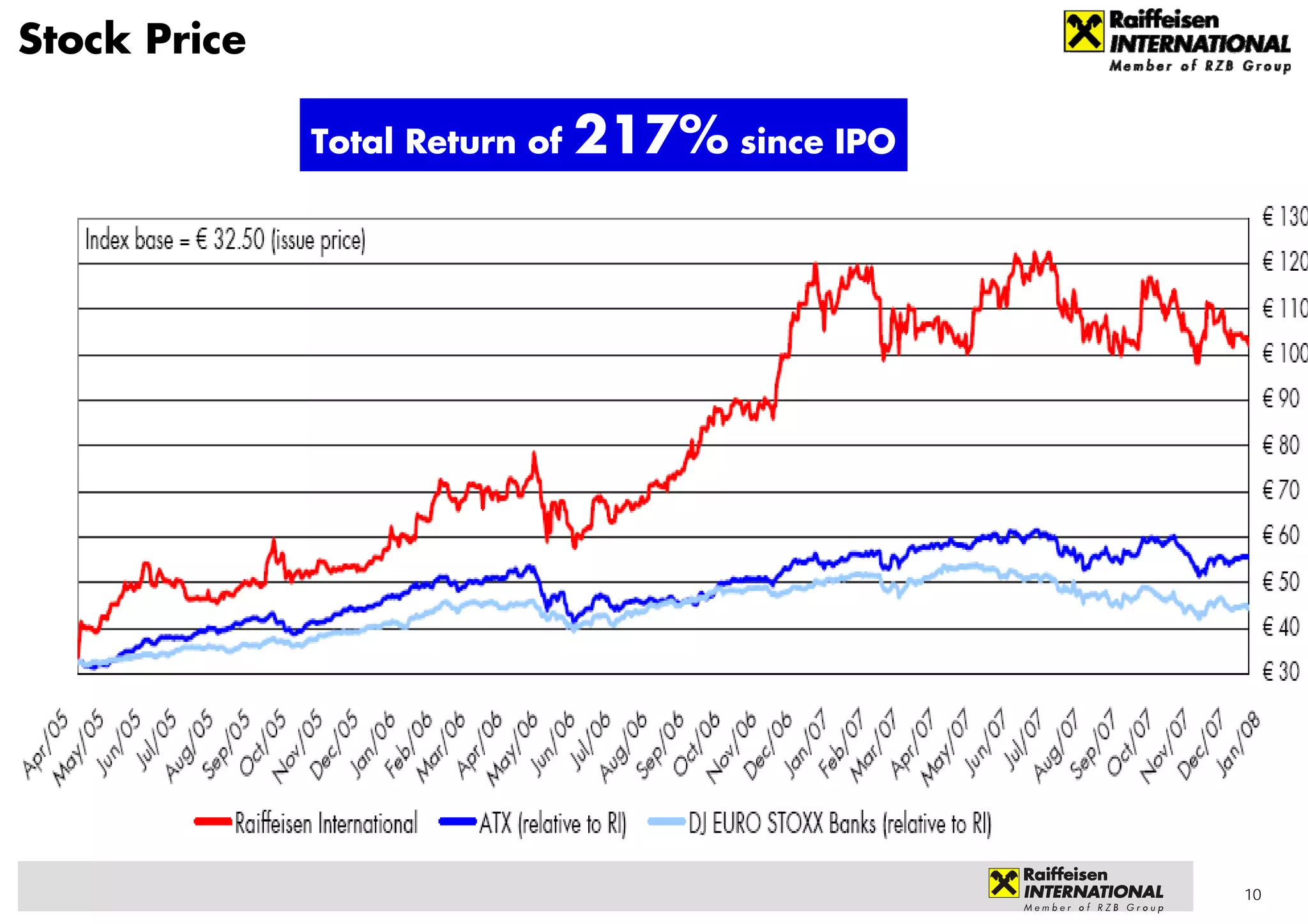

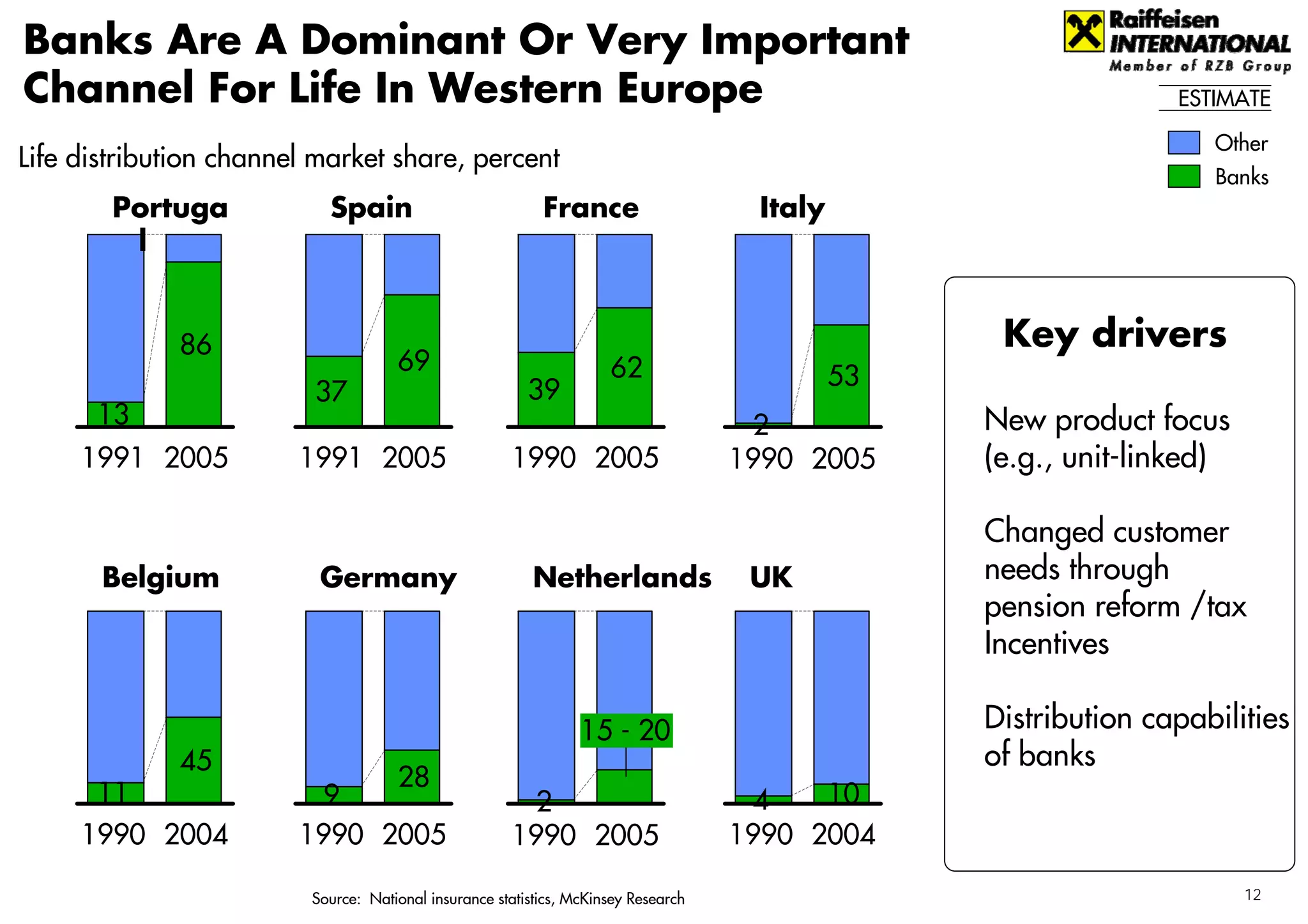

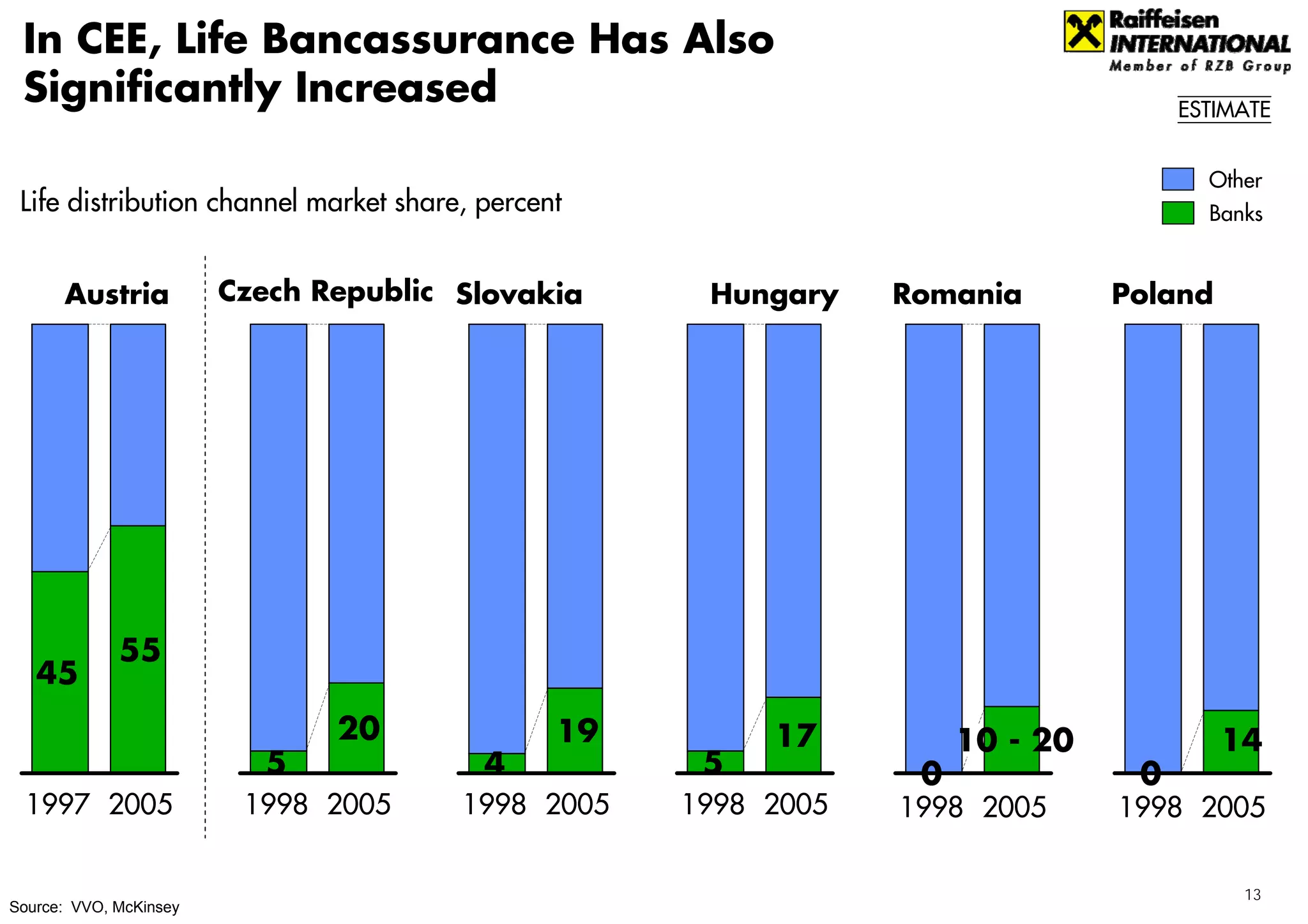

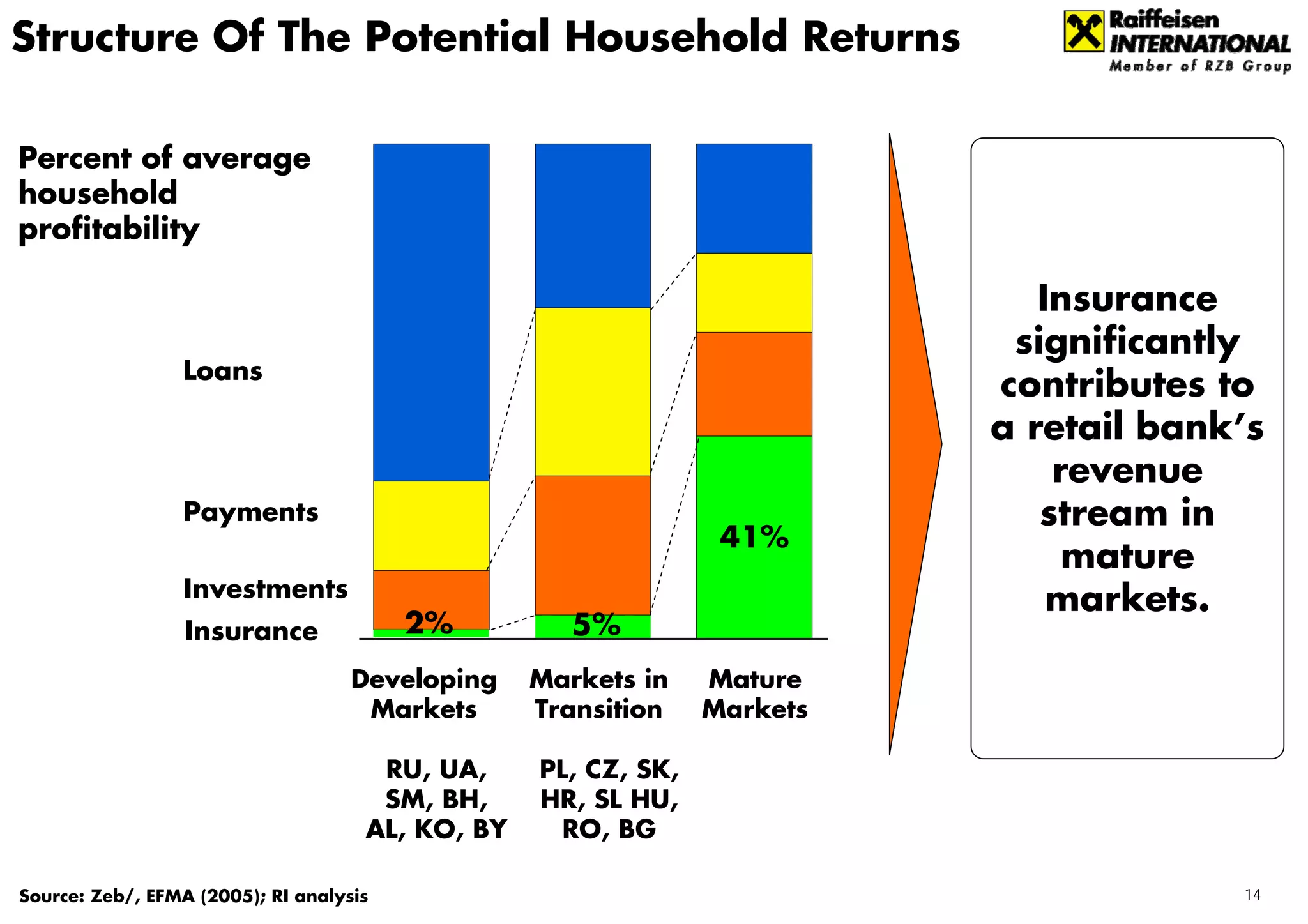

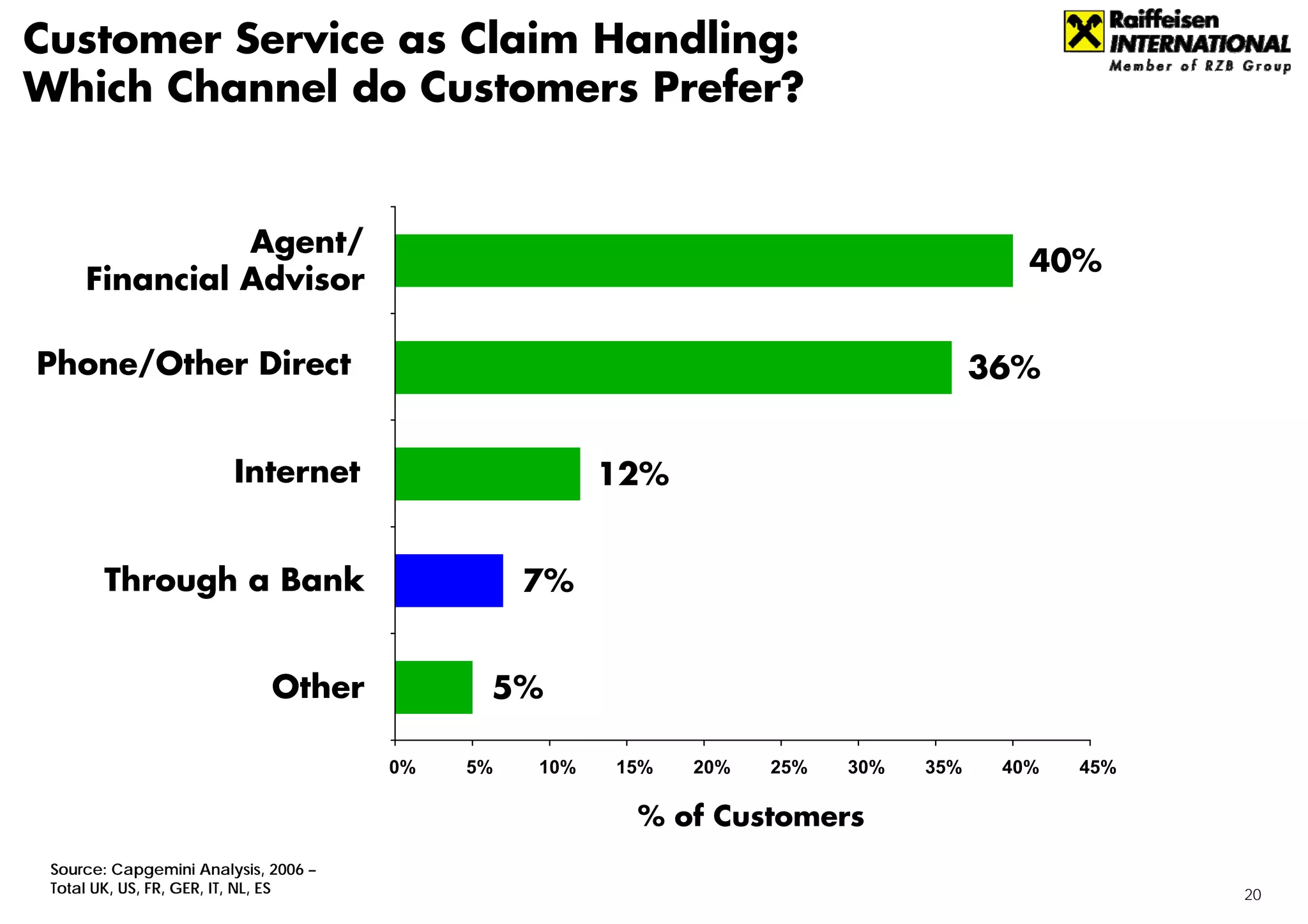

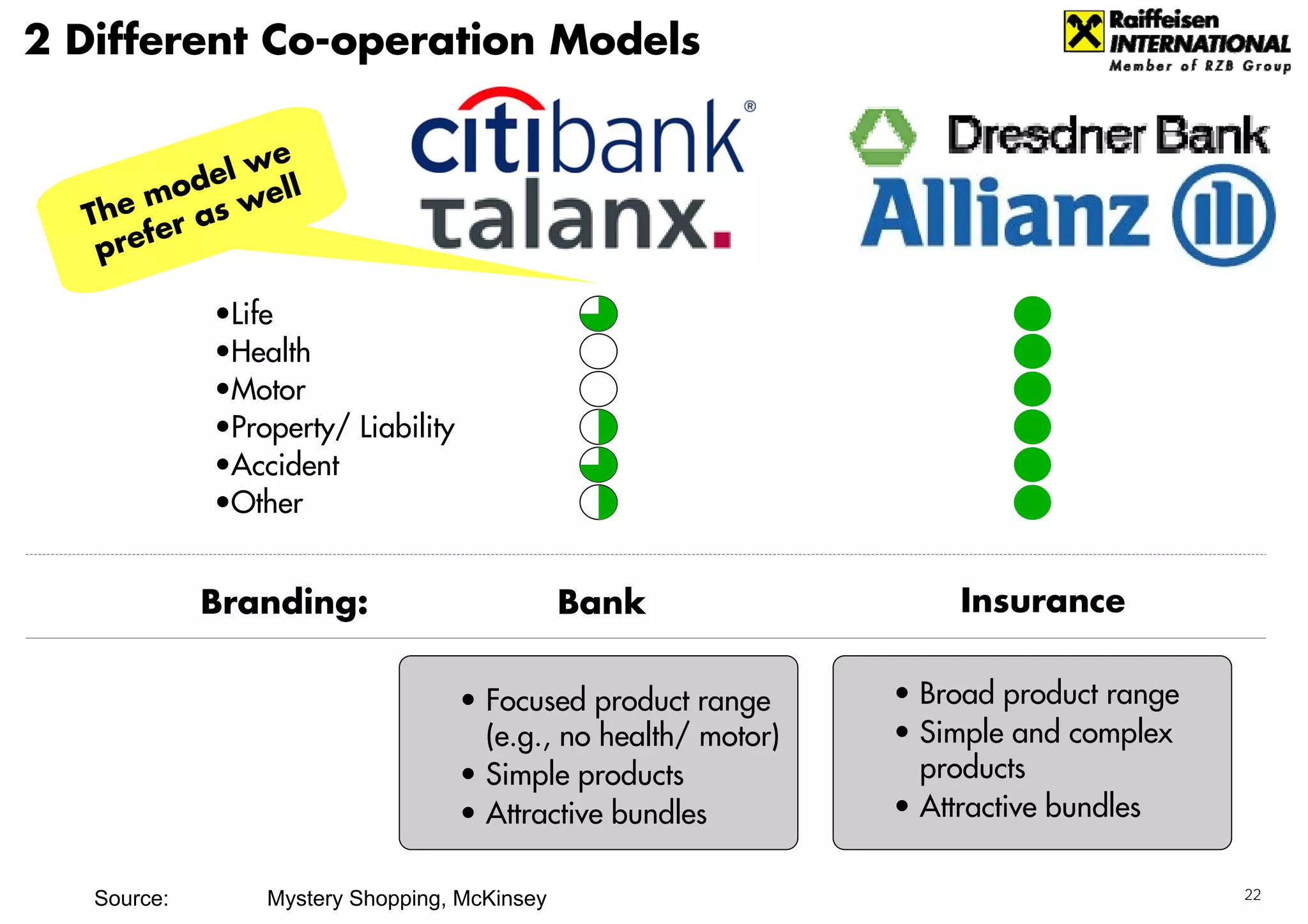

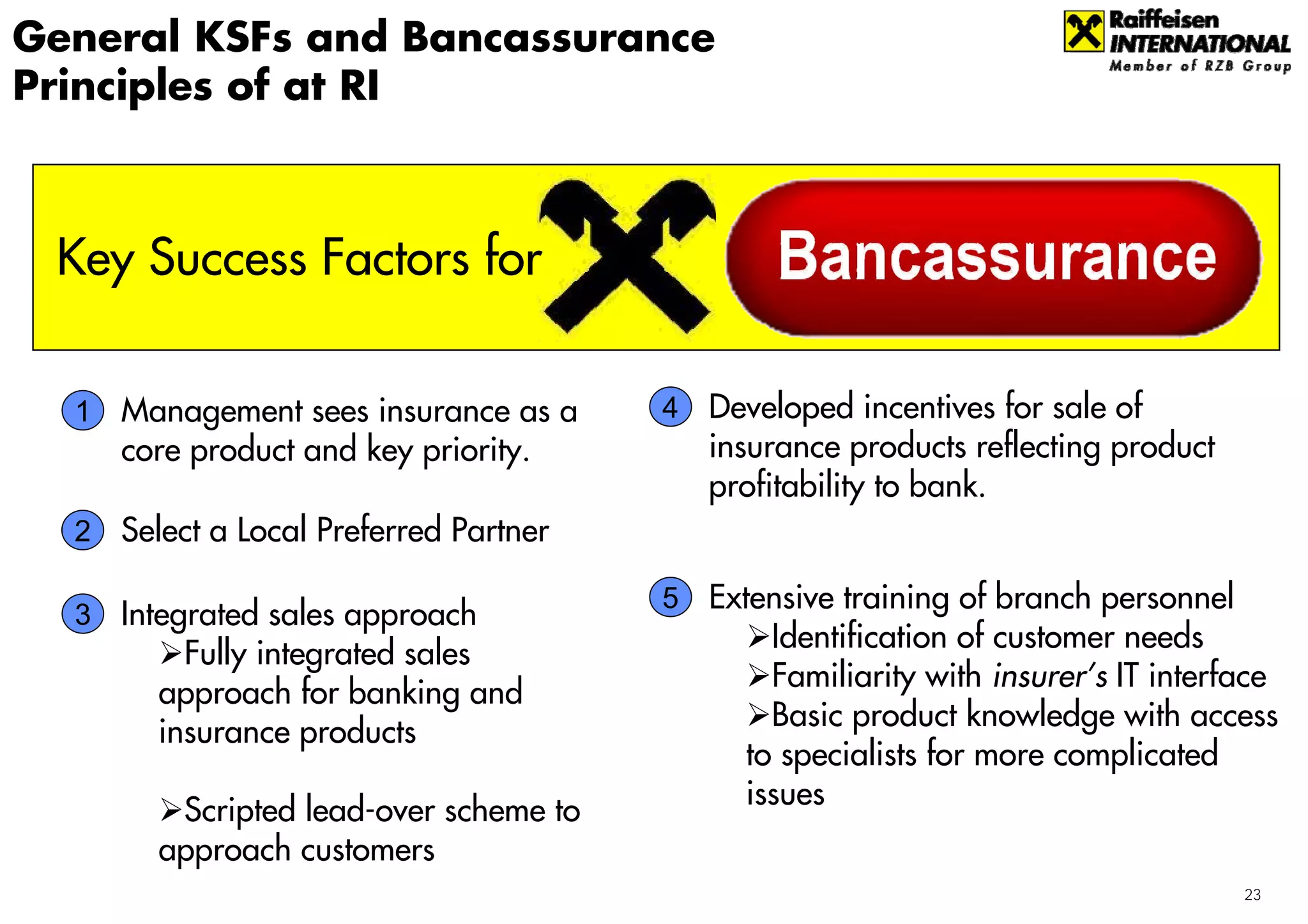

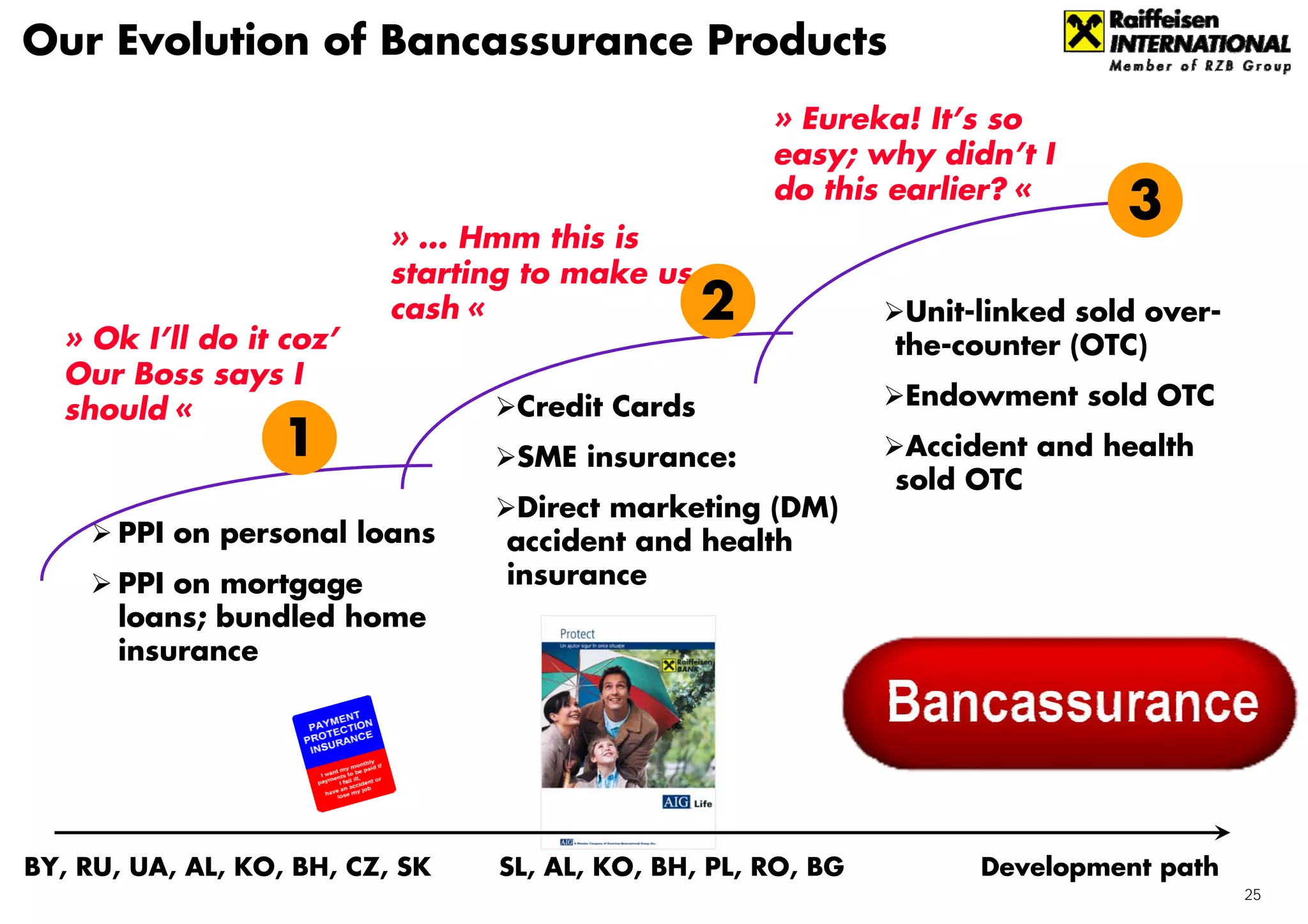

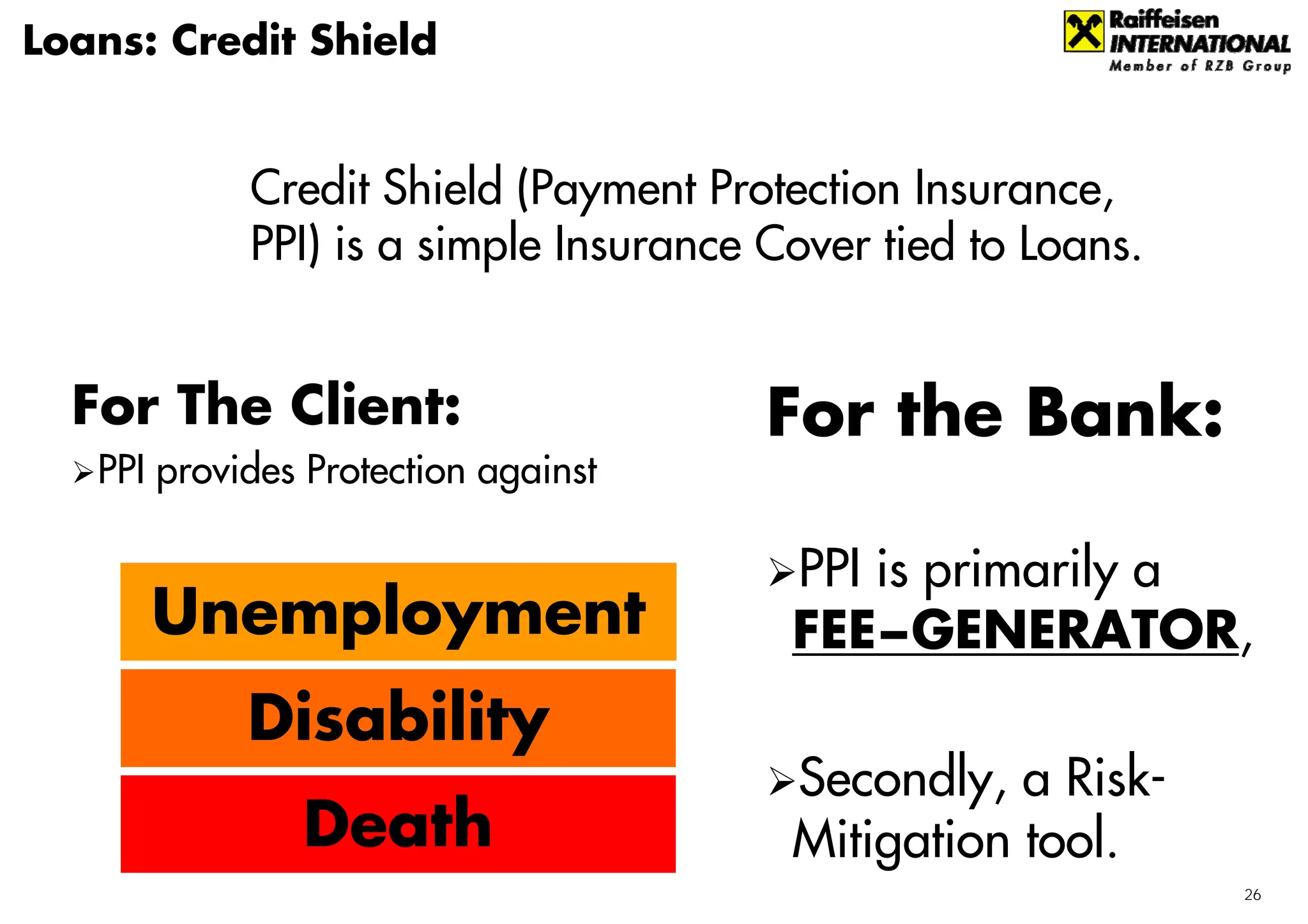

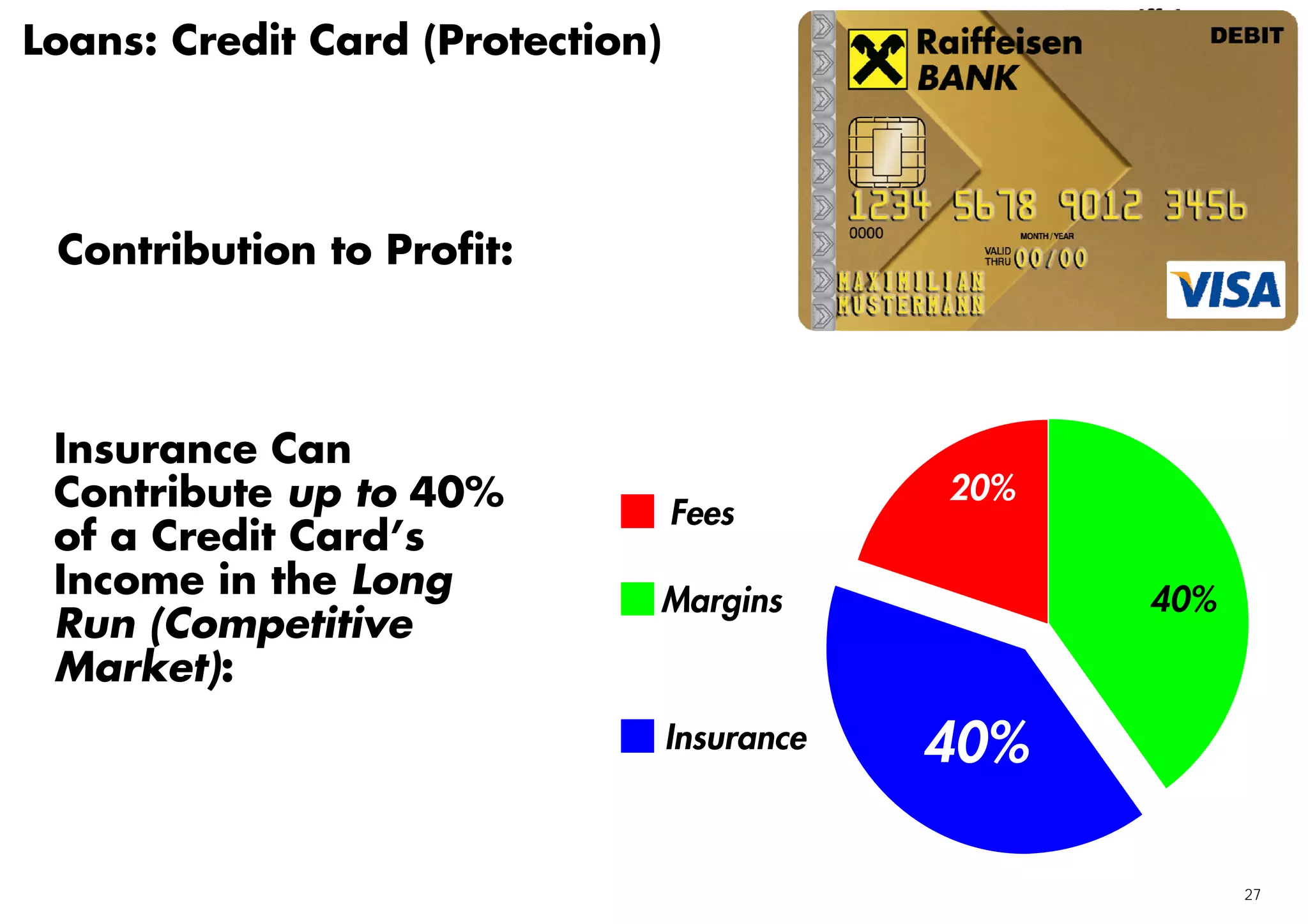

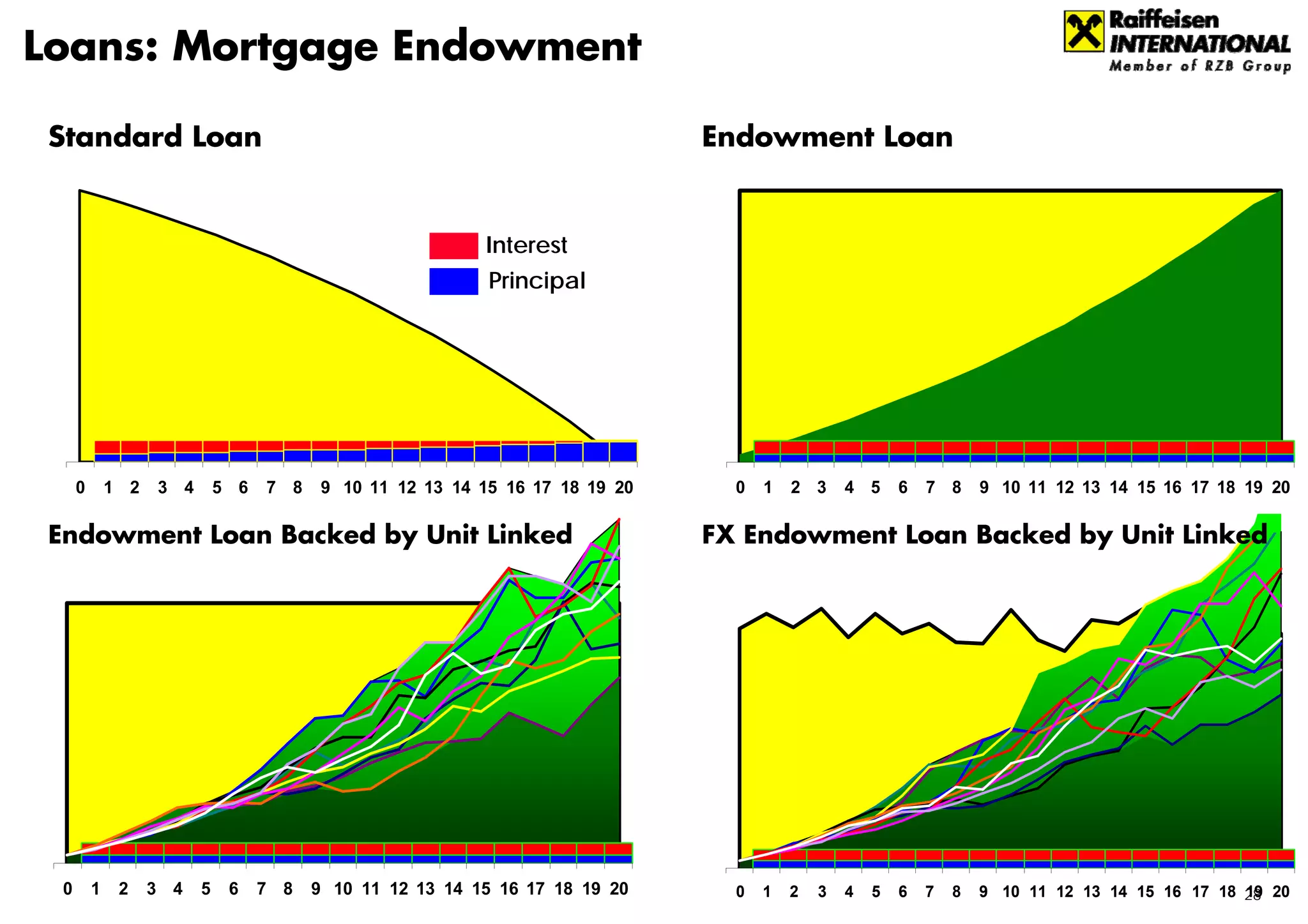

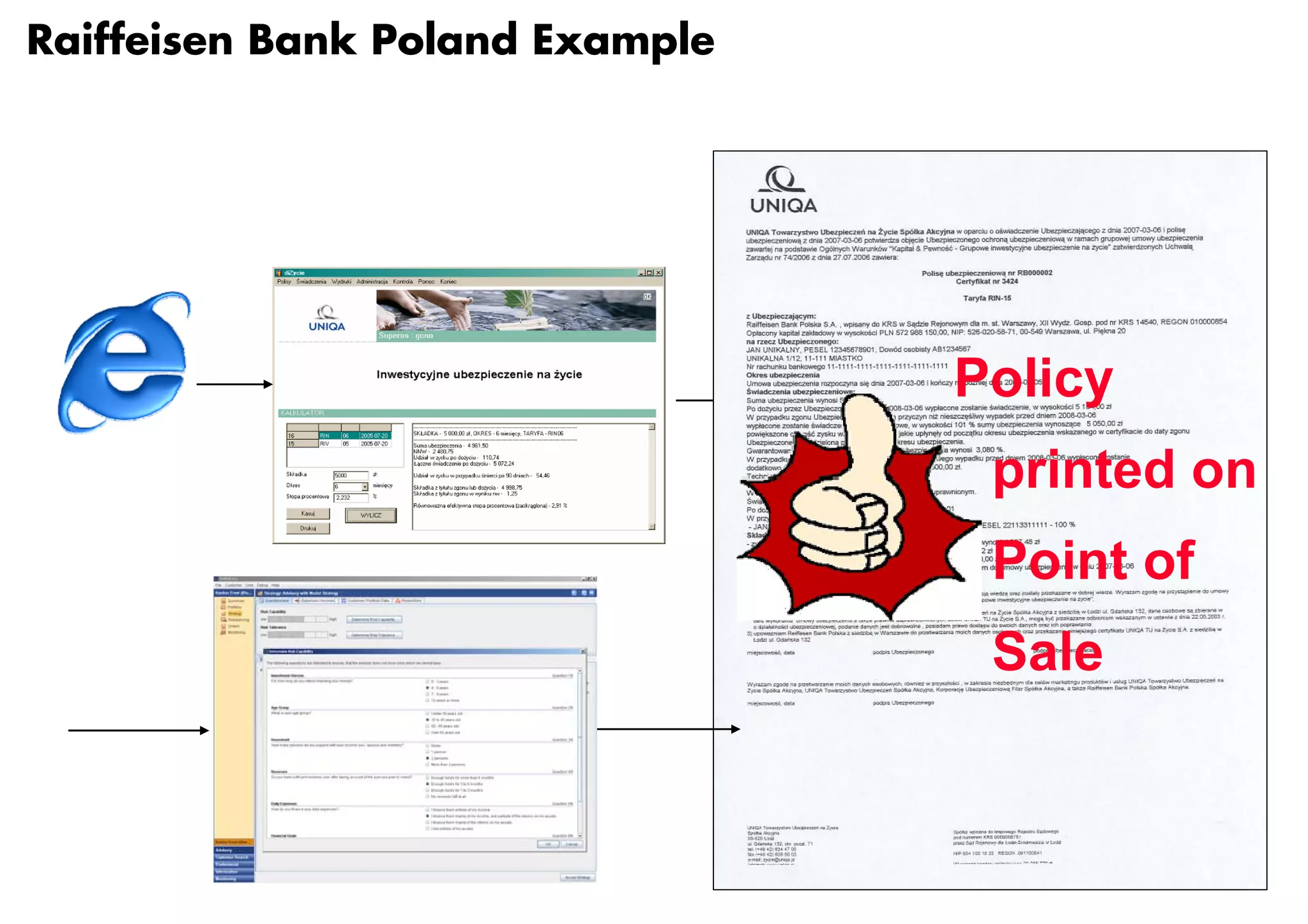

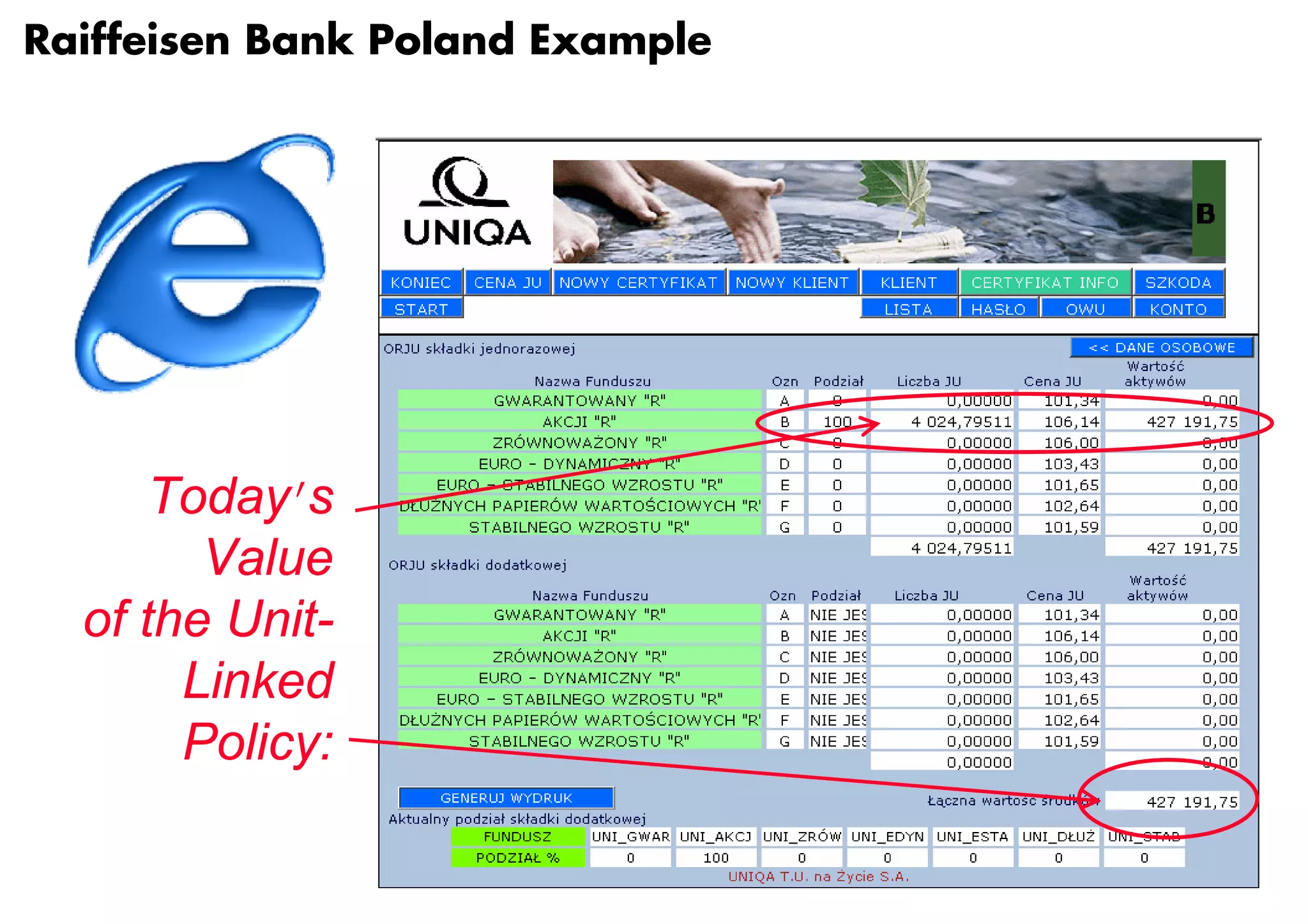

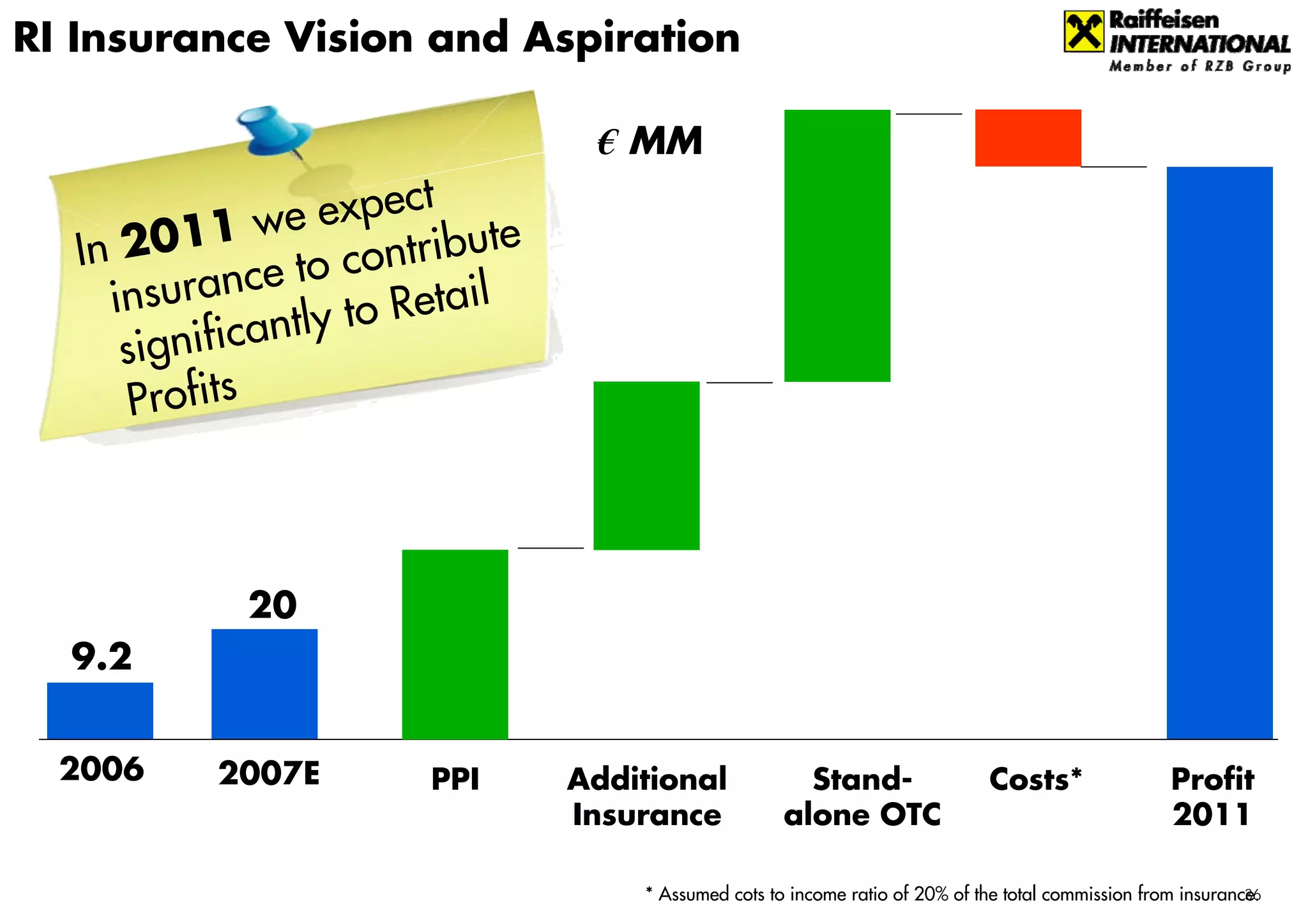

The document discusses bancassurance opportunities in Central and Eastern Europe (CEE) for Raiffeisen International. It provides an overview of Raiffeisen International's network and growth, analyzes insurance market environments and customer preferences in CEE, and outlines Raiffeisen's bancassurance setup including product ranges and expectations to significantly contribute to profits from insurance by 2011.

![[Challenge:Future] The creative change of EE economies](https://cdn.slidesharecdn.com/ss_thumbnails/challengefuture-the-creative-change-of-ee-economies1005-130424032207-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)