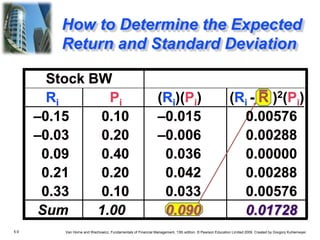

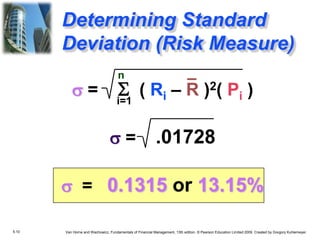

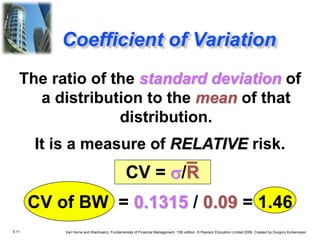

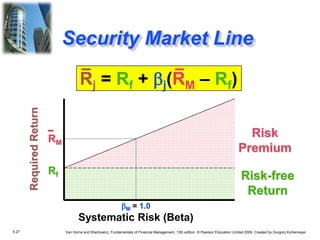

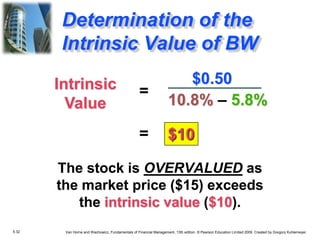

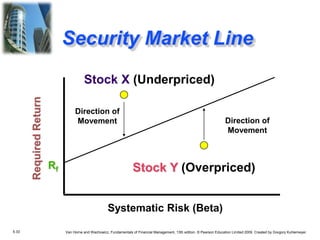

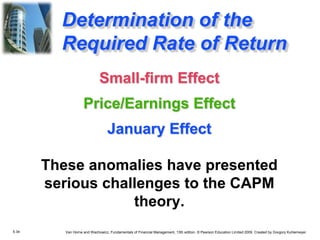

This document contains sections from the 13th edition of the textbook "Fundamentals of Financial Management" by Van Horne and Wachowicz. It discusses key concepts related to risk and return such as defining return, determining expected return and standard deviation, risk attitudes like risk aversion, and the Capital Asset Pricing Model (CAPM). The CAPM holds that a security's expected return is determined by its risk profile as measured by beta in relation to the market portfolio's risk and return. Examples are provided to illustrate return, risk, and CAPM calculations.