Download to read offline

![#AskKtpTax

#AskThkSec

07/07/22

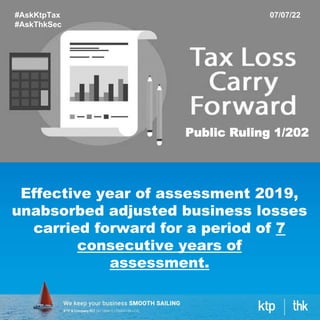

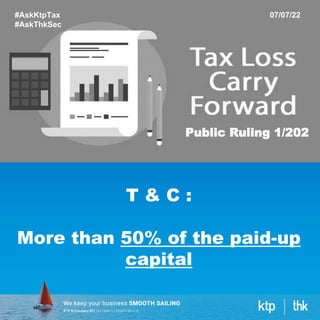

Public Ruling 1/202

…. through the Finance Act 2021 [Act

833] effective year of

assessment 2019.](https://image.slidesharecdn.com/220707unutilisedtaxlosss-220707064343-02301b66/85/unutilised-tax-losss-pptx-5-320.jpg)

The document discusses Public Ruling 1/2022 regarding the time limit for carrying forward unabsorbed adjusted business losses, which is extended from 7 to 10 consecutive years effective from the year of assessment 2019. Any unabsorbed losses beyond this period will be disregarded, and certain conditions regarding shareholding changes must be met to qualify for the carry-forward. Additionally, dormant companies are exempt from this ruling.

![SOCSO Enforce New Salary Ceiling Limit for Contributions[7991].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/socsoenforcenewsalaryceilinglimitforcontributions7991-220918232622-b12f7178-thumbnail.jpg?width=640&height=640&fit=bounds)