Downloaded 12 times

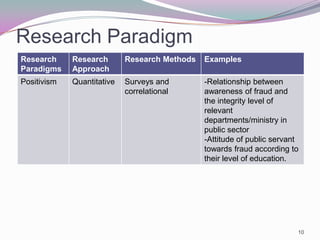

The document outlines the presentation for research on fraud and work ethics awareness in Malaysian public sectors. It includes the research topic, problem statement, research questions, objectives, and paradigm. The problem statement notes that while ethics promotion is emphasized, fraud cases continue rising in Malaysia's public sectors due largely to poor internal controls and a lack of fraud awareness training. The research aims to measure and understand fraud awareness and its impact, as well as identify issues and the relationship between awareness and controls. A quantitative survey approach will be used.