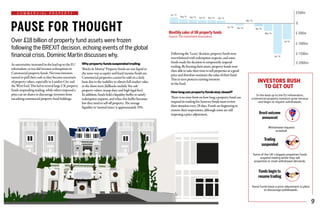

This document provides a market review and outlook from Walker Crips in October 2016 following the Brexit vote. It discusses the resilience of markets in the short-term despite uncertainty around Brexit. It notes the expansion of Walker Crips' assets under management and efforts to prevent fraud. Various economic indicators and sectors in the UK, Europe and US are also reviewed, with the FTSE 100 breaking 7,000 but uncertainties remaining around inflation, interest rates and European banks.