked-and-how-to-stay-safe1-260130170011-4883a9c7-thumbnail.jpg?width=640&height=640&fit=bounds)