Download to read offline

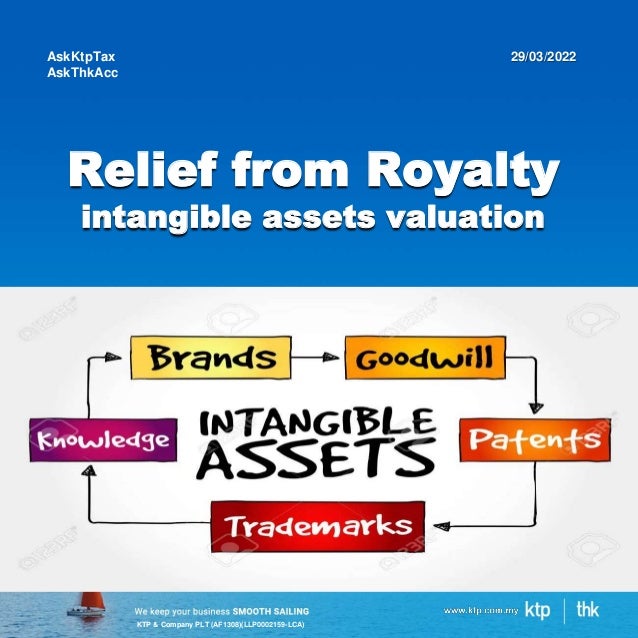

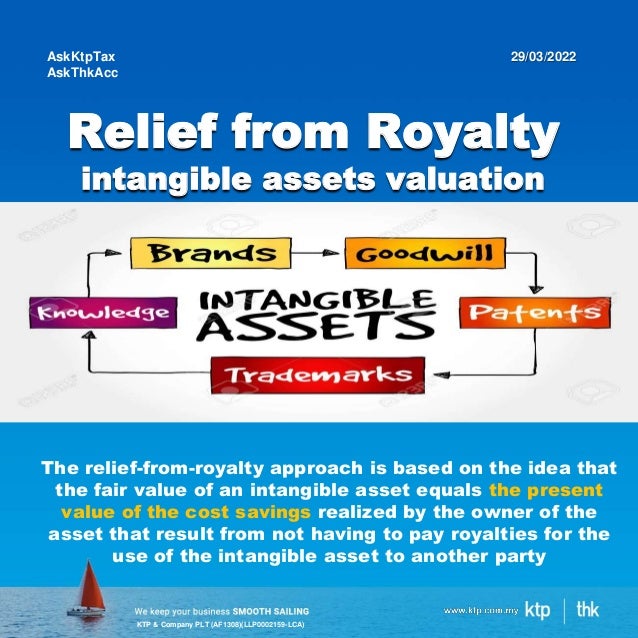

The document discusses the relief-from-royalty (RFR) approach to valuing intangible assets, emphasizing that the fair value corresponds to the present value of cost savings from avoiding royalty payments. It outlines a five-step process for implementing the RFR method, which includes setting the valuation purpose, estimating economic benefits, determining a hypothetical royalty rate, calculating the discount rate, and performing the final calculation. The RFR method aims to provide a structured means of valuing intangible assets based on potential economic advantages.

![SOCSO Enforce New Salary Ceiling Limit for Contributions[7991].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/socsoenforcenewsalaryceilinglimitforcontributions7991-220918232622-b12f7178-thumbnail.jpg?width=640&height=640&fit=bounds)