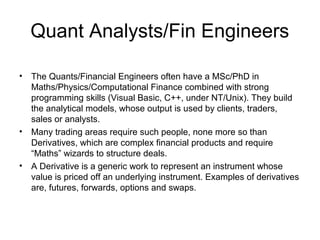

To work as a quantitative analyst on the buy side, skills in mathematics, programming, statistics, and financial modeling are essential. Quantitative analysts build analytical models to value financial instruments and manage risk, requiring expertise in areas like derivatives pricing, portfolio construction, and statistical analysis. Strong problem-solving abilities and communication skills are also important to effectively analyze complex problems and interact with other professionals.