Download to read offline

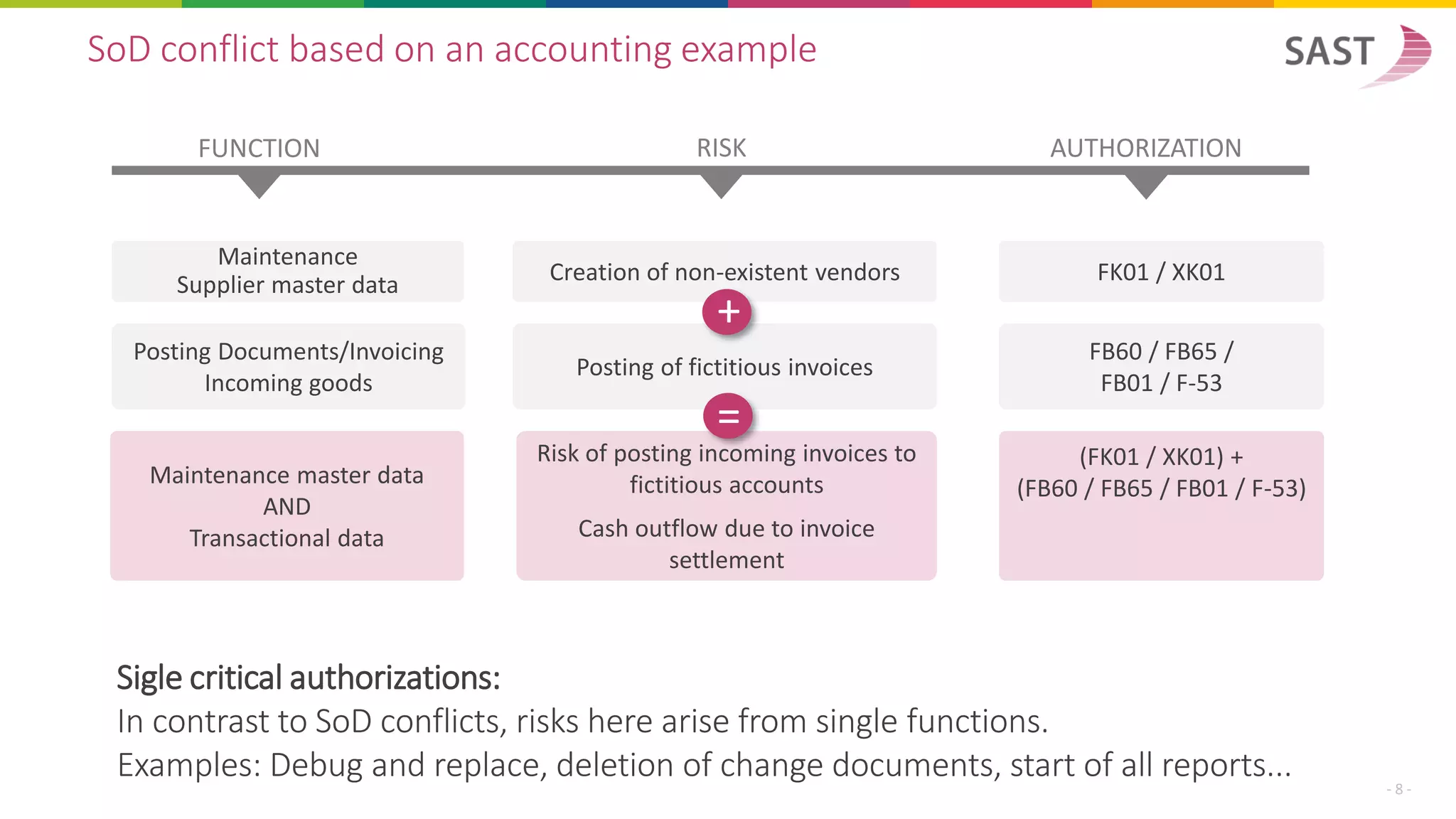

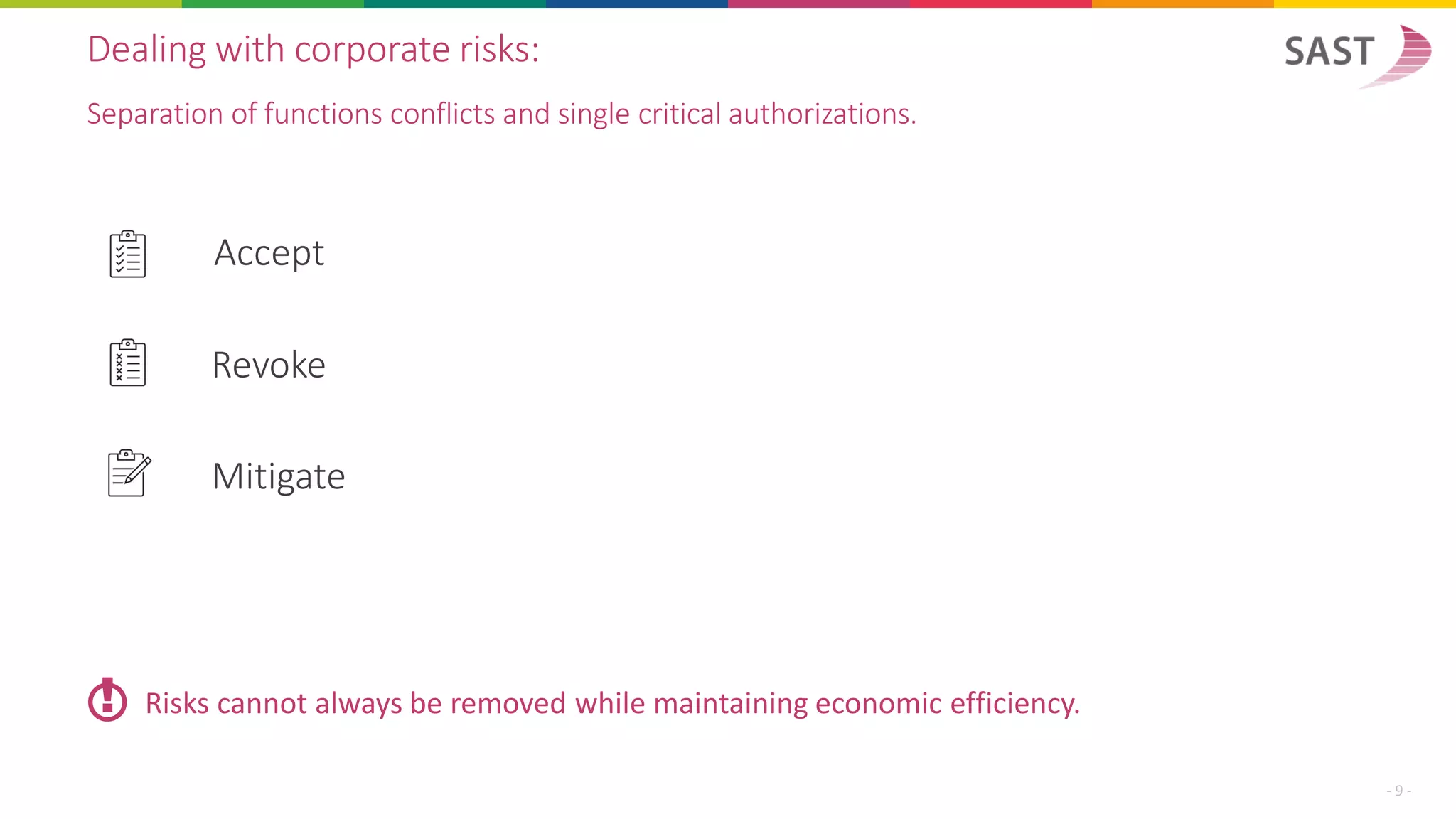

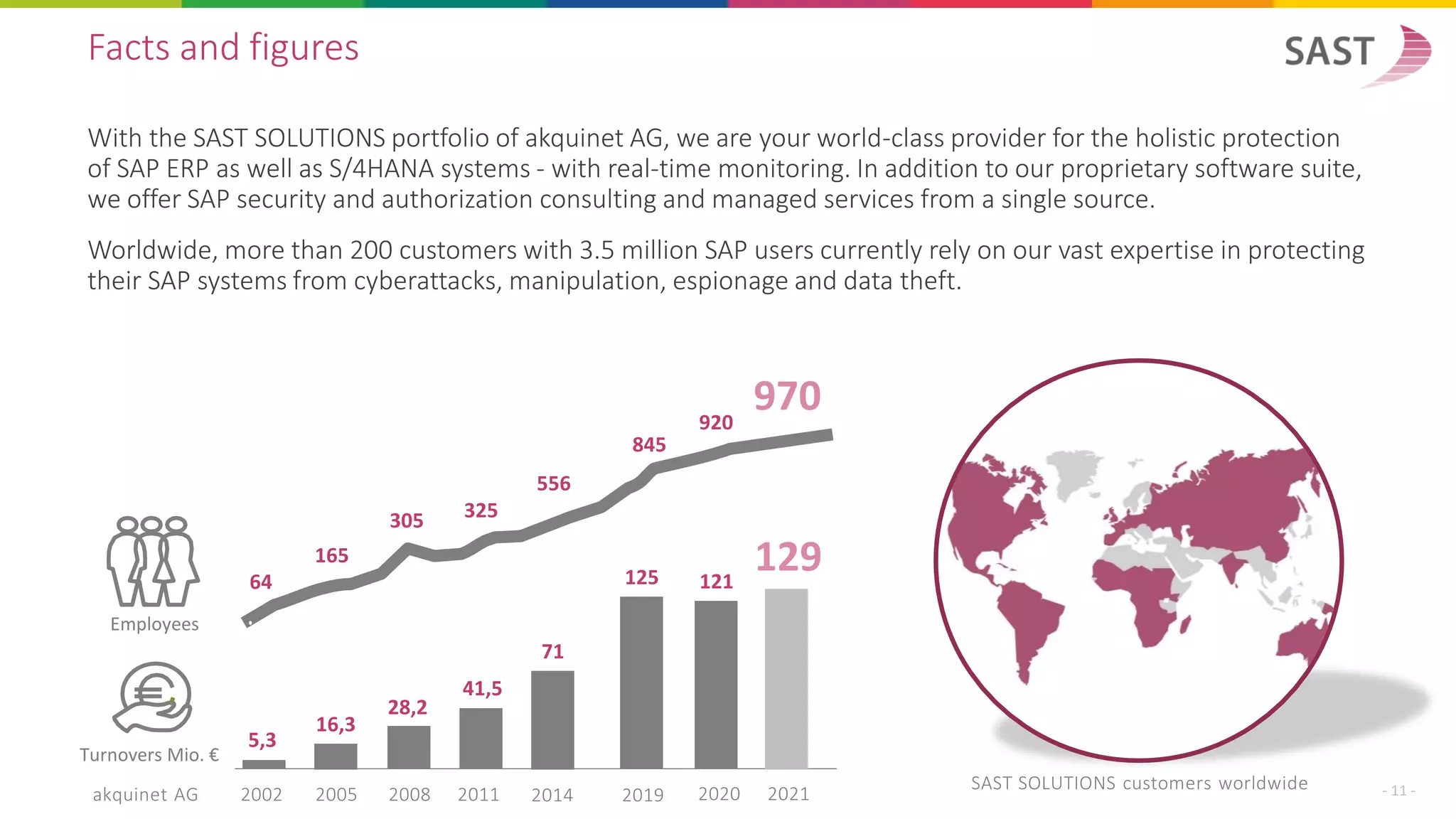

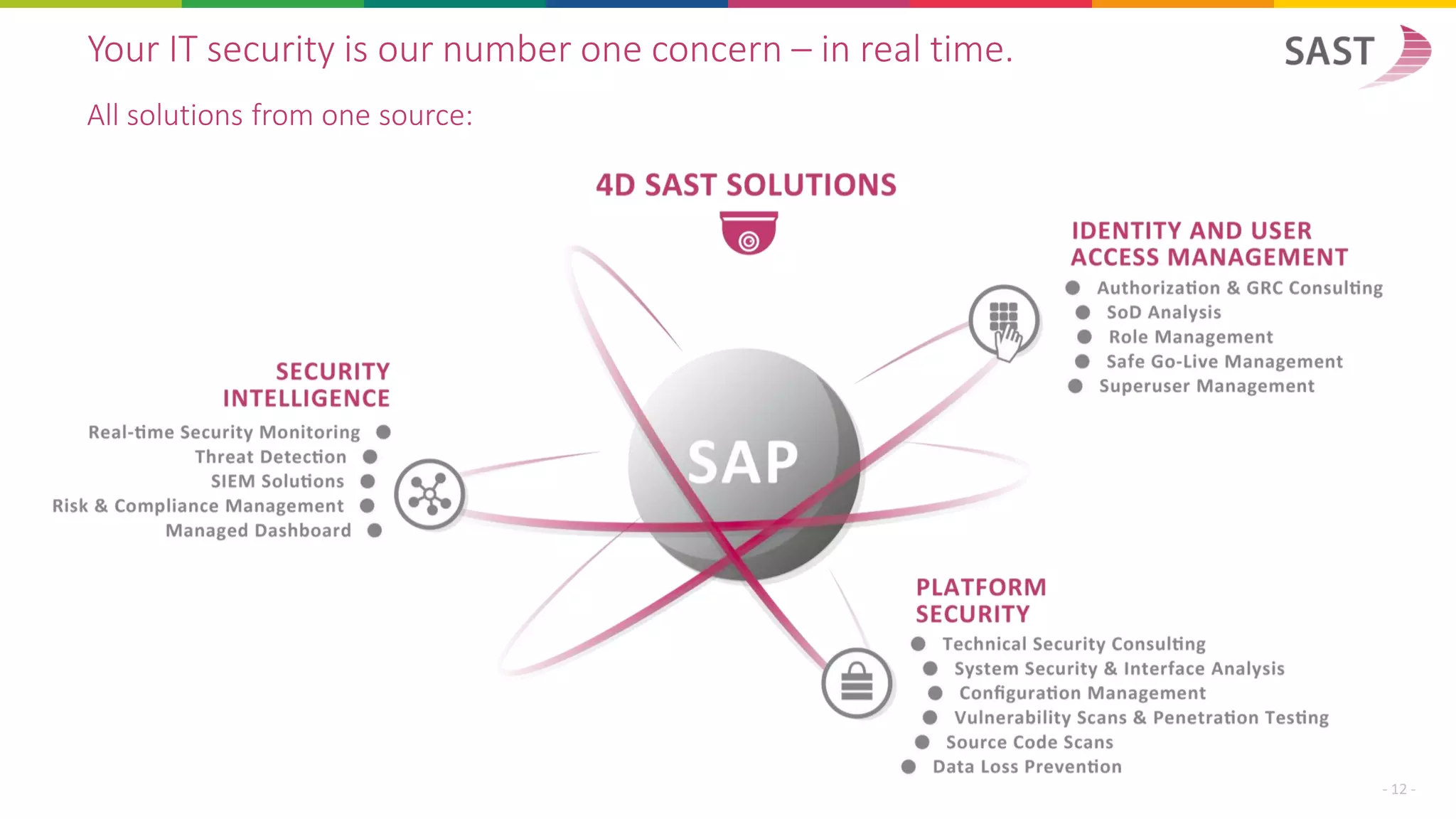

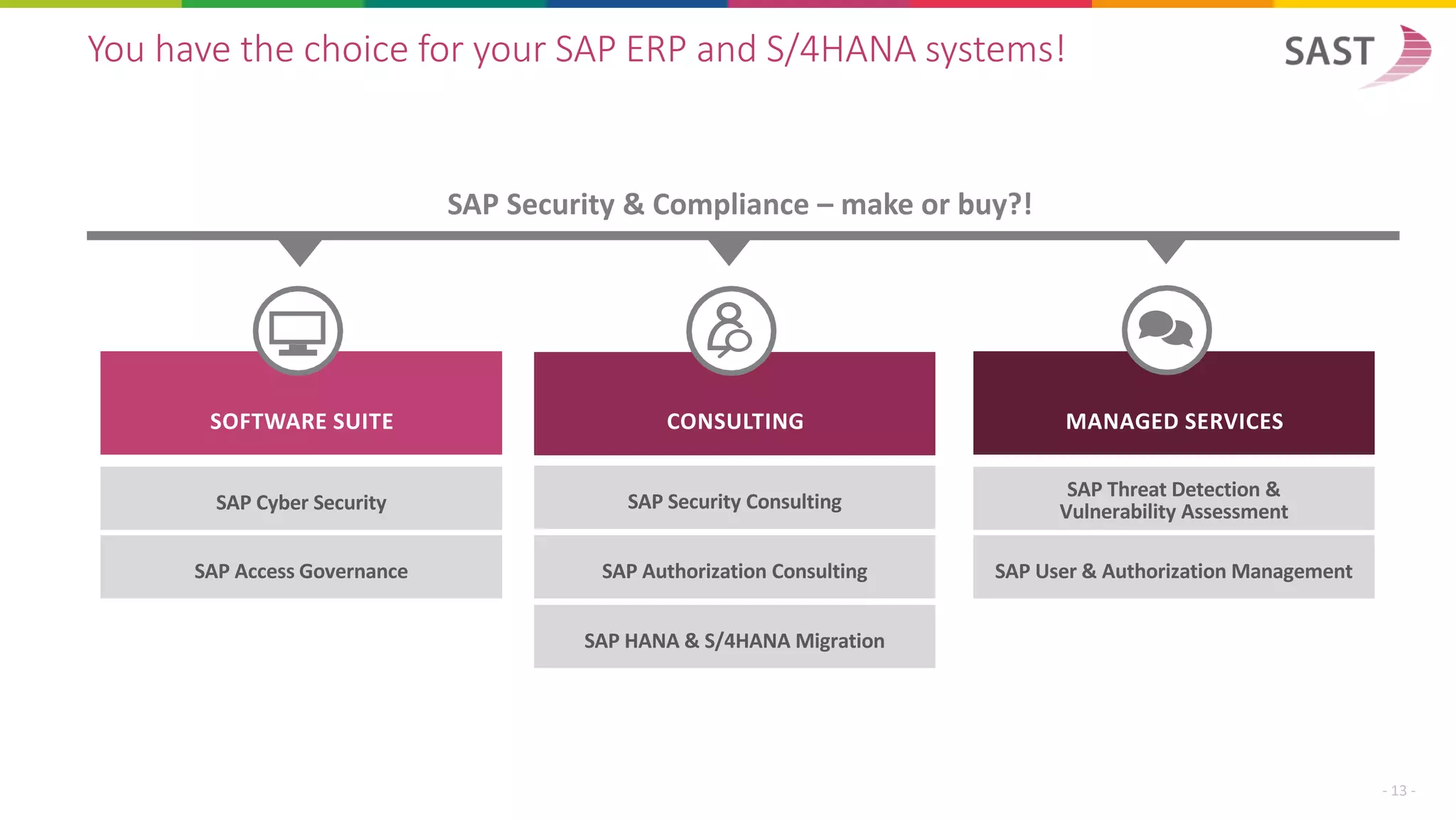

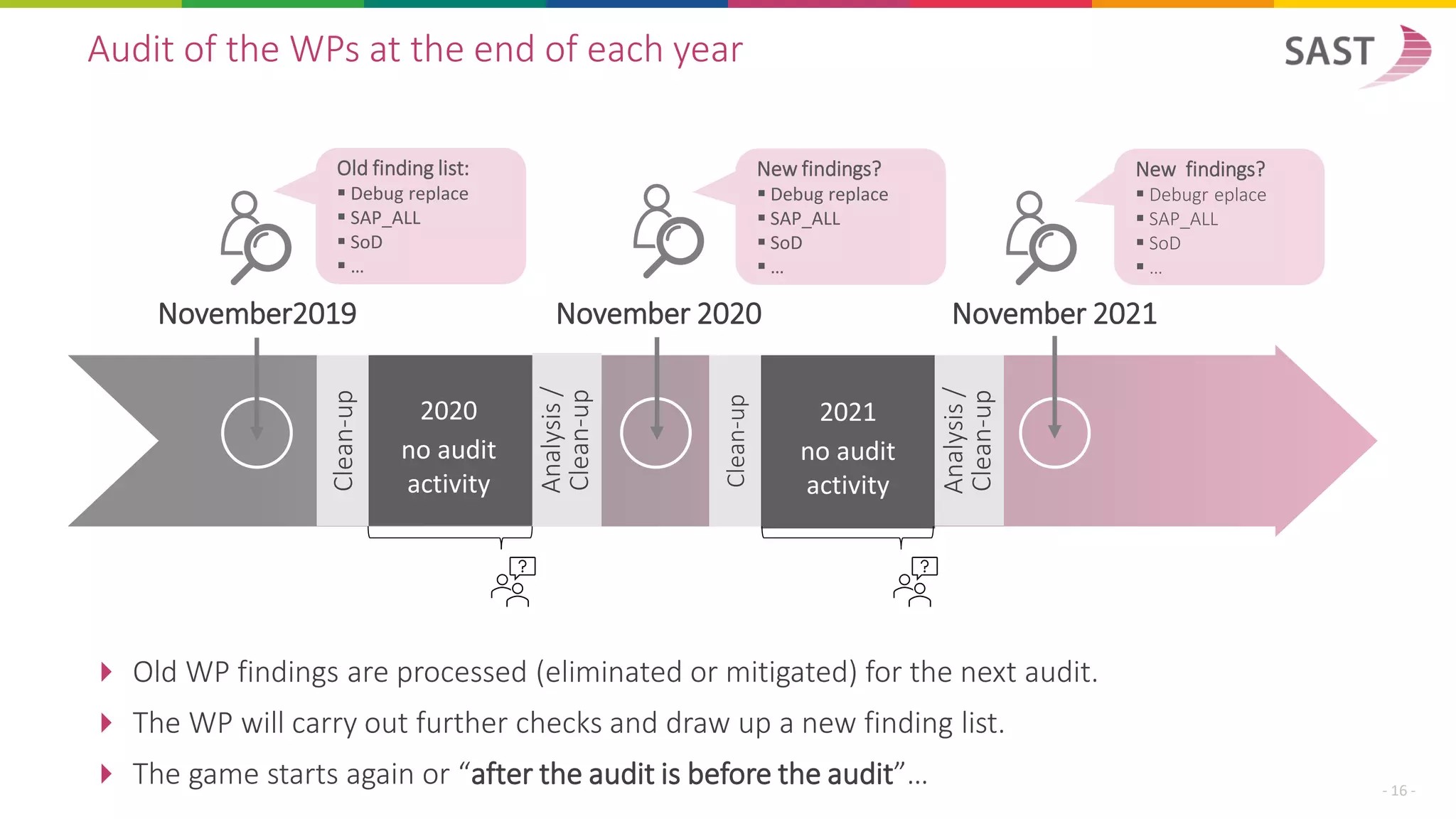

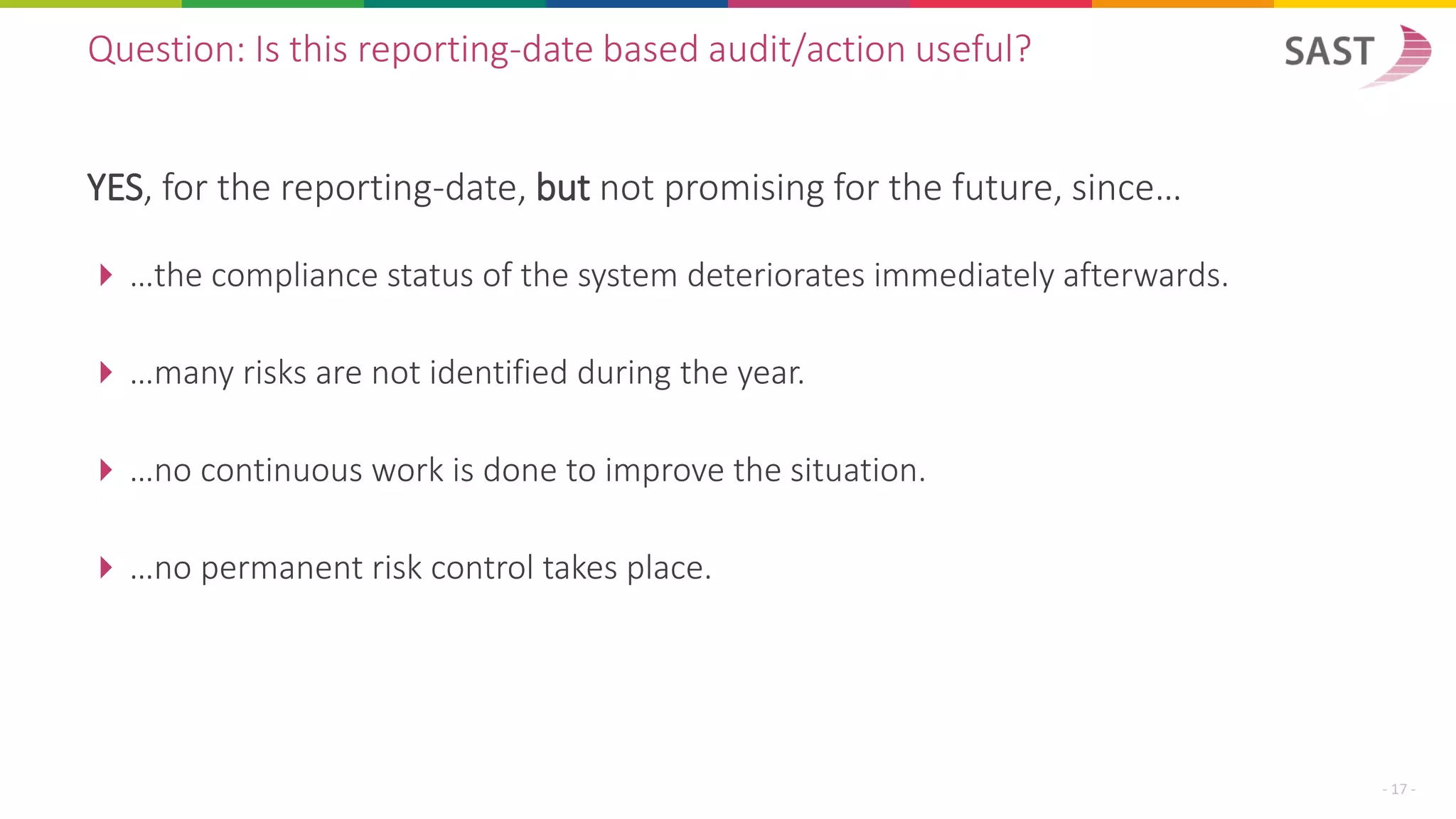

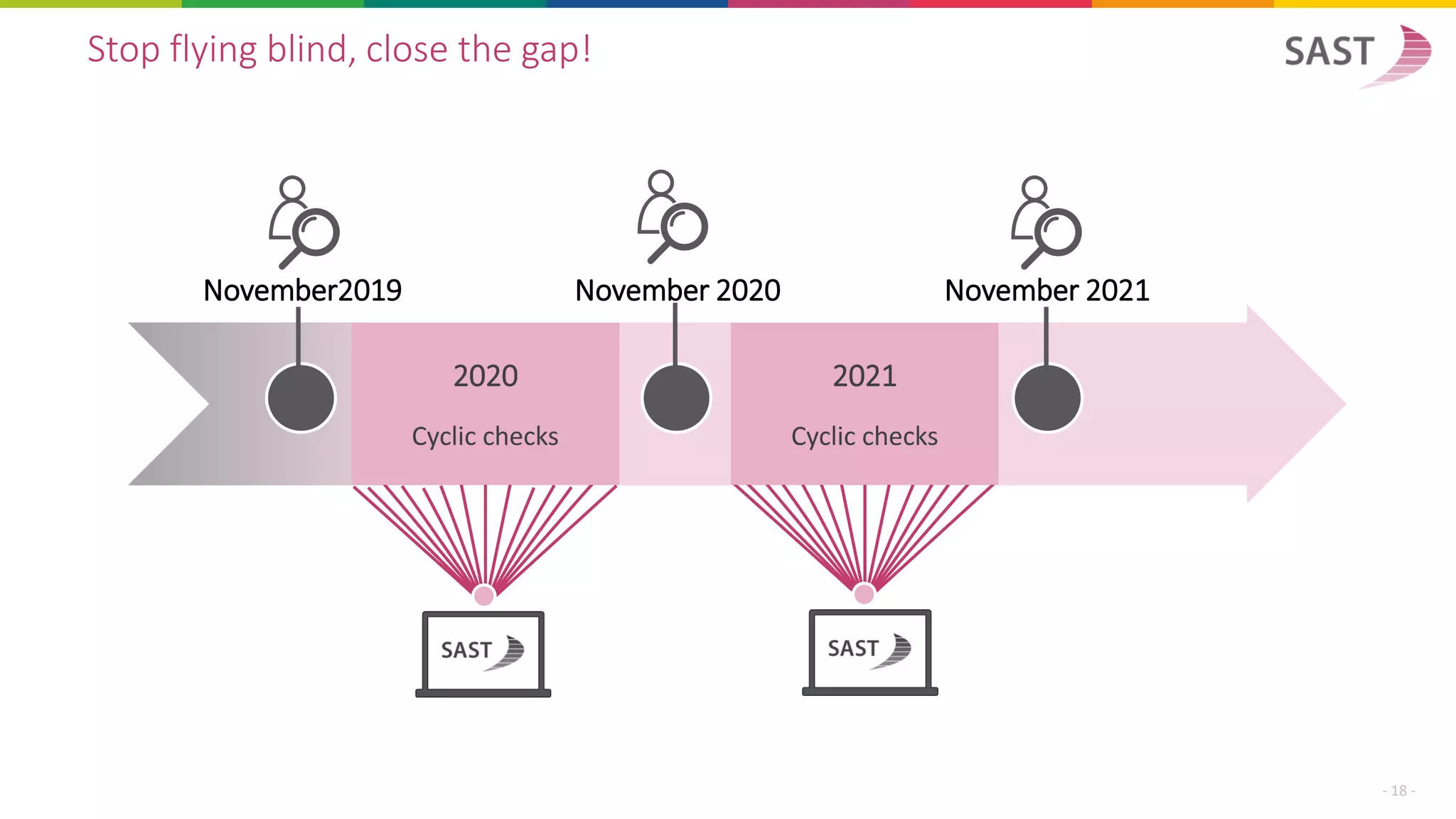

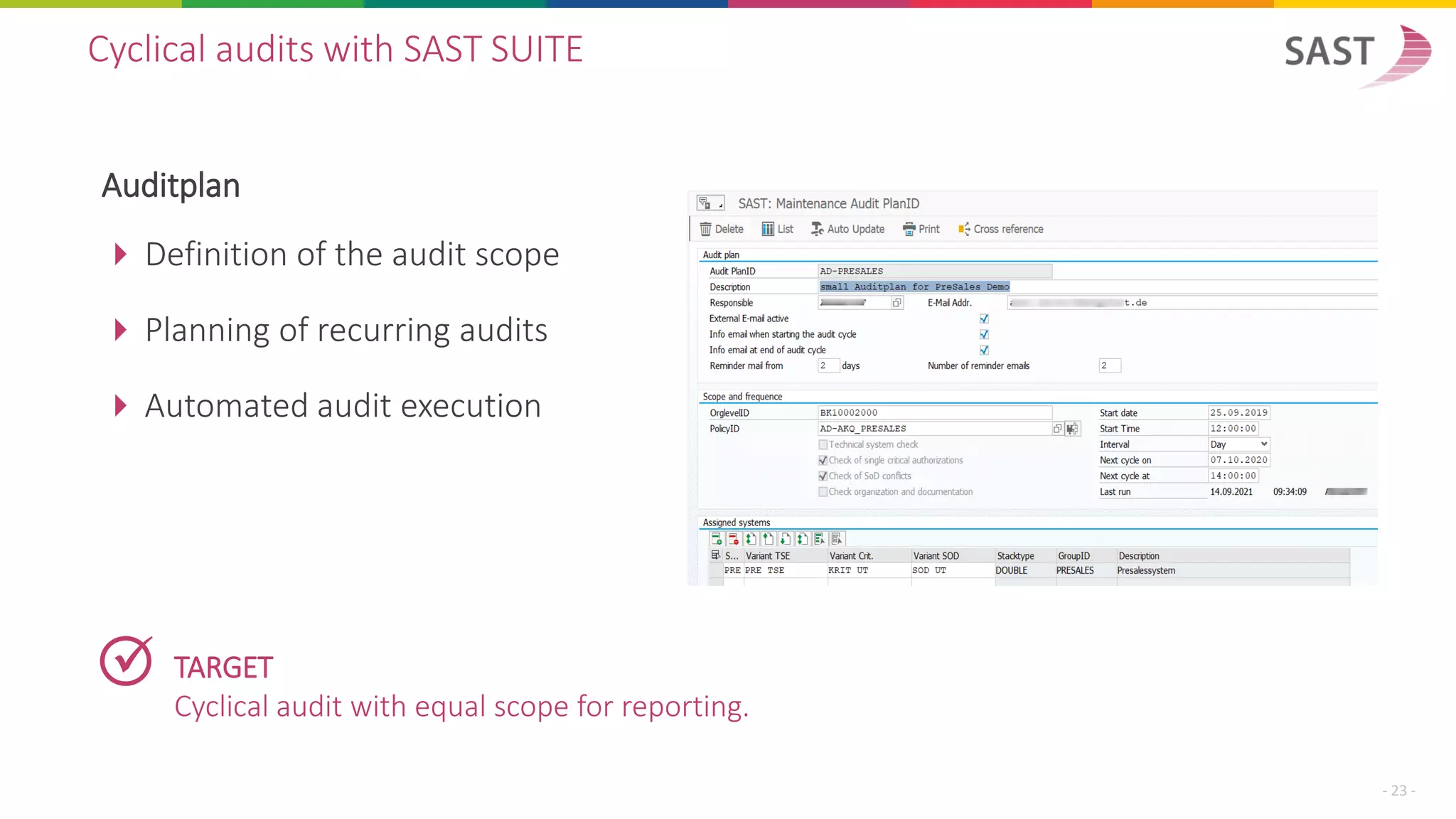

The document outlines the importance of maintaining a robust audit process for IT systems, particularly in relation to SAP environments, highlighting key risks such as segregation of duties (SoD) conflicts and single critical authorizations. It emphasizes a proactive approach to risk management through regular monitoring and the use of the SAST suite for effective compliance and security solutions. The authors advocate for continuous improvement post-audit and the necessity for a holistic strategy to manage risks effectively within SAP systems.

![How Linde identifies and tracks security incidents in its SAP systems. [Webinar]](https://cdn.slidesharecdn.com/ss_thumbnails/linde-210309081132-thumbnail.jpg?width=640&height=640&fit=bounds)

![SAST Safe Go-Live Management for SAP authorizations [Webinar]](https://cdn.slidesharecdn.com/ss_thumbnails/webinarsast-safe-go-live-mgmt1805en-181210174817-thumbnail.jpg?width=640&height=640&fit=bounds)

![SAST Code Security Advisor for SAP [Webinar]](https://cdn.slidesharecdn.com/ss_thumbnails/webinarsast-csa1810en-181210183707-thumbnail.jpg?width=640&height=640&fit=bounds)

![SAST Interface Management for SAP systems [Webinar]](https://cdn.slidesharecdn.com/ss_thumbnails/webinarsast-interface-mgmt1806en-181210180739-thumbnail.jpg?width=640&height=640&fit=bounds)

![Why your works council has nothing to fear from SAP security. [Webinar]](https://cdn.slidesharecdn.com/ss_thumbnails/sastwebinarsap-securityundbetriebsrte210810en-210818084506-thumbnail.jpg?width=640&height=640&fit=bounds)

![Towards new shores with cross-system SoD analyses. [Webinar]](https://cdn.slidesharecdn.com/ss_thumbnails/webinarsodanalysenen-200721061650-thumbnail.jpg?width=640&height=640&fit=bounds)

![SAST Managed Services for SAP [Webinar]](https://cdn.slidesharecdn.com/ss_thumbnails/webinarsast-managedservices1803en-181210161559-thumbnail.jpg?width=640&height=640&fit=bounds)

![SAST Threat Detection for SAP [Webinar]](https://cdn.slidesharecdn.com/ss_thumbnails/webinarsast-threatdetection1811en-181210185759-thumbnail.jpg?width=640&height=640&fit=bounds)

![Cyber attacks on your SAP S/4HANA systems? So you can stay relaxed. [Webinar]](https://cdn.slidesharecdn.com/ss_thumbnails/sastwebinarcyberattacks-on-s4hana-systems-200624093103-thumbnail.jpg?width=640&height=640&fit=bounds)

![How can managed services improve your SAP security and compliance? [Webinar]](https://cdn.slidesharecdn.com/ss_thumbnails/sastwebinarmanagedservice-cases20mrzen-200325121702-thumbnail.jpg?width=640&height=640&fit=bounds)

![Cut your costs: Deactivate inactive users & reduce sap license fees. [Webinar]](https://cdn.slidesharecdn.com/ss_thumbnails/sastwebinarlizenzkostenen-210518133555-thumbnail.jpg?width=640&height=640&fit=bounds)

![Tips for the secure conversion of your SAP ERP roles to S/4HANA. [Webinar]](https://cdn.slidesharecdn.com/ss_thumbnails/sastwebinarroleconversionserviceen-200825062633-thumbnail.jpg?width=640&height=640&fit=bounds)