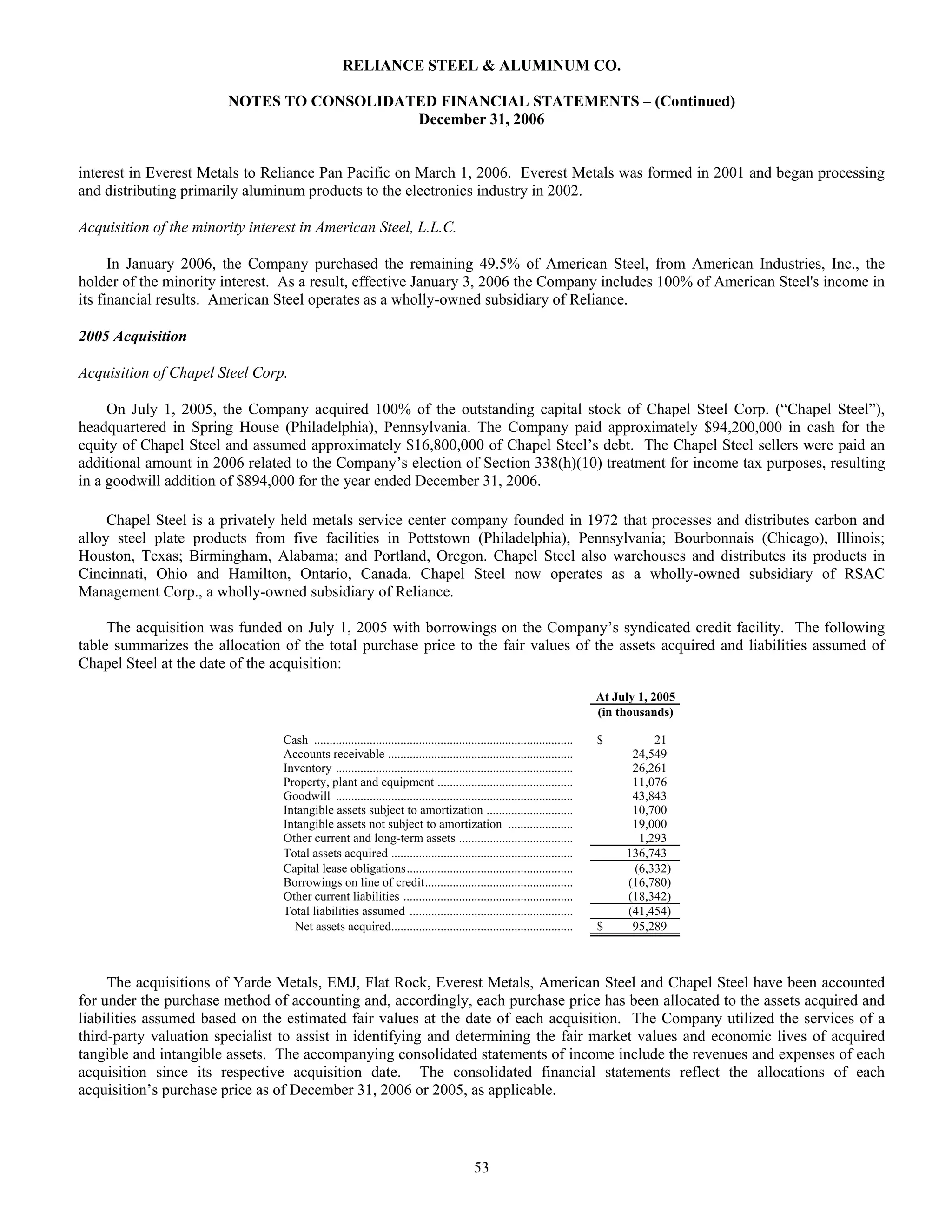

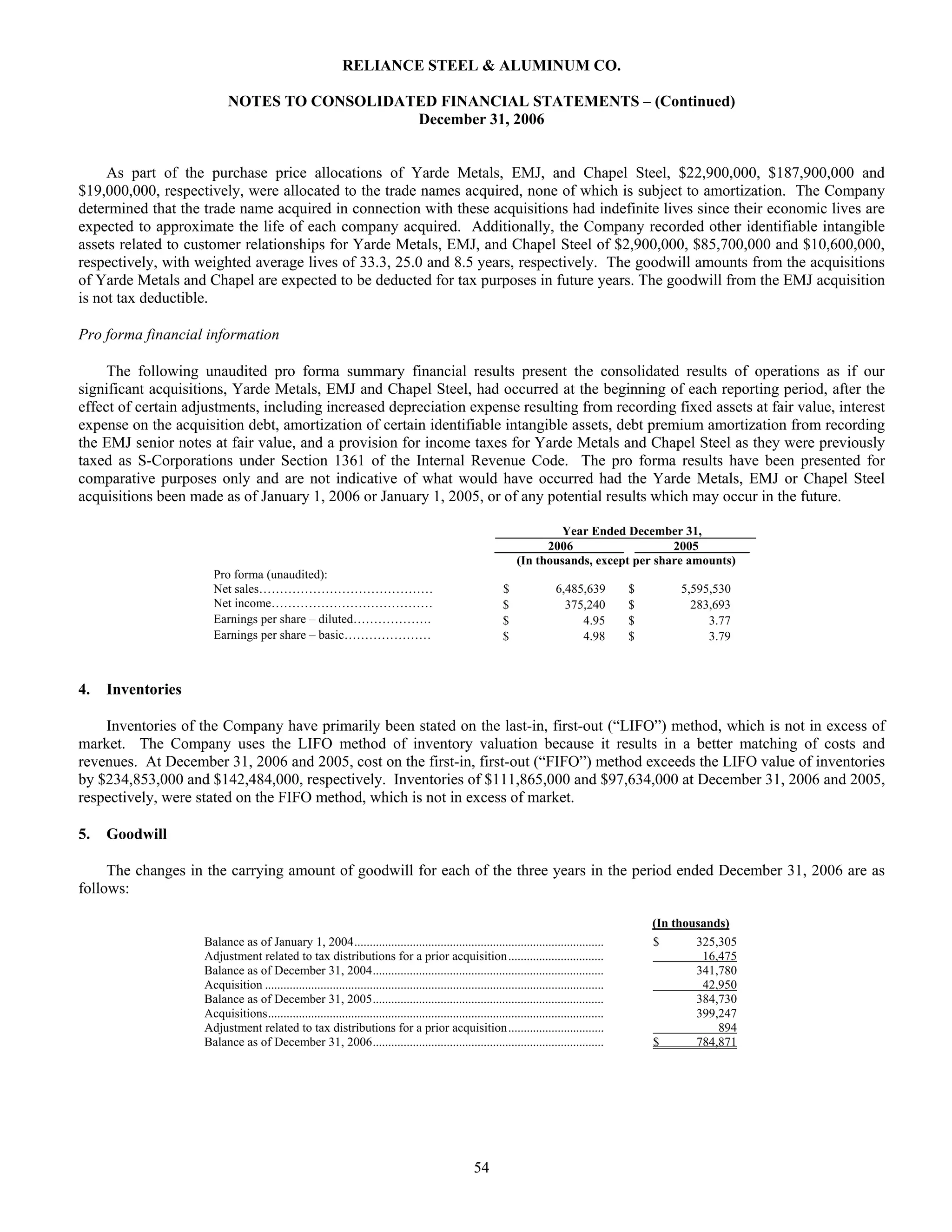

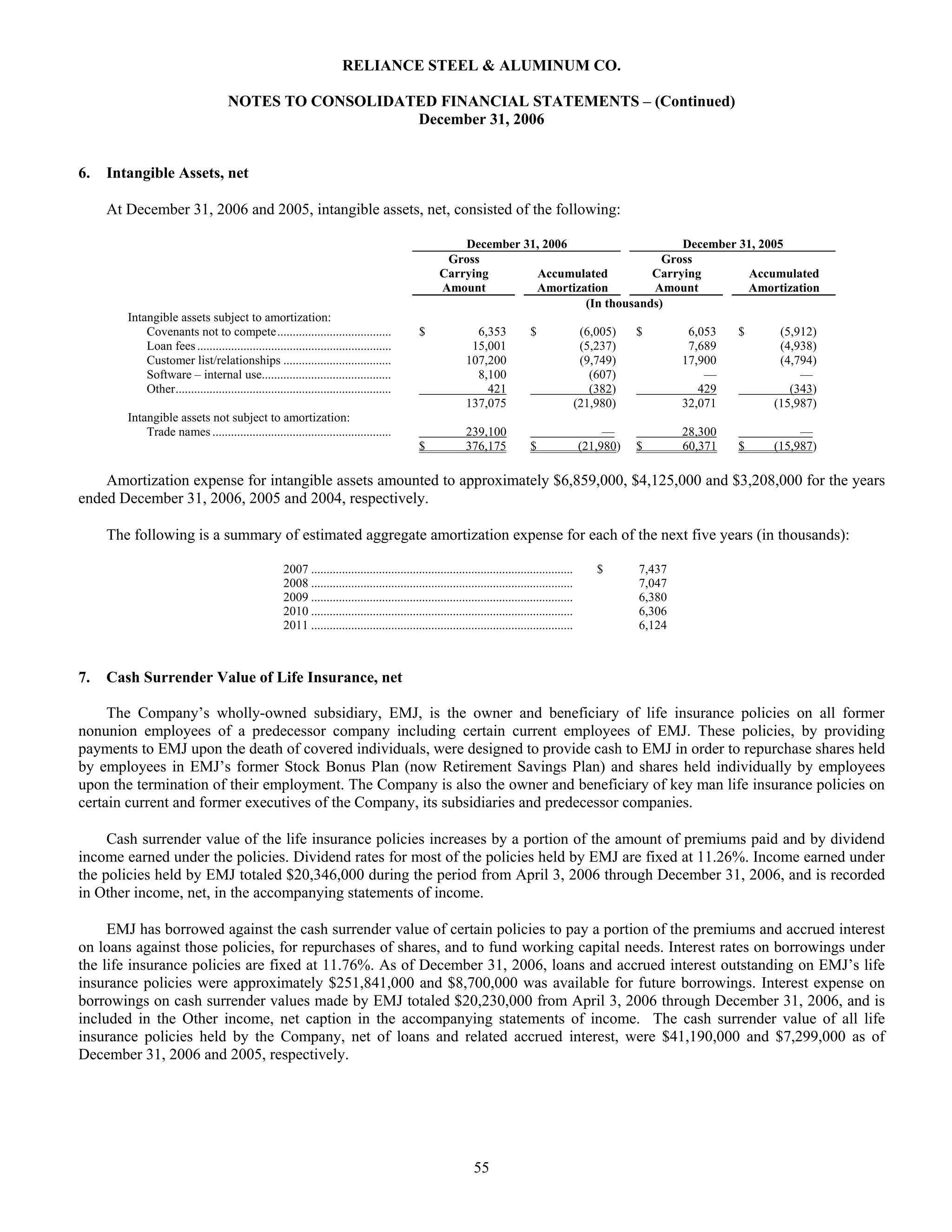

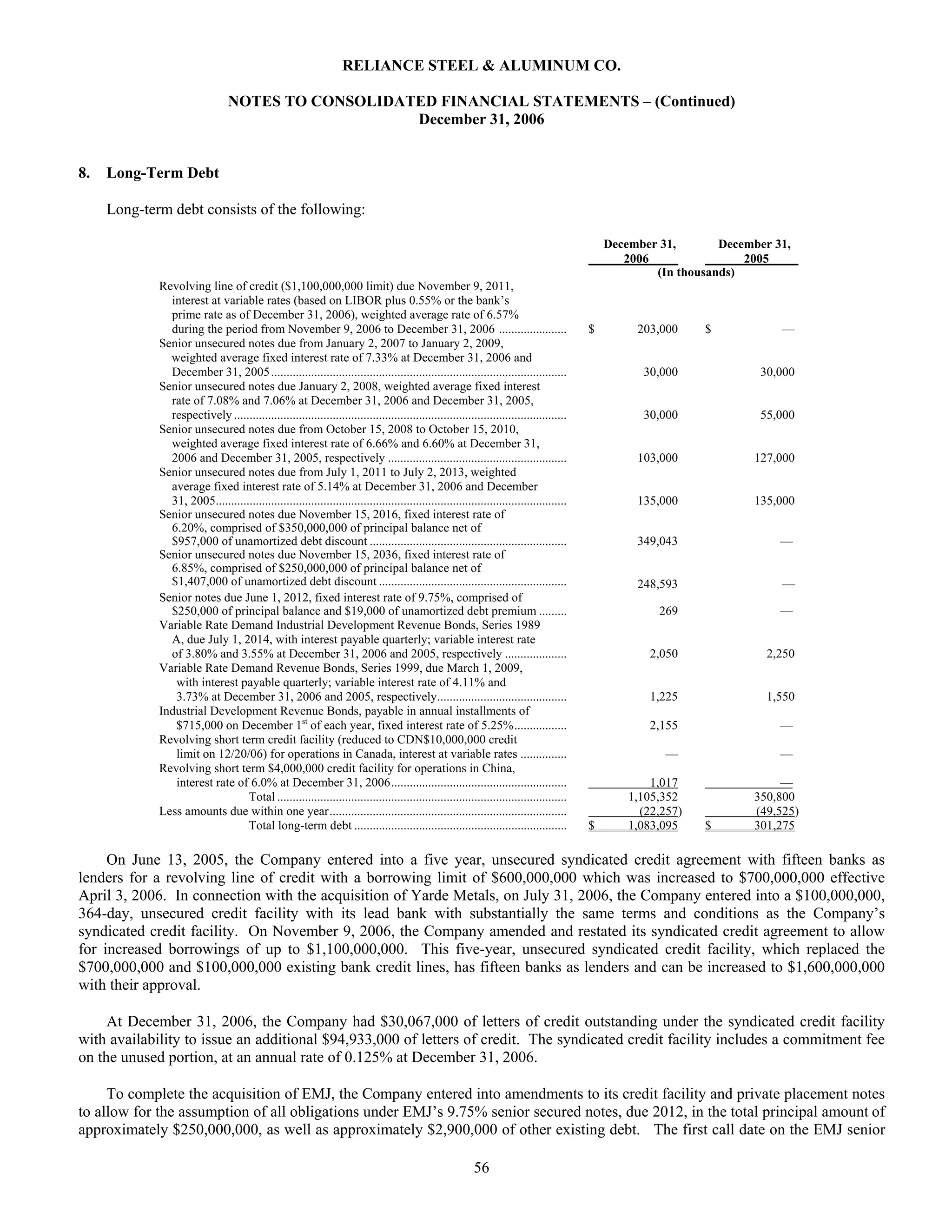

Download to read offline

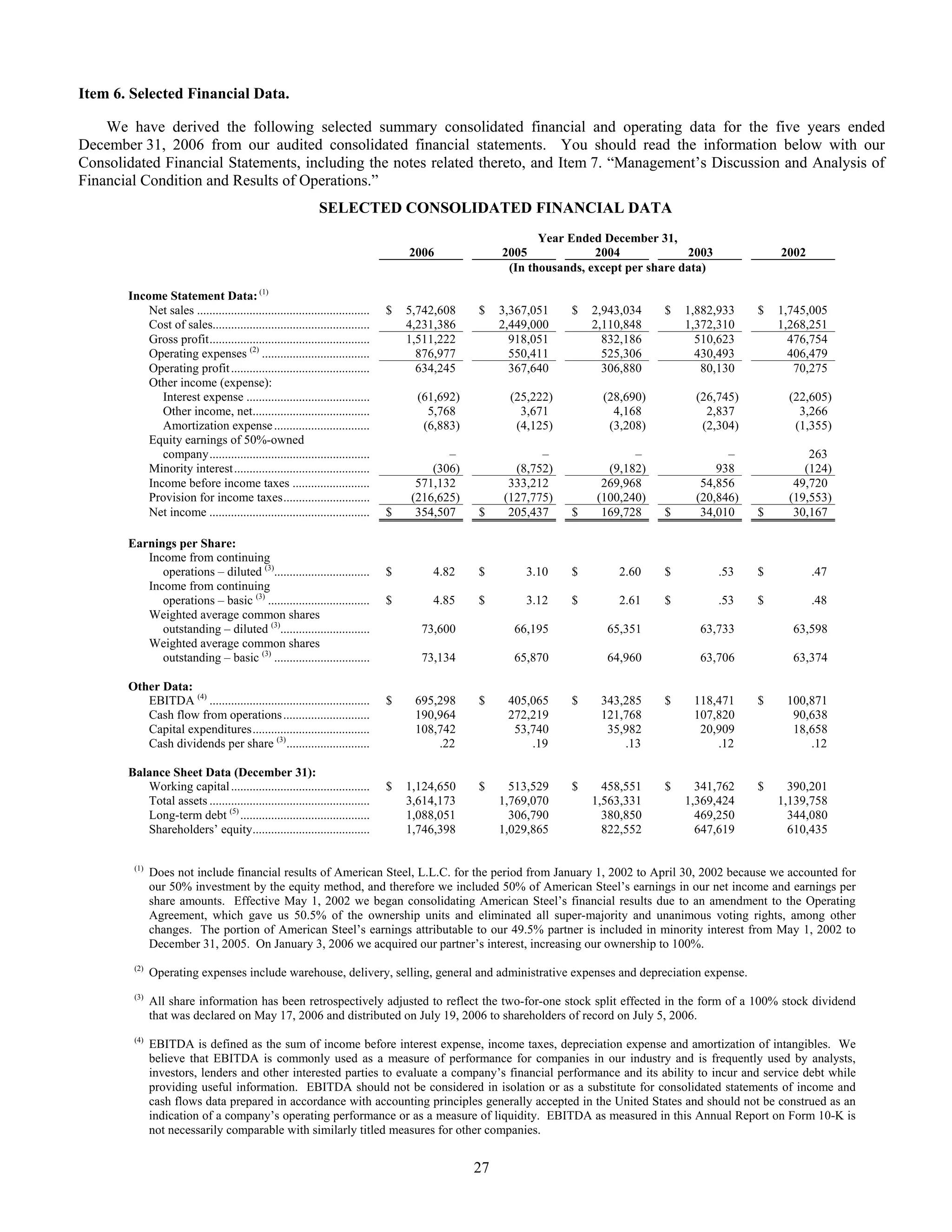

This document is Reliance Steel & Aluminum Co.'s annual report (Form 10-K) filed with the SEC. It provides an overview of the company's business including: the metals service center industry, Reliance's history and operations, customers, suppliers, products/services, competition, regulations, and risk factors. Key details include that Reliance operates over 180 locations in North America and Asia, distributes over 100,000 metal products, and achieved record sales of $5.74 billion and net income of $354.5 million in 2006.