Rbi ppt

•Download as PPTX, PDF•

0 likes•774 views

The Reserve Bank of India (RBI) made several changes to monetary policy measures in 2011-12, including hiking repo and reverse repo rates, adjusting reserve requirements, and revising economic projections. Specifically, the RBI hiked repo rates by 0.5% and then later by 0.25%, increased the cash reserve ratio by 0.5%, and revised GDP growth projections downward from 8% to 7% while inflation projections rose from 6% to 7%. Throughout 2011-12, the RBI made adjustments to key policy rates and reserve requirements in response to economic conditions while revising its forecasts for GDP growth and inflation.

Recommended

Recommended

More Related Content

Viewers also liked

Similar to Rbi ppt

Similar to Rbi ppt (20)

More from SRI GANESH

More from SRI GANESH (18)

Rbi ppt

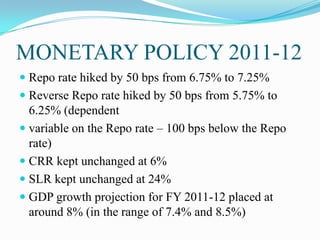

- 1. MONETARY POLICY 2011-12 Repo rate hiked by 50 bps from 6.75% to 7.25% Reverse Repo rate hiked by 50 bps from 5.75% to 6.25% (dependent variable on the Repo rate – 100 bps below the Repo rate) CRR kept unchanged at 6% SLR kept unchanged at 24% GDP growth projection for FY 2011-12 placed at around 8% (in the range of 7.4% and 8.5%)

- 2. CONT- FY 2011-12 March end WPI inflation baseline projection placed at 6% with an upward bias M3 growth projected at 16%, deposit growth at 17% and non-food credit growth at 19% Bank rate kept unchanged at 6%. MSF introduced at 1% above the Repo rate (8.25%) LAF corridor width set at 200 bps (with base at reverse repo – 6.25% & ceiling at MSF – 8.25%) MP 2011-12.docx

- 3. FIRST QUARTERLY REVIEW Increase / (Decrease) At present since March 2010 Repo Rate .5% 8%. Reverse Repo Rate .5% 7% Cash Reserve Ratio Unchanged 6%. Statutory Liquidity Unchanged 24% Ratio Bank Rate Unchanged 6%

- 4. KEY FEATURES GDP growth projection for FY 2011-12 kept unchanged at around 8% Inflation projection for March end FY 2011-12 revised upwards to 7% from 6%

- 5. SECOND QUARTERLY REVIEW Increase / (Decrease) At present Repo Rate .25% 8.5% Reverse Repo Rate .25%. 7.5% Cash Reserve Ratio Unchanged 6% Statutory Liquidity Unchanged 24% Ratio Bank Rate Unchanged 6%

- 6. KEY FEATURES RBI lowered the growth forecast for 2011-12 from 8% to 7.6% (in line with our expectations) Inflation forecast is kept at 7% by Mar-12 end. Money supply and Credit growth maintained at 15.5% and 18% respectively Depreciation of the rupee has emerged as another risk for inflation. Indian economy continued to face suppressed inflation as prices are administered in petroleum sector.

- 8. Increase / (Decrease) At present Repo Rate Unchanged 8.50% Reverse Repo Unchanged 7.50% Rate Cash Reserve .50% 5.50% Ratio Statutory Unchanged 24.00% Liquidity Ratio Bank Rate Unchanged 6.00%

- 9. KEY FEATURES The drop in November 2011 WPI inflation to 9.11%, mainly due to softening in food inflation (4.35% for the week ended December 3, 2011) GDP growth rate has fallen to 6.9% from 7.7%(expected in Q2) Due to sharp moderation in industrial growth to -5.1% The fiscal deficit at 74.4% of budgeted 2011-12 was significantly higher than 42.6% in 2010-11

- 10. CONT- FDs (Fixed Deposits) are offering interest in the range of 7.25% - 9.40% p.a. Projection of GDP growth for 2011-12 is revised downwards from 7.6% to 7%. In reducing the CRR,INR 320 bn of primary liquidity will be injected into the banking system

- 12. RBI projections in three reviews in 2011-12 Table 1: RBI Projections in Monetary Reviews (in %) May-11 Jul 11 Oct-11 Growth (2011-12) 8 8 7.6 Inflation (Mar-12) 6 7 7 M3 (Mar-12) 16 15.5 15.5 Deposit (Mar-12) 17 - - Credit (Mar-12) 19 18 18

- 14. PRESENTATION BY