• Initial recognition:

•Purchase price:

• Import duties

• Non refundable purchase taxes

• Directly attributable costs:

• Site preparation

• Initial delivery and handling costs

• Installation and assembly costs

• Professional fees

Assets- Property, Plant and Equipment

2

3.

• Measurement AFTERrecognition

• Cost model

• Cost less accumulated depreciation

• Revaluation model

• Valuation: sufficient regularity that does not differ materially from Fair

Value(market value):

• - volatile: annual

• - non volatile: 3-5 years

• Revalue entire class

Assets- Property, Plant and Equipment

3

4.

• Measurement AFTERrecognition

• Revaluation model

• Upward revaluation to OCI (Other Comprehensive Income)

• Downward revaluation:

• 1st to OCI then to p&l

Assets- Property, Plant and Equipment

4

5.

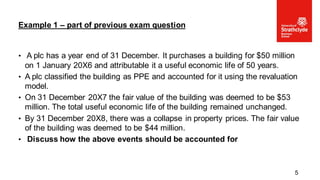

• A plchas a year end of 31 December. It purchases a building for $50 million

on 1 January 20X6 and attributable it a useful economic life of 50 years.

• A plc classified the building as PPE and accounted for it using the revaluation

model.

• On 31 December 20X7 the fair value of the building was deemed to be $53

million. The total useful economic life of the building remained unchanged.

• By 31 December 20X8, there was a collapse in property prices. The fair value

of the building was deemed to be $44 million.

• Discuss how the above events should be accounted for

Example 1 – part of previous exam question

5

6.

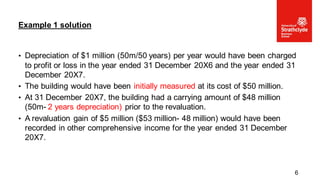

• Depreciation of$1 million (50m/50 years) per year would have been charged

to profit or loss in the year ended 31 December 20X6 and the year ended 31

December 20X7.

• The building would have been initially measured at its cost of $50 million.

• At 31 December 20X7, the building had a carrying amount of $48 million

(50m- 2 years depreciation) prior to the revaluation.

• A revaluation gain of $5 million ($53 million- 48 million) would have been

recorded in other comprehensive income for the year ended 31 December

20X7.

Example 1 solution

6

7.

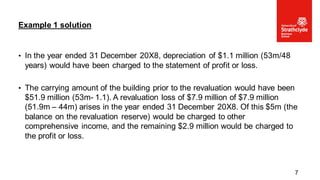

• In theyear ended 31 December 20X8, depreciation of $1.1 million (53m/48

years) would have been charged to the statement of profit or loss.

• The carrying amount of the building prior to the revaluation would have been

$51.9 million (53m- 1.1). A revaluation loss of $7.9 million of $7.9 million

(51.9m – 44m) arises in the year ended 31 December 20X8. Of this $5m (the

balance on the revaluation reserve) would be charged to other

comprehensive income, and the remaining $2.9 million would be charged to

the profit or loss.

Example 1 solution

7

8.

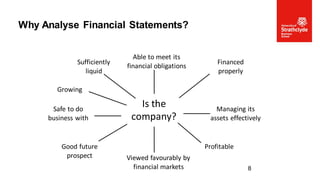

Why Analyse FinancialStatements?

8

Is the

company?

Growing

Profitable

Managing its

assets effectively

Sufficiently

liquid

Financed

properly

Able to meet its

financial obligations

Viewed favourably by

financial markets

Good future

prospect

Safe to do

business with

9.

• Quick andsimple check on financial health

• Small number of ratios gives a picture of the business.

• Easy to calculate, harder to interpret.

• Provide a starting point for further investigation.

Financial ratios

9

10.

• Simple summaryof complex information

• Compare businesses of different size

• Gives picture of company strategy

• Financial and trading performance

• Compare with industry averages

• Simple summary of complex information

Advantages of ratios

10

11.

• No agreementon definitions or specific set of ratios

• Timing of data does not match user needs

• Differing accounting policies

• May not give sufficient attention to the notes to the accounts

• Accounting policies may affect comparison

• Industry differences

Problems with ratio analysis

11

£ £

Revenue 500,000

Openinginventory25,000

Purchases 305,000

Closinginventory (30,000)

Costof sales 300,000

Gross profit 200,000

Otheroperatingexpenses (60,000)

Interestpaid (24,000)

Profitforyear 116,000

Alpha Ltd

Income Statement for the year ended 31 December 20*7

13

14.

£ £

ASSETS

Non-current assets540,000

Current assets

Inventory 30,000

Trade receivables 62,500

Bank 7,000

99,500

Total Assets 639,500

EQUITY & LIABILITIES

Equity

Share capital 145,625

Reserves 256,000

401,625

Non-current liabilities

Debenture Loans 200,000

Current liabilities

Trade payables 37,875

Total equity and liabilities 639,500

Alpha Ltd

Statement of financial position as at 31 December 20*7

14

15.

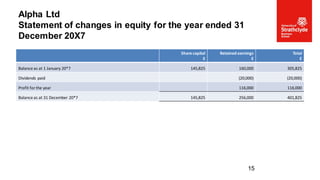

Share capital

£

Retained earnings

£

Total

£

Balanceas at 1 January 20*7 145,825 160,000 305,825

Dividends paid (20,000) (20,000)

Profit for the year 116,000 116,000

Balance as at 31 December 20*7 145,825 256,000 401,825

Alpha Ltd

Statement of changes in equity for the year ended 31

December 20X7

15

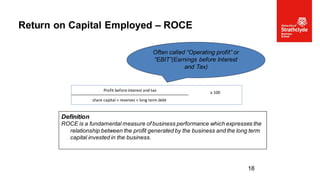

Return on CapitalEmployed – ROCE

18

Definition

ROCE is a fundamental measure of business performance which expresses the

relationship between the profit generated by the business and the long term

capital invested in the business.

Often called “Operating profit” or

“EBIT”(Earnings before Interest

and Tax)

Profit before interest and tax x 100

share capital + reserves + long term debt

19.

• Return oncapital employed is a useful ratio in analysing profitability and

efficiency together.

Return on Capital Employed – ROCE

19

Gross profit =Revenue or Sales minus Cost of sales

Cost of sales = “making ready for sale” so includes all costs incurred in manufacturing a product or

acquiring a product for sale

Gross Profit Margin (GPM)

22

Definition

Gross profit represents the difference between sales and the cost of sales. The

ratio is thus a measure of profitability in buying/producing and selling goods

before any other expenses are taken into account

Gross profit x 100

Revenue

23.

• Possible reasonsfor changes in the gross profit margin year on year or

differences between two organisations include:

• (a) change in sales price

• (b) change in sales mix (e.g. selling silver cutlery (high profit per item) versus

plastic cutlery (low profit per item)

• (c) Change in purchase price and/or production costs

• (d) Stock written off

Gross Profit Margin (GPM)

23

24.

Net Profit Margin(NPM)

22

Definition

Net profit represents the difference between sales and the all other costs

including cost of sales, operating expenses, interest and taxes. The ratio is

useful in comparing overall performance.

Net profit x 100

Revenue

25.

• Possible reasonsfor changes in the net profit margin year on year or

differences between two organisations include:

• (a) One-off non-recurring expenses

• (b) Efficiency savings (economies of scale)

Net Profit Margin (NPM)

25

26.

• Calculate thegross profit and net profit ratios for Alpha Ltd.

Alpha Ltd

26

• Can wepay the bills as they fall due?

• Can we pay the wages of employees?

• Buy stock/inventory

• Ideally, match cash flows in and out

Liquidity ratios

28

29.

Current Assets

Current Liabilities

Thisratio measures a company’s ability to pay its current liabilities out

of its current assets.

The industry the company operates in should be taken into

consideration. For example, a supermarket has low receivables

(mainly cash), low inventory (as perishable) and high payables

(superior bargaining power), so overall will have a low current ratio

Current Ratio

29

Current Assets lessInventory

Current Liabilities

This is similar to the current ratio except that it omits the inventories figure from

current assets.

This is because inventories are the least liquid current asset that the company

has, as it has to be sold, turned into receivables and then the cash collected.

Quick Ratio (Acid Test)

32

Current Assets lessInventory

Current Liabilities

Quick Ratio (Acid Test)- Alpha

34

35.

• Ratios maybe used to measure the efficiency with which certain resources

have been utilised within the business.

• The most common ratios used are:

• Inventory days

• Receivables days

• Payables days

• Cash conversion cycle

Efficiency/Working Capital Ratios

35

36.

Inventory x 365

Costof Sales

Change 365 to 12 for a calculation in months.

Inventory days

36

Definition

Stock or inventory represents a major part of the assets of many businesses.

The average stock turnover period measures the average period for which

stocks are being held. Normally a business prefer a low number of days so

that funds are not tied up in stocks when they (i.e. the funds) could be used

more profitably.

37.

• Inventory dayswill depend on the type of goods and services sold by a

company.

• For example, a company selling fresh fruit and vegetables should have a low

inventory holding period as these goods will quickly become inedible.

• A manufacturer of aged wine will have a very long inventory holding period.

• It is important for a company to keep its inventory days as low as possible,

subject of course to being able to meet its customers’ demands.

Inventory days

37

Trade Receivables x365

Revenue

Trade Receivables =customers who buy on credit

Receivables days

40

Definition

The trade receivable collection period calculates how long, on average, credit

customers take to pay the amounts that they owe to the business. There is

no such thing as an ideal debtor collection period. A business however would

become concerned if the days were rising as this could indicate difficulties in

collecting cash from customers.

Trade Payables x365

Purchases or Cost of Sales

•This ratio measures the time it takes the company to settle its trade payables. Trade payables

provide the company with a valueble source of short term fiancé, but delaying payment for too long a

period of time can cause operational problems as suppliers may stop providing goods and services

until payment is received.

Payables days

43

Trade Payables x365

Purchases or Cost of Sales

Alpha Payables days

45

46.

• A measureof working capital efficiency and calculated as:

Inventory days + Receivable days – Payable days

• The cycle measures the average number of days that working capital is

invested in the operating cycle .

• Also referred to as ‘working capital cycle’

Cash Conversion Cycle

46

47.

• Calculate theworking capital ratios for Alpha Ltd

Alpha Ltd

47

48.

Inventory days +Receivable days – Payable days

• =

Alpha working capital days

48

49.

• Ratios whichexamine the relationship between the amount financed by the

owners of the business and the amount financed by outsiders such as banks.

• The main ratios used are:

• Gearing ratio (or Debt/Equity ratio)

• Interest cover ratio

Financing

49

50.

• Is ita good idea to borrow?

• Creates greater risk - interest payments and capital repayments

• Benefits for shareholders when profits are rising

• Risks for shareholders when profits are falling

Financial structure

•Page 50

51.

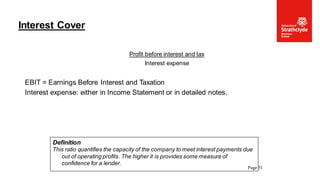

Profit before interestand tax

Interest expense

EBIT = Earnings Before Interest and Taxation

Interest expense: either in Income Statement or in detailed notes.

Interest Cover

Page 51

Definition

This ratio quantifies the capacity of the company to meet interest payments due

out of operating profits. The higher it is provides some measure of

confidence for a lender.

52.

• Calculate theinterest cover ratio for Alpha Ltd.

Alpha Ltd

52

Page 55

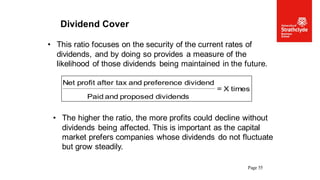

Dividend Cover

•This ratio focuses on the security of the current rates of

dividends, and by doing so provides a measure of the

likelihood of those dividends being maintained in the future.

times

X

=

dividends

proposed

and

Paid

dividend

preference

and

tax

after

profit

Net

• The higher the ratio, the more profits could decline without

dividends being affected. This is important as the capital

market prefers companies whose dividends do not fluctuate

but grow steadily.

56.

Page 56

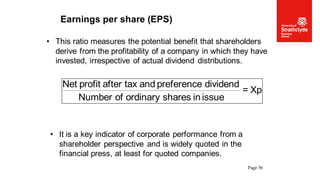

Earnings pershare (EPS)

• This ratio measures the potential benefit that shareholders

derive from the profitability of a company in which they have

invested, irrespective of actual dividend distributions.

• It is a key indicator of corporate performance from a

shareholder perspective and is widely quoted in the

financial press, at least for quoted companies.

Xp

=

issue

in

shares

ordinary

of

Number

dividend

preference

and

tax

after

profit

Net

57.

Page 57

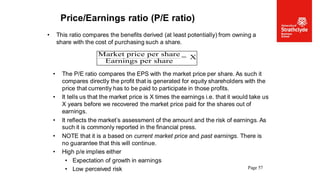

Price/Earnings ratio(P/E ratio)

• This ratio compares the benefits derived (at least potentially) from owning a

share with the cost of purchasing such a share.

• The P/E ratio compares the EPS with the market price per share. As such it

compares directly the profit that is generated for equity shareholders with the

price that currently has to be paid to participate in those profits.

• It tells us that the market price is X times the earnings i.e. that it would take us

X years before we recovered the market price paid for the shares out of

earnings.

• It reflects the market’s assessment of the amount and the risk of earnings. As

such it is commonly reported in the financial press.

• NOTE that it is a based on current market price and past earnings. There is

no guarantee that this will continue.

• High p/e implies either

• Expectation of growth in earnings

• Low perceived risk

Market price per share

Earnings per share

= X