Download to read offline

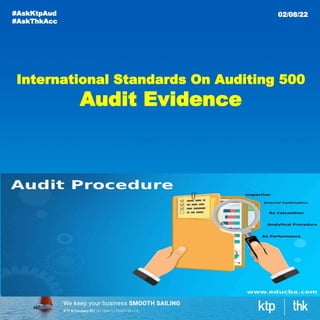

The document outlines various audit procedures used to gather audit evidence according to International Standards on Auditing 500. Key procedures include inspection, observation, external confirmation, recalculation, reperformance, analytical procedures, and inquiry. Each procedure is defined in terms of its purpose and application in the auditing process.

![Audit evidence a framework (ppt ch7[1].pdf)](https://cdn.slidesharecdn.com/ss_thumbnails/auditevidence-aframeworkpptch71-pdf-121211154609-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![SOCSO Enforce New Salary Ceiling Limit for Contributions[7991].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/socsoenforcenewsalaryceilinglimitforcontributions7991-220918232622-b12f7178-thumbnail.jpg?width=640&height=640&fit=bounds)