Download as PDF, PPTX

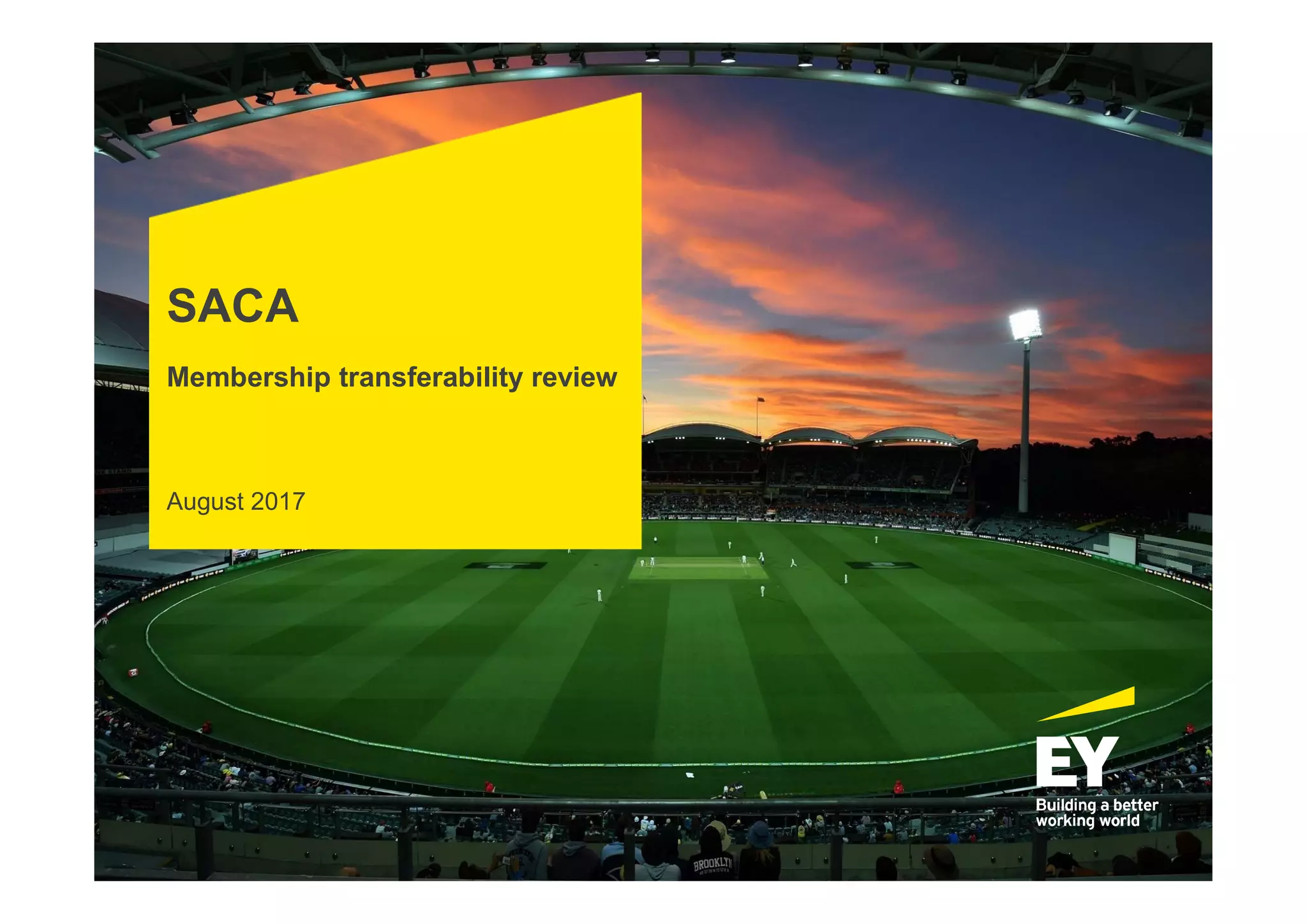

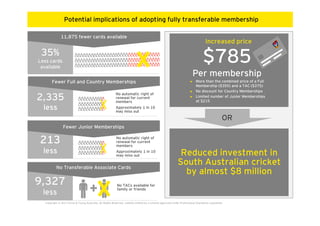

The Ernst & Young report assesses the financial and other implications of making South Australian Cricket Association (SACA) memberships fully transferable. Key findings suggest significant membership reductions and substantial price increases are necessary to avoid financial decline, potentially leaving SACA $7.9 million worse off annually without increased membership fees. The findings also highlight potential brand health risks and outline the necessity for careful implementation of any changes to membership structure.